How does Banana Gun siphon millions of dollars from users and Ethereum validators?

The monkey's tricks are still ongoing.

The monkey's tricks are still ongoing.Author: JUGGERNAUT

Compiled by: Deep Tide TechFlow

Last year, I published twoshort articles exploring the origins of the Banana Gun Bot team.

These articles analyzed the flow of funds used to create the Banana Gun Bot on-chain and raised some unsettling questions about the developers' backgrounds. When the background of an anonymous developer of a leading trading bot appears suspicious, the ensuing question is, who does the Banana Gun Bot operate for?

In the micro-cap market, ten months is a long time. In fact, it is also a long time across the entire decentralized finance (DeFi) space. I sat down to reflect on how right (or wrong) my views on the Banana team were. The issues I discovered were much deeper than I initially imagined—and raised serious questions about how Ethereum will operate in the future.

To set the context, let's look at some data.

Since May 2023, TG Bots have been widely adopted in the DeFi ecosystem, becoming a stable business model and making significant contributions to daily on-chain trading volume. Over the past year, the trading volume of TG Bots accounted for 20% - 30% of the total Ethereum trading volume, calculated as a percentage of transaction count. As of June 2024, the trading volume of all TG Bots accounted for 9.4% of Ethereum's trading volume, coming from nearly 5.3% of Ethereum wallets. Therefore, TG Bots like Banana have now become significant transaction initiators on Ethereum and play an important role in the Ethereum ecosystem.

Since June 2023, at least $5.25 billion in capital has flowed through the Banana Gun router. While part of this was on Solana, it places Banana second in this category, only behind Maestro (the first participant in the field, leading competitors by over a year) and Bonk Bot (seen by some as a bet on the entire SOL junk coin ecosystem).

Observers are puzzled by the speed at which Banana has captured market share. The primary reason for establishing this overwhelming dominance is the success rate of Banana Gun Bot's sniper bundles. In its early days, Banana became the preferred bot for users who wanted to snipe rather than just trade. In the world of junk coins, where the trading lifecycle typically lasts only a few hours, being the first to enter at "Block 0" is often the only thing that matters.

Simply put, the Block 0 of a token refers to the block in which that token "opens for trading" at launch, and sniping a token at launch means your buy transaction needs to be executed immediately after the token developer's "open trading" transaction. To achieve this, since its launch in late May 2023, Banana Gun has suppressed all competitors by "bundling" user bribes. These bundled transactions are more profitable for Ethereum developers as they enhance and aggregate the tips paid to developers.

This strategy of Banana Gun has been so effective that from June to October 2023, the "Block 0" dominance of Banana Gun users rose from 7% to winning 88% of the first sniper bundles in the TG Bot space compared to the industry-leading TG Bot "Maestro" (operating since mid-2022).

Source: The Scientific Crypto Investor and Duncan | Flood Capital

A new market reality is forming—in this reality, ordinary junk coin investors are doomed to fail by choosing Banana's competitors. If you want to enter first, you must join a Banana Block 0 bundle. Among the Banana user community, a culture of paying high bribes is gradually forming, initially mocked on crypto Twitter but quickly accepted as a fait accompli.

Source: Banana Gun TG

In fact, the high-bribe culture among Banana users is seen as a hallmark of its commercial success and is considered a value indicator for $BANANA token holders. Of course, one characteristic of the Banana user bribery culture is that even in bundled transactions, it is a form of PvP (player versus player) competition, where well-funded users enter the token first, while smaller bribe payers provide exit liquidity for leading Banana users.

The Banana team itself admits that the bot was initially created for a small circle of "friends," but was later opened to the public due to its development team's apparent fervor for decentralized communism.

Source: Banana Gun X Handle

It is worth mentioning that the allegations that the Banana team has been front-running trades by monitoring user bribes have yet to be clarified. Regardless, the second aspect of Banana Gun Bot's dominance in sniper bundles is beginning to evolve into a case study for the entire Ethereum ecosystem.

Separation of Proposers and Builders

When Advantage Becomes Status Quo

In September 2023, the Banana Gun Bot team launched the $BANANA token, promising to share 40% of the revenue generated by the bot with users. By November 2023, Banana Gun Bot had already captured over 90% of all Block 0 snipes, far ahead of its competitors in adoption and revenue generation. According to sources, by December 2023, the Banana team executed a brilliant strategy. In ETH junk coin trading, Banana normalized the high-bribe culture, leveraging its Block 0 dominance to exploit a long-theorized but unrealized systemic weakness in Ethereum, cleverly transforming its early lead in the TG Bot market into an economic moat against competitors.

