Preventing LPs from losing money is the key to the survival and development of DEX

DEX must ensure that LP has sufficient profitability.

DEX must ensure that LP has sufficient profitability.Author: @G_Gyeomm

Compiled by: Shenchao TechFlow

Regardless of the uncertainty in short-term market sentiment, the recent activity of decentralized exchanges (DEXs) keeps us optimistic about the long-term future of blockchain or on-chain ecosystems. Currently, the trading volume of DEXs has reached its highest level since the inception of blockchain. According to data from The Block, as of August 2024, the spot trading volume of DEXs accounts for about 14% of centralized exchanges (CEXs), while data from DeFilama shows that the trading volume executed through DEXs in the past 24 hours is approximately $7 billion.

In the past, the FTX incident increased the custodial risks for market participants, leading to a rise in DEX usage. Such short-term events often temporarily boost DEX usage. However, the increase in DEX usage we are currently witnessing shows a sustained trend. Compared to CEXs, this stable rise in DEX usage can be seen as a result of continuous improvements and significant progress in areas such as usability.

*Source: Spot Trading Volume of DEX vs. CEX (%) *

Among these developments, the DEX component I want to emphasize today is the liquidity provision (LPing) mechanism of automated market makers (AMMs), particularly the constant product market maker (CPMM), which is adopted by most DEXs, where trades are executed through xy=k. Sufficient liquidity provides a smooth trading environment by minimizing slippage; therefore, DEXs must align incentives between the protocol and liquidity providers (LPs) to maintain a continuous state of liquidity provision, which is considered the core of DEXs. In other words, DEXs must ensure that LPs have sufficient profitability.

However, a recent issue that has arisen in AMM DEXs is that "LP losses exceed expectations." The entities causing LP losses are external parties, such as arbitrageurs. As the value generated within the protocol is continuously extracted by external entities, the value obtained by participants operating the protocol decreases. Therefore, the risks of liquidity provision, such as LVR (loss versus rebalancing), have become important topics, and DEXs that eliminate such risks and quickly adopt newly developed technologies are once again receiving attention. Next, we will explore the various attempts of these DEXs and clarify their importance in the recent trends of DeFi protocols.

1. Background - Attempts to Mitigate LP Profitability Risks

1.1 CoW Protocol - MEV Capture AMM

Source: CoW Protocol Documentation

CoW Swap provides a swapping service that protects traders from MEV attacks, such as front-running, back-running, or sandwich attacks, through an offline batch auction system. In CoW Swap, traders do not settle trades directly on-chain but submit their intent to trade tokens to the protocol. When these traders' trades are bundled into an offline batch, a third-party entity called a Solver seeks the best trading paths from AMMs (such as Uniswap, Balancer) and DEX aggregators (such as 1inch). This allows traders to be shielded from MEV and trade at optimal prices.

Source: CoW Protocol Documentation

CoW Swap focuses on preventing value extraction by external traders through batch auction-based trading and Solver intervention. Based on this mechanism, CoW Swap introduces CoW AMM as the next step to protect traders from MEV impacts while also safeguarding LPs. CoW AMM is proposed as an MEV capture AMM that eliminates LVR caused by arbitrageurs.

Source: Delphi Digital

Here, LVR (Loss versus Rebalancing) is a risk management metric that quantifies the losses LPs incur due to asset price fluctuations and the differences between internal asset prices in the AMM and external market prices. In other words, while impermanent loss is another risk of liquidity provision, LVR represents the ongoing cost that LPs bear as counterparties to arbitrageurs throughout the LP period, considering only the opportunity cost LPs may experience due to asset price fluctuations. This requires further explanation, but the fundamental issue to emphasize here is that liquidity providers are affected by adverse trading conditions from external arbitrageurs.

CoW DAO | Don't get milked : CoW AMM uses a function-maximizing AMM (FM-AMM) design to capture surplus for protected liquidity pools through batch auctions. The Solver that provides the highest surplus wins the right to rebalance the pool, thereby capturing LVR for the pool.

