Jingwei Venture Capital Analyst: The TON ecosystem has great potential, but why do large-scale VCs have no opportunity to participate?

The Ton ecosystem is still in its early stages and has a lot of potential, but it may not have opportunities for larger funds.

The Ton ecosystem is still in its early stages and has a lot of potential, but it may not have opportunities for larger funds.Author: Zixi.eth

The Ton ecosystem is still relatively early. Ton has a great opportunity, but projects in the Ton ecosystem may not have a chance with large funds.

After Ton started building its ecosystem in the second half of last year, we saw the first wave of explosion in the Ton ecosystem this year. Overall, the execution capability of the Ton Foundation is very good, and in less than a year, it has taken shape.

The Ton Foundation is very clear about what should be decentralized and what should be centralized. For example, wallets and payments should be centralized, which was one of WeChat's core competitive advantages back in the day, and Ton is well aware of this. Only by solving the security issues of fund custody (everyone trusts TG's technology, and wallets won't be lost), simplifying payment (no need to use cumbersome bank cards, everything runs on Ton/U), and making it user-friendly (no need to jump through 78 steps like buying something on Taobao in the early years) can we truly achieve a Web3 version of WeChat Pay. Other ecosystems adopt a crypto-native approach, outsourcing everything and incentivizing the community to participate.

The profit model for ecosystem projects no longer needs to be like pure Web2/3 projects; the profit model is becoming diversified. Web2 models can earn advertising fees, sell users to exchanges, sell value-added services in games, charge subscription fees, or not issue tokens. Web3 models can collect fees from DeFi and other financial protocols, sell NFTs, or issue tokens.

TG has a base flow of users and solves payment issues, but these users are dispersed in low-value areas, and most users have low unit value. Does this mean that Ton should not focus on Web3 financial tools but rather adopt a more Web2 traffic approach?

The Ton ecosystem itself is an HTML5 Web2 company, just adding blockchain at the payment/settlement layer. Similarly, why do these projects have to add Ton? Theoretically, they can fully utilize TG's traffic and then use Polygon, Solana, or other L2s. At its core, TG has traffic, and Ton provides settlement. Other ecosystem projects do not necessarily have to start from scratch; they can simply integrate Ton (just like Travala for booking flights and hotels, Oobit for crypto payments, where Ton is a nice addition rather than the core).

On-chain TVL is growing rapidly, but limited by Ton's relatively small market cap, the ceiling will also be relatively small. Engaging in DeFi should still be done on BTC and Ethereum. However, Ton is different from BTC and Ethereum; Ton's chips are relatively concentrated. Do the core stakeholders of Ton have financial needs? Personally, I am conservative about innovations in non-BTC and Ethereum assets; this is no longer the era of DeFi and finance.

TG is a completely unregulated environment. This means that those doing traffic and casino businesses can operate without legal oversight.

From the current perspective, doing business on the platform may make more sense than investing. A large number of projects have already generated considerable revenue, such as Catizen with over $10 million in revenue and Hamster earning millions daily. However, as an investor, the risk-reward ratio is not high.

The lifecycle of projects here may be shorter. For example, Catizen and Hamster users are mostly looking for quick gains; once a token is issued, the quick gainers may dump it, and the project could end up losing 50% of its value. Could this evolve into an extreme ROI recovery business?

Crowdsourced projects may be inherently suitable for rooting in TG. Because TG gathers a large number of low-value users (user profiles may resemble YGG), are crowdsourced projects with positive cash flow suitable for TG? For example, data labeling, data collection for autonomous driving, and food delivery.

