Doubler: A Crypto Native DeFi protocol tailored for turbulent cycles

Doubler is a protocol tailored for this round cycle, and its innovative gameplay provides a new perspective on the dilemma of "shortage of off-chain and on-chain liquidity >> cycle alpha." By aggregating liquidity to resist market volatility and improve overall winning rates, it enhances individual odds for risk-seeking users through a yield separation strategy.

Doubler is a protocol tailored for this round cycle, and its innovative gameplay provides a new perspective on the dilemma of "shortage of off-chain and on-chain liquidity >> cycle alpha." By aggregating liquidity to resist market volatility and improve overall winning rates, it enhances individual odds for risk-seeking users through a yield separation strategy.Author: Gwen Li, NG, Chen Li

Corresponding Author: Youbi Research Team

1 The Liquidity Dilemma of the Current Cycle

In the current bull market cycle, market behavior shows significant differences from previous cycles, such as higher volatility and deeper pullback periods. Both institutional and individual investors frequently encounter declines in asset value, reflecting two major dilemmas present in the current cycle.

1) Shortage of liquidity both on and off the market, with on-chain token issuance leading to dispersed liquidity.

In the current macroeconomic context, the U.S. has maintained a rate hike cycle for 2 years and 4 months, along with a 2-year and 1-month quantitative tightening (QT) cycle. Rate hikes reduce the amount of circulating funds in the market by increasing borrowing costs, thereby lowering market liquidity, while QT directly withdraws liquidity from the market. Compounding the issue is the high debt and deficit situation in the U.S. caused by excessive monetary easing during the pandemic, leading to an oversupply of U.S. Treasury bonds since 2023, further draining liquidity from the financial market. However, the repeated inflation and robust economic conditions in the U.S. have continuously delayed expectations for rate cuts, creating significant uncertainty in the market regarding future rate cut timing and magnitude, which has also contributed to high market volatility.

Although the ETF narrative in this cycle has brought new funds from traditional institutions into the market, on one hand, traditional institutions lack confidence in future market trends, resulting in random inflows and outflows of ETFs; on the other hand, due to the delivery methods of ETFs, it is difficult for this portion of funds to spill over into the altcoin market. Moreover, with the low barriers to asset issuance, the speed and scale of token issuance in this cycle have reached unprecedented heights, further dispersing the already insufficient on-chain liquidity.

2) Lack of Alpha, insufficient overall upward momentum, and no one is spared from the downturn.

The fundamental reason for the inability to attract more funds from the off-chain market is the scarcity of genuinely innovative products in this cycle. When market alpha is insufficient, secondary trading devolves into a liquidity game, making it difficult to establish an independent market trend. As a result, most users in this cycle have generally focused on hot topics and airdrop investments rather than true value investing. The so-called "failure of value investing" in the market is likely due to the lack of value innovation in investment targets; the essence of the rise in these tokens is a slowdown in liquidity. This has led to increased panic in the market when signs of a downturn appear, resulting in a widespread decline.

2 DeFi Alpha Problem-Solving Approach

Under the dual pressure of insufficient external liquidity and inadequate internal innovation, the average win rate and odds for investors are declining. So what kind of DeFi protocol do we need to enhance user win rates and odds?

1) Addressing liquidity shortages

Products should emerge in response to market conditions, combating high market volatility by aggregating market liquidity to improve overall win rates.

Avoid mutual liquidation on-chain; the core game for users comes from external profits, allowing pool players to share returns and improve average win rates.

Prevent liquidity lock-up caused by repeated nesting, avoiding TVL withdrawals due to the expiration of incentive activities.

2) Addressing insufficient alpha

Launch products suitable for any market phase, even during downturns.

Innovate business models to realize the true value of decentralization rather than narrative shelling, providing risk hedging and yield optimization for assets through innovative solutions, offering excess return exposure to some users and improving individual odds.

Target assets should not be limited to staking and airdrop points; long-tail assets should also be applicable, lowering the entry barrier for users and meeting broader user needs, thus expanding market space.

3 Why Doubler?

Doubler is a cost-revenue separation protocol that utilizes a generalized martingale strategy to achieve low buying and high selling. While improving overall win rates, it increases odds for risk-tolerant users and provides a lower-risk investment strategy with the same excess returns as call options and leveraged long positions, with more flexible trading durations. By introducing positive externalities to the market, it generates external returns for the pool and aggregates market liquidity to combat high market volatility, while decentralization brings the "ever-profitable" characteristic of the martingale strategy closer to an ideal state. Additionally, Doubler separates costs from future revenue rights, meeting the excess return needs of risk-tolerant investors under lower risks than traditional options and contract leverage markets.

