RWA: The Rise of Real Assets

This article explores the trend and development prospects of tokenizing real-world assets (such as real estate, bonds, stocks, etc.) through blockchain technology and integrating them into the decentralized finance (DeFi) ecosystem. The article introduces the historical evolution of RWAs, the main tracks, and the regulatory challenges they face, pointing out the application potential in the securities, real estate, lending, and stablecoin markets, as well as the possible investment risks.

This article explores the trend and development prospects of tokenizing real-world assets (such as real estate, bonds, stocks, etc.) through blockchain technology and integrating them into the decentralized finance (DeFi) ecosystem. The article introduces the historical evolution of RWAs, the main tracks, and the regulatory challenges they face, pointing out the application potential in the securities, real estate, lending, and stablecoin markets, as well as the possible investment risks.1. Tracing RWA

RWA------Real World Assets

RWA, short for Real World Assets, refers to assets in the real world that are represented and traded in a digital, tokenized manner within the blockchain or Web3 ecosystem. These assets include but are not limited to real estate, commodities, bonds, stocks, artworks, precious metals, intellectual property, and more. The core idea of RWA is to bring traditional financial assets into the decentralized finance (DeFi) ecosystem through blockchain technology, achieving more efficient, transparent, and secure asset management and trading.

The significance of RWA lies in its ability to enhance the liquidity of relatively illiquid assets in the real world through blockchain technology, allowing them to participate in the DeFi ecosystem for lending, staking, trading, and other operations. This method of connecting real assets with the blockchain world is becoming an important development direction in the Web3 ecosystem.

RWA------Special Asset Status

RWA tokenizes real-world assets, transforming them into digital assets that can generate utility on the blockchain, essentially acting as a bridge between crypto-native assets and traditional assets. Crypto-native assets are generally realized through smart contracts, with all business logic and asset operations completed on-chain; adhering to the principle of "Code is Law"; while traditional assets such as bonds, stocks, and real estate operate under the legal framework of the real world, protected by government laws. The series of tokenization rules proposed by RWA requires both on-chain technical support from smart contracts and legal protection for underlying assets like stocks and real estate in the real world.

In fact, under the RWA framework, tokenization is not merely a simple process of issuing a token on the blockchain; it involves a complex set of processes that relate to asset relationships in the real world off-chain. The tokenization process typically includes: purchasing and custodizing the underlying assets, establishing a legal framework for the token's relationship with these assets, and finally issuing the tokens. Through this tokenization process, off-chain laws and regulations and related product operation processes are integrated, ensuring that token holders have a legal claim to the underlying assets.

RWA------Historical Tracing

The development of RWA can be divided into three stages: early exploration, preliminary development, and rapid expansion.

Early Exploration Stage (2017-2019)

2017: RWA Exploration Begins

With the gradual maturity of the decentralized finance (DeFi) concept, the idea of RWA (Real World Assets) began to emerge. Pioneer projects like Polymath and Harbor started exploring the feasibility of tokenizing securities. Polymath focused on creating a platform for issuing security tokens, aiming to solve legal compliance issues, while Harbor aimed to provide a compliance framework for the liquidity of security assets on the blockchain.2018: Beginning of Commodity Tokenization

In the fields of real estate and commodity tokenization, some pilot projects began to emerge. For example, the RealT project attempted to tokenize real estate in the U.S., allowing global investors to gain partial ownership and rental income from U.S. real estate by purchasing tokens.2019: TAC Alliance Established

The TAC Alliance was established to promote the standardization and cross-platform interoperability of RWA, facilitating cooperation and development among different projects. Additionally, platforms like Securitize and OpenFinance were launched during this period, focusing on providing compliance solutions for tokenized assets.Preliminary Development Stage (2020-2022)

2020: Multiple Projects Introduce RWA

The Centrifuge project gained significant attention by tokenizing real-world receivables and invoices, enabling small and medium-sized enterprises to obtain financing on the blockchain. Moreover, well-known DeFi projects like Aave and Compound began experimenting with RWA as collateral to expand their lending operations.2021: Maker DAO Joins the RWA Market

Centrifuge introduced RWA as collateral to the MakerDAO lending platform, allowing users to obtain the stablecoin DAI by holding RWA.2022: Traditional Capital Engages with RWA

Large financial institutions like JPMorgan and Goldman Sachs began conducting research and pilot projects related to RWA, exploring how to digitize traditional assets through blockchain; the RWA Alliance was established to promote the standardized development and global adoption of RWA.Rapid Expansion Stage (2023-Present)

2023: Government Involvement in RWA Legal Framework

Large asset management firms like BlackRock and Fidelity began attempting to manage part of their asset portfolios through tokenization to enhance liquidity and transparency; the U.S. Securities and Exchange Commission (SEC) and the European Securities and Markets Authority (ESMA) also began to gradually intervene, attempting to establish a regulatory framework related to RWA.

