Revealing: How the big players manipulate spot contract prices to ultimately harvest retail investors

This article discusses a common strategy for manipulating the prices of spot and contract cryptocurrencies, which may involve the project's own market value management team, professional market makers, or large speculative investors with significant capital. Therefore, the term "庄" will be used uniformly in the following text, as it is a term that people commonly prefer.

This article discusses a common strategy for manipulating the prices of spot and contract cryptocurrencies, which may involve the project's own market value management team, professional market makers, or large speculative investors with significant capital. Therefore, the term "庄" will be used uniformly in the following text, as it is a term that people commonly prefer.Source: Owen.btc X account

Author | @OwenJin12, authorized reprint by Wu Shuo

The author has previously worked in relevant overseas institutions, mainly focusing on risk management at the trading level. He has had considerable direct or indirect contact with large market makers, project parties, and institutional users. Recently, there has been a lot of manipulation in small-cap contracts, and based on his experience, he aims to decode and discuss how project parties, market makers, and large institutional investors interact in spot and contract trading, and why this constitutes unfair competition against retail investors.

This article is not aimed at $P****; I just randomly selected a project with obviously abnormal secondary market-related data for convenience in argumentation.

This article discusses a common strategy for manipulating the prices of spot and contract cryptocurrencies, which could involve the project party's own market cap management team, professional market makers, or large speculative investors. Therefore, the following text will uniformly refer to them as "the manipulators."

1. Simple Process Overview

2. Phenomena

Do you often encounter the following unreasonable situations on exchanges?

Phenomenon 1: Low on-chain and spot trading volume, but high contract trading volume

Taking Gate as an example, the contract trading volume is about 60 times that of the spot trading volume.

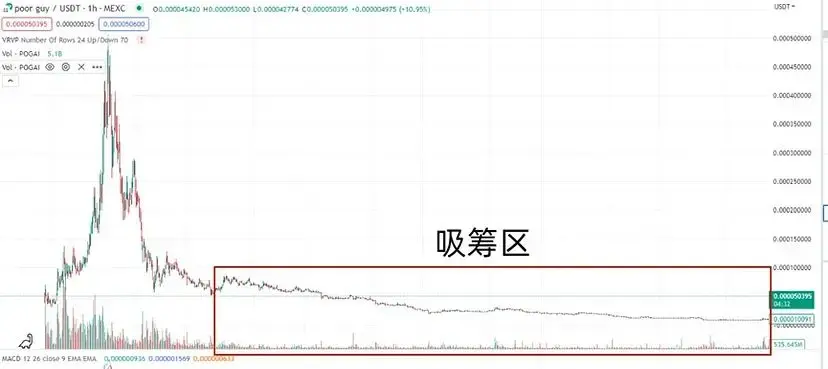

Phenomenon 2: Prices are rising, but trading volume is gradually decreasing?

Prices keep rising, but trading volume is decreasing, and MACD shows a clear bearish divergence.

Phenomenon 3: The long-short ratio of trading orders in spot and contract markets is completely opposite, resulting in negative funding rates

The rising prices lead users to collectively take short positions, but without holding any coins, they can only open short positions in contracts. Thus, the spot and contract markets generate completely opposite market sentiments.

The completely opposite market sentiment causes the funding rate to reach -0.66%, settled every 8 hours, resulting in -1.98% over 24 hours.

For example, trading derivatives (contracts) is like buying and selling houses. I am a real estate developer, and my houses mainly serve wealthy person A, who suddenly buys all the units in my development. The pricing power exists only between me and A; we are the supply and demand sides that affect house prices.

However, B, who is not a homeowner, believes that the prices of this development will fall. Therefore, B puts up 1 million to bet against A, thinking that A's investment will definitely lose money. B is unlikely to succeed because the circulating price of the houses is controlled by me and A; the transactions between me and A will truly affect the circulating price, and as long as we agree on the transaction price, B will definitely lose. The bet between B and A is similar to derivative trading and will not affect the circulating price of the spot.

Even if B believes the house price is artificially high and is worth only 1 yuan/square meter, that cannot be realized because his transaction is not a spot transaction but a derivative transaction. And derivative trading bets on the spot price, so those who control the spot price (me and A) can largely determine derivative trading.

In this example, the real estate developer is the project party, A is the "manipulator" who controls the circulating supply of the spot (possibly controlling the spot price), and B is the contract user.

This is also why it is often said that naked short selling in the derivatives market is a very risky behavior.

