Data Chart Review: What Changes Occurred in Ethereum After the Cancun Upgrade?

L2 has paid more than 10,000 ETH in fees on Ethereum, but in July, they paid less than 400 ETH in fees.

L2 has paid more than 10,000 ETH in fees on Ethereum, but in July, they paid less than 400 ETH in fees.Author: ParaFi Capital

Compiled by: 1912212.eth, Foresight News

We are conducting an in-depth study of Ethereum's development after EIP-4844, focusing primarily on the following three important directions:

- What is the latest progress on ETH burn rates?

- How attractive are L2 networks?

- What is the economic relationship between L2 and Ethereum?

After the EIP-1559 and the Merge upgrade, there has been excitement around ETH as a cash-flow-generating asset. Following the initial two upgrades, the supply of ETH did indeed decrease, dropping by about 0.38% from September 2022 to April 2024. However, since then, the supply of ETH has started to rise as the burn rate has slowed down.

In the past 12 months, the ETH staking reward rate has been on a downward trend, as the number of Ethereum validators has increased by 79% over the past year, while L1 transaction fees have decreased.

Although the burn rate has slowed, applications and protocols such as Uniswap, Tether, 1inch, and MetaMask continue to drive most of the Gas consumption on Ethereum. In 2023, Arbitrum and ZKsync were the main Gas consumers, but their data has significantly declined this year due to the EIP-4844 proposal, which allows L2 to publish data more efficiently, reducing their data storage requirements.

Over the past two and a half years, the number of transactions on Ethereum has remained relatively stagnant, while the total number of transactions on L2 exceeded L1 by more than 10 times in August 2024.

The growth in L2 activity can be attributed to the launch of new L2s and explosive growth in some existing L2s. Since March, the daily transaction counts for Base and Arbitrum have surpassed Ethereum. While this chart aggregates transactions from multiple L2s, each L2 is providing alternative block space for Ethereum, highlighting the significant trend of migration from L1 to L2.

The increasing growth of Ethereum L2s is also reflected in their capture of a significant share of the DEX market from Ethereum. After the EIP-4844 upgrade, L2 has pushed the DEX market share on the Ethereum mainnet below 60%.

However, this also highlights the issue of liquidity fragmentation due to the continuous development of Rollup networks. Despite the tremendous success of these L2s, their costs for publishing data on Ethereum have been relatively low due to the EIP-4844 upgrade. EIP-4844, implemented in March 2024, introduced a new data storage mechanism called "blobs," which serves as a cheaper alternative to the previous Calldata structure.

In March 2024, L2s paid over 10,000 ETH in fees on Ethereum, but by July, they paid less than 400 ETH, a decrease of about 96%. As costs have declined, L2s now contribute less to ETH burn and have reduced Gas fees on the mainnet.

Since L2s need to publish a large amount of transaction summary data on-chain, they have rapidly adopted blobs. Since early June, Ethereum has seen at least 16,000 blobs published daily. This has led to a decrease in the total fee proportion paid by major L2s, dropping from 12% in 2024 to 1%.

