Three key words for the first half of 2024: GameFi, BTC Layer 2 Network, and DePin

In the first half of 2024, the cryptocurrency market shows a trend of diversification, with three major sectors standing out: Gamefi, Bitcoin Layer 2 networks, and decentralized physical infrastructure (DePIN).

In the first half of 2024, the cryptocurrency market shows a trend of diversification, with three major sectors standing out: Gamefi, Bitcoin Layer 2 networks, and decentralized physical infrastructure (DePIN).Abstract

In the first half of 2024, the cryptocurrency market has shown a trend of diversification, with three major sectors—GameFi, Bitcoin Layer 2 networks, and Decentralized Physical Infrastructure Networks (DePIN)—standing out prominently. GameFi, as the most mature sector, although susceptible to market fluctuations, has its ecosystem's continuous prosperity providing strong support for the application and implementation of cryptocurrency in daily life. Bitcoin Layer 2 networks, although a newcomer, are developing rapidly. Layer 2 solutions represented by the Lightning Network are continuously deepening and improving, significantly enhancing transaction efficiency and network throughput, effectively addressing the scalability issues of the Bitcoin mainnet. The DePIN sector demonstrates a high degree of integration with the real world. By introducing decentralized concepts into traditional physical infrastructure, DePIN is expected to promote the digital transformation of traditional industries and open new directions for the future development of decentralized technologies.

1. GameFi Sector

1) Overview of the GameFi Market

In the past five years, GameFi has been regarded as the best field for connecting Web2 users with Web3. During this period, many phenomenal products have emerged in GameFi, such as Axie Infinity, as well as AAA titles created in Web3 by major companies, like ILV. These projects have received substantial funding. However, the reality is that over the past five years, a total of 2,817 Web3 games have emerged, with the lowest failure rate reaching 45.9% (according to network data). It can be said that by the end of the bull market, most games had ceased operations or lost their activity. This indicates that success in the GameFi field is not easy and requires overcoming many challenges.

Network Statistics

As of the first half of 2024, in terms of the number of games, the GameFi sector has reached a peak, totaling over 3,285 games. In fact, the number of online games in the first half of 2024 even exceeded the total number of games in the past five years. Therefore, overall, the GameFi sector was in a phase of vigorous development in the first half of 2024. The market capitalization peaked at $41.25 billion on March 12, 2024. However, due to the overall market conditions, the market capitalization has been continuously declining, currently at $18.69 billion (as of June 30, 2024).

Emerging Trends and Innovative Projects in the GameFi Market

In this round of the bull market, significant innovations have occurred in various aspects. The original X-to-Earn economic model has fallen into a spiral deadlock, where the balance between earning and spending is hard to achieve. The roles participating in GameFi include players, teams, and project parties. If only individuals or teams are earning without spending players participating, it is likely to create significant selling pressure in the later stages of the project, making it difficult for the project to continue, or even putting it in a soft rug state.

Starting in 2024, with the rise of projects like PEPE, it can be seen that insiders are more inclined towards projects with community consensus, no longer blindly believing in the myth of venture capital. More traffic is directed towards fully circulating projects, which are more favorable for retail participation. GameFi has also been inspired to adopt a free-to-play-to-earn model. Everyone can participate for free, without additional costs or high startup equipment fees; all that is needed is a mobile phone to participate in the game and gain utility value through gameplay, with the opportunity to earn money. This model aligns better with the interests of most people. For example, Not in the Ton ecosystem is a popular product adopting this model.

NOT Game Page

Key Factors Attracting Users

The ability of GameFi to attract a large number of users hinges on two key factors: playability and wealth effect. First, the playability of the game is an important factor in attracting users; only interesting, challenging, and easy-to-learn games can retain players. Secondly, the wealth effect is the core appeal of GameFi, where players can gain real economic returns through participation in games and investments. This mechanism of wealth appreciation attracts more people to participate. The new mini-games in the TG track indeed meet the above two important conditions, becoming a new trend in GameFi development.