3.1 Generalized Martingale Strategy

The martingale strategy refers to the practice of doubling the bet amount after each loss. Once a profit is achieved, it not only covers all previous losses but also ensures a profit equal to the initial bet amount. However, when used alone, this strategy carries relatively high risks because individual capital is limited, and consecutive losses can quickly deplete an investor's funds.

Martingale strategy wiki link: https://en.wikipedia.org/wiki/Martingale(probabilitytheory)

Doubler incorporates the core principle of "buying the dip, buying more as prices fall" from the martingale strategy into an open shared liquidity pool. During periods of high market volatility, reasonable additional investments can lower overall holding costs, creating a cost advantage in profits, with profitability achieved once the market rebounds above the low average price. All investors joining the pool share risks and returns, breaking through the limitations of individual investor capital size. This method not only optimizes the risk diversification mechanism but also provides participants with a new way to pursue wealth growth beyond personal capital constraints.

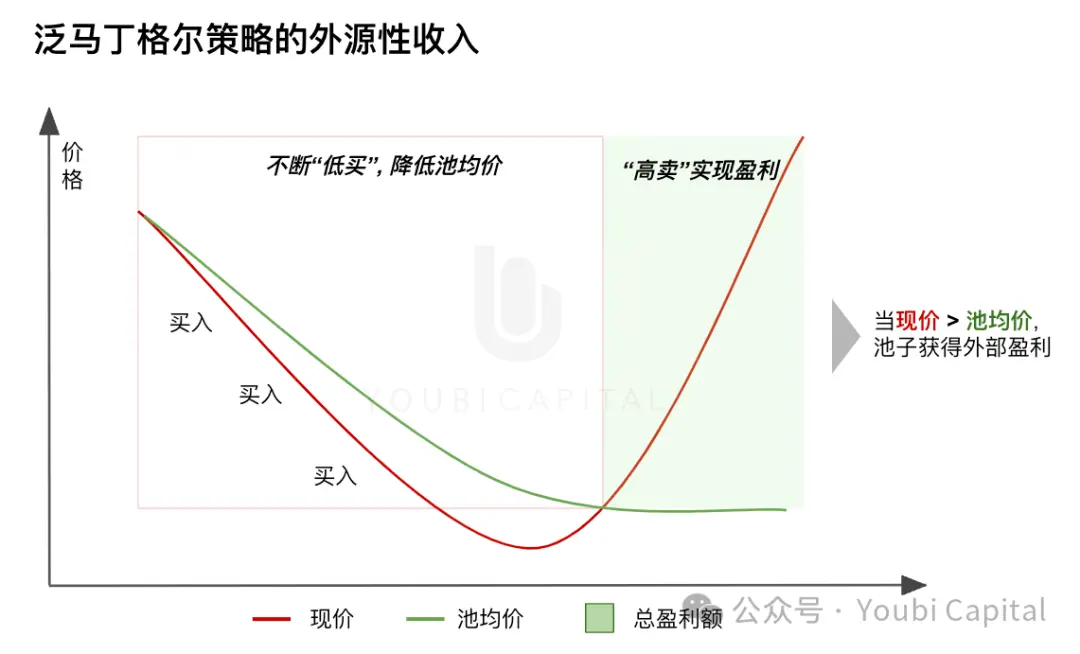

Introducing External Income for "Win-Win"

In both centralized and decentralized finance, investment models have often been a tense zero-sum game. For example, both long and short operations rely on finding a counterparty, making the market a competitive environment where one party's profit inevitably comes from another party's loss.

However, Doubler's profits come from the real returns generated by building a liquidity pool through "low buying and high selling," obtaining external income that not only provides participants with a new revenue opportunity but also truly achieves a win-win situation for all participants in the pool, breaking the traditional zero-sum competitive environment prevalent in decentralized finance.

Figure 1: External Income of the Martingale Strategy

Figure 1: External Income of the Martingale Strategy

Aggregating Market Liquidity for "Ever-Profitable"

The traditional martingale strategy is often hailed as an "ever-profitable protocol," with its core logic being that as long as there is sufficient capital liquidity, continuous doubling of bets can offset all previous losses and yield profits equal to the initial bet. However, in reality, to achieve guaranteed profits, a massive amount of capital is needed to support the exponential growth of bet amounts, which poses limitations for most individual investors due to their typically limited TVL or liquidity.

