L2 in the data: Abrupt growth, the knockout stage begins

A comprehensive overview of the basic landscape, development models, market data, and future breakthroughs of the Layer 2 sector.

A comprehensive overview of the basic landscape, development models, market data, and future breakthroughs of the Layer 2 sector.Author: Ice Frog

It has been proven that Layer 2 has not been disproven, but the expectation of PUA users through airdrops on L2 has been disproven.

In the context of the overall poor performance of the Ethereum ecosystem and the imbalance between Infra and Application, L2 has to face a brutal market elimination competition. The market's concerns about liquidity fragmentation will also dissipate in this elimination competition. Looking ahead, once breakthroughs are made on the Ethereum application side based on solving interoperability, L2 may regain its former glory.

I. Overview of L2: From Scalability and Cost Reduction to PUA Users

L2 as Infrastructure: Low Barriers, Diverse Options; Homogeneity, Weak Narratives

After Ethereum transitioned to a POS mechanism, the competition for Layer 2 (L2) has become one of the most anticipated areas in the Ethereum and blockchain world. Essentially, L2 solutions aim to reduce transaction costs and increase throughput by sacrificing a small portion of security. This is a key step towards ultimate sharding in Ethereum's mainnet roadmap.

With Optimism open-sourcing the OP Stack, one-click chain deployment has become a reality, lowering the technical barriers for L2 to the minimum. Various projects are emerging, and according to incomplete statistics, there are currently over 60 active L2s in the market. This indicates that Ethereum's attractiveness remains high, but it also raises doubts about whether so many L2s are truly necessary, especially as the liquidity fragmentation issue caused by the high homogeneity of various L2s becomes increasingly severe. This has led to the situation where, after the introduction of EIP-4844 in the 2024 Ethereum Cancun upgrade, although L2 transaction fees have significantly decreased, the Ethereum and L2 ecosystems have not experienced the expected prosperous explosion. Homogeneity, weak narratives, and excess infrastructure have led to continuous criticism and pessimism in the market.

Development Models of L2: Ecological Victory or PUA Users

While L2 was still held in high regard by the market, the four major projects (Arbitrum, Optimism, ZkSync, StarkWare) have been closely watched by the community and the entire market. With massive funding, extremely high valuations, extensive ecosystems, and technical strength, they have become the leaders in the L2 race. However, in today's muddy L2 landscape, some have transformed from kings to "fallen kings," while others have maintained their leading positions, continuously widening the gap with competitors. The differences among them can be traced back to their development models.

The business model of L2 is relatively simple, akin to that of a sub-landlord, profiting from the gas price difference between L2 and L1. Under this business model, L2s face two groups: developers and users. They need developers to keep building while also requiring users to continue transacting. This simple logic tests the operational capabilities of the projects themselves. This has led to a divergence in development among projects: some continuously lower the barriers for developers and expand ecological alliances; some focus on nurturing native applications and strengthening core advantages; while others attract user participation through airdrop expectations, boosting TVL.

With the same profit model, different development paths and focuses have resulted in today's starkly different outcomes. Market data shows that projects that seriously focus on building ecosystems have higher activity levels and stronger risk resistance, while those that continuously PUA users through airdrop expectations have become outdated and neglected.

II. Market Data: From Kings to Fallen Kings, Just One Airdrop Away

Market Data: Some Daily Active Users as Low as Single Digits, Others Steady

In the blockchain world, launching a token somewhat signifies the arrival of the harvest period, but whether it can still attract users afterward is an important indicator of a project's quality.

Looking at the timeline of token launches:

Established projects that have launched tokens include: Arbitrum, Optimism;

Recently launched tokens include: ZkSync, Starknet, Blast;

Tokens expected to launch soon include: Linea, Scroll.

The data is as follows:

Arbitrum

As the leading L2, Arbitrum boasts a massive TVL of $13 billion. From the data, daily averages are relatively stable, with ETH bridging reaching an average of 1,000 ETH daily, high activity, large trading volume, and significant protocol revenue.

Even though other L2s have used various means to siphon off TVL, Arbitrum's activity remains unaffected, truly reflecting its leading value.

Chart: Arbitrum Daily Average Bridged Funds

Data link:

Optimism

As an established L2, Optimism's data lags behind Arbitrum, but its activity and stability remain relatively good.