2) Data Analysis of GameFi in the First Half of the Year

Number of Protocols and Growth Rate

In the first half of 2024, the number of protocols within GameFi slightly increased, from about 2,800 to around 3,200. As for the growth rate of DAOs, it is related to specific events and extreme market conditions, mostly remaining at a mid-to-low level, around 0.1% to 0.3%. This indicates that overall, based on the solid foundation laid in 2023, the number of protocols in the GameFi sector and the growth rate of DAOs are relatively stable, without significant explosive growth.

Market Capitalization and Active Users

According to Footprint data analysis, in the first half of 2024, the market capitalization of GameFi remained consistent with that of Bitcoin, steadily rising. However, starting in April, the market capitalization began to decline, and the decline was much greater than that of Bitcoin. This indicates that the market capitalization trend of GameFi has a certain correlation with that of Bitcoin, but during the decline, GameFi's performance was weaker.

Regarding active users, the active user data in the gaming sector maintained a relatively healthy growth trend. Overall, it kept a rapid growth rate in the first half of the year. However, affected by market fluctuations, the active user data remained at that level after the peak in early April, with little growth and even a slight decline at one point.

Transaction Volume and Transfer Numbers

As for Txns (transaction volume), it is one of the important indicators of on-chain activity. Compared to the continuously increasing number of active users, the number of transfers experienced a slight peak between February and March, then continued to decline.

This change in transfer numbers may reflect the behavioral patterns of users participating in GameFi and the influence of market trends. During the small peak period in February and March, it may have been due to specific activities, the launch of new projects, or market hotspots, leading to increased transfer activities among users. However, the subsequent decline may be due to changes in market sentiment, the weakness of specific projects, or adjustments in investors' risk preferences towards the GameFi sector.

Let's take a look at the latest daily data, with daily active users around 2.64 million, the latest daily transfer number about 12.96 million, and daily transaction volume around 9.44 million, indicating that despite the market cooling, the GameFi market can still maintain a certain number of online users.

Finally, let's look at the distribution of the gaming sector across various chains. Since 2021, the top three chains remain Ethereum, BNB, and Polychain. However, starting in 2024, gaming projects have gradually begun to explore more different chains, leading to a continuous increase in the number of games on these different chains.

This trend of multi-chain distribution may be due to the continuous development and innovation of blockchain technology and the level of support for chain games, enabling more chains to support game development and operation. Different chains have different communities and ecosystems, with the more popular public chains in 2024 likely leaning towards IMX and RONIN.

2. BTC Layer 2

1) Overview of the Bitcoin Layer 2 Market

After the significant breakthrough of the inscription track Ordi last year, the Bitcoin ecosystem has begun to become one of the hottest fields in 2024. Following the inscriptions, runes have also emerged, with each subfield being highly sought after. Compared to the surging MEME trend, Bitcoin's second-layer solutions (BTC L2) focus more on addressing issues in the construction of Bitcoin ecosystem infrastructure.

Despite the development of inscriptions for a year, the severe network congestion has significantly hindered the further development of the Bitcoin ecosystem. At this critical time, both Ethereum's second-layer solutions and Bitcoin's own second-layer solutions aim to elevate their respective ecosystems to achieve broader applications and adoption.

New Developments and Technological Progress in Solutions

Bitcoin's second-layer solutions mainly include the following:

l Centralized Layer 2 Solutions: These solutions build centralized exchanges or payment networks on top of the Bitcoin mainnet, transferring some transactions from the Bitcoin mainnet to this layer for processing, thereby alleviating the burden on the mainnet. These transactions are completed within the layer 2 network and only submit the final results to the Bitcoin mainnet when necessary. Typical representatives include Lightning & RGB, which utilize bidirectional payment channels and a multi-hop payment mechanism based on Hash Time-Locked Contracts (HTLC), considering scalability and privacy to some extent.

l Decentralized Sidechains: These solutions are independent blockchains built on top of the Bitcoin mainnet, introducing new tokens and consensus mechanisms. These sidechains typically have their own node networks and consensus algorithms while interacting with the Bitcoin mainnet. For example, Stacks (formerly Blockstack) uses Staked BTC (STX) tokens and the Proof of Transfer (PoX) consensus mechanism. Babylon and Interlay are also other decentralized sidechain projects. The advantages of these solutions lie in their relatively high degree of decentralization and security, while providing more functionality and scalability.