Understanding this process requires a basic understanding of how Ethereum operates post-merge—particularly the concept of "Proposer-Builder Separation" (PBS). For those like me who do not understand but want to learn about the concepts behind PBS, I have a separate note that can be found here.

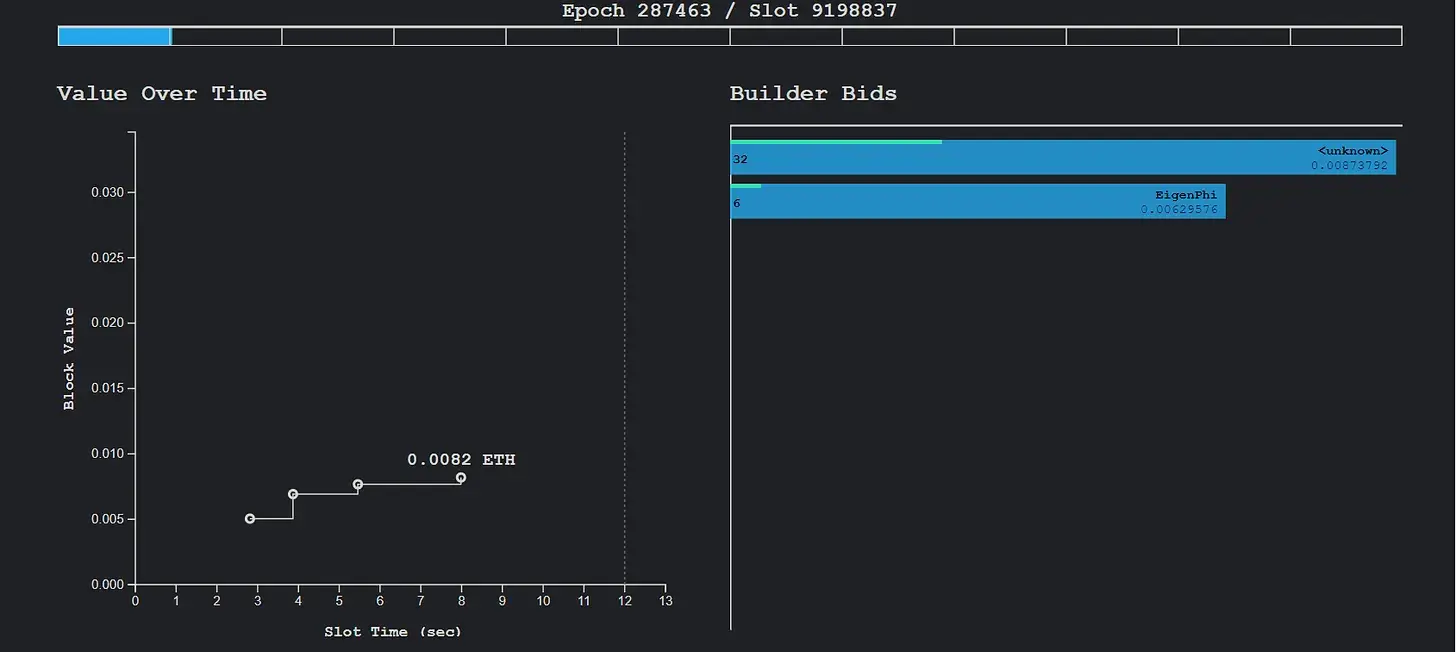

Typically, in a healthy competitive PBS-based block building market, transactions initiated by TG Bots are allocated to various builders, who take pending transactions from the transaction memory pool, optimize them to maximize value, build blocks, and bid to proposers to ensure their own blocks are included. This transaction process can be visualized in real-time on Payload during the 12-second lifecycle of a block.

In an ideal scenario, in an open competitive bidding process, proposers earn the highest fees by selecting the best bids among competing builders. Thus, value is redistributed back to the Ethereum ecosystem (as proposers stake ETH and secure the Ethereum chain), while builders are also compensated competitively (as they transfer most of the transaction fees to proposers).

The problem is that the competitive nature of the block building market may be constrained by various factors. Last year, the Special Mechanisms Group pointed out in their paper “Concentration Effects” (Gupta et al., 2023) that over time, a small group of savvy builders will naturally dominate PBS. Interestingly, they proposed in May 2023 that this concentration trend primarily stems from "block top" opportunities, such as CEX-DEX arbitrage.

