The Labyrinth of Daedalus: The "Token Economic Model" Hidden from Retail Investors

The tricks of consultant shares, conflicts of interest in market making, exaggerated listing fees, high-interest TVL leasing... The real token distribution schemes are often hidden beneath the surface.

The tricks of consultant shares, conflicts of interest in market making, exaggerated listing fees, high-interest TVL leasing... The real token distribution schemes are often hidden beneath the surface.Original Title: Phantom Tokenomics, Inside the Obscure Daedalus Labyrinth

Author: 0xLouisT, L1D Partner

Compiled by: Azuma, Odaily Planet Daily

Editor’s Note: Tokenomics has always been an important criterion for investors to evaluate a target, but L1D partner 0xLouisT revealed in a recent article that, in addition to the conventional tokenomics presented to the market, many projects hide another invisible "tokenomics" underwater. Apart from the internal team and related parties, it is difficult for outsiders to know the true distribution plan of a token.

In the article, 0xLouisT uses the story of "Daedalus' Labyrinth" from Greek mythology as a metaphor, believing that these hidden "tokenomics" are like a labyrinth, and the project parties that create these labyrinths are akin to Daedalus, ultimately leading to their own demise.

Below is the original content by 0xLouisT, compiled by Odaily Planet Daily.

In Greek mythology, there is a bloodthirsty creature called the Minotaur, which has a body structure that is half human and half bull. King Minos feared this creature, so he asked the genius Daedalus to design a complex labyrinth from which no one could escape. However, when the Athenian prince Theseus killed the Minotaur with Daedalus's help, Minos was furious and retaliated by imprisoning Daedalus and his son Icarus in the labyrinth that Daedalus himself had built.

Although Icarus ultimately fell due to recklessness (flying too high during their escape, causing the sun to melt his wings), Daedalus was the true architect of their fate—without him, Icarus would never have been imprisoned.

This myth reflects the pervasive hidden "insider trading" in the current cryptocurrency cycle. In this article, I will reveal these types of trades—labyrinthine structures meticulously crafted by insiders (Daedalus), destined for the project's (Icarus) failure.

What is "Insider Trading"?

The token structure of "high FDV, low circulation" has become a hot topic, and the market has engaged in extensive debate about its sustainability and impact. However, there exists a dark corner in this discussion that is often overlooked—"insider trading." These trades are often reached by a small number of market participants through off-chain contracts and agreements, typically concealed, making it nearly impossible for outsiders to identify them on-chain. If you are not an insider, you may never know about these trades.

In @cobie’s latest article, he introduced the concept of "phantom pricing," emphasizing how true price discovery occurs in private markets. Based on this context, I would like to introduce the new concept of "phantom tokenomics" to reveal how to disguise the real "phantom tokenomics" using the apparent tokenomics model—the publicly visible tokenomics often only represents the "upper limit" of a certain distribution category, which is misleading; the "phantom version" is the most accurate representation of the distribution situation.

Although there are many types of "insider trading," some of the most noteworthy types are as follows.

· Advisor Allocation: Investors can obtain additional tokens through advisory services, and such shares are usually categorized under team or advisor categories. This is often a means for investors to reduce their costs, and they provide little or no additional advice. I have personally witnessed an institution's advisor share being five times that of its investor share, reducing the institution's real cost by 80% compared to official financing and valuation data.

· Market Maker Allocation: A portion of the token supply will be reserved for market making on centralized exchanges (CEX). This has certain positive implications as it can enhance the liquidity of the token, however, when market makers are also investors in the project, conflicts of interest arise—this allows them to use market-making shares to hedge their still-locked investment shares.

· CEX Listing Fees: To list on top CEXs like Binance, project parties often need to pay marketing and listing fees. If investors can assist and ensure the token is listed on these exchanges, they may sometimes receive additional business fees (up to 3% of the total supply). Arthur Hayes previously published a detailed article revealing that these fees could be as high as 16% of the total token supply.

· TVL Leasing: Whales or institutions that can provide liquidity are often promised exclusive higher yields. Ordinary users may be satisfied with a 20% annual yield, while some whales can quietly earn 30% with the same contribution through private transactions with the foundation. This practice may have some positive implications, helping to maintain early liquidity, but project parties should disclose these transactions to the community in the tokenomics model.

· OTC "Financing": OTC "financing" is common and not necessarily a bad thing, but due to the terms usually not being disclosed, these transactions often lead to significant opacity. The most notorious of these is the so-called "KOL round," which is seen as a short-term catalyst for token prices. Some leading Layer 1 projects (I won't name names) have recently adopted this strategy—KOLs can subscribe to tokens at a significant discount (about 50%) and a shorter lock-up period (six months linear unlock), and for profit reasons, they will strive to market xxx as the next xxx (insert a certain Layer 1 here) killer. If you have questions, you can check out my previous KOL script translation guide.

· Selling Staking Rewards: Since 2017, many PoS networks have allowed investors to stake locked tokens and receive staking rewards at any time, which has become a way for early investors to profit in advance. Celestia and EigenLayer have recently been pointed out to have such situations.