l Federated Sidechains: These solutions are based on collaboration, expanding Bitcoin's functionality by simplifying operations and improving efficiency. These sidechains are usually managed by trusted consortia or institutions, maintaining a certain level of trust with the Bitcoin mainnet. Representative projects include Liquid (launched by Blockstream), which provides faster transaction confirmations and higher transaction capacity for Bitcoin, while increasing privacy. Rootstock and Botanix are also examples of such federated sidechain projects. However, this solution may come at the cost of sacrificing Bitcoin's foundational decentralization, as it relies on large holders, raising some centralization risks.

Future Development

Due to Bitcoin's high price and scarcity, ordinary people find it difficult to participate easily; existing Bitcoin investments are mainly concentrated among certain countries, institutions, or wealthy individuals. To enable more people to truly participate in the Bitcoin ecosystem, Bitcoin's second-layer solutions may be more attractive. However, existing second-layer solutions still face some issues, such as high transaction fees (gas fees) and network congestion, which to some extent limit the development of the second-layer ecosystem.

If these issues can be effectively resolved, Bitcoin's second-layer solutions should welcome broader development prospects in the future. For example, by further optimizing and innovating to reduce transaction fees and alleviate network congestion, ordinary people can easily participate. This would significantly enhance the accessibility and attractiveness of the second-layer network, laying the foundation for further expansion and development of the Bitcoin ecosystem.

