The "EBOLA" Dilemma of Ethereum VC: When Investment Logic is Infected by Token Burdens

Stop listening to the mandatory infrastructure narrative from VCs; it's time for liquid funds to thrive.

Stop listening to the mandatory infrastructure narrative from VCs; it's time for liquid funds to thrive.Author: Yash Agarwal

Compiled by: Deep Tide TechFlow

Ethereum Venture Capitalists Face EBOLA - Ethereum Bags Over Logic Affliction.

(Deep Tide Note: Here, EBOLA is a pun in English, referring on the surface to being infected with the Ebola virus, but actually describing a state where investors, due to holding a large amount of Ethereum-related assets (bags), neglect or suppress rational logical thinking.)

I will explain the origins of this highly contagious affliction and how you can get vaccinated against it.

Two weeks ago, choppingblock, hosseeb, and tomhschmidt from dragonflyxyz presented a series of arguments in a discussion about Ethereum and Solana.

In general, Solana has:

→ An incomplete venture capital ecosystem

→ Capital levels lower than Ethereum

→ A Memecoin chain

→ Launching on Ethereum is like "starting up" in the U.S., and EV+ is more.

We will review these arguments and:

--- Highlight the structural issues of large funds

--- How this drives them to lean towards infrastructure investments

--- Worse, how this drowns founders in bad advice.

Finally, we will share tactical advice on how to avoid contracting Ebola.

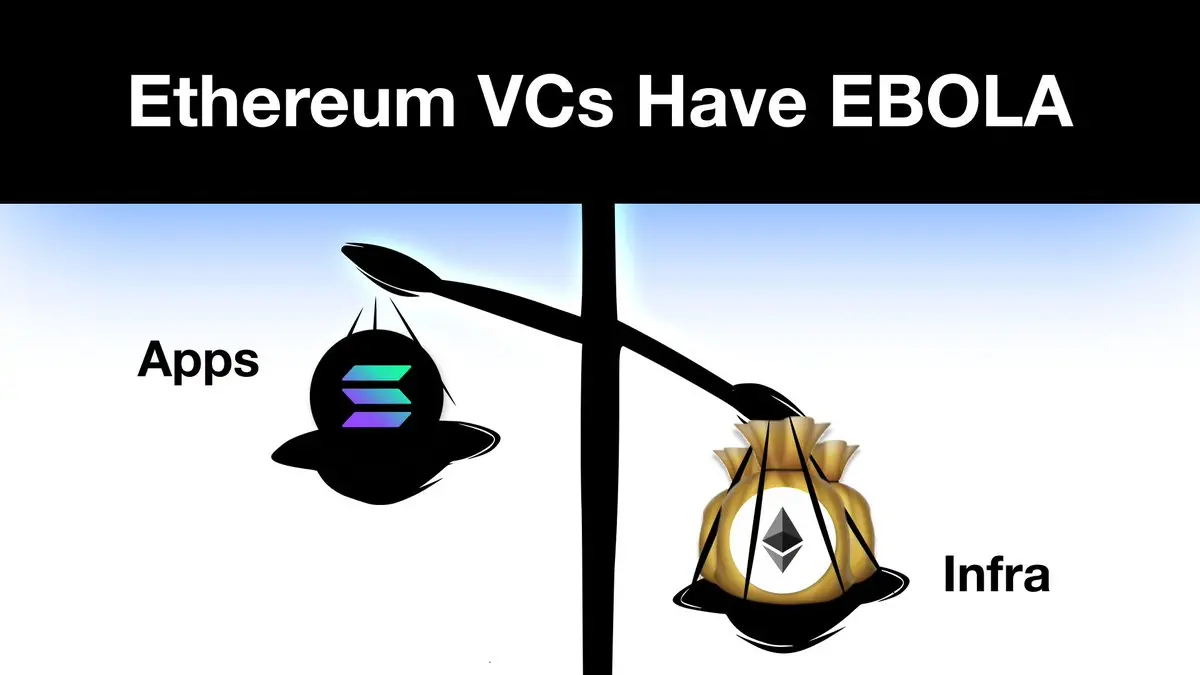

Chapter One: Ethereum Venture Capitalists Infected with Highly Contagious EBOLA

As calilyliu said, Ebola (EVM's Obsession with Logic) is a disease affecting Ethereum venture capitalists—this is a structural issue, especially for large "Tier 1" venture capitalists.

Taking dragonfly_xyz (which raised $650 million) as an example, they may have presented an infrastructure-focused argument to LPs.

Large funds are structurally incentivized to deploy their capital within—say, 2-3 years—willing to fund larger rounds → granting higher valuations.

If they do not fund larger rounds, they cannot deploy capital and must return it to LPs.

Given that infrastructure projects (like Rollups/interoperability/re-staking) can quickly reach over $1 billion in FDV, considering the billions in infrastructure exits from 2021-2022—investing in infrastructure projects is EV+.

However, this is a narrative they have created themselves, accelerated by Silicon Valley's capital and legitimacy engine.

This narrative is quite compelling, but the question is: when we consider the next EVM infrastructure stack, have we deviated from the original vision of global currency TCP/IP? Or is this reasoning driven by the fund economics of large crypto funds (like Paradigm, Polychain, a16z crypto)?

Chapter Two: Ebola Makes Founders and LPs Uncomfortable

Due to infrastructure brands driving high valuations; many major EVM applications announce or launch L2s to achieve these high valuations.

The chase for EVM infrastructure is so frantic that even top consumer founders, like the founder of pudgypenguins, feel the need to launch L2s.

Criticism of low circulation, high FDV projects is valid; what about low impact, high FDV projects?

