2024 First Half Web3 Financing Report: Financing Exceeds 7.5 Billion USD, Number of Transactions Increases by 58%

The seed stage financing of Web3 has shown strong resilience, setting a new high in the first half of 2024, raising a total of $189 million.

The seed stage financing of Web3 has shown strong resilience, setting a new high in the first half of 2024, raising a total of $189 million.Original Title: “1H24 Web3 Fundraising”

Author: Cheeky Rolo

Compiled by: Deep Tide TechFlow

Summary

In the first half of 2024, fundraising activities in the Web3 sector saw a significant increase, with 1,240 projects raising $7.52 billion, representing a 24% growth in capital and a 58% increase in the number of deals compared to the second half of 2023. This outperformed the overall venture capital market, which saw a 16.1% growth in capital but a 16.7% decrease in deal volume.

Seed and pre-seed stage financing in Web3 demonstrated strong resilience, reaching a new high in the first half of 2024 with $189 million raised across 80 deals. Series A financing also showed robust growth, raising $1.56 billion across 77 deals, nearly doubling the amount from the second half of 2023.

In the second quarter of 2024, the global startup fundraising environment improved, primarily due to an increase in large funding rounds and a surge in funding for the artificial intelligence sector, which doubled to $24 billion. Despite market fluctuations, the overall trend indicates a gradual recovery, especially in the seed and Series A stages.

The growth in investments in artificial intelligence and Web3 reflects investors' confidence in these high-growth areas, contributing to the stabilization and improvement of the market environment in 2024. This trend suggests potential upward momentum in the coming quarters, particularly in early-stage deals.

Highlights of the First Half of 2024

Source: Messari, Quarterly Transactions Across Web3 Stages

*Note: Approximately 20% of projects did not disclose basic information, such as the amount raised; "number of deals" refers to those projects that disclosed their fundraising amounts.

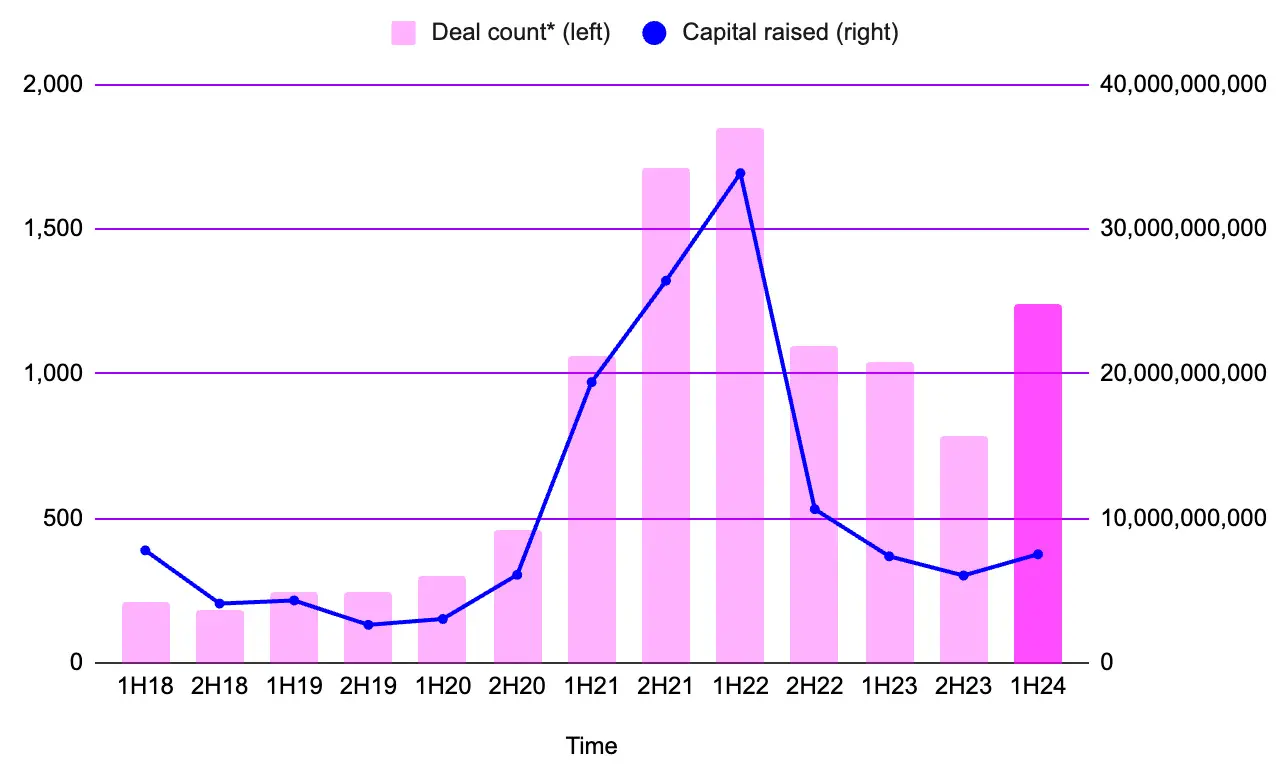

In the first half of 2024, a total of $7.52 billion was raised across all stages, involving 1,240 projects. This represents a 24% increase in capital and a 58% increase in the number of deals compared to the second half of 2023.