"Block top" refers to the first few transactions executed in each block. CEX-DEX arbitrage refers to professional traders exploiting price differences between tokens on centralized exchanges (like Binance) and decentralized exchanges (like Uniswap). SMG noted that the advantages of block top opportunities in PBS are primarily monopolized by builders rumored to be associated with high-frequency trading firms (HFT), such as Manta, Rsync Builder, and Beaver Build. Compared to these HFT-backed builders, the SMG team also analyzed Blocknative, Builder69, and Flashbots as other high-volume but non-HFT builders, validating their hypothesis. Ironically, SMG mentioned Titan Builder's paper in June 2023, demonstrating that these top builders receive more order flow, leading them to dominate PBS auctions.

Visualization of HFT-backed builders' PBS advantages

One important conclusion drawn by SMG is that "builders who earn more from block tops are more willing to pay more for private order flow, as they need to win the entire block to leverage their block top advantage." Therefore, SMG envisioned a scenario where savvy, HFT-funded builders could form a monopoly in PBS if they secured private order flow to solidify their lead. In doing so, they would suppress smaller builders—just as Titan Builder contemplated in its June 2023 paper (the young Titan's public RPC only went live on April 17, 2023).

So, what is private order flow?

The rebellious rise of junk coins in 2020 created a systemic issue for Ethereum—"MEV." Over the past three years, transaction senders have become increasingly reluctant to send transactions to the public Ethereum pending transaction pool, instead turning to private pending transaction pools to avoid being front-run by MEV bots. To some extent, private pending transaction pools provide protection for transaction senders, thus constituting a public good. TG Bot transactions are seen as premium trades for MEV bot operators, as their users are typically advised to set high slippage to ensure their trades succeed in high-volatility tokens.

To guard against this possibility, nearly 97% of TG Bot transactions are conducted through these private pending transaction pools. However, this is not the type of transaction that SMG refers to when expressing concerns about HFT firms monopolizing the PBS system. The "private order flow" mentioned by SMG refers to order flow from a single transaction initiator, specifically sent to a single builder.

First, TG Bots provide users not only with sniping services but also with regular buy and sell transactions, including on-chain limit orders. However, Banana's business model is primarily rooted in its "sniping" narrative. Its high Block 0 bribe culture drives its strong revenue stream. Therefore, Banana's business model is based on assuring users that they will enter token trades before any competitors. Typically, to maximize the chances of a successful Block 0 bribe bundle on-chain, such initiators will send their users' bundles to all leading builders on Ethereum.

For example, suppose you and I, as Ethereum builders, receive the same 10 ETH bundle from a TG Bot, which includes a 5 ETH "tip" to incentivize that bundle to be prioritized in the block over all others. I build a potential block, and you build one too. I bid 1 ETH, and upon seeing that, you bid 1.1 ETH, and so on, until the entire 5 ETH is exhausted. In this case, ultimately, this 5 ETH will be sent to the proposer, rather than pocketed by some builder.

Note: This example assumes no other TX is sent to the builder.

Logically, when TG Bots send their bundles to multiple builders, they can maximize the chances of that bundle being included in the winning block and being put on-chain, as builders compete with each other to ensure their blocks are accepted by validators. On the other hand, sending exclusive order flow (EOF) to a single builder means that builder must successfully put the order flow (and bribe) on-chain. Any delay would undermine this advantage—the bundle would no longer be a sniper. Therefore, initiators like Banana should ideally provide order flow to at least the builders with the highest inclusion rates on-chain. From SMG's research at the launch of Banana, it is evident that builders like BeaverBuild, along with other HFT-backed builders, would be the ideal EOF recipients for Banana. But as we will see next, the Banana team chose a different route.

As of June 2023, the PBS market. Source: SMG

One indirect effect of providing Banana order flow exclusively to a certain builder could be as follows.

When high-bribe bundles are specifically sent to a certain builder, other builders cannot access that bundle and thus cannot receive its bribe. The chosen builder's rational strategy is to gradually raise their bid to ensure they only need to pay the minimum amount to the proposer to include that bundle in the next block. Therefore, if a Block 0 bundle with a 5 ETH bribe is routed via EOF, while the highest block bid from competing builders is 1 ETH, the exclusive builder can bid "just enough" to secure that block (e.g., 1.1 ETH) and keep the remaining 3.9 ETH as pure profit.

