【Macroeconomic Weekly Report┃4 Alpha】Market pressure increases, waiting for the implementation of reciprocal tariffs?

The risk of stagflation in the United States is rising: Q1 GDP is expected to decline by 1.8%, with unemployment rates rising in 290 out of 387 metropolitan areas, highlighting the stickiness of PCE inflation. Market risk aversion dominates, with gold rising / U.S. stocks under pressure, and credit spreads widening, exacerbating recession concerns. The decision on reciprocal tariffs on April 2 may become a short-term indicator; it is recommended to allocate gold and U.S. Treasuries to hedge against volatility, and to reduce holdings in technology and crypto assets on rallies.

The risk of stagflation in the United States is rising: Q1 GDP is expected to decline by 1.8%, with unemployment rates rising in 290 out of 387 metropolitan areas, highlighting the stickiness of PCE inflation. Market risk aversion dominates, with gold rising / U.S. stocks under pressure, and credit spreads widening, exacerbating recession concerns. The decision on reciprocal tariffs on April 2 may become a short-term indicator; it is recommended to allocate gold and U.S. Treasuries to hedge against volatility, and to reduce holdings in technology and crypto assets on rallies.4 Alpha Core Views:

I. Macroeconomic Review This Week

1. Market Overview

- Market sentiment weakened in the second half of the week due to Trump's tough stance on auto tariffs.

- The crypto market momentum is weak, with liquidity and macro uncertainty persisting, as the market awaits the implementation of reciprocal tariffs.

- Gold continues its upward trend, while U.S. stocks, cryptocurrencies, and commodity markets show weak performance.

2. Economic Data Analysis

- GDPNow predicts Q1 GDP at -1.8%, indicating a trend of economic weakening.

- The labor market shows clear signs of fatigue, with rising unemployment rates in 290 metropolitan areas and an increase in continued unemployment claims.

- February PCE exceeded expectations, while consumer spending declined, presenting a combination of "weak growth + high inflation."

3. Liquidity and Interest Rates

- The Federal Reserve's broad liquidity has slightly improved but remains at around $6 trillion.

- The U.S. Treasury yield curve is "bear steep," with long-term bond yields rising faster than short-term yields, as the market still harbors concerns about inflation.

- Pressure in the credit market is increasing, with widening credit spreads in high-yield bonds, a deteriorating corporate financing environment, and rising recession risks.

II. Macroeconomic Outlook for Next Week

1. The Biggest Market Variable: On April 2, Trump's reciprocal tariffs will be implemented. If tariffs exceed expectations or provoke retaliation, it will impact market sentiment.

2. Focus on U.S. March unemployment rate and non-farm payroll data to validate recession risks.

3. Investment Advice: Prioritize defense, avoid chasing highs and lows.

- Appropriately allocate to arbitrage-type quantitative funds, gold, and U.S. Treasuries as safe-haven assets.

- High-valuation tech stocks and crypto assets remain under dual pressure from interest rates and recession fears; it is advisable to reduce positions or take profits.

- If the tariff impact is less than expected, market risk appetite may warm up, but this does not indicate a trend reversal; further macro support is still needed.

The market is currently in a "weak economy + high inflation + policy swings" pattern, facing downward pressure on risk assets. The future market direction depends on the impact of reciprocal tariffs and whether U.S. employment data confirms recession risks. In the short term, a defensive approach is still necessary, maintaining patience for clearer signals.

Increasing Market Pressure, Waiting for Reciprocal Tariffs to Take Effect?

I. Macroeconomic Review This Week

1. Market Overview This Week

As we analyzed last week, the market is still waiting for the implementation of reciprocal tariffs, and risk assets have shown significant volatility this week.

Aside from gold continuing its upward trend, U.S. stocks, cryptocurrencies, and the commodity market have shown overall weak performance. After Trump's announcement of a tough stance on auto tariffs, market conditions noticeably worsened in the second half of the week.

Chart 1: 4h level, BTC still below EMA200

Source: Tradingview

From the cryptocurrency market perspective, the overall market was calm this week, but momentum was weak. The U.S. House of Representatives introduced the "Stablecoin Transparency and Accountability Promotion Act," aimed at regulating payment-type stablecoins, establishing a new compliance mechanism, expanding regulatory powers, and clarifying key definitions related to the issuance and use of dollar-backed digital assets. The continued easing of policy has not immediately reversed the market's malaise; in the context of poor overall liquidity and ongoing macro uncertainty, our previous judgment remains consistent: the market still needs to find a new direction after the implementation of reciprocal tariffs.

2. Economic Data Analysis

This week's data focused on the U.S. labor market and PCE data, with a particular forward-looking analysis of the credit market.

The latest GDPNow Q1 GDP forecast is -1.8%, unchanged from last week. Notably, the model has made an official adjustment, incorporating gold's imports and exports into consideration. According to recent data from the U.S. Census Bureau and the National Association of Realtors, the forecast for the first quarter's real domestic private investment growth rate has been revised down from 9.1% to 8.8%, with the adjusted model predicting 0.2%.

Chart 2: Latest GDP Forecast

Source: Atlanta Fed

From the data, the trend of economic weakening in the U.S. is very evident, but there is currently no hard data providing a clear signal of recession. However, multiple data points from the labor market and credit market indicate that recession risks have indeed increased.

In terms of the labor market, although the initial jobless claims data released this week was slightly lower than expected and below the previous value, the fatigue in the labor market is very apparent when viewed over a longer period.