Chart: Optimism Daily Average Bridged Funds

Data links:

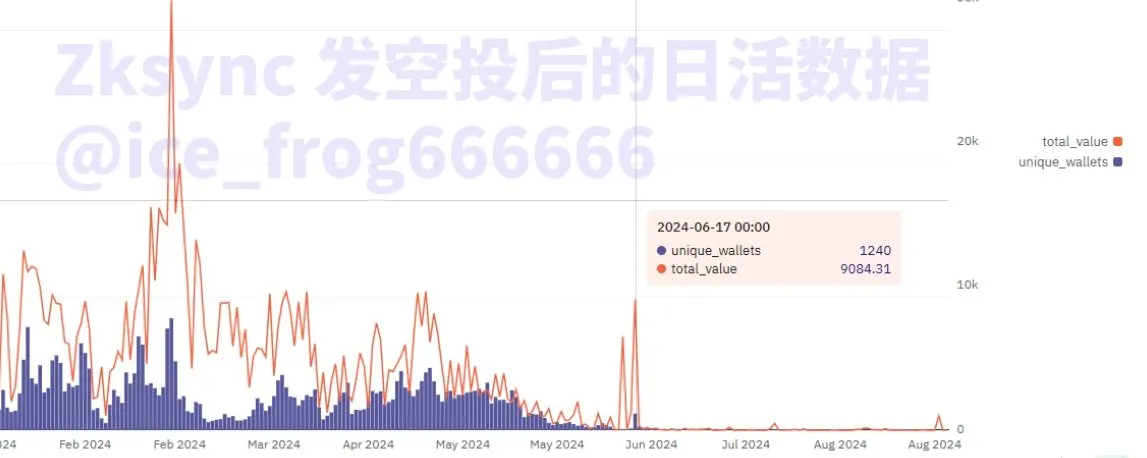

ZKsync

As a leader in zero-knowledge proofs, it has gone from "king" level to "fallen king" level, just one airdrop away. Although both Vitalik and the industry recognize the foresight of ZK technology, its market performance and controversial airdrop have led to unsatisfactory results.

Currently, ZkSync's overall activity is extremely low, especially after its TGE and airdrop release on June 7, which resulted in a sharp decline in on-chain activity. There are often days with deposits below 1 ETH and fewer than 10 depositors, with daily protocol revenue barely maintaining around 1 ETH, essentially operating at a loss.

Chart: ZkSync Protocol Revenue and Daily Activity After Airdrop

Data links:

- https://dune.com/gm365/era

- https://dune.com/peyha/sequencer-profit-on-l2s

- https://dune.com/queries/3813897/6414359

- Further examination of recent data shows that activity is nearly zero, with depositors in single digits and only depositing a few dozen dollars. For a project with an FDV of $2 billion and over $100 million in funding, the data is dismal to the point of being unviewable.

Starknet

Starknet also uses zero-knowledge proof technology, but its data is slightly better than ZkSync, with daily average bridged deposits around several hundred thousand dollars. However, overall active users remain low, with daily transaction counts dropping to an average of 70,000 transactions since this year, and the daily trading volume on DEXs is less than $5 million. For a public chain with an FDV of $4 billion, the activity level is still poor.

Chart: Starknet Daily Average Bridged Funds & Daily Deposit Count & DEX Trading Volume

Data links:

Blast

Blast's daily active users are extremely low, and its TVL has sharply declined from a peak of $3.5 billion earlier this year to $1.5 billion, a drop of 60%. There is a serious outflow of project funds. From the data, it is clear that this year, only on the day of the airdrop did daily active users exceed 3,000. Currently, three months after the airdrop claim, the average daily active users are less than 100.

Chart: Blast TVL Data & Daily Active User Data

Data links:

- https://dune.com/alec/blast-the-new-eth-l2

- https://tokenterminal.com/terminal/projects/blastbridge?v=NDhjMTQ3YzUwYzg4ZGU5MjI5MzNmYWVh

Linea

Linea initially performed well, but due to a lack of a clear token launch plan and airdrop expectations, recent user activity has significantly declined, with daily bridged funds sometimes falling below 1 ETH. However, the number of users remains relatively high, with an average of about 150 daily bridge users. The comparison of these two data points indirectly indicates that users seeking airdrops contribute many small transactions. Overall, due to the lack of clear expectations for Linea's token launch, DAU has declined, with only about a thousand new users added daily, far from the previous daily increase of 100,000 new users.

Chart: Linea Daily Active User Data & Daily New Users

Data links:

Scroll

Scroll's DAU has been declining since the beginning of this year, with daily new users around 100. However, due to strong expectations for Scroll's token launch and high historical retention, interactions from old wallets continue. In terms of revenue, Scroll's protocol income is average, but compared to other recently launched L2s, the data is relatively good.