3. Some Essential Contract Basics

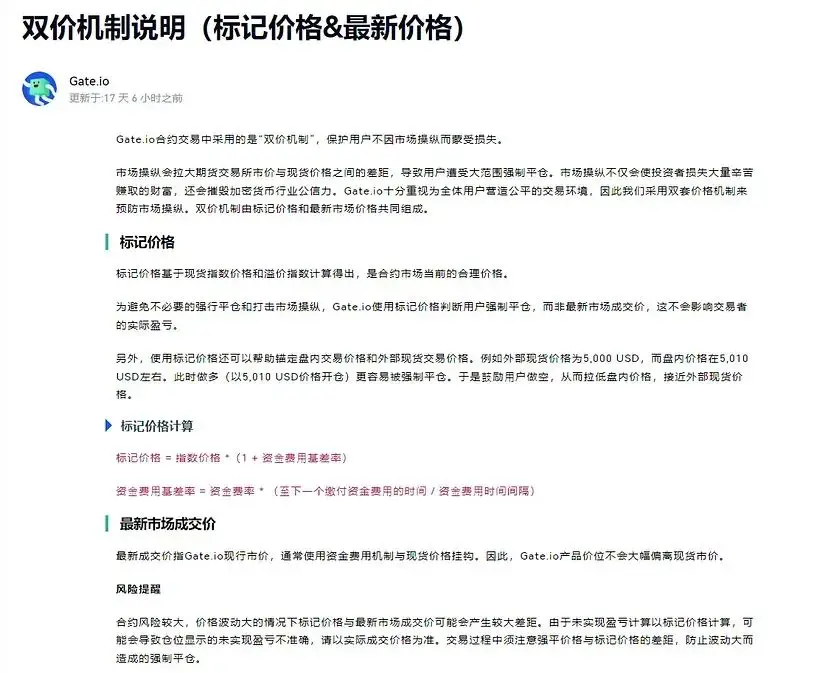

Knowledge Point 1: What are the mark price and last transaction price of a contract?

A contract has two prices: the last transaction price and the mark price. When users buy and sell, the last transaction price is generally used by default. However, liquidation uses the mark price, which is calculated using the latest transaction price of the external spot market through an algorithm to objectively reflect the price situation.

Explanation of Gate's contract mark price:

https://www.gate.io/help/futures/futures_logic/22067/instructions-of-dual-price-mechanism-mark-price-last-price

In other words, as long as the spot price is controlled, the mark price can also be controlled, thereby controlling whether the contract market will liquidate.

Knowledge Point 2: What is the funding rate of a contract?

To prevent the latest transaction price of the contract from decoupling from the latest transaction price of the spot, every 8 hours, funding is exchanged between long and short positions, either from long position users to short position users or vice versa, narrowing the gap between the latest transaction price of the spot and the contract.

Knowledge Point 3: What is the circulating market cap of a project?

The economic mechanism of a project is detailed in its white paper. Generally, it is divided into project parties, early investors, community airdrops, project treasury, etc. If a project's white paper is not transparent enough, it is more likely to be manipulated. For example, if the white paper gives the community enough freedom, it also gives market makers/institutional investors enough freedom --- they can acquire low-priced tokens at low levels, and once obtained, they cannot be diluted because there is no issuance or linear unlocking mechanism.

4. Small-Cap Contract Control Process

Step 1: Find a project with a relatively low circulating market cap that has opened contracts on a CEX

Typically, small projects with a circulating market cap of 1~10M USDT are chosen, and the contract leverage is generally between 20~30 times.

Step 2: Prepare funds, funds > external circulating market cap

Million-level speculative investors prefer to control small-cap contracts. Taking $P**** as an example, with a circulating market cap of 5M. During a prolonged decline, if the manipulator acquires 60% of the circulating supply at a low price, they only need to prepare 2M USDT and 3M tokens to fully control the spot and contract prices of this token.

Step 3: Control the spot order book price

As long as the 3M tokens are not sold, there can be at most 2M sell orders in the spot order book. Therefore, as a "manipulator" wanting to manipulate the token price, they need to prepare 2M USDT to maintain the spot price.

Clearly, even if all the $P**** held by "the manipulator" is sold at the same time, the price will not drop.

Step 4: Control the contract mark price

As mentioned earlier, the mark price of the contract is the spot price from various exchanges, meaning the mark price of the contract remains unchanged.

Step 5: Open long positions in contracts

Once it is ensured that the mark price is controlled, the manipulator can use their own funds to open any leveraged position in the contract. They can choose to open a lower position for safety or a higher one for aggression --- it doesn't matter, as the mark price has already been controlled, and the manipulator's long position will never be liquidated.

Step 6: Use funds to pump or trade against small accounts

For tokens with low depth and small market caps, it doesn't require much capital to pump the spot price by 100% in a day. If it cannot be pumped, the manipulator can open a small account and place a sell order at +100% price; once executed, it will naturally show a recent 24H price increase of +100%.

After seeing this news, retail investors will flood in, creating a large demand for short positions.