Data Analysis

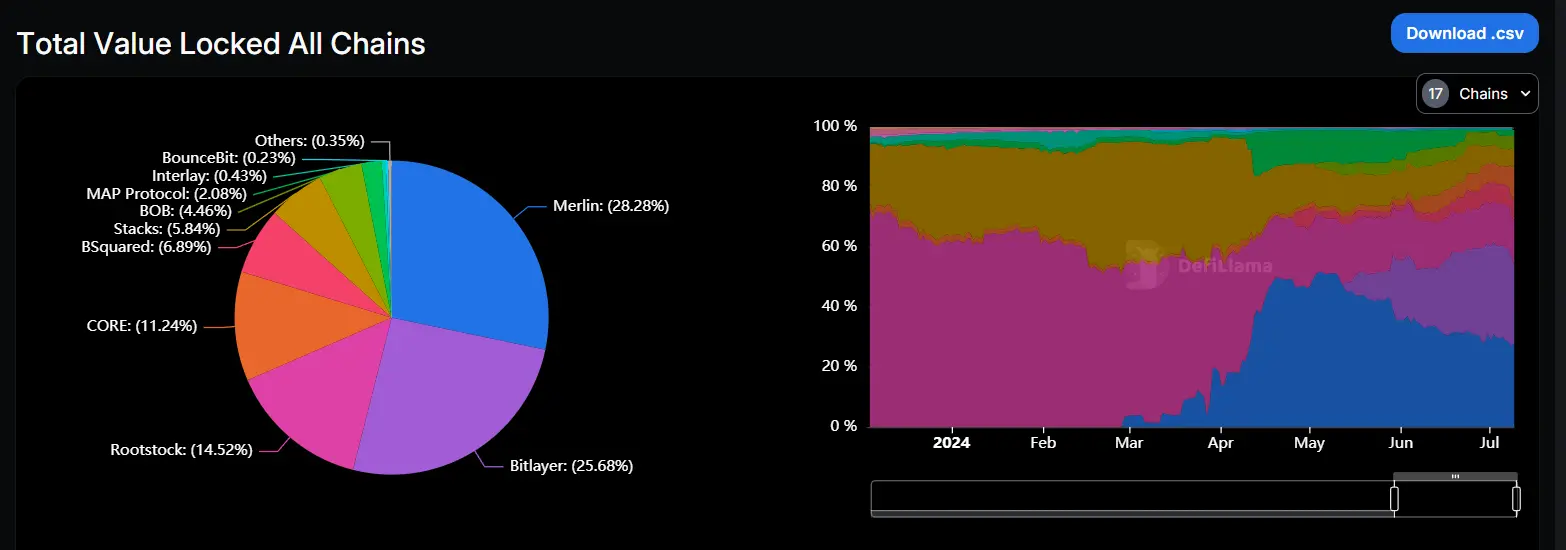

Defillama Bitcoin Layer 2 TVL Data

In contrast, data analysis and reports on Bitcoin's second-layer networks are relatively scarce. According to Defillama, the total locked value (TVL) of Bitcoin's second-layer network (Layer 2) is approximately $1,063.04 million. Among them, the largest shares are held by Arbitrum, Bitlayer, and Rootstock, accounting for 28.28%, 25.68%, and 14.52%, respectively.

It is noteworthy that starting in April, the market shares of traditional large staking projects Rootstock and Arbitrum have seen a significant decline. In contrast, emerging projects Bitlayer and BounceBit have gained more market share, successfully encroaching on the market of some existing projects.

3. DePIN Sector

Overview of the DePIN Track

DePIN (Decentralized Physical Infrastructure Networks) is an emerging model for infrastructure construction and management. It refers to the construction and maintenance of infrastructure in the physical world through decentralized means. This "infrastructure" can be WiFi hotspots in wireless networks or household solar panels in energy networks, among others. This innovative approach is fundamentally changing the way traditional centralized infrastructure and hardware networks are created and managed.

According to Messari's forecast, by 2028, the DePIN industry is expected to reach a scale of $35 trillion. This decentralized infrastructure construction model has the potential to add $10 trillion to global GDP over the next decade and is expected to reach a scale of $100 trillion in ten years.

Currently, the main subfields of the DePIN industry include cloud storage, computing power, and wireless sensor networks. These fields are all based on decentralized underlying architectures, utilizing distributed hardware resources to provide more flexible, scalable, and efficient infrastructure services.

In addition to GameFi and RWA (real-world assets), DePIN can be seen as the third track closest to Web2 users. This field is expected to develop the economic circulation model to its fullest.

The reason for this is that the DePIN field can directly compare and analyze actual data and traditional industries to find greater advantages. For example, DePIN's decentralized storage solutions are about 70%-80% cheaper than traditional cloud storage.

These obvious advantages make DePIN an important connection point between Web2 and Web3. No other field can utilize distributed hardware network resources as effectively as DePIN and expand them to compete with tech giants. Investment institutions' input into the DePIN field is gradually realizing the connection between the cryptocurrency world and traditional industries. This track is expected to play an important role in the future, promoting the decentralized transformation of traditional industries.

Overview of the DePIN Ecosystem

Data Analysis

According to CoinGecko's data statistics, the Decentralized Physical Infrastructure Networks (DePIN) sector currently ranks 29th, with a total market capitalization of around $2.014 billion. Overall, the market capitalization of the DePIN sector shows a steady upward trend.

In terms of the number of users of DePIN, it is positively correlated with the total number of devices. According to the latest data, the total increase in DePIN devices reached 1.7 million in the past seven days, with the main growth coming from key application projects like WIFI Map.

From a geographical distribution perspective, DePIN devices are mostly concentrated in Europe, North America, and Southeast Asia. This reflects that these economically developed and technologically mature regions are widely adopting DePIN solutions.

It is noteworthy that in the domestic market, due to factors such as policy regulation, the deployment and application growth rate of distributed resource devices has significantly slowed down. This indicates that geopolitical and regulatory environment differences are becoming one of the important factors limiting the development of DePIN in certain regions.

Despite this, DePIN still shows a good growth trend.

Revenue Situation of Leading DePIN Protocols

According to industry data provided by Artemis, in the past year, the top three DePIN protocols (Helium, Geodnet, and Akash Network) generated a total of $3.5 million in fee revenue. This highlights the strong position and good business model of leading projects in the DePIN field.

It is noteworthy that the profitability of DePIN protocols also shows a certain degree of volatility. Data shows that the profit level in the first quarter of 2024 was about 30% higher than that in the second quarter. This change may be related to the impact of fluctuations in the cryptocurrency market, but overall, it indicates broad recognition of DePIN technology and application scenarios in the market.