Meme "devours" the market, VC projects fall out of favor, where will the market go next?

The "double-edged sword" of VC Token.

The "double-edged sword" of VC Token.Author: Terry, Plain Language Blockchain

Memecoin or VC Token, which one would you choose?

Before 2022, everyone would probably have unhesitatingly chosen well-known VC-backed, high-profile, high-valuation star projects. Now, in just two short years, the tide has turned, especially with the small trend sparked by Ordinals in 2023, which has quickly grown into a powerful anti-VC wave in the crypto world.

Since the first half of this year, Memecoin has been leading the market performance compared to VC Token, attracting a large amount of attention and capital inflow in a short period of time. The call for fairness from the general public it represents is also becoming a trend. So, behind this, is it that funds are voting with their feet, or is it a short-term illusion within the market?

VC Token "Ice and Fire"

The first half of 2024 will almost be a concentrated realization period for a series of former "superstar" projects, from Wormhole to Polyhedra Network, from Starknet to LayerZero, and from Zksync to Blast, all of which are Airdrop projects that community users and yield farmers have been eagerly anticipating.

However, the actual price performance after realization has not been satisfactory, especially after the industrialization of Airdrop, a massive number of community users/yield farming studios have helped these star projects achieve extremely impressive paper data, thus pushing up project valuations, while the increasingly exaggerated FDV caused by VC financing has also buried the seeds of early liquidity sell-off risks.

For example, the recent new VC-type Token issuances like W (Wormhole), ZK, ZRO, and STRK can be described as a mess—with extremely high FDV and a continuous downward trend, almost every day closing with a bearish candle since listing, leaving no user who entered unscathed.

Based on data from late June (not accounting for the recent significant drop), PORTAL and SAGA have already fallen about 80% from their opening prices, while W, ZKJ, STRK, OMNI, and ALT have also dropped over 50% from their opening prices.

Source: @terryroom2014 / X

From a data perspective, for ordinary users, the era of "buying VC Tokens and easily reaping high returns" has come to an end.

At least for the recent new Tokens, purchasing in the secondary market is becoming more cost-effective than later financing valuations, and there are even signs of valuation inversion between the primary and secondary markets:

As of the latest data on July 10:

ZRO has historically raised $3 billion, with a current total market cap of only $3.8 billion;

W has historically raised $2.5 billion, with a current total market cap of $2.9 billion;

ZK has historically raised $1.25 billion, with a current total market cap of $3.1 billion;

ZKJ has historically raised $1 billion, with a current total market cap of $1.2 billion.

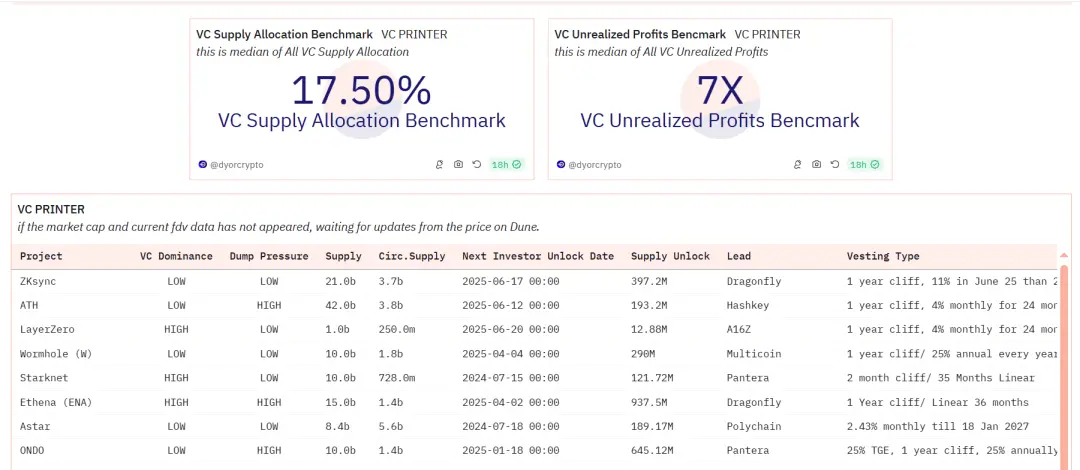

Interestingly, Dune's statistical data shows that even in the face of a continuous market decline, major VCs still have dozens or even nearly a hundred times unrealized gains on their investments in these Tokens, with the overall unrealized profit for VCs still as high as 7 times.

Source: dune.com

Source: dune.com

Moreover, hitesh.eth, co-founder of DYOR, has also compiled the top 10 "VC Tokens" in terms of overall VC return rates, most of which are currently the main forces in the market that are continuously declining, significantly impacting market confidence.