2. RWA Track Directions

Given the diversity of traditional asset forms, the RWA track shines in various fields. From tangible assets such as real estate, commodities, precious metals, artworks, and luxury goods, to intangible assets like bonds and securities, intellectual property, carbon credits, insurance, non-performing assets, and fiat currencies, RWA (Real World Assets) demonstrates its application potential across different domains.

Real Estate Industry

In traditional finance, real estate is often viewed as a relatively stable asset for long-term investment, possessing strong capital appreciation potential in normal market conditions. However, the low liquidity and high leverage characteristics of real estate raise the transaction threshold and increase the investment risks for individual investors. In RWA projects related to real estate, tokenization can significantly enhance asset liquidity and reduce the risks borne by individuals.

Tangible: Focuses on the tokenization of physical assets (such as real estate and precious metals), enabling these traditionally hard-to-trade assets to achieve liquidity on the blockchain.

Landshare: By tokenizing real estate, Landshare allows small investors to participate in the real estate market, especially through its blockchain-based real estate fund model.

PropChain: Provides a blockchain-based global real estate investment platform, allowing investors to gain exposure to the global real estate market through tokens without needing to purchase properties directly.

RealT, RealtyX: Allow investors to own a portion of U.S. real estate and earn rental income by purchasing tokens.

Fiat to Stablecoins

In the stablecoin sector, there are USDT (Tether), FDUSD, USDC, and USDE, among others. These stablecoins provide a low-volatility asset in the crypto market by pegging their value to fiat currencies, with USDT (Tether) being the most well-known. Tether is currently the largest stablecoin by market share, with its value pegged to the U.S. dollar at a 1:1 ratio. This means that each USDT corresponds to one dollar.

In traditional financial markets, fiat currency itself is a real-world asset (RWA), maintaining its value through reserves and regulatory mechanisms. When fiat currency enters the blockchain in the form of stablecoins, it is repackaged as a programmable digital asset that can directly participate in various operations within the decentralized finance (DeFi) ecosystem, such as lending, payments, and cross-border transfers. Tether directly associates the value of USDT with real-world assets priced in U.S. dollars, significantly enhancing the stability of USDT while providing a relatively safe and stable environment for the introduction and use of RWA.

USDT's Operating Mechanism

Tether supports the value of USDT by holding a basket of reserve assets. These reserve assets include cash, cash equivalents, short-term government bonds, commercial paper, secured loans, and a small amount of precious metals. When users deposit fiat currency (such as U.S. dollars) into Tether's account, Tether issues an equivalent amount of USDT to the user, thereby achieving the 1:1 peg between USDT and the U.S. dollar.USDT's Stability and Risks

Systemic Risk: Since USDT's value is directly pegged to the U.S. dollar, its users bear systemic risks and market volatility associated with the dollar. For example, if the dollar experiences significant depreciation in the global market, the purchasing power of USDT will also decline.

Regulatory Risk: If regulatory authorities question or take action against Tether's operating model, it may affect the issuance and use of USDT.

Collateral Risk: Although Tether claims that USDT is fully backed by reserve assets, there have been ongoing concerns about the transparency and sufficiency of these reserves. If Tether cannot maintain adequate reserves or if the quality of the reserve assets declines, it may lead to USDT losing its peg, meaning it can no longer maintain its 1:1 value with the dollar.

Liquidity Risk: Under extreme market conditions, Tether may face liquidity shortages. If a large number of users simultaneously request to exchange USDT back to dollars, Tether may struggle to fulfill these requests in a short time, leading to market panic and price volatility.

The various dilemmas and issues faced by Tether are not unique to the stablecoin market but are problems that affect the entire RWA market. The safety of RWA is always closely related to the quality of its underlying assets and is easily influenced by the laws and regulations of different countries and regions.

