Is there currently a bubble in AI investment? - An analysis from the perspective of supply and demand

Web3 AI Deep Report

Web3 AI Deep ReportAuthor: Dylan Wang

Key Points of the Report:

Riding the Wave: Both supply and demand are working together to drive continuous transformation in the AI field. On the demand side, more and more companies are beginning to adopt AI tools and plan to invest further in AI. At the same time, the expanding Generation Z and Generation C will further stimulate the potential demand for AI. On the supply side, the productivity-enhancing effects of AI are remarkable, and the continuous decline in costs further unleashes supply-side potential.

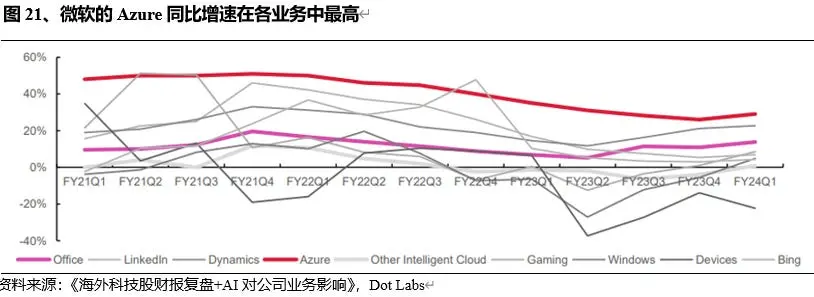

Learning from History: A comparison with the internet bubble of the 2000s. First, the current valuation levels are not as high as those in 2000. Second, the current profitability of companies is fundamentally different from that in early 2000. In early 2000, the net profit margin of the Nasdaq 100 was poor, with the lowest below -30%, and the entire tech industry was in a state of loss. In contrast, the current rise driven by AI is supported by performance. At the industry level, Bank of America expects that AI strategies will drive operating margin expansion in 24 out of 25 industries over the next five years. At the company level, taking Microsoft as an example, its AI business Azure has the highest year-on-year growth rate among all its businesses.

Therefore, we are still riding the wave of the AI revolution. Although AI has already gone through a wave of hype, the market believes that the current capabilities of AI have been fully explored, lacking breakthroughs for large-scale applications, the development of AI is multi-layered and multi-wave. For example, according to the capabilities of foundational large models, we are currently in the second phase of AI, with many breakthroughs to look forward to, such as multimodal, AI agents, spatial computing, and embodied intelligence. In the face of a new generation of technological revolution centered on AI, we should put aside our mental burdens and embrace this new generation of technological revolution!

Full Text:

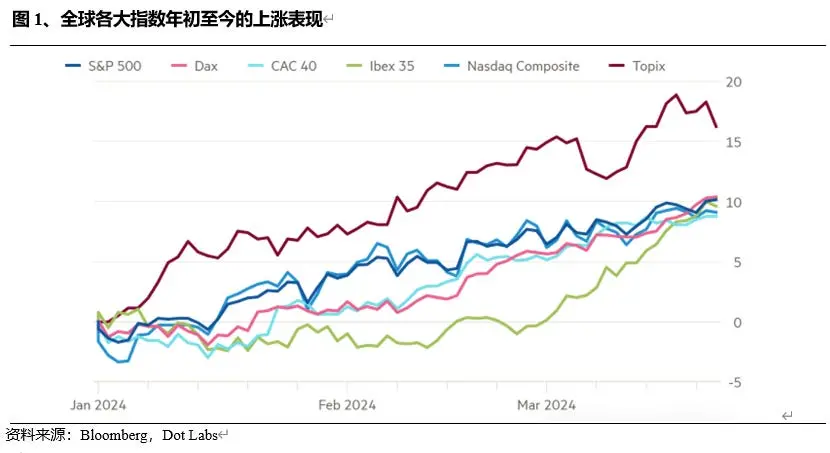

The MSCI All Country World Index has risen 7.7% this year, the highest increase since 2019, driven by the booming concept of artificial intelligence. Chip design company Nvidia added over $1 trillion in market value in the first three months of this year, accounting for about one-fifth of the total rise in the global stock market during the same period. As AI concept stocks continue to climb, doubts have begun to emerge more frequently. The loudest question is whether the hype around AI is excessive. In October 2023, global tech research and consulting firm CCS Insight released a forecast report stating that the booming generative AI field will face a reality check in 2024. This will manifest as: the gradual fading of tech hype, rising operational costs, increasing calls for regulation, and investors no longer being as excited and optimistic as before. Does generative AI truly possess disruptive potential? Is artificial intelligence a bubble?