Take EigenLayer as an example—this is a single project on Ethereum that raised $171 million but has yet to produce any significant impact, let alone generate revenue. It will make some venture capitalists and insiders (holding 55% of the tokens) wealthy.

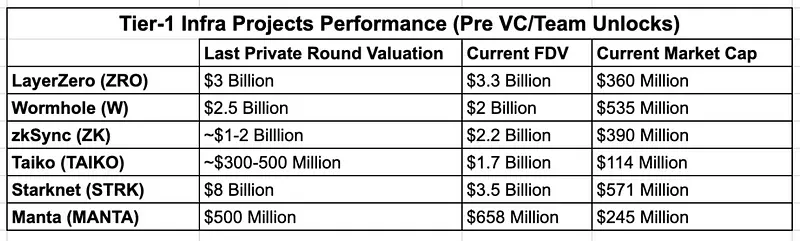

The infrastructure bubble has begun to burst, and many Tier 1 infrastructure projects have launched tokens in this cycle that are now below their private round valuations.

With major unlocks in 6-12 months, venture capitalists will face losses, ultimately leading to a race of who sells first.

There is a reason for the new wave of anti-venture sentiment in the general market; this sentiment is:

More venture capital = more high FDV, low circulation infrastructure.

Chapter Three: The Graveyard of Bad Venture Advice

Driven by venture capitalists, Ebola has also infected promising applications and protocols. From social/consumer applications to high-frequency DeFi, many built on Ethereum are unfeasible due to modem-like performance and unbearable gas fees—leading to a graveyard of applications that are conceptually promising but unable to move beyond the "proof of concept" stage.

++LensProtocol++ is one of the best examples of bad infrastructure advice.

The $140 million funding for StoryProtocol, led by a16zcrypto, aimed at "providing blockchain for intellectual property," shows that Tier 1 venture capitalists are still doubling down on the infrastructure narrative—the only evolution is: from "infrastructure" to "application-specific infrastructure."

Chapter Four: Structurally Broken Risk Markets

The current risk market lacks effective capital allocation between private and public markets.

Crypto venture capital manages billions of dollars in assets, essentially needing to deploy them into specific missions over the next 24 months: from private seed rounds to Series A projects.

The insufficient supply of capital in public markets leads to poor price discovery; for example, the total FDV of all tokens launched in the first six months of 2024 is about $100 billion, which is only half of the total market cap of all tokens ranked from 10 to 100.

The private risk market has already been shrinking. Even Haseeb acknowledges this—these funds are smaller than their previous funds, and the reasons are obvious. If they could, Paradigm would raise 100% of the size of their previous fund.

The structurally broken risk market is not just a crypto problem.

The crypto market clearly needs more liquidity as structural buyers in public markets, which would help address the issues in these broken risk markets.

Chapter Five: Vaccination Against Ebola

Enough, let’s discuss potential solutions and what the industry needs to do, both for founders and investors.

For investors—lean towards liquidity strategies by embracing public markets to scale rather than fighting against them.

As Arthur_0x points out, an effective liquid crypto market requires the presence of active fundamental investors—liquid crypto funds have vast room for growth.

19/ Multicoin's TusharJain_ and KyleSamani summarized this well seven years ago, suggesting that liquid funds can achieve the best of both worlds—combining venture capital economics (investing in young tokens for outsized returns) with public market liquidity.

20/ In contrast to Ethereum, Solana's average financing size in 2023-24 is quite small, except for DePIN; almost all first-round financings are below $5 million.

Major investors include Frictionless, 6thManVentures, goasymmetric, and BigBrainVC, besides ColosseumOrg.

As the liquid market on Solana develops, liquid funds can become reverse investments for individuals and small institutions.

Large institutions should start targeting increasingly larger liquid funds.

For founders—choose an ecosystem with low startup costs until you find product-market fit (PMF).

As naval says, stay small until you figure out what works.

Compared to Ethereum, Solana has lower startup costs.

As tarunchitra points out; on EVM, achieving sufficient novelty and ensuring good valuations often requires a lot of infrastructure development, which is essentially resource-intensive (e.g., the entire application turning into a Rollapp craze).

Applications typically do not require sufficiently high funding to launch; examples include Uniswap, pumpdotfun, and Polymarket.

Solana is the best place for "starting up" for the following reasons:

→ Community/ecosystem support

→ Scalable infrastructure

→ Spirit of rapid delivery

Solana is not just about Memecoins.

Many may argue that DeFi on Solana is dead, and Solana's blue chips are underperforming, like Orca and Solend/Save, but the statistics tell a different story:

While one might argue that the prices of Solana DeFi tokens have plummeted, the same is true for Ethereum's DeFi blue chips, highlighting the structural issues of governance tokens in value accumulation.

Final Chapter: Advice for Application Founders

The larger the fund, the less you should listen to their advice.

Chasing Tier 1 venture capitalists and high valuations, especially when you have not yet found PMF, will lead to valuation burdens and difficulties in discovery at launch, making it harder to build a truly decentralized community around the project.

Financing—Small scale financing. More community-focused.

Raise funds from angel investor groups through platforms like echodotxyz—seek relevant founders/KOLs or choose accelerators like alliancedao or ColosseumOrg.

This is underrated: you exchange valuation for distribution, thus launching in strength.

Utilize superteam for very early stages; this is a shortcut.

Consumer-focused—Embrace speculation. Attract attention.

When venture capitalists see billions exiting here, they are likely to follow the same infrastructure playbook to handle consumer applications. We have seen applications generating $100 million in annual revenue (e.g., pumpdotfun).

In short;

Stop listening to venture capitalists' forced infrastructure narratives.

It’s time for liquid funds to thrive.

Build for consumers. Embrace speculation. Chase revenue.

Solana is the best place for experimentation due to low startup costs.