However, at the same time, projects like ENA, DYM, and SAGA have caused significant losses for secondary market investors, while VCs can still lock in profits of over 10 times— with ENA's return rate reaching around 100 times and ALT's at over 10 times, the experience of VCs and secondary market investors can be described as "ice and fire."**

Memecoin "Devouring" the Market

In contrast to the continuous decline of star VC Tokens listed on trading platforms, the secondary market price performance of on-chain assets like Memecoin has been outstanding, almost "devouring" the entire market, becoming a cultural symbol of Web3 at this stage.

Whether it's emerging Memecoin leaders like PEPE and FLOKI, or GME and other new public chain Memecoins, they have continuously emerged as wealth codes multiplying by several times or even dozens of times, reminiscent of the market environment during the DeFi Summer of 2020.

Especially since April of this year, the volatility of newly launched star VC Tokens has decreased, making it difficult for secondary market traders to profit, leading to more severe FUD sentiment towards VC Tokens, while Memecoin has shown unique charm, attracting a large amount of attention and capital inflow in a short time through community consensus.

In contrast, although VC Tokens have strong background support, their performance has not fully met investors' expectations amid rapid market changes.

Source: dune.com

Interestingly, Dune's statistical data also shows that during this round of Meme supercycle, the number of actual on-chain holder addresses for the top 46 Memecoins has indeed shown a significant growth trend over the past 90 days:

Among the 46 Memecoins, except for 4 that are in a declining trend (with FLOKI only slightly down), the remaining 42 Memecoins have all achieved widespread double-digit or even over 100% growth in the number of on-chain holders, which undoubtedly reflects the market's increasing attention and enthusiasm for these Memecoins.

Moreover, the relative ratio of buyers to sellers over the past 30 days has also remained above 1, indicating that investors hold a relatively optimistic attitude towards the future trend of Memecoins and are willing to invest more funds to seek potential returns.

In short, unlike many previous crypto projects dominated by large financing and VC narratives that had high thresholds and were more aimed at crypto OGs and on-chain whales (wealthy elites), Meme has given more opportunities to the general public beyond OGs and whales, especially allowing the general public to gain fair participation and share in the dividends.

Therefore, in comparison, discussions and doubts about Memecoin and VC are bound to become mainstream in the community. Meme can at least bring continuous incremental funds and attention through user flow, while the new projects with valuations of tens of billions of dollars are often just grand narratives or outdated conceptual products, which are naturally rejected by the community.

Community Resistance Behind the Meme Wave

In fact, if we closely examine the current market environment, we will find that beyond short-term speculation, the call for fairness represented by the general public behind Meme has gradually become a trend, with funds voting with their feet.

In simple terms, the rise of the Meme wave actually represents, to some extent, a correction by community users and the market against the traditional "financing—realization" model of the past two years: the previous model of star projects relying on top VCs to gather resources, combined with lofty technical narratives to conduct high-valuation large-scale financing, and then attracting the community to pile up a series of impressive on-chain data through so-called "Airdrop," has basically come to an end.

Especially this year, projects like ZKsync and LayerZero, which have been long awaited, have sparked significant controversies related to Airdrop, such as "witch hunts" and "insider trading," indicating that the Web3 world is gradually entering the "post-Airdrop era"—when star project teams begin to treat Airdrop as a form of arrogant power in resource allocation, Airdrop is no longer a mutual fulfillment between community users and project teams.

It is precisely because of this that the rise of Memecoin is due to their often being unbound by the traditional rules of primary and secondary market takeovers. Although this also means higher risks and more volatile prices, it at least provides ordinary users with another choice.

If we delve into the reasons behind the ebb and flow of Memecoin and VC Token, the objective market conditions are almost evident:

First, the selling pressure brought by high valuations and low circulation, as today's star projects almost all follow the pattern of high FDV and low actual circulation, creating a potential instability factor, with a very long sell-off cycle, putting immense pressure on the market;

Second, users are gradually becoming immune to technical narratives, especially from L2 to Restaking. After experiencing numerous projects, especially stars, embellishing technical innovations, users have become more rational and cautious, no longer easily swayed by seemingly profound but actually lacking substantial breakthroughs in technical narratives;

Additionally, the high-frequency capital extraction effect cannot be ignored, similar to the large-scale IPO bloodletting phenomenon in the stock market, the community has recently debated whether the intensive launch of star projects has led to a significant amount of capital being drained from the market, severely impacting market liquidity;

After all, funds voting with their feet cannot be deceived.

To some extent, the collaboration and interest entrenchment between VCs in the crypto world and the Web3 industry have reached a stage that clearly needs to be broken, and users' spontaneous pursuit of real profit effects and hotspots is also understandable.

After all, in this market full of temptations and opportunities, users instinctively lean towards those opportunities and popular trends that can bring tangible returns, and once existing projects fail to meet this demand, they will express dissatisfaction and resistance in various ways to seek better investment returns and market environments.

This also serves as a wake-up call for VCs and project teams accustomed to path dependence.