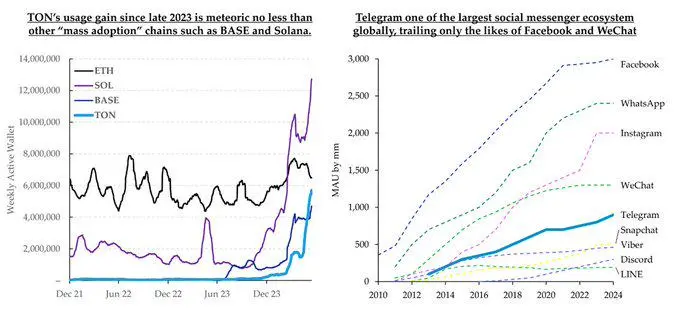

1/n TG is currently the fifth-largest social platform, founded in 2013 by the Durov brothers. Ton was initiated in 2017, launched its mainnet in the second half of 2021, and only began to ramp up promotion and operations in 2023. Ton's comparable counterparts are Solana and Base, as both are high-performance public chains with clear 2C attributes. Solana was previously backed by FTX, Base by Coinbase, and Ton by TG, all having certain traffic carriers. From the current Weekly active wallet perspective, Ton's growth has surpassed Base and is now close to half of Solana. Currently, Ton's approach is fully mirroring WeChat mini-programs, starting its unique Web3 journey. (Image source: Folium Ventures)

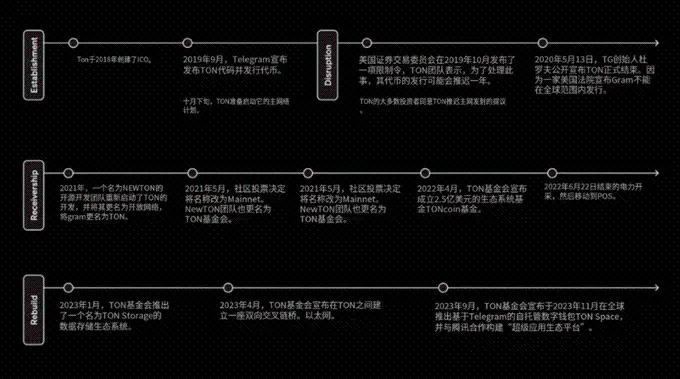

2/n In 2013, the Durov brothers created TG; in 2018, Pavel Durov launched TON and ICO'd $1.7 billion; in 2020, under the entanglement with the SEC, TG abandoned the dominant development of Ton; at the same time, the TON community established the Ton Foundation to continue leading Ton's development; in September 2021, the mainnet was launched and tokens were issued; from 2021 to early 2022, the Ton Foundation and miners accumulated over 80% of Ton's chips; in September 2023, TG announced an exclusive partnership with Ton, fully replicating WeChat mini-programs; in February 2024, Pantera heavily invested $300 million in Ton; in April 2024, Tether began deploying USDT on Ton, allowing users to start transferring through TG; in June 2024, Notcoin/Hamster/Catizen and others began to explode on TG.

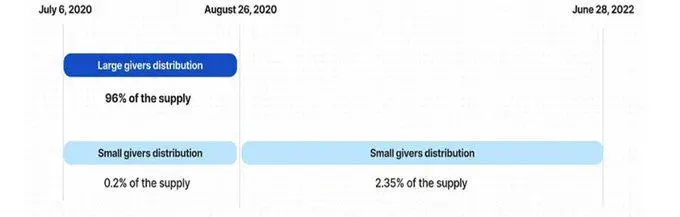

3/n The risk of highly concentrated chips needs to be considered. There are two types of contract addresses: Small Givers and Large Givers. The latter distributes more tokens each time (100,000 tokens instead of 100), but requires more computational power. Telegram launched token mining on July 6, 2020, transferring tokens to 20 contracts through system addresses, which distribute tokens. Mining continued from July 6, 2020, to June 28, 2022, but almost all token issuance was completed in the first 51 days: from July 6, 2020, to August 26, 2020, Large Givers distributed 4.8 billion (96%) tokens, while Small Givers distributed 9.9 million tokens (0.2%); from August 27, 2020, to June 28, 2022, Small Givers distributed 117.3 million tokens (2.35%). Notably, a total of 3,278 unique addresses participated in mining, but only 248 addresses participated in Large Givers' distribution. Therefore, we know that 96% of the TON supply was allocated to 248 addresses. Additionally, these 248 addresses are closely related: we found that many miner address groups are interconnected and share similar patterns, such as mining start and end times or the operations of mined tokens. We also discovered some retail activities, but most of the token supply was mined by a group of interconnected whales. Source: Whiterabbit