Doubler upgrades this strategy through an open liquidity pool, no longer limited to individual capital amounts, significantly increasing the available chips by aggregating market liquidity. It cleverly utilizes the openness of the cryptocurrency market to reduce the risk of strategy failure, which is the essence of decentralization. The Lite version encourages users to increase their investments during market downturns through a strategy of tokenizing revenue rights (detailed below), making it the first protocol truly applicable to bearish markets/high-volatility markets. Smart contracts ensure the normal operation of the strategy while bringing the martingale strategy infinitely closer to an ideal state, moving towards the goal of achieving so-called "ever-profitable."

3.2 Asset Revenue Rights Separation Strategy

At this point, readers may wonder why new users would buy more as prices fall. When the pool's average price is higher than the market price, wouldn't entering sacrifice their costs and lower others' average prices? This brings us to the ingenious cost-revenue rights separation design of Doubler Lite.

In Doubler Lite, for each asset invested in the pool, the protocol separates the ownership of costs and future revenue into C-tokens and 10X-tokens, along with equity tokens E-tokens. Depending on market conditions, users will receive different tokens. In a downturn, users will receive revenue tokens that share all future profits to incentivize their investment, allowing users to buy more as they anticipate future price increases. The specific calculation methods and issuance mechanisms for the three types of tokens are detailed in the white paper.

C-token: Represents the cost token, with the issuance quantity representing the total cost of all assets in the investment pool, priced in USD. When the pool is in a profitable state, C-tokens will earn dynamic fee rate income, settled daily.

10X-token: Represents the revenue token, entitled to capture the overall profits of the pool, with a maximum issuance of 10% of the pool's value. There are three ways to obtain it: 1) Invest assets when underwater to mint 10X; 2) Exchange E-tokens; 3) Trade on secondary markets, such as Uniswap.

E-token: Represents the one-way minting right for 10X tokens of the unissued portion of the pool, which can be exchanged for 10X tokens at a certain ratio.

Figure 2: Asset Revenue Rights Strategy, Doubler Supplement Scenario 1: When the overall pool is in a profitable state (above water), meaning the current price is greater than the average price, users will receive C-tokens and E-tokens upon investment.

Figure 2: Asset Revenue Rights Strategy, Doubler Supplement Scenario 1: When the overall pool is in a profitable state (above water), meaning the current price is greater than the average price, users will receive C-tokens and E-tokens upon investment.

Continuing to rise: (C-token dynamic fee rate income, gold standard profit) + (E-token can be exchanged for 10X-token, capturing rising profits)

Experiencing a downturn: (C-token value remains unchanged) + (E-token can be exchanged for 10X-token, continue to hold or sell on the secondary market to users optimistic about future price increases)

Scenario 2: When the overall pool is in a loss state (underwater), meaning the current price is less than the average price, users will receive 10X-tokens, C-tokens, and E-tokens.

Continuing to decline: (C-token value remains unchanged) + (E-token can be exchanged for 10X-token) + (10X-token can continue to be held or sold on the secondary market to users optimistic about future price increases)

Experiencing a rise: (C-token dynamic fee rate income, gold standard profit) + (E-token can be exchanged for 10X-token) + (10X-token shares the pool's profits)

Users exit priced in USD, settled in tokens (e.g., currently settled in ARB-ETH within the pool). The core game point for users in the pool lies in the timing of entering and exiting the pool, the timing of burning E-tokens and minting 10X-tokens, and the trading game between C-tokens and 10X-tokens. These game points determine the overall strategy and potential profitability for players, while Doubler also offers more gameplay mechanisms for users to explore.