I. Both Supply and Demand are Working Together

1. Demand Pull

(1) AI applications across industries are gradually taking shape, and demand for artificial intelligence may see an explosion

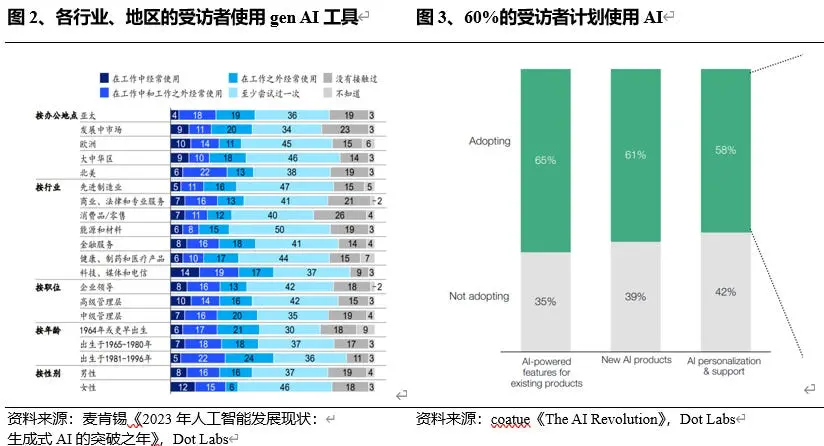

Overall, companies in various regions and industries are increasingly using AI. A 2023 survey by McKinsey indicates that although generative AI has only recently entered the public eye, it has already sparked interest among business professionals: everyone is trying to use generative AI both at work and outside of it. 79% of respondents indicated that they have encountered generative AI at least in their work or outside of it. 22% of respondents stated that they frequently use generative AI in their work. COATUE also reported that 60% of respondents plan to use AI.