To address this issue, CoW AMM is designed to protect liquidity providers (LPs) from external arbitrageurs' interference and internally capture MEV. In CoW AMM, when arbitrage opportunities arise, Solvers compete to bid for the right to rebalance the CoW AMM pool. The specific process is as follows:

LP deposits liquidity into the CoW AMM pool.

When arbitrage opportunities arise, Solvers bid to rebalance the CoW AMM pool.

The Solver with the most surplus left in the pool wins the right to rebalance the pool. Here, surplus refers to the extent to which the AMM curve moves upward, simply put, it is the remaining funds in the liquidity pool that are retained by providing LPs with the most favorable trading conditions. For a detailed explanation of surplus capture AMMs, please refer to this article.

Through this mechanism, CoW AMM can internally capture the arbitrage profits extracted by MEV bots in existing CPMMs, eliminating the LVR risk faced by LPs, while LPs will receive surplus as an incentive for providing liquidity. In other words, unlike existing CPMMs, CoW AMM can treat MEV as a source of income rather than relying solely on trading fees.

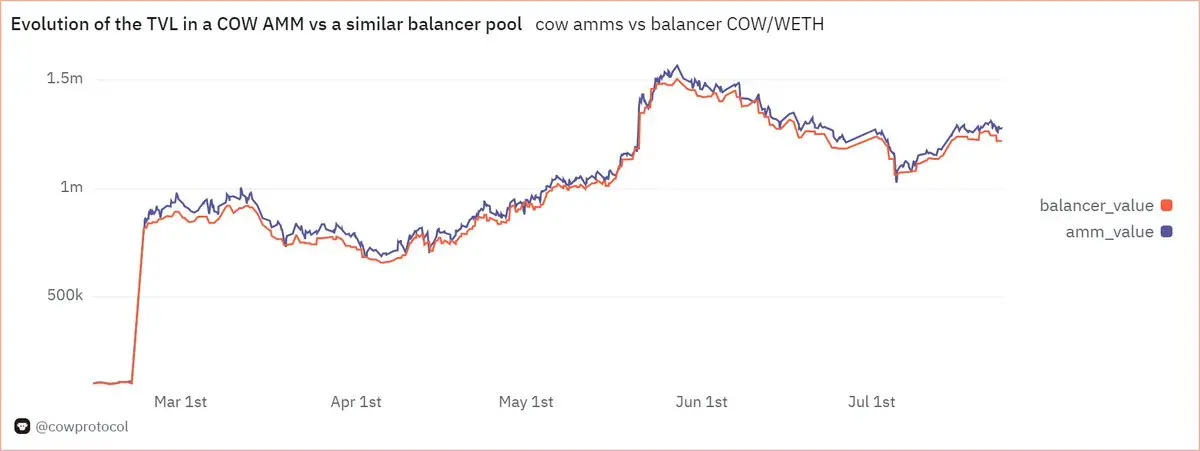

Source: Dune (@cowprotocol)

This CoW AMM is similar to CoW Swap, applying a single price for token buy and sell trades within a specific batch and ultimately adopting a method that allows a batch to form a block. Therefore, it fundamentally prevents MEV based on price differences, such as arbitrage, and minimizes LP's LVR by not providing outdated AMM prices that do not reflect price fluctuations to external arbitrageurs.

1.2 Bunni V2 - Out-of-Range Hooks

Bunni V2 utilizes the out-of-range hooks from Uniswap v4 as another method to enhance LP profitability. The hooks here are one of the architectural upgrades of the upcoming Uniswap V4, allowing the customization of Uniswap's liquidity pool contracts based on different usage scenarios (dynamic fees, TWAMM, out-of-range, etc.).

Bunni V1 was initially a liquidity provision derivative (LPD) protocol aimed at improving the limitations of concentrated liquidity proposed by Uniswap V3, developed alongside Gamma and Arrakis Finance. However, after the release of V2, it built its own DEX by combining various hook usage functions, including out-of-range hooks. Here, concentrated liquidity is a method of liquidity provision that allows LPs to directly determine any price range for liquidity provision, thereby improving the capital efficiency of liquidity provision positions. While this concentrated liquidity improves capital efficiency, its limitation is that LPs must constantly adjust the range of liquidity provision to match changing market prices. Therefore, Bunni provides a solution that automatically manages the range of liquidity provision when LPs delegate their funds.