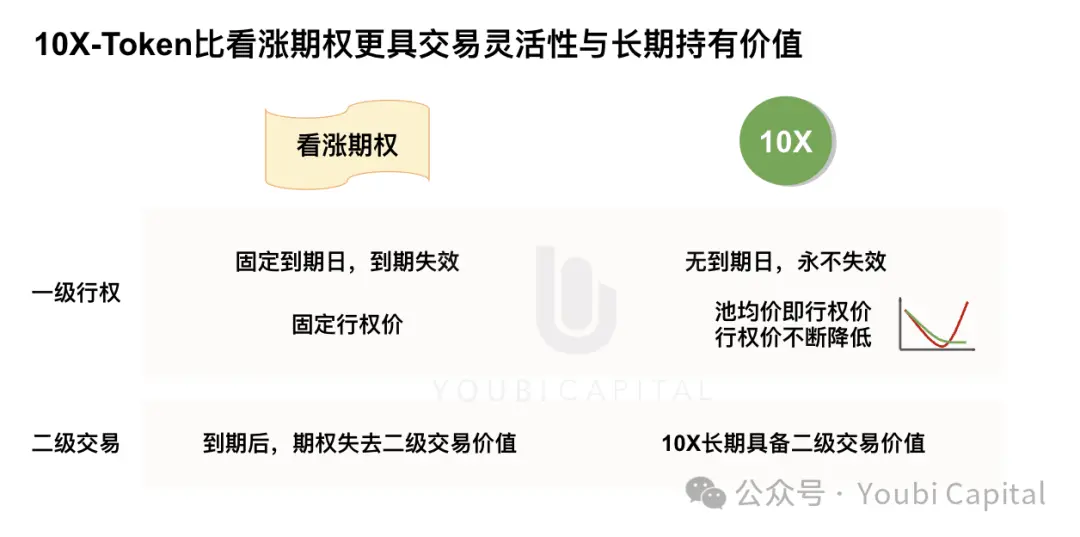

10X: A Call Option That Never Expires

From the scenario assumptions, we can see that if users are optimistic about the future price increase of the token, then it is worthwhile for them to buy in when underwater, capturing more future profits at a lower cost. Since the maximum issuance of 10X tokens is 10% of the overall pool value, 10% of the tokens enjoy 100% of the revenue rights in the pool, making holding 10X tokens similar to holding a call option.

In traditional American call options, users must exercise their rights at a predetermined price within a specified time. When the market rises as expected, reaching the ideal range before expiration, they can exercise their rights and gain profits from the rise. If the market does not rise as expected and does not reach the exercise price by expiration, the user cannot exercise their rights, and the option loses its value.

Clearly, compared to traditional American options, the strategy of holding 10X tokens is superior.

From the perspective of exercising call options: 1) 10X tokens have no expiration date, extending the exercise period indefinitely; 2) 10X tokens have a non-fixed exercise price, with the pool's average price serving as the exercise price in Doubler's strategy. As long as the market price is higher than the pool's average price, it is profitable, and 10X tokens can capture returns. The strategy of buying more as prices fall in a downturn will continuously lower the exercise price of 10X tokens while also increasing their profit value.

In terms of the trading value of options in the secondary market, traditional options face expiration and potential loss of value if they do not reach the exercise price as the expiration date approaches. In contrast, 10X tokens, with no expiration date, will permanently retain their secondary trading value, with the core game revolving around the differences in users' costs and future price increase expectations.

Finally, there may even be additional arbitrage opportunities between the options market and the 10X token market. For example, selling call options while holding 10X tokens can hedge risks while profiting from the cost value of the options. This will not be elaborated here, as more gameplay awaits user exploration.

Figure 3: Call Option vs 10X-Token

Figure 3: Call Option vs 10X-Token

10X: A Long Position with No Liquidation Risk

Another way to bet on the upward potential of an asset while willing to use lower principal for greater returns is to take a long position with leverage. However, it is well known that leverage is a high-risk derivative, amplifying both profits and losses. For example, if 10x leverage is used, the market price only needs to drop by 10% for the investor to face liquidation and lose all their principal.

In contrast, holding 10X tokens can yield nearly 10 times the leveraged returns, but users do not need to bear the loss risks associated with 10x leverage. The open liquidity pool aggregates market liquidity as a whole, breaking through individual principal limitations and continuously expanding the overall pool's margin, achieving ever-profitable liquidity pools. Moreover, regardless of how the asset price fluctuates, the maximum issuance of 10X tokens is 1/10 of the pool's market value, ensuring it never exceeds the critical value, thus eliminating the risk of "liquidation."

The risk users bear is that 10X tokens have no actual value when the pool is in a loss state. However, since 10X tokens can circulate in the secondary market, as long as there are users optimistic about the future price trend of the asset, they can exit at will. Compared to the leveraged market where a 10% drop results in the loss of all principal, 10X tokens can withstand high market volatility, providing a lower risk exposure for excess returns.