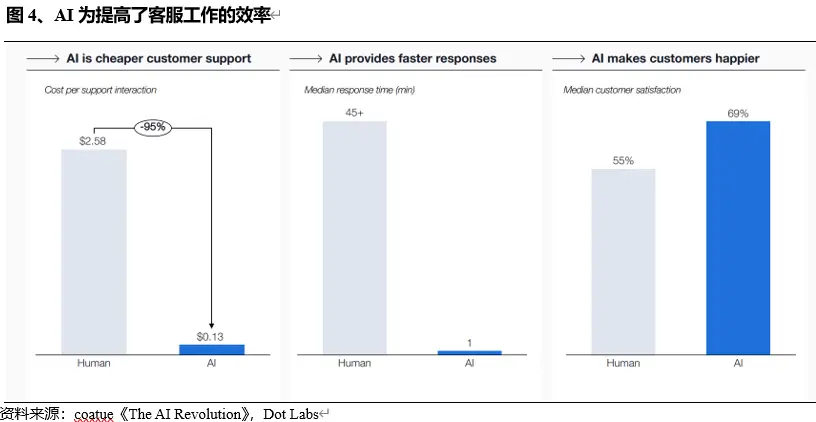

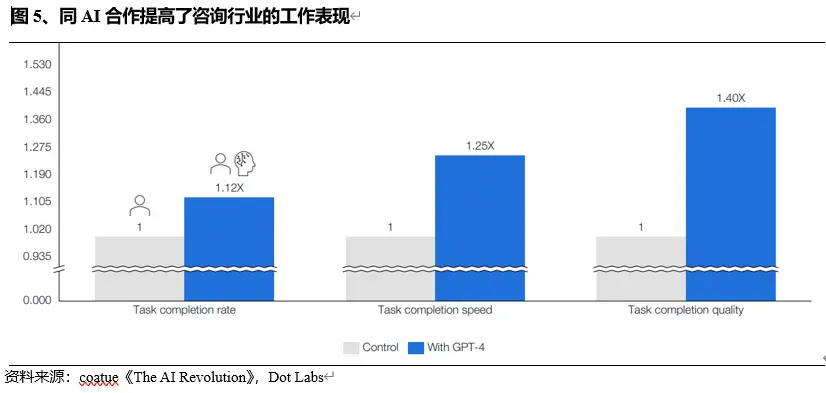

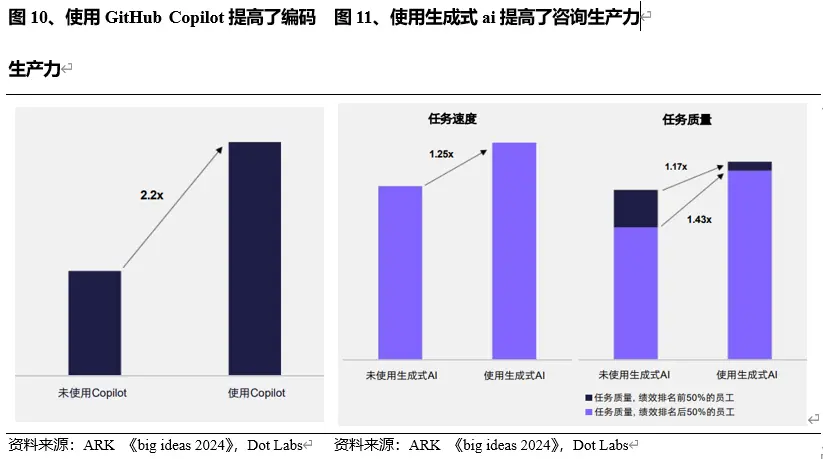

From an industry perspective, AI has shown considerable performance in replacing human labor, and the process of AI replacing human roles is expected to continue. A company named Finicch has used AI for customer service, saving 95% of labor costs; reducing response time from 45 minutes to 1 minute; and increasing customer satisfaction from 55% to 69%. Additionally, knowledge-based work such as consulting will also be transformed by AI. Research shows that BCG consultants perform better on all tasks after using AI, with work quality improving by 40%.

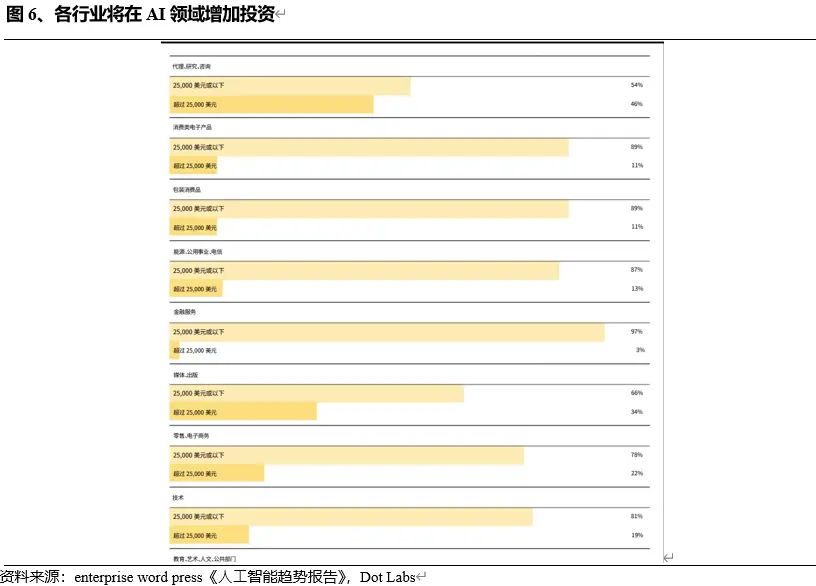

Based on the strong performance of AI, companies across industries will increase their investments in AI. According to a report by Enterprise WordPress, half of the respondents in the research and consulting industry indicated that they plan to invest over $100,000 in AI next year.

