Trends in the cryptocurrency industry in the first two quarters of 2024: Ethereum dominance, rise of non-European and American startups, and diverse talent backgrounds

20-30% of unicorn companies are founded by solo founders.

20-30% of unicorn companies are founded by solo founders.Original Title: “Crypto Industry Trends H1 2024”

Authors: @QwQiao & @xyczzcyx

Compiled by: Shenchao TechFlow

At @alliancedao, we receive about 3,000 applications each year to join our crypto startup accelerator. We collect data on factors such as the blockchain they use, product type, and geographic location. Due to the large sample size and our neutral stance on these factors, we can gain unique insights into the development trends of the industry.

Blockchain

Layer 1

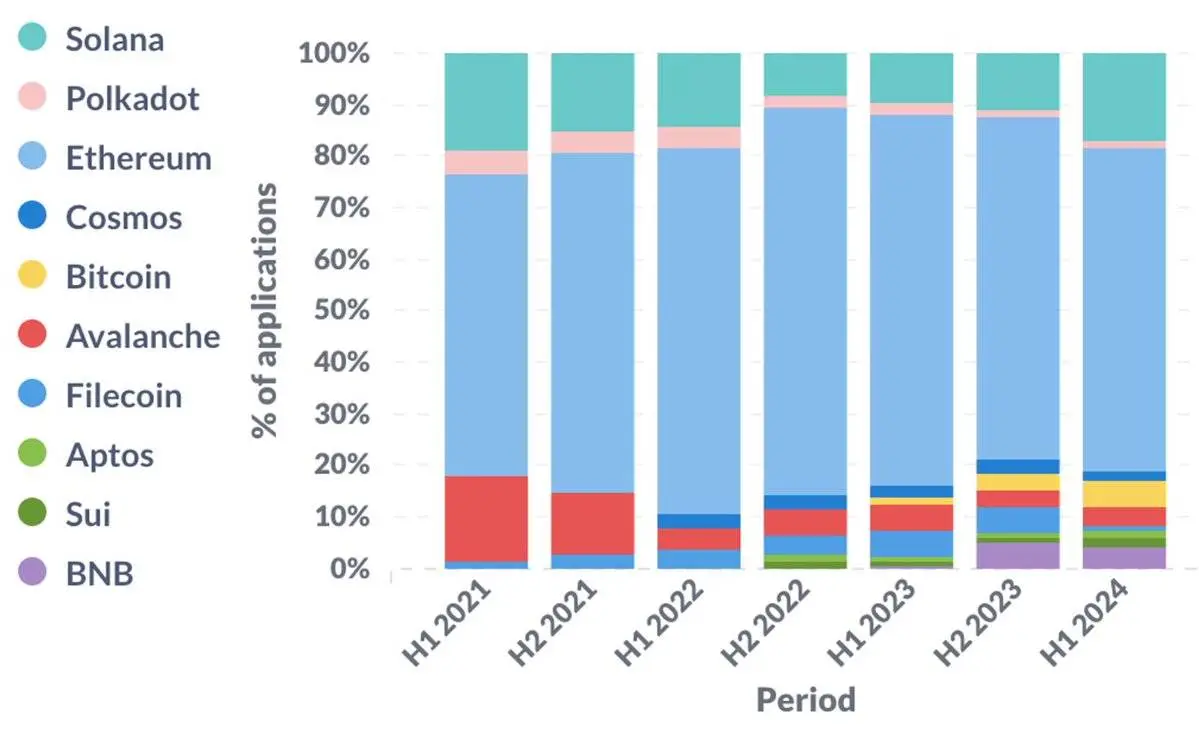

Ethereum remains the dominant ecosystem. However, Solana is recovering after hitting a low in the second half of 2022, which may be related to the collapse of FTX during the same period. Bitcoin is experiencing a revival amid the craze for ordinals, runes, and Bitcoin L2 technologies.

Changes in L1 share over time

L1 share situation in the first half of 2024

Ethereum Layer 2

Focusing on Ethereum L2 (and sidechains). Over the past three years, Optimistic rollups have gradually gained more attention. Notably, in the first half of 2024, Base accounted for over a quarter of the startups building on Ethereum L2.

Changes in L2 share over time

Product Trends

An increasing number of startups are focusing on infrastructure, DeFi, payments, and the combination of AI and cryptocurrency, often at the expense of NFTs. In these areas, the development of infrastructure and AI aligns with public discussion trends. However, the rise of DeFi and payments may surprise many, as there has been little public attention on these topics. Coincidentally, we believe these two areas are among the few verticals where cryptocurrency has found a clear product-market fit (PMF).

Changes in product share over time

Product share situation in the first half of 2024

Please note that this is an imperfect method of product classification, as these categories are not mutually exclusive. For example, a startup may operate in both gaming and NFT sectors, in which case we would assign a weight of 0.5 to both gaming and NFT.

Geographic Distribution

In the first half of 2024, we saw the proportion of startups from the United States and Canada reach a historic low, while the proportion from Asia and Africa reached a historic high. This may be due to 1) increasing regulatory uncertainty in the U.S., and 2) the growing practical applications of cryptocurrency in emerging markets.