Source: X (@bunni_xyz)

The out-of-range hooks represent a new attempt to improve capital efficiency by interoperating idle liquidity with external protocols, rather than readjusting the range of liquidity provision when idle liquidity exceeds the current market price range. By depositing idle liquidity into lending protocols and vaults that can generate interest income, such as Aave, Yearn, Gearbox, Morpho, etc., it not only provides LPs with trading fees from liquidity provision but also offers additional returns. Of course, since Bunni's attempt is still in the testing phase, it is essential to closely monitor potential trade-offs that may arise in the future, such as increased contract risks due to liquidity interoperability or the depletion of liquidity required for AMM exchanges, which could come at the cost of capital efficiency.

2. Key Points

2.1 Advantages DEX Can Offer That CEX Cannot

When summarizing the market share of DEXs and the current state of CEXs, an important question arises: why should we use DEXs instead of CEXs? From an objective perspective, considering only the convenience and abundant liquidity of CEXs, it seems challenging to find a compelling reason to mandate the use of DEXs. Even if the usage of DEXs continues to rise, a 14% market share frankly is not substantial.

The FTX bankruptcy incident reminded market participants of the risks associated with custodial exchanges, temporarily stimulating the use of DEXs, but this is merely a temporary substitute. Therefore, as a method to gradually expand the market share of DEXs, it is particularly important to continue attempting to create unique value propositions for DEXs that cannot be experienced in CEXs.

Source: AAVEnomics Update

In this regard, liquidity provision (LPing) and profit redistribution mechanisms are crucial as unique values of DEXs. LPing is not only a necessary condition for providing a smooth trading environment but also generates pathways for passive income through LPing, offering market participants another motivation to engage with DEXs. At the same time, the profit redistribution mechanism could be the starting point for a self-sustaining economic system or token economy, where participants contribute based on token incentives on decentralized protocols and receive rewards, which may be an ideal way to maximize the utility of blockchain and cryptocurrencies.

2.2 Internalizing Protocol Value Becomes Increasingly Important

As the unique value of DEXs is reflected in liquidity provision and profit redistribution mechanisms, internalizing the value previously extracted from external entities (such as arbitrageurs or various MEVs) becomes particularly important. The DEX functionalities discussed in this article aim to address this issue. CoW AMM captures MEV internally to eliminate LP risks, while Bunni V2's out-of-range functionality interoperates liquidity within AMM pools to maximize LP profitability. Although not mentioned in this article, some recent DeFi protocols are exploring attempts to internalize OEV (oracle extractable value) profits based on oracle price information.

Moreover, with the recent re-emphasis on mechanisms that redistribute the value obtained by protocols back to protocol participants, its importance is further highlighted. In fact, the Aave protocol has proposed new AAVEnomics, repurchasing $AAVE through protocol revenue and distributing it to $AAVE holders. At the same time, Uniswap's fee switch has also recently regained attention, and even Aevo announced plans to repurchase $AEVO.

As DeFi protocols attempt to introduce mechanisms for redistributing value, the sustainable revenue model of the protocol and the internally accumulated value become increasingly important. For example, if Uniswap proposes to distribute trading fees to $UNI holders, it needs to share a portion of the trading fees that were previously entirely obtained by LPs with $UNI holders. In this case, the protocol needs to accumulate more value internally to redistribute value to protocol participants, while the importance of internalizing the value previously extracted from external entities is also emphasized.

From this perspective, the differentiated liquidity provision methods proposed by CoW AMM and Bunni V2, or the development of mechanisms that return the value obtained by the protocol to ecosystem participants, are all attempts worthy of close attention. Additionally, various protocols are also developing attempts to improve LPing, such as Osmosis's Protorev to prevent back-running, or Smilee Finance's "impermanent yield" as a method to hedge against impermanent loss risks. The process of DeFi protocols creating unique value through these attempts will continue to be an important focus for gradually increasing DEX activity.