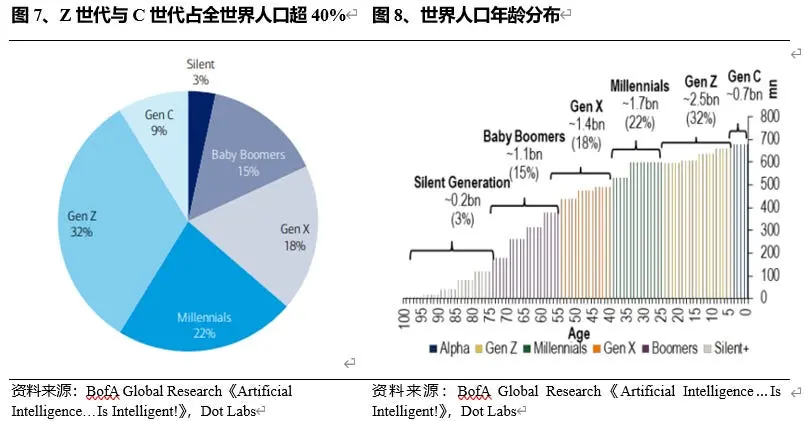

With an aging population, the proportion of Generation Z and Generation C in the population is increasing, and the adoption of artificial intelligence should also rise, as these two generations, especially Generation C, cannot escape online interactions in most aspects of their lives. Even 40% of Generation Z's social interactions are online. By the end of 2021, the number of Generation C was 700 million, accounting for 9% of the world's population, and is expected to reach 2 billion by 2025, accounting for about 20%. However, due to declining birth rates, its scale will be smaller than that of Generation Z.

Compared to older generations, Generation Z and Generation C will adopt a more open and proactive attitude towards the new era of artificial intelligence.

2. Supply Side Drive

(1) AI significantly improves productivity

The large number of jobs created by artificial intelligence may enhance labor productivity, thereby significantly promoting global economic growth. AI-driven automation can improve global productivity and domestic GDP through two channels.

First, most occupations that workers engage in will be partially affected by AI automation, and after adopting AI, they may use at least part of their freed-up capacity for productive activities. This dynamic can be observed in companies that have already adopted AI; research shows that after adopting AI, the annual growth rate of labor productivity can increase by 2-3 percentage points over several years.

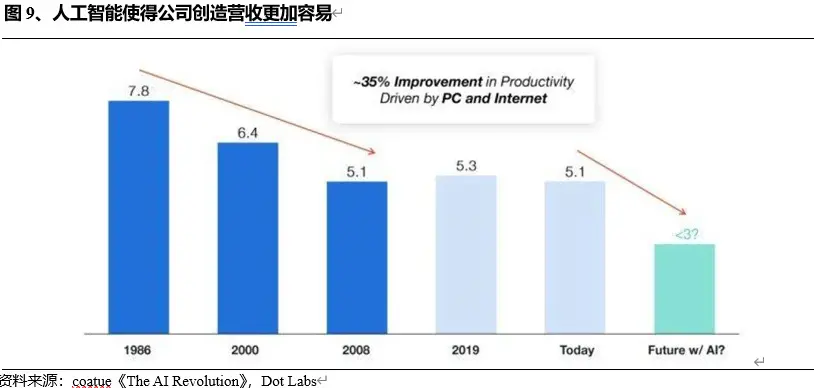

Economists estimate that the widespread application of AI (assuming it will be achieved within 10 years) could increase the annual growth rate of U.S. productivity by 1.5 percentage points over 10 years and raise the trend growth rate of real GDP by 1.1 percentage points over the same period. Another comparison is that in 1986, S&P 500 companies needed to hire about 7.8 people to generate $1 million in revenue, while now it is 5.1 people, and in the future, in the AI era, this number will be less than 3 people.

AI coding assistants like GitHub Copilot and Replit have improved software developers' productivity and job satisfaction. AI agents are enhancing the performance of knowledge workers.