Overall, North America, Europe, and Asia remain the three major regions, each contributing about 1/4 to 1/3 of all startups.

Changes in geographic distribution over time

Geographic distribution in the first half of 2024

The content from here may be more appealing to founders and venture capitalists. If you are one of them, please continue reading.

Founder Background

Big Tech Companies

The proportion of founders with a big tech background peaked in 2021 at 30%. We define big tech companies as those in the S&P 500 index. The exact definition is not important; the key is the trend over time.

Proportion of founders from big tech companies over time

Proportion of founders from big tech companies in the first half of 2024

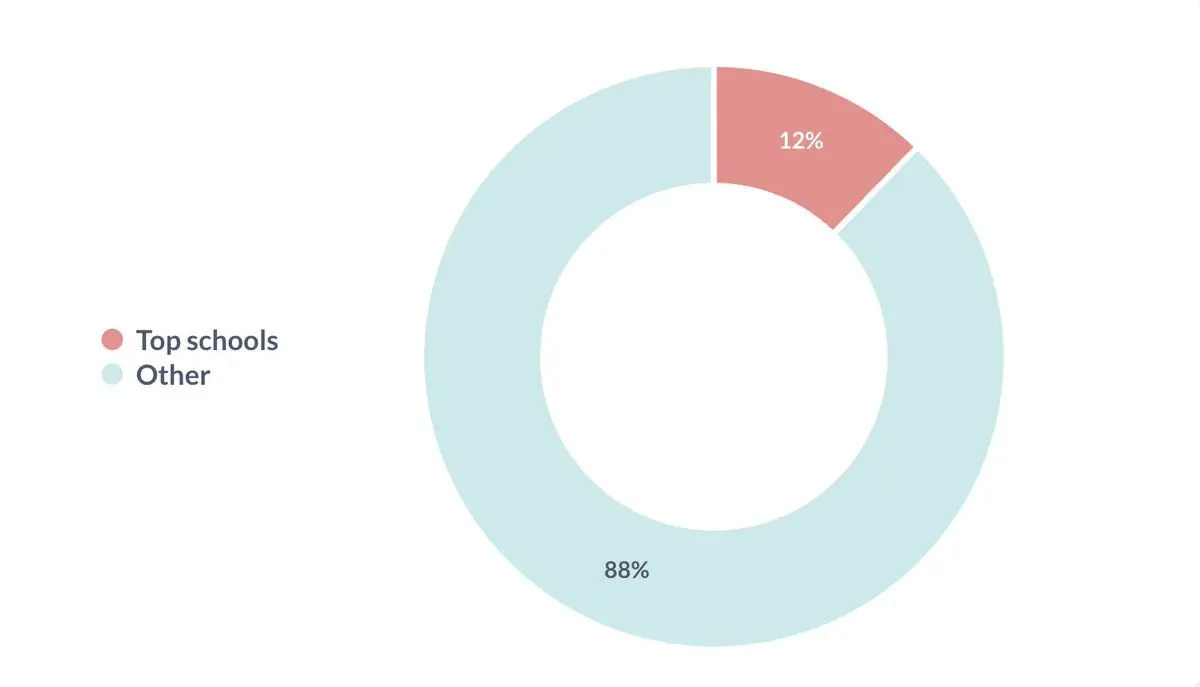

Top Universities

Similarly, the proportion of founders who graduated from top universities peaked in 2021. We define top universities as those in the QS World Top 100.

Proportion of founders from top universities over time

Proportion of founders from top universities in the first half of 2024

Repeat Founders

About 1/10 of founders have previously founded startups.

Repeat founders

Team Composition

Team Size

More than half of startups have team sizes between 2 and 5 people. We believe this is the optimal size for pre-product-market fit (PMF) startups.