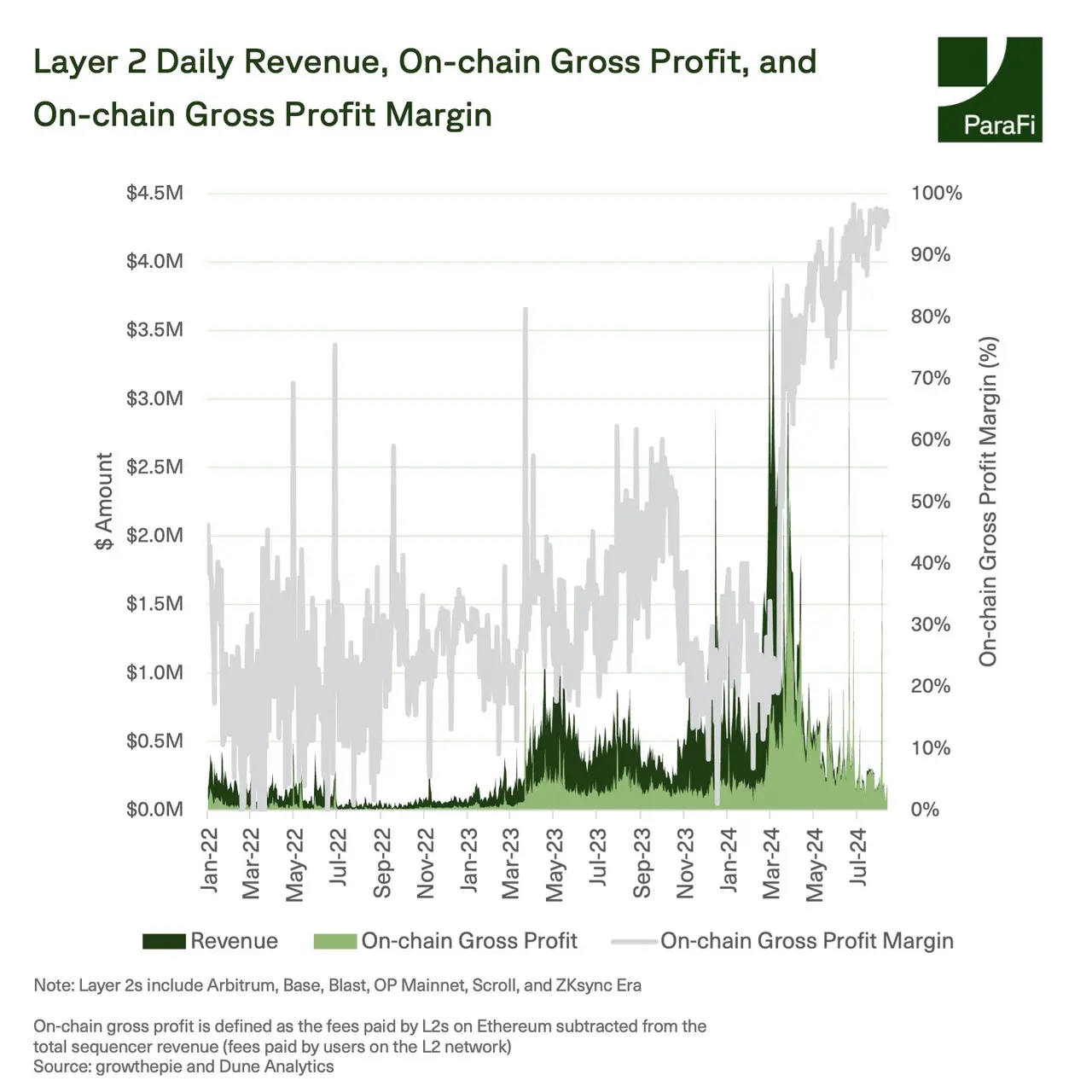

Since the implementation of EIP-4844, the operating profit margins for L2s have significantly increased. Although the total sequencer revenue (i.e., the total fees paid on L2 networks) has averaged a decline of about 48% this year, operating costs have decreased by about 87%, meaning that Rollups now retain most of their revenue. Mainstream L2s now have operating profit margins exceeding 90%, even after passing a significant portion of cost savings to users. Users benefit from this, as fees on networks using blobs have decreased by about 90% over the past year, with median transaction costs typically below $0.01.

EIP-4844 has had a significant impact on Ethereum L1.

Despite the surge in L2 usage, the direct benefits to ETH as an asset remain unclear. In recent months, although L2 profits have risen significantly, the burn rate of ETH has decreased, leading to a reduction in the value flowing into ETH.

This leaves many questions for the Ethereum ecosystem to ponder:

- As L2 usage continues to grow, what role will L2 tokens play? How much value will L2 tokens capture compared to ETH?

- Are the rewards for Rollups relative to Ethereum excessive? Or is this structure ideal for attracting more users and developers into the broader Ethereum ecosystem?

- How will users and liquidity interoperate between these different networks as more L2s are launched?

- With Ethereum mainnet fees now at historical lows, will we see developers reconsider deploying directly on L1, or will L2 still be more attractive?