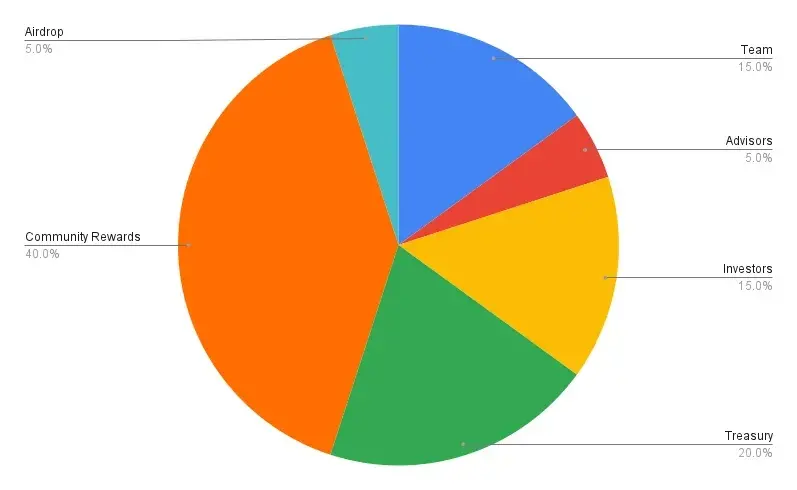

All of these "insider trades" collectively construct the "phantom tokenomics." As a community member, you may often see tokenomics charts like the one below and feel satisfied with their distribution and transparency.

But if we peel away the layers of disguise and reveal the hidden "phantom tokenomics," you may find that the true token distribution looks like the image below, leaving little opportunity for the community.

Just as Daedalus designed a prison for himself, this distribution method determines the fate of many tokens—insiders trap their projects in the labyrinth of opaque trading, causing the value of the tokens to leak from all sides.

How Did We Get Here?

Like most problems caused by market inefficiencies, this issue stems from a severe imbalance between supply and demand.

The number of projects entering the market exceeds demand, many projects are byproducts of the 2021/2022 venture capital boom, with many having waited over three years to launch their tokens, and now they are all crowded together, struggling for TVL and attention in a cooler market environment—please note, it is no longer 2021.

Conversely, demand has not kept pace with supply, with not enough buyers to absorb the frenzy of newly listed projects. Similarly, not all protocols can attract funds and accumulate TVL, making TVL a scarce resource.

Many projects have not found product-market fit (PMF) and have fallen into the trap of overpaying token incentives, artificially inflating key metrics, masking the project's lack of sustainable appeal.

Nowadays, many trades occur privately. With the loss of retail investors, most venture capital and funds struggle to maintain meaningful returns; their profits have shrunk, forcing them to create excess returns through insider trading rather than simply choosing value-added assets.

One major issue remains token distribution, as regulatory barriers make it nearly impossible for project parties to allocate tokens to retail investors, leaving the team with very limited options—typically only airdrops or liquidity incentives. If you are a project party trying to solve the token distribution issue through an ICO or other alternatives, feel free to talk to us.

Revelation

Using tokens to incentivize stakeholders or accelerate project growth is fundamentally not a problem; it can indeed serve as a powerful tool. The real issue is that this can easily lead to a complete lack of transparency in the tokenomics.

Here are several key points that cryptocurrency founders can use to improve transparency:

Do not offer advisor shares to investors: Investors should provide as much help as they can to your company without needing extra advisor shares. If an institution requires additional tokens to invest, they likely lack genuine confidence in your project. Do you really want such people on your investor list?

Seek competitive market-making quotes: Market-making services have become highly commercialized, and you should seek competitive quotes without overpaying. To help founders navigate this issue smoothly, I previously wrote a guide.

Do not confuse fundraising with unrelated operational matters: During the fundraising process, you should focus on finding funds and investors that can help add value to the project. During the fundraising stage, you should avoid discussing market-making or airdrops, and do not sign any documents related to these topics on a whim.

Maximize on-chain transparency: The public tokenomics should accurately reflect the true state of token distribution. During the token genesis phase, tokens can be transparently distributed through different addresses to reflect the real token economic distribution situation. For example, in the pie chart below, you need to ensure you have six main addresses representing the distribution for teams, advisors, investors, etc. You can proactively contact teams like Etherscan, Arkham, Nansen to label addresses, reach out to Tokenomist to create unlock schedules, and contact CoinGecko and CoinMarketCap to display correct circulation and supply data.

Use on-chain unlock contracts: For teams, investors, OTC, or any type of unlock, ensure that it is executed transparently on-chain through smart contracts.

Lock staking rewards: If you allow investors or insiders to stake locked tokens, at least ensure that the staking rewards are also locked. You can check my detailed views on this practice in this article.

Focus on the product, forget about CEX listings: Stop obsessing over whether you can list on Binance; this will not solve your fundamental problems or improve your fundamentals. Take Pendle as an example; it initially only stayed on decentralized exchanges (DEX), but after finding product-market fit (PMF), it easily gained support from Binance. Focus on product development and community growth; as long as your fundamentals are solid enough, CEXs will rush to list your token at better prices.

Avoid using token incentives unless necessary: If you easily distribute your tokens, there must be issues with your strategy or business model. Tokens are valuable and should be used cautiously for specific purposes. Incentives can serve as a growth tool at certain stages, but they should not be a long-term solution. When planning token incentive programs, ask yourself, "What will happen to a metric once the incentives stop?" If you believe that a metric will drop by 50% or more once the incentives cease, then your token incentive program likely has flaws.

In summary, if this article has only one core point, it is "prioritize transparency." I write this article not to blame anyone but to spark a genuine debate, improve industry transparency, and reduce the phenomenon of "phantom tokenomics." I sincerely believe that this will improve over time.

Risk warning Risk warning

Risk warning Risk warning