Lending Market

The combination of RWA and the credit lending market can bring more collateral options and higher loan amounts. In DeFi protocols like Maker and AAVE, borrowers need to provide crypto assets worth more than the loan amount as collateral to ensure loan security. The involvement of RWA expands the range of collateral to include traditional assets like real estate and receivables, allowing not only crypto assets but even assets from the real economy to participate in this system. This initiative can bring more public funding for the development of small and micro enterprises, provide larger enterprises with more lending channels, and allow ordinary investors to invest in companies and gain returns from future developments.

Bonds and Securities

In traditional financial markets, bonds and securities are among the most widely used investment methods, often backed by comprehensive financial regulatory systems. Therefore, in RWA projects related to bonds and securities, aligning with real-world laws and regulations is the most crucial step.

Maple Finance: Provides a way for businesses and lenders to create and manage loan pools on-chain, making the issuance and trading of bonds more efficient and transparent.

Securitize: Offers services for the issuance, management, and trading of tokenized securities. This platform allows companies to issue bonds, stocks, and other securities on the blockchain and provides a complete set of compliance tools to ensure that these tokenized securities meet the legal and regulatory requirements of various countries.

Ondo Finance: Offers products including tokenized short-term government bond funds, which provide stable returns, further blurring the lines between DeFi and traditional finance.

3. RWA Market Size

RWA experienced a significant explosion in May 2023, and as of the time of writing, according to defillama, the TVL related to RWA remains as high as $6.3 billion, a year-on-year increase of 6000%.

According to data from RWA.xyz, there are as many as 62,487 holders of RWA-related assets, with 99 issuers, and a total value of stablecoins amounting to $169 billion.

Many well-known Web3 companies, including Binance, are optimistic about the future market value of RWA, estimating that its total market value could reach $16 trillion by 2030.

As an emerging track, RWA is changing the DeFi market with unprecedented strength, and its vast potential is worth investors' expectations. However, the development of RWA projects is highly related to reality, and the differing laws and regulations in various countries and regions can easily become constraints on its development.

4. RWA Ecosystem Development

With the entry of traditional capital from firms like Goldman Sachs and SoftBank, as well as well-known Web3 companies like Binance and OKX, strong projects in the RWA track are gradually emerging. New and established projects like Centrifuge, Maple Finance, Ondo Finance, and MakerDAO are beginning to shine in this blue ocean, becoming true leaders in RWA in terms of technology and ecosystem layout.

Centrifuge: Real Asset On-Chain Protocol

Concept

Centrifuge is a platform for tokenizing real-world assets on-chain, providing a decentralized asset financing protocol that connects well-known DeFi lending protocols like MakerDAO and Aave with borrowers in the real world who have pledgeable assets (usually startups), facilitating the circulation between DeFi assets and real assets.