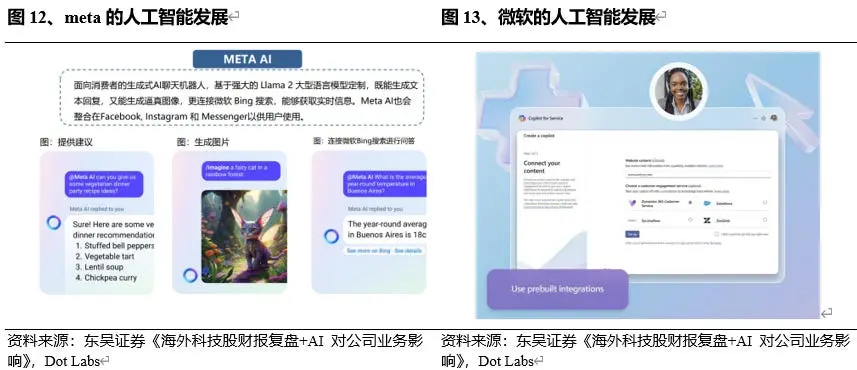

At the enterprise level, AI is also continuously advancing quality enhancement and efficiency improvement. Meta: 1) Improvements in AI algorithms have led to a 25% year-on-year increase in viewing time for video content in Q4; 2) Personalized recommendations have enhanced user engagement; 3) META AI assistant and some conversational AI products have been launched in the U.S.; 4) Currently testing over 20 AI features in products, expecting to enhance user participation in the future.

Microsoft: Several software products under Microsoft have integrated AI features. For example, Microsoft Copilot for Sales can update data in real-time, create personalized sales content, engage in personalized interactions with customers, improve customer interaction processes, and enhance team collaboration. Microsoft Copilot for Service is an intelligent assistant aimed at customer service personnel. It can connect with Outlook, Teams, and external platforms like Salesforce and ServiceNow to create automated tasks, etc.

(2) AI provides more upward potential for the stock market

Goldman Sachs stock strategists Ryan Hammond and David Kostin believe that the potential productivity gains associated with artificial intelligence may provide more upward potential for the U.S. stock market.

Based on assumptions in the Dividend Discount Model (DDM), the estimated compound annual growth rate of earnings per share for the S&P 500 index over the next 20 years will be 5.4%, which is 50 basis points higher than the 4.9% excluding AI impacts. The widespread application of artificial intelligence will result in an 11% increase in earnings per share for the S&P 500 index over 20 years.

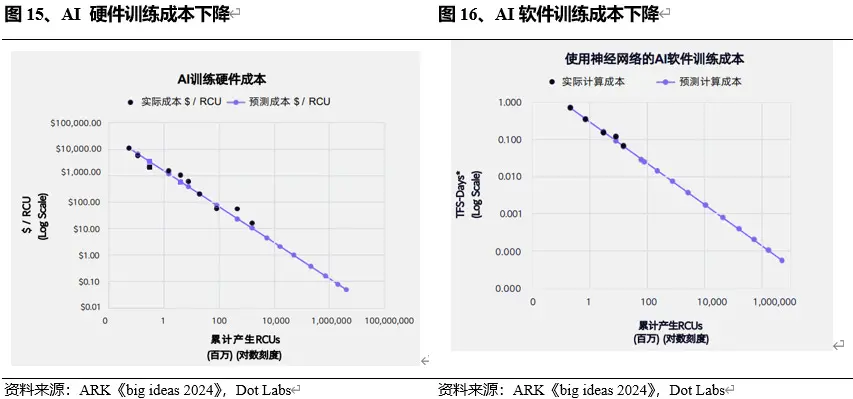

According to Wright's Law, improvements in accelerated computing hardware will reduce the production cost of AI relative computing units (RCU) by 53% annually. Additionally, enhancements in algorithm models can further lead to a 47% annual decrease in training costs. By 2030, the integration of hardware and software could reduce AI training costs at an annual rate of 75%.

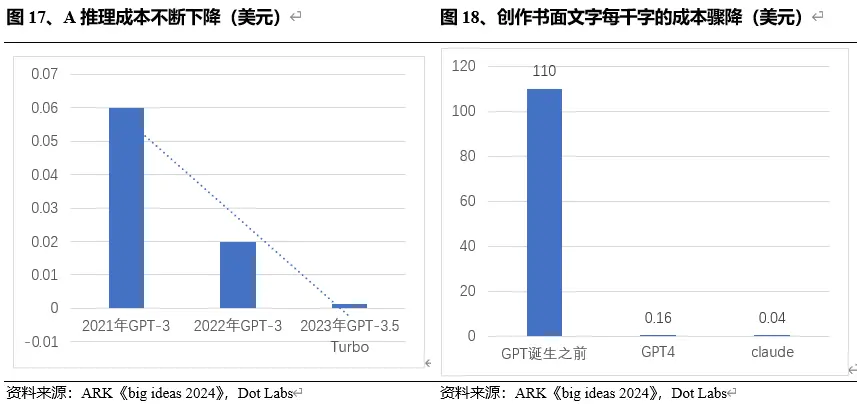

At the same time, the reasoning costs of AI are also continuously declining, with a decrease of up to 80%. The reasoning costs associated with GPT-3.5 have significantly dropped compared to GPT-3 from two years ago. The cost of creating written text has also plummeted from $110 per thousand words in the non-AI era to the current $0.16 or even $0.04.