What does the Banana team gain from providing EOF to a single builder? The answer lies in the potential kickback from the profits that builder brings. This EOF arrangement means that the builder can return part of the bribe to Banana (as payment for the EOF), so now Banana profits not only from transaction fees but also from the high bribe culture generated among its users. This is not a novel business model—Robinhood Markets in the U.S. was paid hundreds of millions by Citadel for "order flow payments."

Source: Ethereum Block 19238546

Q: Did the Banana team disclose the existence of such an EOF agreement?

A: No.

Q: As the issuers of the $BANANA token and custodians of the project treasury, did the Banana team redistribute excess bribes to its users or $BANANA token holders?

A: Absolutely not.

Q: But more importantly, in 2023, did the Banana team execute EOF agreements with the Ethereum builders with the highest market share in block building to ensure users had the best chance of getting their bribe's Block 0 bundles on-chain in good faith?

A: Strangely, no.

'Behind-the-Scenes Deals in the Dark Forest'

Analysis of transactions through the Banana Gun router shows that the Banana team has routed its sniper bundles almost exclusively through Titan Builder most of the time.

Titan had only a 1% market share in the PBS block building market in April 2023. When the Banana team began directing exclusive order flow (EOF) to Titan, Titan's performance in the PBS market lagged far behind other builders. Notably, in the seven days prior to the publication of this article, Titan contributed nearly 40% of all Ethereum blocks.

In short, in less than a year, Titan has become:

The second-largest builder on Ethereum, and

The most profitable builder in the Ethereum PBS ecosystem, largely thanks to the Banana Gun team's EOF support.

Source: libMEV

A closer look at the data in the graph above on libMEV reveals the true scale of Titan's success.

