Usual bond decoupling, RWA stablecoins withstand volatility test

Under the test of fluctuations, can RWA withstand pressure?

Under the test of fluctuations, can RWA withstand pressure?Author: Pzai, Foresight News

RWA stablecoins have recently become a hot narrative, with their backing by off-chain assets introducing a fresh influx of capital into the stablecoin space and opening up ample imaginative possibilities for investors. Among them, the representative project Usual has also gained market favor, quickly attracting over $1.6 billion in TVL. However, the project has recently faced certain challenges.

On January 9, the liquidity staking token USD0++ within the project suffered a sell-off following an announcement from Usual. Meanwhile, some players in the RWA stablecoin camp are experiencing varying degrees of decoupling, reflecting a shift in market sentiment. This article analyzes this phenomenon.

Mechanism Changes

USD0++ is a liquidity staking token (LST) with a staking period of 4 years, similar to a "4-year bond." For every USD0 staked, Usual will mint new USUAL tokens in a deflationary manner and distribute these tokens as rewards to users. In Usual's latest announcement, USD0++ will transition to a lower limit redemption mechanism and provide conditional exit options:

- Conditional Exit: 1:1 redemption, requiring the forfeiture of part of the USUAL earnings. This part is planned to be released next week.

- Unconditional Exit: Redemption at a floor price (currently set at $0.87), gradually converging to $1 over time.

In the context of significant volatility in the crypto market, fluctuations in market liquidity (for example, the underlying asset of RWA—U.S. Treasury bonds—has also seen discounts in recent fluctuations) combined with the implementation of the mechanism have dampened investor expectations. The USD0/USD0++ Curve pool was rapidly sold off by investors, with the pool's deviation reaching 91.27%/8.73%, and the APY for the USD0++/USD0 lending pool on Morpho skyrocketing to 78.82%. Before the announcement, USD0++ had maintained a premium over USD0 for a long time, possibly due to the 1:1 early exemption option provided during pre-trading on Binance, maximizing airdrop benefits for users before the protocol launch. After the mechanism was clarified, investors began to flow back into the more liquid native currency.

This incident has had a certain impact on USD0++ holders, but most of them are incentivized by USUAL, holding for a long time, and the price fluctuation has not fallen below the floor price, reflecting panic selling.

Perhaps influenced by this event, as of the time of writing, USUAL has also dropped to $0.684, with a 24-hour decline of 2.29%.

Gradual Volatility

From a mechanistic perspective, USUAL has the potential to anchor returns to USD0++ through USUAL tokens in the future (by burning USUAL to drive up the token price, increasing yields while attracting liquidity back). In the process of RWA stablecoins pulling in new liquidity, the role of token incentives is also self-evident. The mechanism of USUAL is to reward the entire stablecoin holder ecosystem through USUAL tokens, anchoring while maintaining stable gains. In a volatile market, investors may need liquidity to support their positions, further exacerbating the volatility of USD0++.

In addition to Usual, another RWA stablecoin, Anzen USDz, has also long experienced a decoupling process. Since October 16 of last year, possibly influenced by airdrops, the token has continuously faced sell-offs, once dipping below $0.9, weakening potential returns for investors. In fact, the Anzen protocol also has similar functions to USD0++, but its overall staking scale is less than 10%, limiting the impact of sell-off pressure, and its single pool liquidity is only $3.2 million, far less than USD0's nearly $100 million liquidity in Curve.

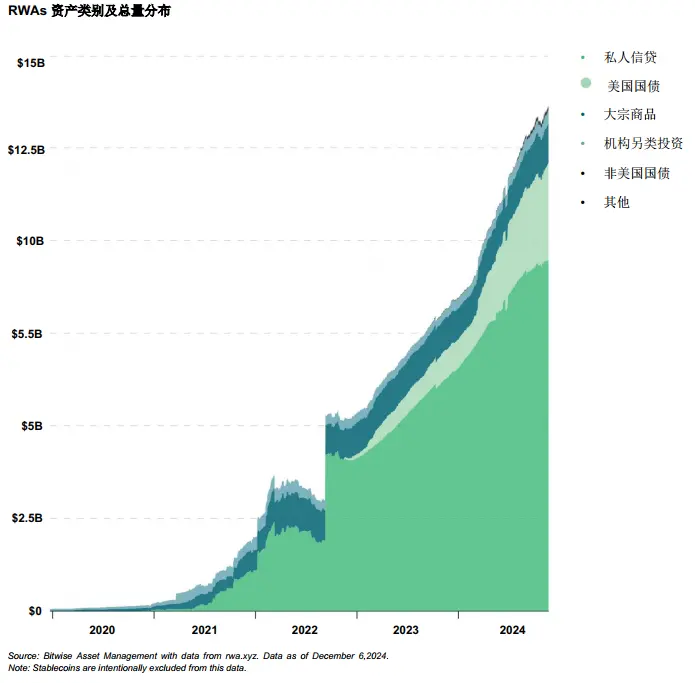

In terms of business models, RWA stablecoins face many challenges, including how to balance the relationship between token issuance and liquidity growth, and how to ensure the growth of real returns synchronizes with on-chain activities. According to Bitwise analysis, most RWAs are U.S. Treasury assets, and the singular asset distribution also exposes stablecoins to some shocks from U.S. Treasuries. How to resist these shocks through mechanisms or reserves is a direction worth considering.

For stablecoin projects, they seem to have fallen back into the "mine-sell-withdraw" cycle reminiscent of the DeFi Summer. While this model can attract a large number of users and funds in the short term through high token incentives, it fundamentally fails to address the long-term value creation of the protocol, and instead risks causing token prices to continuously decline due to excessive selling pressure, ultimately damaging user confidence and the healthy development of the project ecosystem.

To break this cycle, project teams need to focus on the long-term construction of the ecosystem by developing more innovative products, optimizing governance mechanisms, and strengthening community participation, gradually building a diversified and sustainable stablecoin ecosystem rather than relying solely on short-term incentives to attract users. Only through these efforts can stablecoin projects truly break the "mine-sell-withdraw" cycle, providing users with tangible real returns and strong liquidity backing, thus standing out in a competitive market and achieving long-term development.