Funding of 38 million USD, what opportunities are worth participating in with Huma Finance?

Huma Finance is one of the most powerful platforms in the PayFi field, focusing on solving liquidity issues in the cross-border payment industry through innovative payment financial technology.

Huma Finance is one of the most powerful platforms in the PayFi field, focusing on solving liquidity issues in the cross-border payment industry through innovative payment financial technology.Author: MetaHunter168

Huma Finance is one of the most powerful platforms in the PayFi sector, focusing on solving liquidity issues in the cross-border payment industry through innovative payment financial technology. By strategically acquiring Arf Financial and integrating its operations, Huma has established a leading position in the PayFi space. Huma provides robust liquidity and application layers through its PayFi Stack, positioning itself as the first PayFi Network, aiming to offer efficient financing solutions for the cross-border payment sector and deliver substantial real-world returns to investors.

Team Background

Both co-CEOs of Huma Finance are accomplished former executives from Google and Facebook.

With strong backgrounds, one led the successful launch of GoogleFi, while the other drove Facebook to achieve groundbreaking growth, helping the platform reach its first billion users. One sold his company to Facebook, and the other was a core team member who facilitated Lyft's successful IPO. In summary, the team is impressive, with a history of success and capability.

Funding Situation

Huma Finance has completed a $38 million funding round.

Major Investors:

- Major institutions from Europe and the U.S. include Distributed Global, Circle Ventures, Robot Ventures, and ParaFi.

- Asian institutions include Hashkey Capital, Folius Ventures, and ARF's investor Fenbushi.

Huma Business Model Overview

Huma's business model revolves around payments, achieving integration of the liquidity layer and application layer through the newly launched PayFi Stack.

Business Features Include:

- Cross-Border Payments: Traditional cross-border payment companies typically rely on conventional banking channels for global transactions. This process is very slow, as anyone who has sent remittances knows. To address this issue, some financial institutions will provide funding on behalf of the settlement party. Data shows that up to $4 trillion is tied up in global prepaid funding accounts. This portion of funds significantly limits the growth of these companies. Therefore, the payment industry needs more effective liquidity solutions. By providing liquidity to payment institutions, Huma perfectly addresses the prepaid funding issues caused by the slow traditional banking channels in the cross-border payment industry.

- Stable and Efficient Returns: The Huma platform offers over 20% annualized real-world returns, allowing investors to achieve stable returns of 10-12%, primarily sourced from the platform's liquidity business, which is quite impressive.

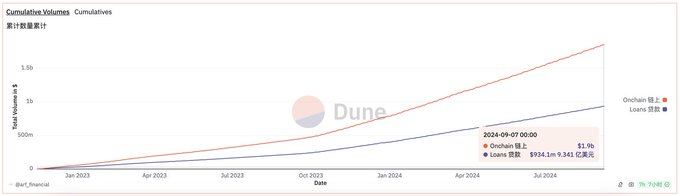

- Zero Default Rate: So far, over $1.9 billion in on-chain transactions have been processed, indicating excellent compliance and risk control capabilities.

Huma and Arf's Strategic Cooperation and Solutions

Huma completed the acquisition of Arf Financial in 2024. Arf Financial focuses on providing real-time liquidity to licensed financial institutions to help them meet customer cross-border payment needs.

Arf's Business Model:

- Target Clients: Provides liquidity to many licensed financial institutions in developed countries, conducting comprehensive ratings based on business and financial data to determine potential clients, thus largely avoiding credit risk issues arising from lending.

- High Capital Utilization: With a capital turnover cycle of about 1-6 days, the number of capital turnovers exceeds 50 times per year, significantly enhancing capital utilization efficiency.

- On-Chain Transparency: All lending and repayments are completed through USDC and are updated in real-time via smart contracts, ensuring on-chain transparency and fund security.