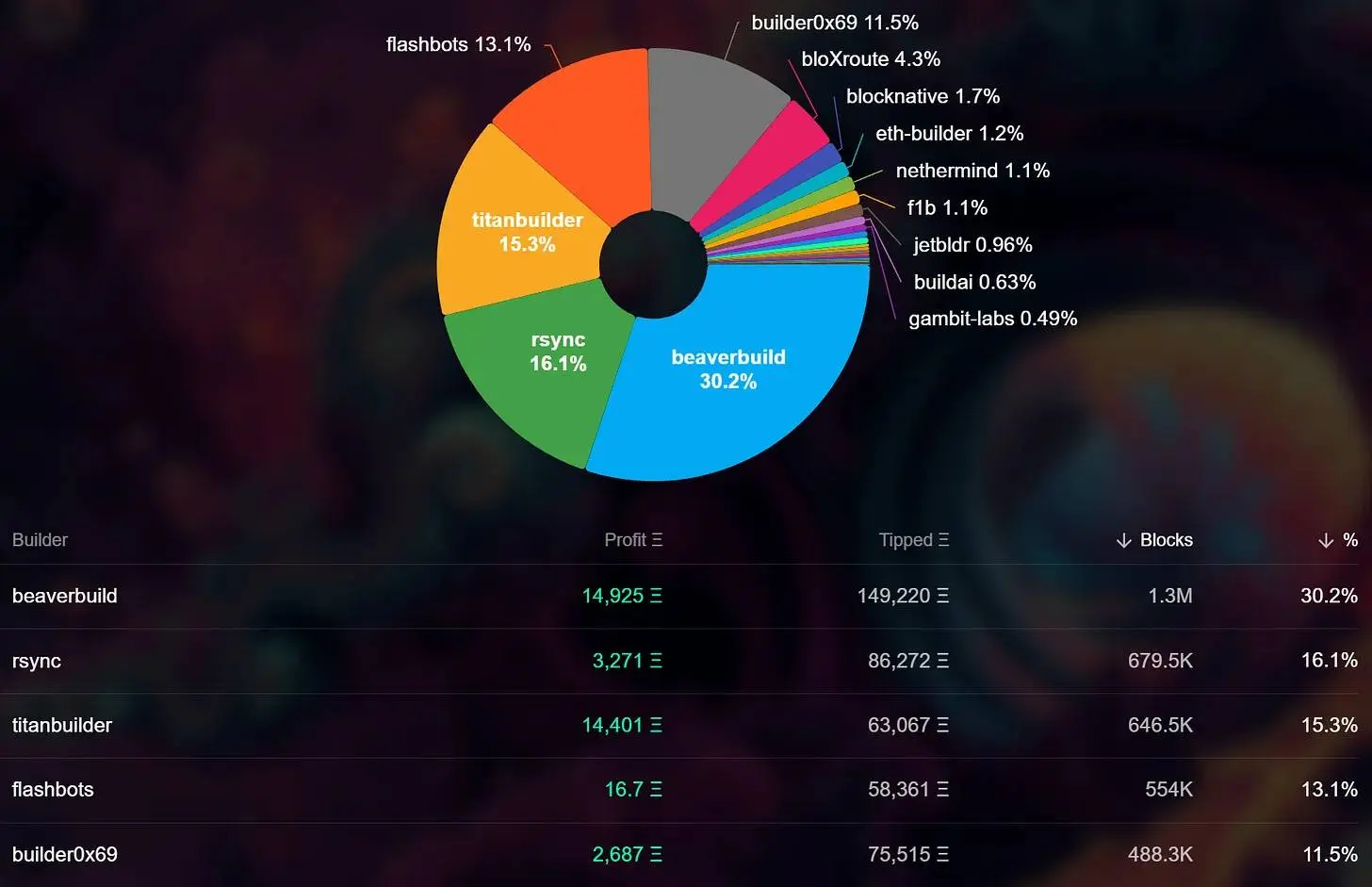

Beaverbuild is the leading block builder in post-PBS Ethereum. Since the merge, it has built over 1.2 million blocks, earning Ethereum validators 146,241 ETH, while generating 14,520 ETH in profit for Beaverbuild.

For example, the Flashbots builder has delivered over 552,800 blocks, earning 16.7 ETH in profit while transferring 58,349 ETH to the Ethereum ecosystem through its validator fees. In contrast, Titan has delivered 615,200 blocks since May 2023, earning 13,151 ETH in profit while transferring 60,912 ETH to the Ethereum ecosystem.

By doing so, Titan's profits are nearly 787 times that of Flashbots builders, while the number of blocks delivered is slightly more than that of Flashbots. Similarly, while Beaverbuild retains about 9% of the ETH from user-paid building blocks, Titan has already secured 17.75% of ETH as its profit, despite delivering less than half the number of blocks as Beaverbuild!

A recent excellent paper by Markovich (May 2024) delves into this arrangement. She cites block 19728051 (referred to as block 8930981 in the paper), which had a total value of 76.38 ETH, a total priority fee of 4.54 ETH, and a total bribe paid to Titan of 72 ETH.

Source: “Decentralized Monopoly Power in DeFi”, Sarit Markovich

Sarit points out that in block 19728051, proposer Lido could only earn 19.75 ETH from that block, while Titan, through its EOF agreement with the Banana Gun team, secured a pure profit of 56.6 ETH.

Sarit analyzed 181,651 blocks between April 6 and May 5, 2024. She studied both Banana and Maestro, but the latter team is not relevant to this article as it has no token and does not promise any benefits or profits for token holders to maintain their investments in its ecosystem. Sarit reported that in her dataset, the total block value was 21,406 ETH, of which only 17,127 ETH was transferred to the Ethereum ecosystem through its proposer. Thus, the proposer lost 4,279 ETH during this short period. Specifically, Lido did not receive a payment of 1,666 ETH in a single month within this dataset.

This paper supports my preliminary calculations when reviewing over 3,500 blocks on the Ethereum chain between December 2023 and March 2024, where Banana Block 0 bundles were almost exclusively routed through Titan Builder. This indicates that out of the total amount of 4,466.89 ETH that Banana users paid to get their sniper trades on-chain, only 2,915.65 ETH was transferred to Ethereum proposers, while 2,271.26 ETH was monopolized by Titan Builder. Even assuming that the private EOF between Banana and Titan was split 50-50, it can be inferred that during this period, 1,135.63 ETH was sent back to the private accounts of the Banana Gun team. These would be unreported profits amounting to millions of dollars, coming from innocent users who were guided into a high-bribe culture by the Banana Gun team.

Source: libMEV

Conclusion

An unidentified team, with a suspicious background,

Allegedly monitoring user trades to front-run them (using them as their own exit liquidity),

Now extracting millions from an apparent exclusive order flow arrangement, rather than paying it to Ethereum validators or distributing it to $BANANA holders,

While creating a concerning concentration effect that pressures the entire Ethereum PBS system,

Moreover, the $BANANA token was listed on Binance, granting their brand significant legitimacy in the public eye.

Thus, the monkey business continues.

Risk warning Risk warning

Risk warning Risk warning