II. Comparison with the Internet Bubble of 2000

First, regarding market fundamentals, the current valuation of U.S. stocks is already quite high, but it is not as high as the levels around 2000. The price-to-earnings ratio of the Nasdaq index reached around 60 times in early 2000, far exceeding the long-term average; the price-to-earnings ratio of the S&P 500 index also reached around 40 times during the same period, with the cyclically adjusted price-to-earnings ratio around 44 times. Moreover, in early 2000, the net profit margin of the Nasdaq 100 was poor, with the lowest below -30%, and the entire tech industry was in a state of loss, with the market fundamentals lacking strong revenue support.

Currently, the price-to-earnings ratios of the S&P 500 index and the Nasdaq index are not as high as those around 2000. The current S&P 500 index is about 25 times, and the Nasdaq index is 40 times, which does not reach a very high valuation level. From the performance of leading companies, such as Apple, Amazon, and Microsoft, which have relatively stable profit models and strong cash flows, comparisons with the levels around 2000 can be made. Among the S&P 500 constituent companies, 75% exceeded market expectations for earnings per share in the fourth quarter of last year, higher than the historical average of 63%. From a fundamental perspective, the current valuations also reflect the actual profitability, market position, and cash flow of companies, rather than being purely market speculation.

The main cause of the internet bubble in 2000 was that stock prices lacked actual earnings support. However, the current AI trend can indeed enhance companies' profitability.

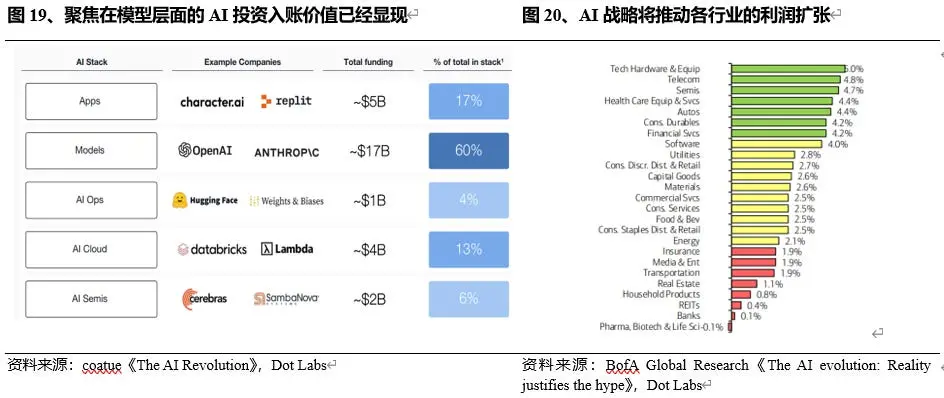

At the industry level, Bank of America’s Global Research Department conducted a survey of 114 fundamental stock analysts to study the impact of AI on various industries worldwide. The survey found that about three-quarters of the 3,500 companies with the largest market capitalization globally will experience AI-driven financial impacts over the next five years. Analysts expect that the AI implementation strategies of the companies studied will drive operating margin expansion in 24 out of 25 industry groups over the next five years. The industries most likely to experience the largest operating margin growth are technology hardware (+5%), telecommunications (+5%), and semiconductors (+5%), while the industries expected to see the smallest percentage increase in operating margins are banking (+0.1%), real estate investment trusts (+0.4%), and home products (+0.8%). Pharmaceuticals, biotechnology, and life sciences are the only industries where analysts expect operating margins to contract due to AI implementation.

At the company level, AI business can contribute to a company's profitability. For example, Microsoft's AI contributes 6 percentage points to Azure's growth rate, with 3 percentage points contributed in FY24Q1, exceeding market expectations. Over the past three fiscal years, Azure and Office have accounted for the largest share, and the development of AI can directly lead to revenue growth in these two areas.