Step 7: Use funding rates to stabilize profits

At this time, there are very few sell orders in the spot order book, while there are many short positions in the contract, causing the spot price to be higher than the contract price, resulting in negative funding rates. The greater the gap, the more negative the funding rate, meaning that even if the mark price remains unchanged, short position holders must pay a high funding rate to long position holders every 8 hours.

Under this game mechanism, the manipulator continuously profits from the funding rate. For a more extreme example, holding SRM without moving positions for 24 hours can yield a 16% return.

Coincidentally, recent exchanges have frequently adjusted funding rates to help narrow the price gap between the spot and contract markets. However, they have not identified the root cause of the abnormal funding rates; expanding the rate range does not solve this problem but instead helps project parties/market makers/institutional investors harvest retail investors.

Adjusting LINA funding rates

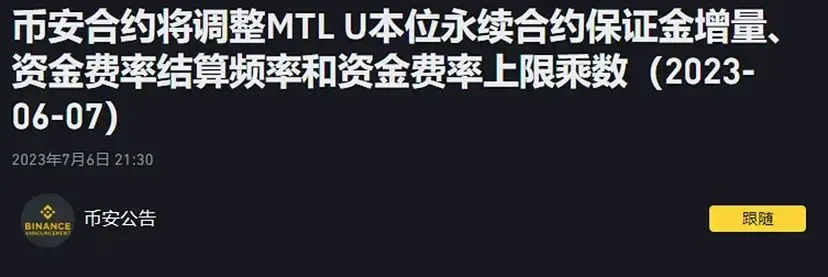

Adjusting MTL funding rates

You will also notice that LINA and MTL were the tokens that experienced significant price increases recently, with contract funding rates showing large negative values.

5. How Manipulators Profit

First profit point: Buy low and sell high in the spot market.

Please remember, manipulating is not charity; the tokens bought are neither gold nor BTC, and ultimately profits must be made through selling. The so-called pump is all for the subsequent dump.

Second profit point: Contract funding rates.

Third profit point: Tokens held without selling can be directly lent in the leveraged lending market. For example, on Gate, they can be placed in the idle token pool to earn an annualized return of 499%+.

After reviewing the process, you can see that the premise is to control the circulating supply of the token. If there are many tokens with linear unlocking mechanisms, they cannot be manipulated long-term. Each unlocking will change the circulating supply.

6. Where is the Problem?

Problem 1: Can the contract Open Interest (OI) exceed the circulating market cap?

Contracts can open positions with just USDT, while spot requires tokens to sell. Acquiring tokens to create selling pressure in the spot market and shorting in the contract market are two different levels of difficulty.

Returning to Step 3 of Part 3, the user controlling the manipulation has already reclaimed the tokens. Even if users believe this token is severely overvalued, they cannot create selling pressure in the spot market. At this point, users will turn to shorting in the contract market. In other words, due to the issue of low circulating supply, users' trading tendencies cannot be released in the spot market and can only be shorted in the contract market.

Going back to the mark price in Part 2. The mark price of the contract is the latest transaction price of the spot, which has been controlled by project parties/market makers/institutional investors. Therefore, how the contract liquidates has also been controlled.

Thus, when contract OI > circulating market cap, it means that due to the scarcity of the token, users' trading demands cannot be reflected in the spot price. The excess contract OI will exacerbate the deviation of the spot price.

Problem 2: When funding rates are abnormal, does expanding the upper and lower limits of funding rates really promote fairness?

The current solution from exchanges is to expand funding rates, which superficially addresses the price gap between the spot and contract markets, but in reality, it expands the ability of project parties/market makers/institutional investors to harvest retail investors. Currently, the funding rate range on exchanges is around [-2%, +2%], and further expansion would actually increase the "manipulator's" profits.

Therefore, while the existing funding rate mechanism helps anchor the derivative market prices to the spot market prices, it does not help make the trading market fairer; instead, it may promote greater unfairness in the trading market.

7. How Retail Investors Can Hedge Risks

Point 1: Be wary of small-cap projects that have opened high-leverage contracts. This gives large investors a significantly unequal competitive advantage over retail investors.

When users choose to buy in the spot market and open long positions in contracts, they accumulate enough buying power for project parties/market makers/institutional investors to offload their tokens and harvest retail investors again.

Point 2: Projects with high absolute values of funding rates.

Point 3: Manipulators do not engage in charity; the costs of pumping must be recouped through dumping for profit.

Escape early to avoid becoming the manipulator's bag holder. When the thought "this token is a value token, I want to hold it long-term until the next bull market" arises, it is not far from the manipulator's dumping. Their goal in pumping is to cultivate this user psychology for their own exit.

In the small-cap contract market, trading against manipulators is like playing poker with them; they are both the players and the dealers.

Risk warning Risk warning

Risk warning Risk warning