Team size

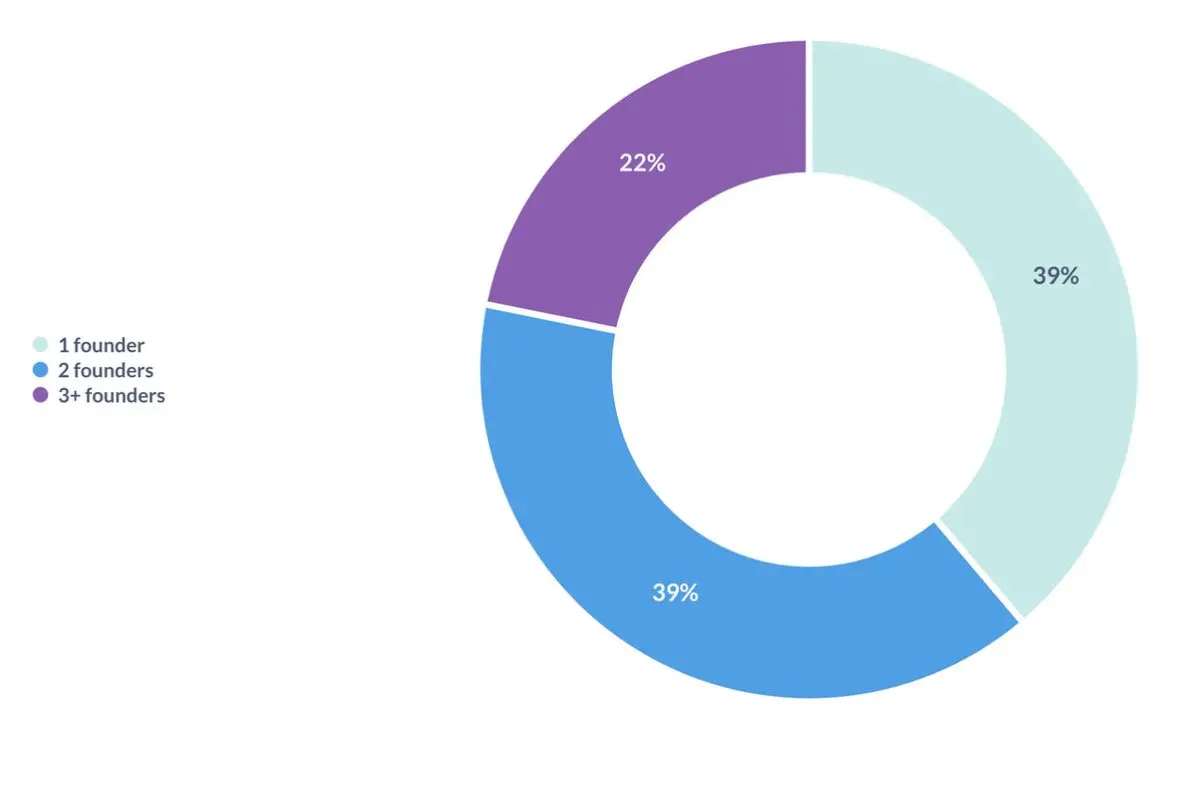

Number of Co-founders

Less than 40% of startups are founded by solo founders. As a reference, various studies indicate that 20-30% of unicorn companies are founded by solo founders.

Number of founders

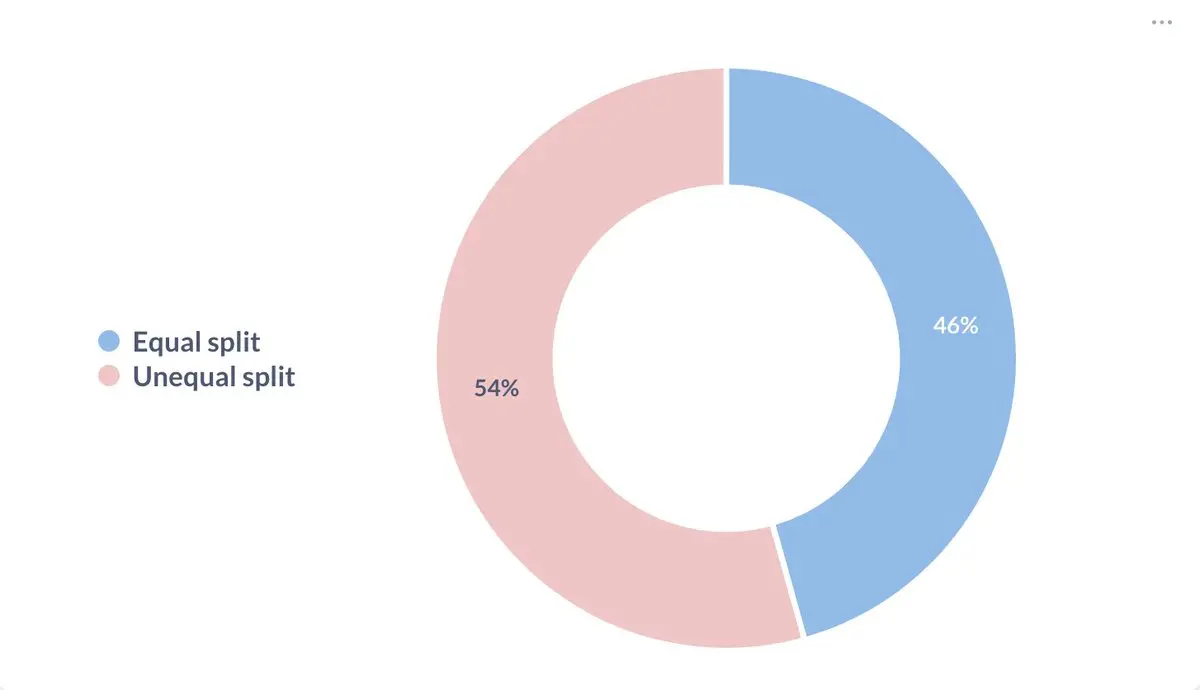

Equity Distribution

Among startups with two or more co-founders, about half of the companies split equity evenly, while the other half do not.

Equity distribution

Remote Work

Close to 3/4 of startups fully adopt a remote work model.

Remote work

Risk warning Risk warning

Risk warning Risk warning