Financing Development

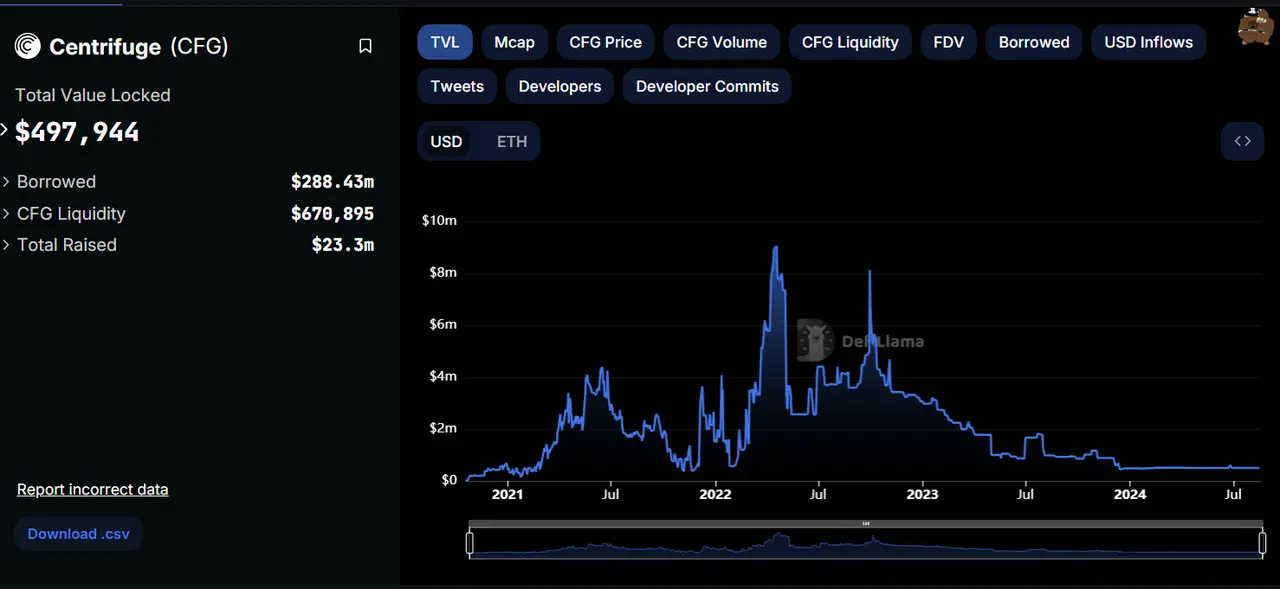

Since its inception, Centrifuge has been highly sought after by capital, raising a total of $30.8 million in five rounds of financing from 2018 to 2024, with notable VCs including ParaFi Capital and IOSG Ventures backing it. The Centrifuge project itself has also achieved impressive results, currently tokenizing 1,514 assets, with a total financing asset amount of $636 million, a year-on-year TVL growth of 23%.

Technical Architecture

Centrifuge's core architecture consists of Centrifuge Chain, Tinlake, on-chain asset net asset value (NAV) calculation, and a layered investment structure. Centrifuge Chain is an independent blockchain built on Substrate (part of the Polkadot parachain), specifically designed for managing asset tokenization and privacy protection; Tinlake is a decentralized asset financing protocol that allows issuers to generate NFTs from assets and use these NFTs as collateral to obtain liquidity.

In a complete lending operation process, real-world assets are tokenized into NFTs through the Tinlake protocol, which are then used as collateral, allowing issuers to obtain liquidity from the pool while investors provide funds to the liquidity pool. At the same time, the on-chain NAV calculation model ensures that both investors and issuers can transparently see the pricing and status of the assets. The layered investment structure allows for three different lending tiers: junior (high risk, high return), mezzanine, and senior (low risk, low return).

Development Issues

Although the Centrifuge project ranks first in attention among RWA projects according to RootData, core data such as TVL has declined due to factors like the impact of the 2022 bear market and unmet project expectations for 2024, currently standing at only $497,944.

ONDO Finance: Leader in U.S. Treasury Tokenization

Concept

Unlike Centrifuge, which aims to build a platform for the circulation of DeFi funds and real assets, Ondo Finance is a decentralized institutional-grade financial protocol designed to provide institutional-level financial products and services, creating an open, permissionless, decentralized investment bank. Currently, Ondo Finance focuses on creating stable asset options beyond stablecoins, bringing risk-free or low-risk, steadily appreciating, and scalable fund products (such as U.S. Treasury bonds, money market funds, etc.) onto the blockchain, allowing holders to enjoy most of the underlying asset's returns while maintaining relatively stable assets.

Financing Development

ONDO Finance has historically conducted three rounds of financing, raising a total of $34 million, with investors including Pantera Capital, Coinbase Ventures, Tiger Global, Wintermute, and other well-known institutions. Additionally, ONDO Finance has partnered with as many as 82 partners across four areas: chain support, asset custody, liquidity support, and service facilities.

ONDO Finance's market performance is also impressive, with the current project token ONDO priced at $0.6979, reflecting increases of 2448%, 1270%, and 784% compared to the A round financing price of $0.0285, ICO financing price of $0.055, and opening price of $0.089, respectively, showcasing the market's enthusiastic pursuit of the project.

In terms of key data like TVL, ONDO Finance has seen significant growth since April of this year, currently reaching $538.97 million, ranking third in the RWA track.

Product Architecture

The main products of ONDO Finance currently include USDY and OUSG.

USDY (U.S. Dollar Yield Token) is a new financial instrument issued by Ondo USDY LLC, combining the accessibility of stablecoins with the yield advantages of U.S. Treasury bonds. Unlike many other blockchain yield tools, USDY's design complies with U.S. laws and regulations and is backed by short-term U.S. Treasury bonds and bank demand deposits.