In the first quarter of 2024, 624 projects raised a total of $3.66 billion, a 6.2% decrease in fundraising compared to the previous quarter.

In the second quarter of 2024, 616 projects raised a total of $3.86 billion across all funding stages, a 5.5% increase compared to the previous quarter.

Preliminary data indicates that the performance in the first half of 2024 was not as strong as in the first half of 2023, when 1,041 deals raised a total of $13.9 billion. This means that the amount raised in the first half of 2024 was 45.8% lower than in the first half of 2023.

However, this significant difference can be explained by a single successful case. In March 2023, Stripe raised $6.5 billion, accounting for 83% of the funds raised that month, as well as 63% of the total raised in the first quarter of 2023 and 47% of the total for the first half of 2023. If we consider Stripe's funding as an outlier and exclude it from the data, the fundraising performance in the first half of 2024 was actually 2% higher than the first half of 2023, with $7.36 billion raised (excluding Stripe).

Source: Messari, Semiannual Transactions Across Web3 Stages

Note: The $6.5 billion funding by Stripe in March 2023 has been removed from the data in this chart.

From the perspective of the overall venture capital market, $39.6 billion was raised through 2,525 deals in the first half of 2024. In comparison, $34.1 billion was raised through 3,031 deals in the second half of 2023. This indicates a 16.1% increase in fundraising from the second half of 2023 to the first half of 2024, while the number of deals decreased by 16.7%.

According to data from Carta, the number of deals and total fundraising in the second quarter of 2024 saw significant growth compared to the first quarter of 2024, with a total of 1,287 funding rounds completed, amounting to $20.9 billion, showing a steady quarter-on-quarter growth trend since the third quarter of 2023. The second quarter of 2024 recorded the highest level of venture capital investment in the past 12 months.

Source: Carta, Hamza Shad, “State of Private Markets Q2 2024, August 2024

Source: Crunchbase, Gené Teare, “Global Funding and M&A Rebound in Q2, AI Funding Surges, July 2024

Global startup funding rebounded in the second quarter, reaching $79 billion, a 16% increase from the previous quarter and a 12% increase from $71 billion in the second quarter of 2023. This growth was largely driven by large funding rounds exceeding $100 million. Crunchbase data indicates that we are currently in the eighth to ninth quarter of a broader funding downturn. Although the funding amount this quarter ranks among the highest since the first quarter of 2023, this does not necessarily mean that the venture capital market has fully recovered. Since 2023, funding levels have fluctuated significantly each quarter, primarily due to increased large funding rounds for pre-IPO companies and those in the AI sector.

Overall, compared to the broader venture capital market, fundraising performance in the Web3 sector showed slight improvement. This is not only due to the relative increase in funds raised (Web3 increased by 24%, while the broader market increased by 16%), but also due to the significant increase in the number of Web3 fundraising deals (Web3 increased by 58%, while the broader market decreased by 17%).

Web3 Pre-Seed Stage Financing Situation

Source: Messari, Web3 Pre-Seed Stage Transactions and Quarterly Fundraising

- Since the second quarter of 2023, pre-seed stage fundraising in the Web3 sector and the broader venture capital market has shown the strongest resistance to bearish trends. Since the third quarter of 2023, the number of pre-seed stage deals has also shown a quarter-on-quarter growth trend. In the first quarter of 2024, Web3 venture capital raised a historic high of $10.6 million in the pre-seed stage through 36 deals.

Source: Messari, Web3 Pre-Seed Stage Transactions and Semiannual Fundraising

- This also set a new record for Web3 pre-seed stage fundraising within a half-year: $18.9 million raised through 80 deals in the first half of 2024, surpassing the previous record of $18.4 million raised through 102 deals in the first half of 2022.

Web3 Seed and Series A Financing Situation

Source: Carta, Hamza Shad, “State of Private Markets: Q2 2024, August 2024

Data provided by Carta illustrates the performance of seed and Series A deals within the broader venture capital market. The number of seed deals in the second quarter of 2024 was nearly on par with the first quarter, while Series A deals outperformed the previous quarter, indicating that the second quarter may serve as a turning point from the first quarter, which recorded the lowest number of seed and Series A deals since early 2019. Although the total fundraising for both stages in the second quarter saw a slight increase, it is noteworthy that Series A financing in the first quarter reached its lowest level in five years. Despite the 16% growth rate in the second quarter, it still places it among the lower quarters for Series A financing, but this may signal the beginning of an upward trend, albeit with insufficient strength.

In the context of the broader fundraising market, the expected growth trend for seed and Series A deals is more pronounced.

