2024 Financing Report: 1,259 financings, $9.615 billion, overall market trend similar to last year

As the year comes to an end, based on the financing information for the entire year, we review the overall performance of the primary market this year to provide a reference for investors.

As the year comes to an end, based on the financing information for the entire year, we review the overall performance of the primary market this year to provide a reference for investors.Author: Zen, PANews

The spring river water warms, and the ducks know first. The financing information of projects is an important signal for market development, reflecting not only the competitiveness of the projects themselves but also the flow and confidence of market funds, as well as indicating the direction and trend of innovation. PANews launches the “Financing Weekly Report” column every Monday morning, continuously recording the financing market information each week. As the year comes to an end, we review the overall performance of the primary market this year based on the financing information from the entire year, providing references for investors.

Overview of the Investment and Financing Market in 2024

According to incomplete statistics from PANews, there were a total of 1,259 disclosed investment and financing events in the primary market of the cryptocurrency and blockchain field in 2024, with a total funding scale exceeding $9.3 billion. In terms of the total number and scale of financing, the investment and financing market situation this year is basically comparable to that of 2023, which had 1,174 transactions completing $9.615 billion in financing. Compared to the 1,660 investment and financing events in 2022, with a total funding amount exceeding $34.8 billion, the past two years have formed a more stable trend, with investment transactions tending to be more cautious and rational.

It is worth mentioning that, in addition to being close in total amount, the trends of "total financing amount" and "number of financings" this year have also fluctuated similarly to those in 2023.

Firstly, the cryptocurrency investment and financing market had a good start, peaking from March to May, with March's financing scale exceeding $1.03 billion, which is also the only month this year where the financing amount surpassed $1 billion. Close to this were April, May, and October, with funding scales all above $950 million;

Secondly, after a strong start, the market began to weaken in the middle of the year, entering a low period from June to September. During this period, the number of disclosed financing events only broke a hundred in August, while the financing scales in July and September were both below $600 million;

Thirdly, after entering the fourth quarter, there was a sudden surge, with 106 disclosed investment and financing events in October and over $957 million in financing, marking the best single-month performance in the second half of the year. Although there was another downturn in November, the performance of the primary market in December was also impressive, with the financing scale exceeding $818 million as of December 22.

With the development of the industry, the narrative themes and categories of startups have become more diverse than ever. Based on market hotspots, PANews has roughly divided projects into eight tracks: DeFi, Web3 games, infrastructure and tools, AI, DePIN, centralized finance, consumer applications, and others, and has compiled statistics on the investment and financing situation in each track.

As the track most favored by capital for a long time, the number and amount of investment and financing transactions in infrastructure and tools were the highest among all tracks, with 381 events and $3.66 billion respectively; the second hottest track this year was DeFi, with 296 events and $1.69 billion, both ranking second; centralized finance was the only track besides infrastructure and tools and DeFi with a funding scale exceeding $1 billion, and its average financing amount was also the highest at $14.92 million; AI projects, as an emerging category, grew rapidly this year, with nearly 100 disclosed financing events and a funding scale of around $600 million.

The specific statistics for each track are detailed below.

Infrastructure & Tools

Among all the projects that completed financing this year, 30% belong to the infrastructure & tools track, with the amount raised accounting for 39.46% of the total. This track also announced the most large-scale financing news, with financing events of $10 million and above accounting for 27.82%, including 6 events with financing scales exceeding $100 million and as many as 106 events at the $10 million level.

The financing situation in the infrastructure & tools track is roughly in line with the overall trend, with the most financing news disclosed in February, totaling 48 events; the single-month financing peak occurred in March, exceeding $543 million.

In December, the Avalanche Foundation raised $250 million through a private token sale, marking the largest single financing of the year. This round of financing was led by Galaxy Digital, Dragonfly, and ParaFi Capital, with over 40 companies, including SkyBridge and Morgan Creek Digital, participating in the investment.

Additionally, in October this year, payment company Stripe acquired the stablecoin payment platform Bridge for a high price of $1.1 billion, marking the largest acquisition in the crypto industry to date. Bridge aims to build a global payment network for stablecoins, providing software tools and technical support for businesses to accept stablecoin payments. Notably, Sequoia Capital, which holds a 16% stake in Bridge, is expected to gain over $100 million from the acquisition deal.