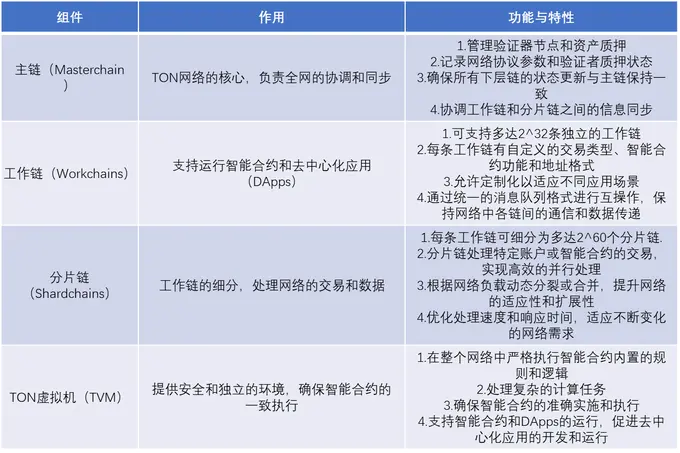

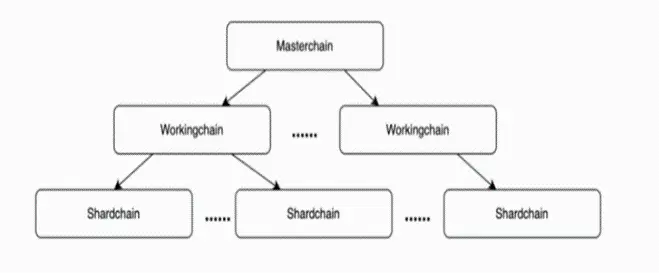

4/n From the structural perspective of the chain, it seemed like a good technical route in 2021. It directly modularized the chain. Ton's development language is different from mainstream Web2 and Ethereum's EVM Solidity; Ton developed its own TVM (Ton Virtual Machine), using three programming languages: Fift, FunC, and Tac. These three languages are specifically designed for development on Ton and are relatively new. The overall developer ecosystem is still in its early stages, mainly due to the relatively early programming languages. FunC is a high-level language specifically designed for programming smart contracts on the TON blockchain. It is a domain-specific, C-like, statically typed language. FunC is used to write smart contracts, which are then compiled into Fift assembly code, ultimately generating bytecode for the TON Virtual Machine (TVM). Fift is a low-level assembly language, and FunC programs are compiled into Fift assembly code. Fift is closer to the underlying layer and is generally not used directly for writing smart contracts but serves as an intermediate representation between FunC and TVM bytecode. Tac aims to provide a higher level of abstraction than FunC while maintaining compatibility with the TON Virtual Machine. FunC is a variant of the C language and resembles C/C++. The choice of FunC was also influenced by the fact that TG is written in C; Ton abandoned the crypto-native approach of EVM Solidity and defined its functionality as supporting TG's ecosystem. This means that Ton is not designed for Web3 geeks; more scenarios are grounded in ordinary Web2 users, essentially creating a blockchain for TG users. Therefore, some technical shadows, such as high concurrency and asynchronous structure, reference Web2 architecture. Thus, from the perspective of the developer ecosystem, it is very Web2 + Web3. This will be evident in the subsequent ecological development.