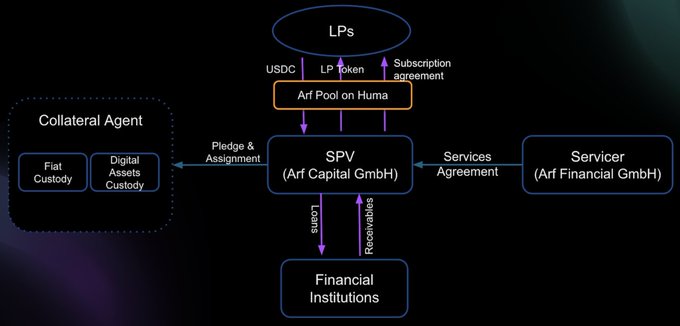

Huma/Arf Solution Diagram

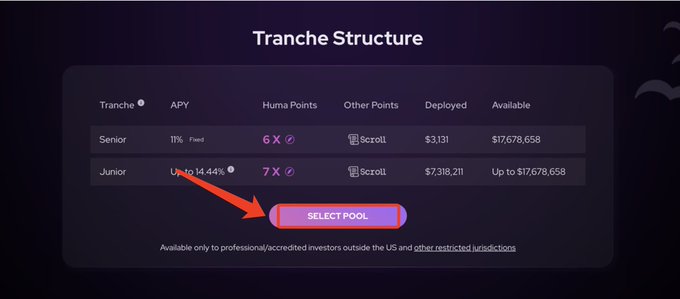

Simply put, the Arf Pool on Huma provides liquidity opportunities for investors, who can choose to participate at either a senior or junior level. Senior level returns are fixed with lower risk; junior level returns are variable, depending on the proportion of junior levels in the pool. Of course, the potential returns are higher than the senior level, but in the event of defaults, junior levels will bear losses first.

Risk Control and Compliance

Huma and Arf have strong compliance and risk control capabilities.

- Safe Accounts: All user funds are stored in safe accounts, ensuring that user funds are separated from institutional operating funds, used exclusively for their intended purpose.

- Legal Risks: Huma and Arf have legal rights over all liquidity loans, allowing Huma to recover liquidity loans preferentially even if a licensed financial institution goes bankrupt.

- Default Risks: The default rate for licensed financial institutions in the payment industry is about 0.25%. Arf's ultra-short loan periods effectively mitigate the possibility of defaults. Additionally, Arf provides a 2% collateral, which will be paid out first in the event of a default. Data shows that Arf has processed over $1.9 billion in on-chain transactions, making it quite reliable overall.

(Data Source: https://dune.com/arf_financial/arf-financia)

Current Participation Opportunities

It has been officially confirmed that participants in the Huma x Scroll event will receive Huma incentives and Scroll marks, allowing them to seize the opportunity of a leading PayFi project while continuing to participate in the Scroll event, effectively getting two benefits from one action. Therefore, it is essential to participate. The event will end by the end of the month, so try to get involved.

Specific Participation Steps and Tutorial:

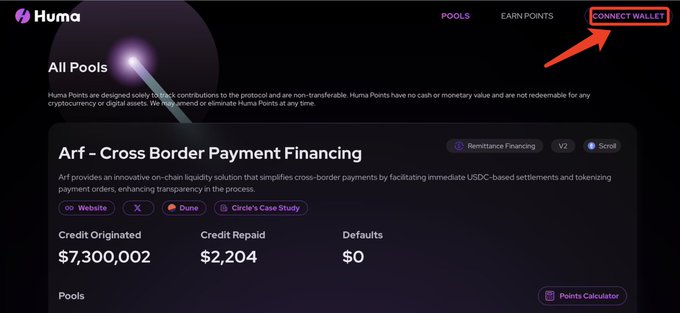

- Open the official website:

https://huma.finance/

- Click "Connect Wallet" in the upper right corner.

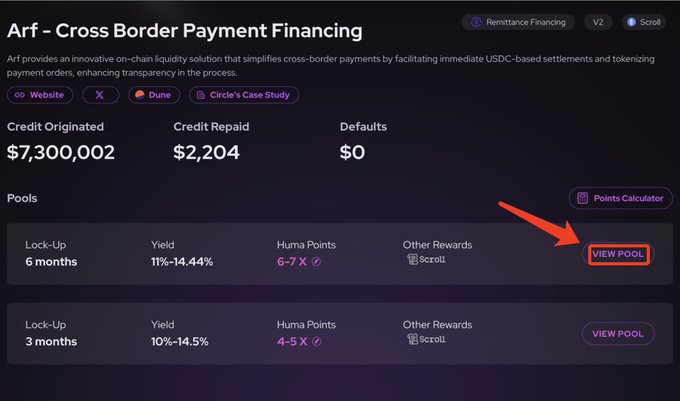

- Choose the corresponding "Locking Period" (I have created a simple table for the specific points and annual interest returns, allowing you to select the appropriate locking time based on your situation; I will use a 6-month locking period for this tutorial).

I have made a table with specific details, which is relatively clear, allowing you to choose the appropriate locking period based on your situation.

- Select "Locking Pool."

- Start "Authorization."

KYC Certification Process:

- Accept the "Agreement" content.

- Authorize "USDC," I chose the senior level.

- Next, select the locked USDC, confirm in the wallet, and complete the locking. This concludes the tutorial.

Summary

In addition to currently participating in earning Huma points and Scroll points activities, you can also pay attention to the subsequent ecological development. The business model is quite good, with strict risk control measures and capital scale. Huma is very likely to become a leader in real-world assets (RWA), with no issues in technical strength and strategic integration, and is likely to play an important role in the global payment industry in the future. If interested, keep an eye on it.

Below are some official materials:

Official Website:

https://huma.finance/

Official Twitter:

https://x.com/humafinance

Official Documentation:

https://docs.huma.finance/