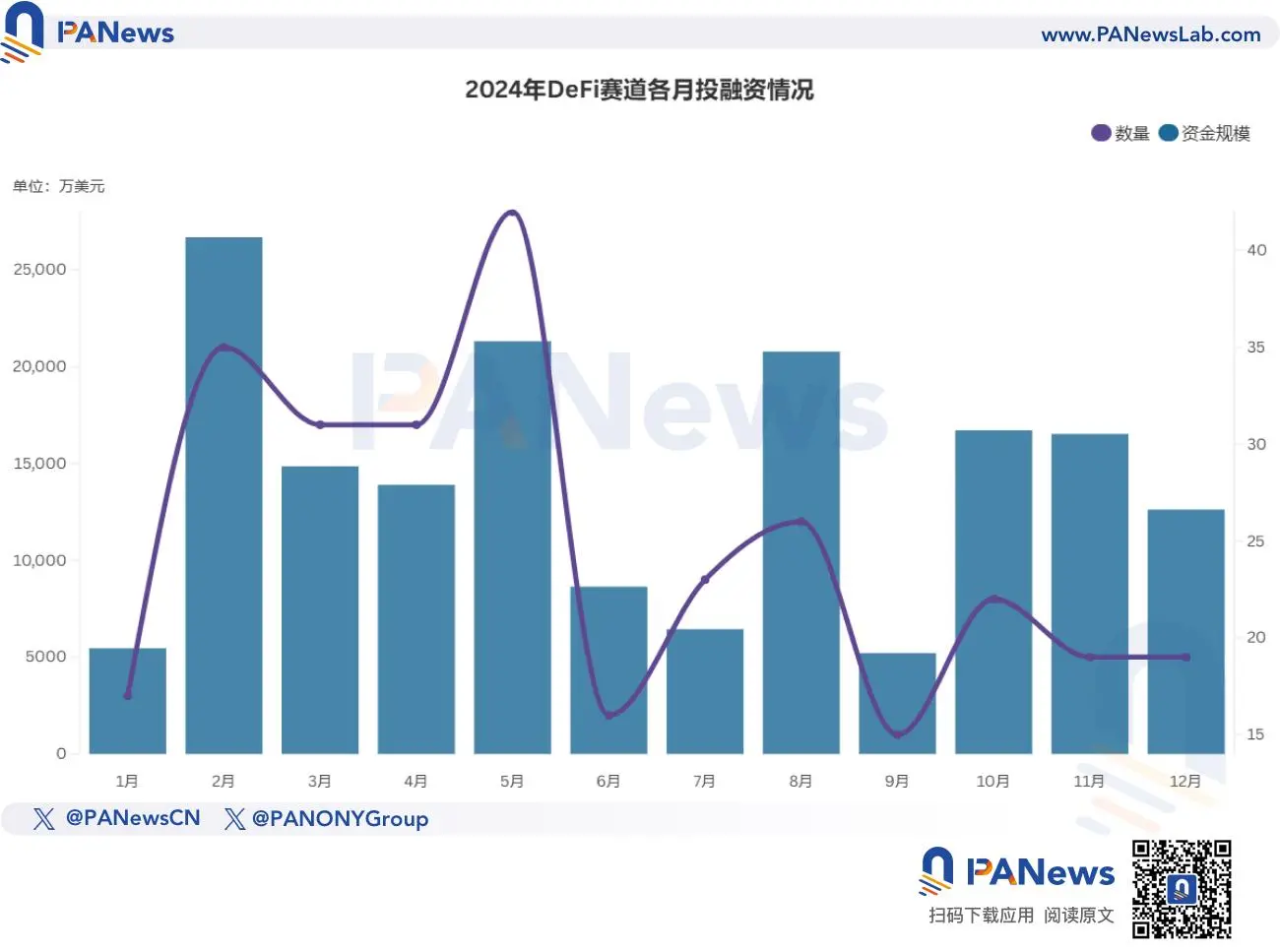

DeFi

The DeFi track saw an explosive start in February this year, with a financing scale exceeding $266 million, the highest for the year. This was mainly due to a16z's $100 million investment in the Ethereum restaking protocol EigenLayer, which was the only project in this track with financing exceeding $100 million this year, boosting confidence in the crypto venture capital market when the form was still unclear. Excluding this factor, the best-performing month for DeFi was May, with 42 disclosed investment and financing events, the most for the year, and a financing scale reaching $213 million.

As mentioned above, the number of investment and financing events and the financing scale for DeFi were 296 and $1.69 billion, accounting for 23.51% and 18.22% respectively. Among the disclosed financing news for DeFi projects, there were 40 events with financing amounts at the $10 million level, accounting for 13.51%, with more concentrated amounts in the millions.

Web3 Games

Compared to the bustling activity in 2022, the gaming track has been much quieter this year. In 2022, the Web3 gaming track disclosed 334 investment and financing events, with a total financing scale of $4.4 billion, of which projects exceeding $10 million accounted for as much as 30%; in 2024, this proportion is only 13.41%. Additionally, among the disclosed financing events this year, the highest was the $42.7 million Series A financing completed by blockchain video game development company Azra Games.