Chart 3: U.S. Initial Jobless Claims Data

Source: Zerohedge

Further state data shows that in 387 metropolitan areas in the U.S., 290 have rising unemployment rates.

Chart 4: Unemployment Rate Data from Some U.S. States (Seasonally Adjusted)

Source: U.S. Bureau of Labor Statistics, MishTalk

Notably, the number of continued unemployment claims in Washington D.C. is currently at its highest level since 2021, but initial claims data has not shown significant changes, indicating that the layoffs and budget cuts led by Musk's DOGE division are not proceeding smoothly, possibly due to facing numerous lawsuits.

The PCE data was released on Friday evening, which is the inflation data most closely watched by the Federal Reserve. The February PCE year-on-year and month-on-month rates both exceeded expectations, and after the data was released, risk assets turned from rising to falling.

Additionally, the PCE data does not reflect tariff-driven impacts; the main factor for this rebound is service costs. Furthermore, U.S. personal spending month-on-month for February was 0.4%, below expectations. These two data points reflect that, on one hand, the economy is weak with declining consumer spending, while on the other hand, inflation remains high, making the final mile of decline difficult.

Chart 5: U.S. February PCE Data

Source: U.S. Department of Commerce

3. Liquidity and Interest Rates

This week, the Federal Reserve's broad liquidity continued to marginally improve, remaining around $6 trillion as of March 19.

From the perspective of the interest rate market, the Treasury yield curve shows a clear bear steep, with the slope of long-term bonds rising significantly faster than the short end. From the perspective of interest rate expectations, based on the latest results from interest rate derivatives trading, the probability of a rate cut in June has decreased compared to last week, while the spread of 10-year inflation-protected securities has slightly increased, indicating that the market still harbors concerns about inflation.

In terms of the overall curve shape, the slope in the middle section is more pronounced, possibly indicating that the market believes the Federal Reserve will remain data-dependent; facing high inflation and tariffs, the Fed cannot prevent rate cuts.

Chart 6: Changes in U.S. Treasury Yield Curve

Source: U.S. Department of the Treasury

Additionally, in the previous two weeks' reports, we highlighted the pressure in the credit market. This week's follow-up data shows that the credit spreads of high-yield bonds are still widening, which does not align with the facts reflected by Treasury yields. This indicates that investors are increasingly concerned about the microenvironment of businesses. If credit spreads continue to widen, it may further squeeze corporate refinancing costs and profits, which is an extremely unfavorable forward-looking signal, indicating that the risk of recession in the U.S. economy has not only not receded but may be increasing.

II. Macroeconomic Outlook for Next Week

The current market focus remains on the reciprocal tariffs that Trump will announce on April 2, which will be the biggest variable for the risk market in the near term. If tariffs exceed expectations or if countries subject to tariffs retaliate more than expected, it will have a significant impact on the already fragile market. Additionally, we need to observe next week's U.S. unemployment rate and non-farm employment situation to further assess recession risks.

In this context, arbitrage-type quantitative fund products may serve as a potential stable component in the overall asset allocation strategy for high-net-worth individuals. The current market direction remains unclear, with insufficient upward momentum, and external uncertainties could strike the market at any time.

Our overall view is:

*

##### Prioritize defense; the current macro environment presents a combination of "weak economy + sticky inflation + policy swings," with risk assets (U.S. stocks, cryptocurrencies, high-valuation tech stocks) facing dual pressure from interest rates and recession expectations. For active positions, we recommend building positions or taking profits down.

*

##### From an allocation perspective, in addition to crypto quantitative arbitrage funds, it is still advisable to moderately allocate to safe-haven assets like gold and U.S. Treasuries.

*

##### If next week's reciprocal tariffs are less than expected or if the retaliation from tariffed countries is milder than market expectations, market risk appetite may shift, but it will not directly create upward momentum. Greater macro-positive stimuli are still needed.

*

##### This week, market vulnerability is extremely high; avoid chasing highs and lows, and strictly adhere to discipline.

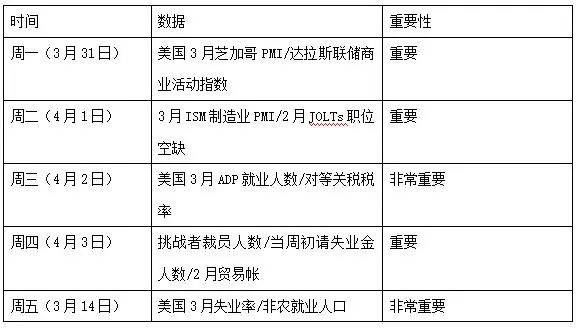

Key macro data for next week is as follows:

Disclaimer

This document is for internal reference only by 4Alpha Group, based on 4Alpha Group's independent research, analysis, and interpretation of existing data. The information contained in this document is not investment advice and does not constitute an offer or invitation for residents of the Hong Kong Special Administrative Region, the United States, Singapore, or other countries or regions where such offers are prohibited to purchase, sell, or subscribe to any financial instruments, securities, or investment products. Readers should conduct their own due diligence and seek professional advice before contacting us or making any investment decisions.

This content is protected by copyright and may not be copied, distributed, or transmitted in any form or by any means without the prior written consent of 4Alpha Group. Although we strive to ensure the accuracy and reliability of the information provided, we do not guarantee its completeness or timeliness and accept no liability for any loss or damage arising from reliance on this document.

By accessing this document, you acknowledge and agree to the terms of this disclaimer.