Figure 4: Long Leverage vs 10X-Token

Figure 4: Long Leverage vs 10X-Token

10X: A More Efficient Revenue Derivative

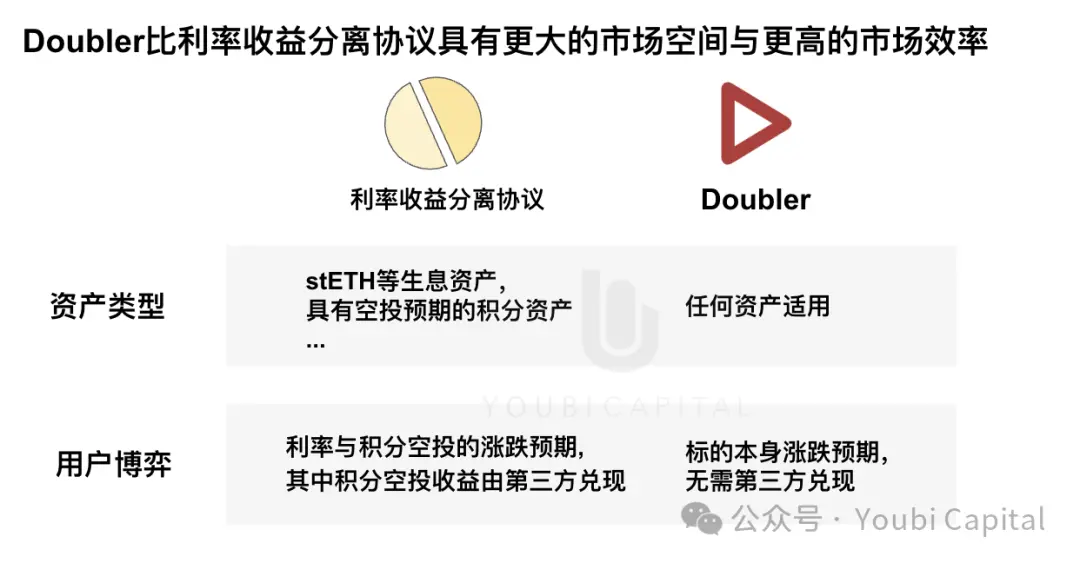

This year, the revenue separation protocol based on interest-bearing assets has opened up new demand markets due to its innovative design. The asset revenue rights separation of Doubler Lite and the interest rate derivative protocol (referred to as interest rate derivatives hereafter) appear to have certain similarities, but the market demand and user game points are entirely different.

1) Differences in Asset Types

Interest rate derivatives split the coin-based assets from the income-generating portion associated with their asset attributes, limiting the types of applicable assets. Common asset types in the market include staking and re-staking assets, stablecoin assets with dynamic yields, and point assets with airdrop expectations. In contrast, Doubler Lite separates the U-based costs from the profits generated by asset value increases, making it applicable to any asset and offering a broader market space.

2) Differences in Trading Duration

The trading methods in the interest rate derivatives market involve partners and protocols setting pools with fixed trading durations, resembling traditional call options. For example, interest-bearing assets based on points will end their point activities before the partner's airdrop expiration, leading to the expiration of the corresponding interest rate derivative trading pool and the loss of TVL for asset redemption, rendering the call option void. As mentioned earlier in the comparison with options, 10X tokens maintain long-term trading value.

3) Differences in User Game Points

The core game point for users of interest rate derivatives lies in the expected rise and fall of interest rates over a certain period. However, this expectation often cannot be completely detached from the partner (the issuer of the asset), or there may be a possibility of a few users front-running. For instance, in the case of Etherfi and LRT assets, the interest rate yield expectations for LRT assets are ultimately fulfilled by the partner Etherfi, leading to a hidden information game in the interest rate derivatives market. According to market efficiency theory, this trading market is classified as a semi-strong efficient market.

In contrast, the core game point for users of Doubler Lite lies in the expected rise and fall of the asset itself, determining the timing of buying and trading strategies. The expected rise and fall of the asset do not need to be fulfilled by the issuer but are reflected through real-time secondary market trading. Compared to interest rate expectations, the expected rise and fall of the asset reduce the likelihood of hidden information games, resulting in stronger market efficiency.

Figure 5: Interest Rate Revenue Separation Protocol vs Doubler

Figure 5: Interest Rate Revenue Separation Protocol vs Doubler

Summary

In summary, Doubler, along with call options and 10x leverage, belongs to U-based financial derivatives. The former can provide the same excess returns as the latter two but enjoys lower risk exposure and more flexible trading durations. In contrast, the revenue separation protocol belongs to coin-based financial derivatives, with Doubler applicable to a wider range of asset types, offering greater user demand and market space, as well as higher market efficiency.

Figure 6: Doubler vs Other Financial Derivatives

Figure 6: Doubler vs Other Financial Derivatives

Conclusion

As the lead investor in the seed round for Doubler, Youbi Capital is pleased to see the launch of the Doubler Lite version on the mainnet, achieving over $3M in TVL within a few days. Doubler can be said to be a product tailor-made for this cycle, applicable even in high-volatility markets. Its innovative gameplay provides new ideas for the dilemma of "shortage of liquidity both on and off the market >> cycle alpha." By aggregating liquidity to combat market volatility, it improves overall win rates and offers risk-tolerant users investment strategies with lower risks than call options and leveraged long positions while maintaining the same odds.

We look forward to more subsequent performances from Doubler, believing that the "doubling pool + big winner" mechanism familiar to testnet users will continue to bring surprises to everyone. Let us wait and see.

Risk warning Risk warning

Risk warning Risk warning

Popular articles