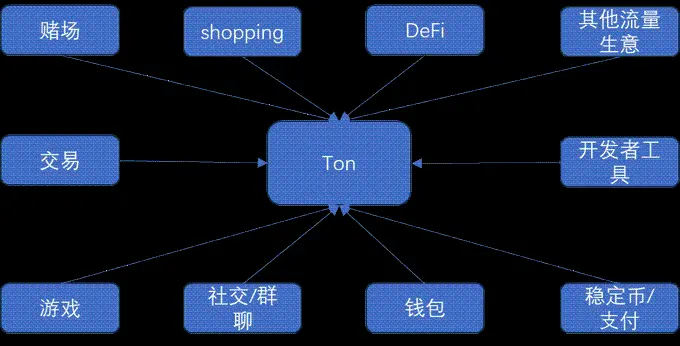

5/n Why is the Ton ecosystem attracting attention now? 1. True Web2 + Web3. TG dapps (mini-programs) have Web2 main businesses, and crypto is just a value add; for example, games can generate substantial revenue through advertising and other Web2 profit models, avoiding the previous crypto model of spending money on marketing, data, and then running away. Additionally, through crypto global payments, cross-border e-commerce/outbound business/hotel bookings, new payment expansion channels can be created. 2. Low development costs. Most mini-programs can be deployed using HTML5, and TON provides a series of technical development documents and templates, allowing developers to complete deployment without writing code from scratch. Feedback indicates that project teams with a Web2 background can complete a mini-program deployment in two to three days. 3. For Web3, the Ton ecosystem opens up new possibilities for project teams, no longer fixated on Infra/DeFi and other crypto-native tracks, supporting developers to build products across various fields such as social, gaming, e-commerce, and cross-border business, thus broadening the options for project teams. Finally, when developers create in the TON ecosystem, they can complete interactions and integrations of various products on a single platform, Telegram. For users, the mini-program applications in the TON ecosystem have obvious advantages in interaction, allowing users to complete one-stop interactive operations through the wallet mini-program without leaving the Telegram platform, without switching to external wallets like MetaMask. Moreover, the wallet on Telegram already supports users to deposit fiat currency OTC, meaning users can directly use credit cards to purchase crypto assets, achieving seamless interaction from fund injection to various on-chain applications.

6/n Below is the Ton ecosystem, which is currently thriving in gaming and social sectors. The current gaming ecosystem mainly consists of tap games, such as click-to-play and match-three games, often using HTML interfaces + crypto-native economy + advertising revenue, but with a large user base, making them current hits. In the Ton ecosystem, gaming is still in a red ocean competitive state, but cross-border e-commerce and crypto payments, which lean more towards Web2 scenarios, are relatively blue oceans.

7/n DeFi------TVL does not perform well, as it is not a crypto-native public chain. Ton's DeFi performance is relatively average, with an overall TVL of only $680 million, even less than mid-tier L2s like Linea and Blast, but this makes sense. From day one, Ton has not positioned itself as a crypto-native public chain, so DeFi is not the focus of its ecological development.

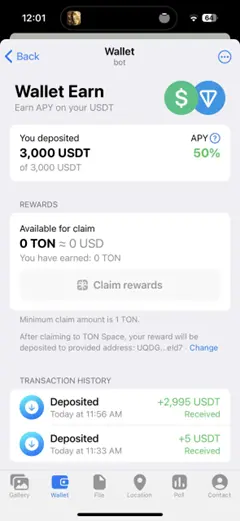

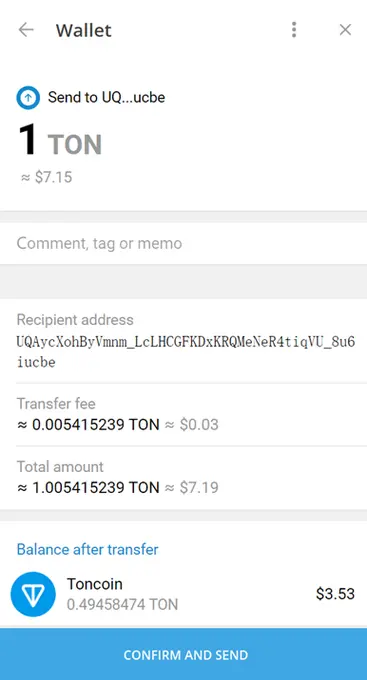

8/n Stablecoins/payments/wallets------priority strategy, a payment ecosystem with Web2 experience. Since 2017, Telegram has been exploring its business model, whether through payment services, advertising, or the ICO financing that was paused by the SEC, but the results have not been ideal. Last year, Pavel Durov revealed that the annual cost to maintain Telegram's normal operations is about $630 million. According to the Wall Street Journal, by April 2021, Telegram had accumulated $700 million in debt. Therefore, since 2021, Telegram has repeatedly issued over $100 million in excess bonds, and in March this year, it raised $330 million through bond sales. Telegram is often seen as the Web3 version of WeChat; from the perspective of active users, there is not much difference between Telegram and WeChat, with WeChat having about 1.2 billion active users and Telegram having 900 million and still increasing. However, their monetization methods differ significantly. Payments are WeChat's main commercialization path, and similarly, Telegram will choose payments. However, due to Telegram not being regulated and unable to obtain mainstream financial regulatory licenses, it only has the Web3 payment route, and founder Pavel Durov entered the crypto industry early on. Since the beginning of this year, Ton has started to focus on a stablecoin strategy, introducing USDT to the Ton chain and offering subsidies. Users who have completed KYC (including those from mainland China and Singapore) can stake USDT through TG's official wallet, Ton Space, with Ton offering a 50% APY and a reward cap of $3,000 over two months, with interest paid in Ton's native currency. After two months of development, the issuance of Ton USDT rapidly grew from $100 million to $500 million. Ton USDT can be directly transferred to friends through the wallet, just like transferring money to friends on WeChat; moreover, this money can be withdrawn, which is completely different from traditional on-chain payments.