March was undoubtedly the most outstanding month for Web3 games this year, with a total financing amount reaching a peak of $155 million. During this period, the market disclosed a total of 7 financing events at the $10 million scale, including the $35 million raised by NFT card game Parallel, while the total number of financing events exceeding $10 million for the year was 24.

From the statistical data, perhaps due to the rise of other narratives such as AI and DeSci, and the fact that several game projects that previously received large financing are still under development, awaiting market validation, Web3 games may no longer be seen as the "hopeful star"; on the other hand, with mini-games on Telegram, especially play-to-earn games, attracting tens of millions to even hundreds of millions of players, the appeal of AAA blockchain games, which require substantial funding and longer development cycles, is declining for investors.

Web3 + AI

As a mainstream narrative in the entire tech industry, the combination of AI with blockchain and cryptocurrency has also become a direction chosen by many startups. Unlike the overall trend of the primary market, the AI track has rapidly expanded and developed this year, remaining in an upward momentum.

Looking at the quarters, the AI track disclosed 34 financing events in the third quarter, with a funding scale reaching $286 million, both the highest for the year. In the fourth quarter, although the overall heat slightly diminished, it remained significantly higher than in the first and second quarters.

In terms of funding scale, 15.2% of AI projects received funding at the $10 million level, with the open-source AI platform Sentient raising $85 million in a seed round led by Peter Thiel's Founders Fund, Pantera Capital, and Framework Ventures, marking the largest financing in this track.

DePIN

DePIN projects are another track that has shown significant growth after AI, with a total of 47 investment and financing events for the year, with a funding scale close to $280 million. Among these, 9 financing events were at the $10 million level, accounting for 19.56%.

The $50 million financing completed by IoTeX, an IoT blockchain platform, was the largest financing in this track; the Solana ecosystem DePIN protocol io.net and the Ethereum-based blockchain solar company Glow both raised $30 million, ranking second, occurring in March and October respectively. Notably, the DePIN track has remained stable throughout the year, raising the highest amount of $84.05 million in the third quarter.

Centralized Finance

This year, there was only one financing event in the centralized finance track close to $100 million, namely the digital asset financial services group HashKey Group, which completed nearly $100 million in Series A financing with a pre-investment valuation exceeding $1.2 billion. Additionally, there were 30 investment and financing events reaching the $10 million level, accounting for as high as 43.48%. Its average financing amount of $14.92 million is also the highest among all tracks. Notably, in the second quarter, when the overall market was hottest, the centralized finance track performed rather flat, with both the number of financings and the funding scale being the lowest for the year.

Consumer Applications

In the statistical process, consumer applications cover entertainment including music and streaming, SocialFi, NFTs, prediction markets, media, gambling, education, insurance, research, and information. This category performed particularly well in May, with 26 disclosed investment and financing events and a funding scale of $307 million. This was mainly due to the $150 million financing completed by the Web3 social media platform Farcaster and the $70 million financing completed by the prediction platform Polymarket, which shone brightly during the U.S. presidential campaign, marking the two largest projects in terms of financing in this track.

According to statistics, consumer applications disclosed a total of 157 investment and financing events, with a funding scale of $817 million. In terms of funding scale, only 11.16% of consumer projects completed financing at the $10 million level, ranking the lowest among all tracks.

Others

The "Others" category includes blockchain applications in traditional industries such as crypto mining, DAOs, DeSci, task reward platforms, healthcare, and logistics, with 38 disclosed investment and financing events, the lowest among all tracks, and a funding scale exceeding $350 million. In this large category, crypto mining companies play a significant role. In terms of funding scale, the $150 million investment received by crypto miner Hut 8 and the $80 million Series B financing completed by mining machine manufacturer Auradine ranked first and second, both disclosed in the second quarter.

Investment Institutions

According to incomplete statistics, 47 crypto investment funds were launched in 2024, with a total scale of $4.34 billion. Among them, 13 funds raised over $100 million. Notably, Paradigm, which was once criticized for "defecting" from the crypto industry, announced in mid-June that it had raised $850 million for its third fund, focusing on early-stage crypto projects, making it the largest fund by scale in 2024.

It is worth mentioning that a16z announced in April that it had raised $7.2 billion, ultimately exceeding the company's previously set fundraising target by about 4%. Although it was not included in the statistics, as a top-tier investment institution in the cryptocurrency industry, a16z will undoubtedly have a significant amount of funds available for future investments in industry-related projects.

Additionally, this year, multiple project parties launched a total of 15 ecological funds, with a total scale of $594 million. Among them, the $150 million Open Loot fund announced by Big Time Studios is the largest, aimed at promoting game development on the Web3 gaming platform Open Loot, providing financial support, marketing, and development guidance for game studios.