Source: Messari, Web3 Seed Round Transactions and Quarterly Fundraising

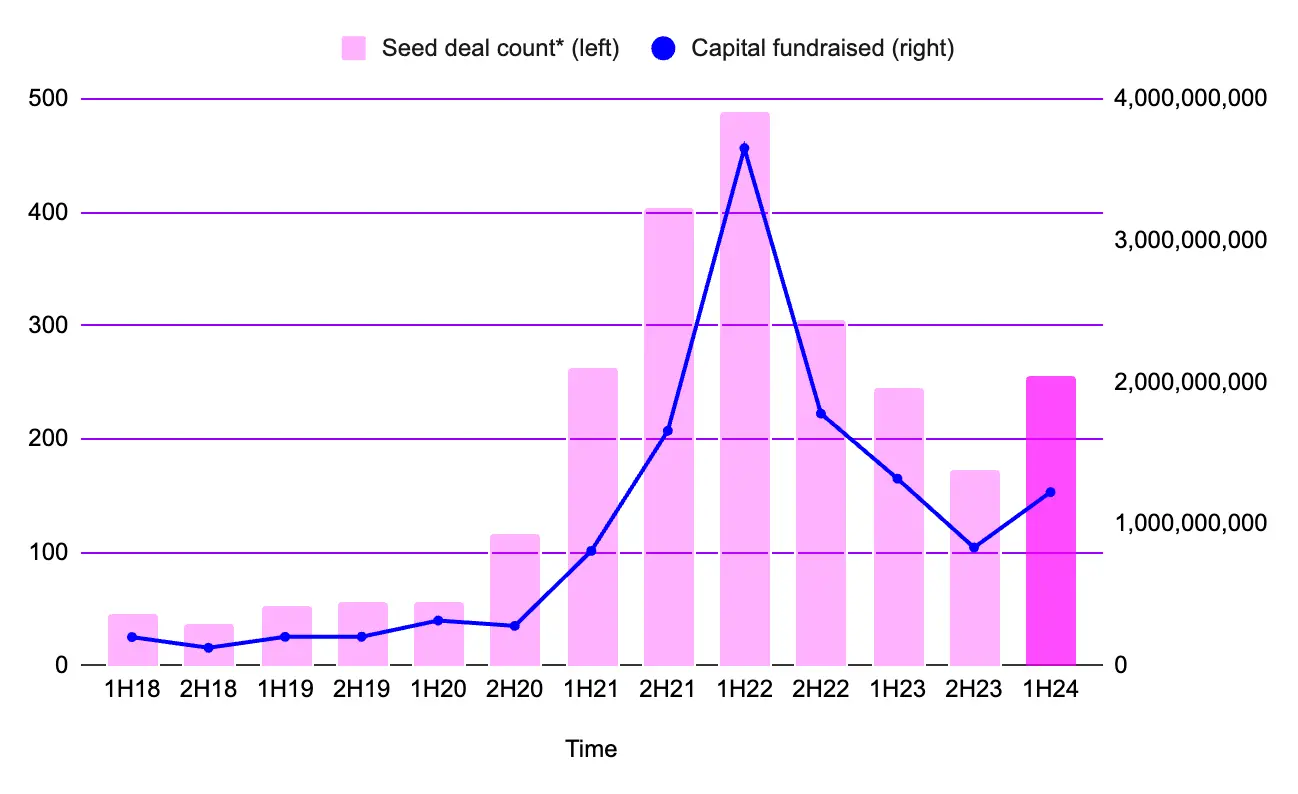

Source: Messari, Web3 Seed Round Transactions and Semiannual Fundraising

- In the first half of 2024, the seed stage raised a total of $1.23 billion across 256 deals. This represents a 47% increase in capital raised compared to the same period last year, with a 49% increase in the number of deals. Although the amount raised in the seed stage decreased by 7% from the first quarter to the second quarter of 2024, there has been a continuous increase in the number of deals for two consecutive quarters. Nevertheless, the total amount raised in the second quarter remains higher than any period from the second to the fourth quarter of 2023.

Source: Messari, Web3 Series A Transactions and Quarterly Fundraising

Source: Messari, Web3 Series A Transactions and Semiannual Fundraising

The upward trend in Web3 Series A transactions is even more pronounced, with both the amount raised and the number of deals increasing each quarter since the end of the fourth quarter of 2023, contrasting with the pre-seed or seed stage transactions during the same period. Overall, in the first half of 2024, $1.56 billion was raised through 77 Series A deals, nearly double the amount from the second half of 2023 (an increase of 97%), with the number of deals also increasing by 75%.

Additionally, there has been a surge in funding in the AI sector, which doubled quarter-on-quarter to $24 billion, accounting for a significant portion of total investments. Public token sales continue to dominate, while early-stage venture capital activity remains stable. This indicates that investors' confidence in high-growth areas such as AI and Web3 remains strong, contributing to the stabilization and improvement of the market environment in 2024.