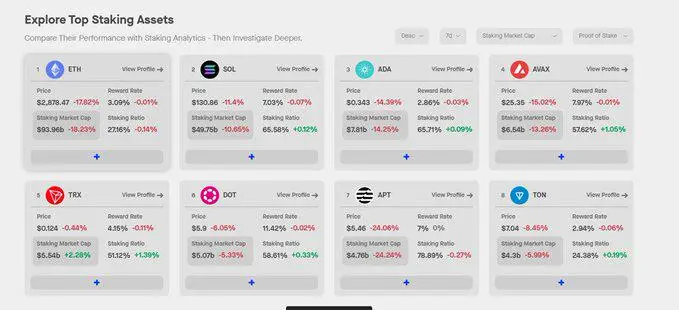

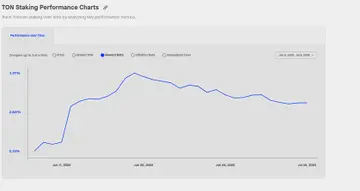

9/n The normal staking ratio for non-Ethereum public chains usually reaches over 50%, and there are high APYs to attract miners. However, Ton's staking ratio and reward ratio are relatively low, speculated to be due to: 1. Most of the chips are still in the hands of the Ton Foundation/early miners; 2. There are very few circulating chips in the market, and the few chips and stakers need to be filtered; 3. The reward ratio = inflation + gas fee, and Ton's gas fee is low ($0.005 * 7 = $0.035), which only indicates that network activity is actually below expectations (this may be because most of the currently popular Ton ecosystem projects only have token issuance expectations and have not fully gone on-chain). Ton's inflation is only 0.3%-0.6%, which means that the vast majority of Ton staking returns come from Ton's gas fees, differing from the measures taken by major public chains like Solana.

10/n Catizen is an early project created by a Web2 gaming team, which previously launched a project called Tap Fantasy, a clicker H5 game on Facebook. Catizen is a game where players combine low-level cats to create higher-level cats, with higher-level cats producing more. Users can purchase additional features with extra crypto tokens or U to speed up cat production. Catizen's in-game revenue has exceeded $10 million, achieved within about two months of the game's launch. In June, Catizen's total user count surpassed 20 million, with a DAU of about 2 million, over 700,000 on-chain users, and about 500,000 paying users. The on-chain user conversion rate remains around 10%, with over 50% of active users being paying users. Based on this, Catizen plans to gradually launch its own mini-game platform, positioning itself as the Telegram version of 4399/Steam.

11/n Hamster Combat is the most popular tap game on TG, where players earn coins by clicking the screen and completing tasks, using coins to build better teams for more earnings, leaning towards idle and nurturing gameplay. Hamster's overall design is quite toxic—tap once to earn a coin, with 1,000 energy needed for 1,000 taps, and players must wait for energy to regenerate before tapping again, with six chances for instant energy recovery each day; the passive income from idling is only valid within three hours of exiting the game, and after that, players need to re-enter the game. Hamster is very popular in the Middle East and Southeast Asia, resembling the logic of gold farming in GameFi back in the day. However, it is worth noting that Hamster has not issued a token, meaning users only earn "points" rather than real tokens, making them more like quick gainers. Hamster's revenue comes from advertising and directing new customers to exchanges, reportedly earning millions in daily ad revenue, with the paying demographic being exchanges.

12/n Other ecosystems are slightly smaller, but without much tracing back, just look at the images. Officially entering the field may leave little opportunity for third parties to participate.