USDY includes two types: USDY (accumulating) and rUSDY (rebase). The price of USDY (accumulating) tokens increases with the yield of the underlying assets, suitable for long-term holders and cash management needs; rUSDY (rebase) maintains a token price of $1.00, with yields realized by increasing the number of tokens, making it suitable as a settlement or exchange tool.

OUSG (Ondo Short-Term U.S. Government Bonds) is an investment tool issued by Ondo Finance that provides liquidity exposure through tokenization, aiming to offer investors ultra-low-risk and highly liquid investment opportunities. OUSG tokens are linked to U.S. short-term Treasury bonds, allowing holders to gain liquidity returns through instant minting and redemption.

Tokenization Structure: The underlying assets of OUSG are primarily held in the BlackRock U.S. Institutional Digital Liquidity Fund (BUIDL), with other portions held in BlackRock's Federal Fund (TFDXX), bank deposits, and USDC to ensure liquidity. Through blockchain technology, OUSG shares have been tokenized, allowing for 24/7 transfers and trading.

Minting and Redemption Mechanism: Investors can instantly obtain OUSG tokens through USDC or exchange OUSG tokens for USDC.

Token Versions: Similar to USDY, OUSG is also divided into OUSG (accumulating) and rOUSG (rebase).

Both OUSG and USDY require user KYC support, so Ondo collaborates with the backend DeFi protocol Flux Finance to provide stablecoin collateral lending services for tokens like OUSG that require permissioned investment, enabling permissionless participation in the protocol's backend.

BlackRock BUIDL: The First Tokenized Fund on Ethereum

Concept

BlackRock BUIDL is an ETF (Exchange-Traded Fund) jointly launched by the globally renowned asset management company BlackRock and Securitize, officially named "iShares U.S. Infrastructure ETF," with the code BUIDL. Similar to USDY, BUIDL is essentially a security; when users invest $100 in BUIDL, they receive a token valued at $1, while also enjoying the investment returns on that $100.

Regulatory Compliance

Unlike many projects in the RWA track, BUIDL has a relatively complete compliance structure. The BUIDL fund is operated by a special purpose vehicle (SPV) established by BlackRock in the British Virgin Islands (BVI), which is an independent legal entity used to isolate the fund's assets and liabilities. Additionally, the BUIDL fund has applied for Reg D exemption under U.S. securities law and is open only to accredited investors.

Underlying Assets

BlackRock Financial is responsible for managing the fund's assets. The fund invests in cash equivalents, such as short-term U.S. Treasury bonds and overnight repurchase agreements, to ensure that each BUIDL token maintains a stable value of $1. Securitize LLC is responsible for the tokenization process of the BUIDL fund, including converting the fund's shares into on-chain tokens. On-chain yields are generated automatically by smart contracts.

Market Response

With the backing of BlackRock's strength and reputation, the BUIDL fund has performed well in terms of market recognition and TVL, stabilizing at $502.41 million, ranking 4th in RWA TVL.

In terms of technical architecture, BUIDL's innovation is not particularly robust compared to other projects, but BlackRock's long-standing reputation in the crypto market is sufficient to secure a place for the project in the RWA track.

In the RWA ecosystem, besides Centrifuge, which integrates traditional lending with DeFi, ONDO Finance and BlackRock BUIDL, there have also been breakthroughs in integrating real estate with DeFi, such as Propbase directly tokenizing real estate assets for circulation and PARCL allowing tokenized investments in neighborhoods or locations.

5. Conclusion

RWA essentially refers to real-world assets, and the fundamental goal of the entire track is to achieve interoperability between real assets and on-chain assets, allowing more real funds to flow into the blockchain while gradually blurring the boundaries between DeFi and traditional finance.

The main tracks of RWA include both tangible and intangible assets. Currently, it focuses on three major areas: securities, real estate, and credit lending.

Compared to other tracks, the RWA track faces greater regulatory scrutiny and stricter compliance requirements, which also gives some well-known companies a significant advantage.

Despite the strong narrative and prospects of the RWA track, due to the uncertainty of its compliance, caution is still needed when investing in related projects to be prepared for potential risks.