Chart: Scroll Daily Active User Data & Protocol Daily Average Revenue

Data link:

Reasons Behind the Data: L2 Competition is Fierce, Airdrop Expectations are a Double-Edged Sword

From the above data, it is clear that due to the large number of L2s, competition is becoming increasingly fierce. In the current landscape, established players like Arbitrum and Optimism are showing strong resilience, while newly launched ZkSync, Starknet, and Blast are falling further behind. Upcoming token launches like Linea and Scroll are barely surviving by dangling airdrop expectations to keep users engaged. The reasons behind this deserve analysis, particularly the management of airdrop expectations.

The wealth creation myth brought by airdrops has led to increasingly high expectations among users, which has become an important tool for project teams to manipulate users. However, as can be clearly seen from the comparisons above, while project teams can indeed increase TVL through airdrops, thereby raising valuations and securing large funding, if they fail to continuously invest time and money in user experience, ecosystem building, and airdrop expectation management, and instead keep raising user expectations, it can lead to a situation of "loud thunder but little rain" or result in unfair outcomes, which will quickly backfire in the market.

ZkSync is a typical example; the airdrop hunters supported a project with a market cap of billions, yet after a four-year wait for airdrops, they were met with community backlash over "insider trading," leading to a rapid decline in reputation and market data, making it difficult to recover its former glory.

In contrast, although Arbitrum and Optimism have not reached new heights in token prices, they have consistently focused on ecosystem building and have tried to ensure fairness in airdrops, at least maintaining stability in the data and ensuring the project's continuous and stable operation. Perhaps the lessons learned from ZkSync have led the yet-to-launch Scroll and Linea to refrain from giving clear signals regarding airdrops and token launches, opting to buy time for space, hoping to survive until the next suitable opportunity.

III. Breaking the Deadlock for L2: Integration or Elimination, Hope Lies in Applications

Since the beginning of this year, the voices criticizing Ethereum have been incessant, primarily due to the fact that the Ethereum ecosystem is not only facing the failure of L2 growth expectations but is also being constantly challenged by Solana and others, compounded by poor overall market conditions. The anticipated prosperity and significant price increases have not materialized. From the perspective of L2, its core revenue comes from the gas fee differential, but when the mainnet gas prices drop to single digits, and there are no more attractive narratives for the mainnet, a significant decline in protocol revenue is to be expected.

If we look solely from the technical and performance perspective of Ethereum, L2 is undoubtedly successful and valuable, at least temporarily alleviating Ethereum's congestion and gas issues. However, as mentioned at the beginning of this article, solving performance issues has also led to liquidity fragmentation, and the internal competition among rollups has intensified the division, with interoperability being the first hurdle L2 needs to overcome. Founder Vitalik has clearly recognized this issue, stating on social media in August that it will soon be resolved. In this process, L2s will inevitably face integration or elimination, as there is no need for more than 60 L2s given the current activity levels.

Looking at the long term, the most critical aspect of L2's business model is gas fees, which heavily depend on C-end users. Ironically, most L2s, burdened with high financing and expectations, have chosen to continue building on the B-end infrastructure, with new narratives like RAAS, DAAS, AVS as a service emerging constantly. This is akin to various projects building highways or road construction tools, while the highway entrances are overgrown with weeds and neglected. Infrastructure is thriving, while applications are few and far between; after all, the former is faster and can secure large funding, while the latter is slower and less attractive, leading to the current imbalance in Ethereum's development.

In July of this year, at the Ethereum Developer Conference, Vitalik's keynote speech titled "The Next Decade of Ethereum" highlighted that the biggest theme for the Ethereum ecosystem in the next decade will be applications. If interoperability issues can be resolved, and some L2s are further integrated or eliminated, combined with the launch of the next round of killer applications, the L2 space can still be revitalized. However, which of the L2s mentioned in this article will survive the culling remains uncertain.

IV. Conclusion

Through a comprehensive review of the basic landscape, development models, market performance data, and future breakthroughs of the Layer 2 space, we can see:

Some projects rely on airdrop expectations to PUA users, and once the token is launched, they instantly revert to their original state, becoming largely ignored, such as ZkSync and Blast;

Some rely on the ecological niche and user base accumulated over time, continuously occupying the market forefront through technological innovation and good operations, with a chance to win in the brutal competition, such as Arbitrum and Optimism;

Some have luxurious backgrounds and unprecedented funding, relying solely on airdrop expectations to support themselves, such as Linea and Scroll.

Data facts prove that L2 has not been disproven, but L2s that PUA users through airdrop expectations have indeed been disproven.

Further analysis shows that in the context of the overall poor performance of the Ethereum ecosystem and the imbalance between Infra and Application, L2 must face a brutal market elimination competition. The market's concerns about liquidity fragmentation will also dissipate in this elimination competition. Looking ahead, once breakthroughs are made on the Ethereum application side based on solving interoperability, L2 may regain its former glory.