Galaxy Partners: MEV will play an important role in the block space market

MEV is a permanent consumer of block space.

MEV is a permanent consumer of block space.Author: Will Nuelle, General Partner at Galaxy Ventures

Compiled by: Luffy, Foresight News

Introduction

In our previous article, "Block Space Business Models," we pointed out that the sale of block space is one of four segments in the cryptocurrency market that can generate repeatable and robust product-market fit. Over time, we expect block space to become the second-largest gross profit segment after exchanges, and it may even become the largest gross profit market as trading volume shifts from CEX to DEX. This is a B2B2C business model where blockchains attract application developers, who in turn attract consumers (including individuals and businesses) to use block space through their applications.

We also believe that block space is a network effect-based business, in stark contrast to its centralized cloud computing counterparts, which have economies of scale but lack network effects. Network effects in blockchain exist in (i) application developers, (ii) application deployment, (iii) users, (iv) liquidity in protocols, and (v) original capital.

Galaxy predicts that the consumption of block space (in terms of the total amount spent on consuming block space) will accelerate over time, and any future increase in blockchain capacity will be filled by demand.

MEV Economics

In this article, we will assess the proportion of block space consumed by MEV transactions and discuss why it is important for evaluating block space as a business model.

MEV transactions are fundamentally different from non-MEV transactions. MEV demand is endogenous, coming from within the system, while non-MEV transaction demand is exogenous, coming from outside the system. MEV is an amplified version of block space demand, generated solely by others using the system.

- Non-MEV transactions: Users are willing to pay for this because they have exogenous demand for using applications, such as paying transaction fees for stablecoin transfers or depositing into Compound.

- MEV transactions: Users can obtain risk-free profits (or statistically risk-free profits) based on the state of the system. The exogenous demand for using the system creates the demand for consuming block space. In other words, it is endogenous demand.

In studying block space as a business model, I have been pondering: how much demand does MEV contribute?

MEV as a Driver of Block Space Demand

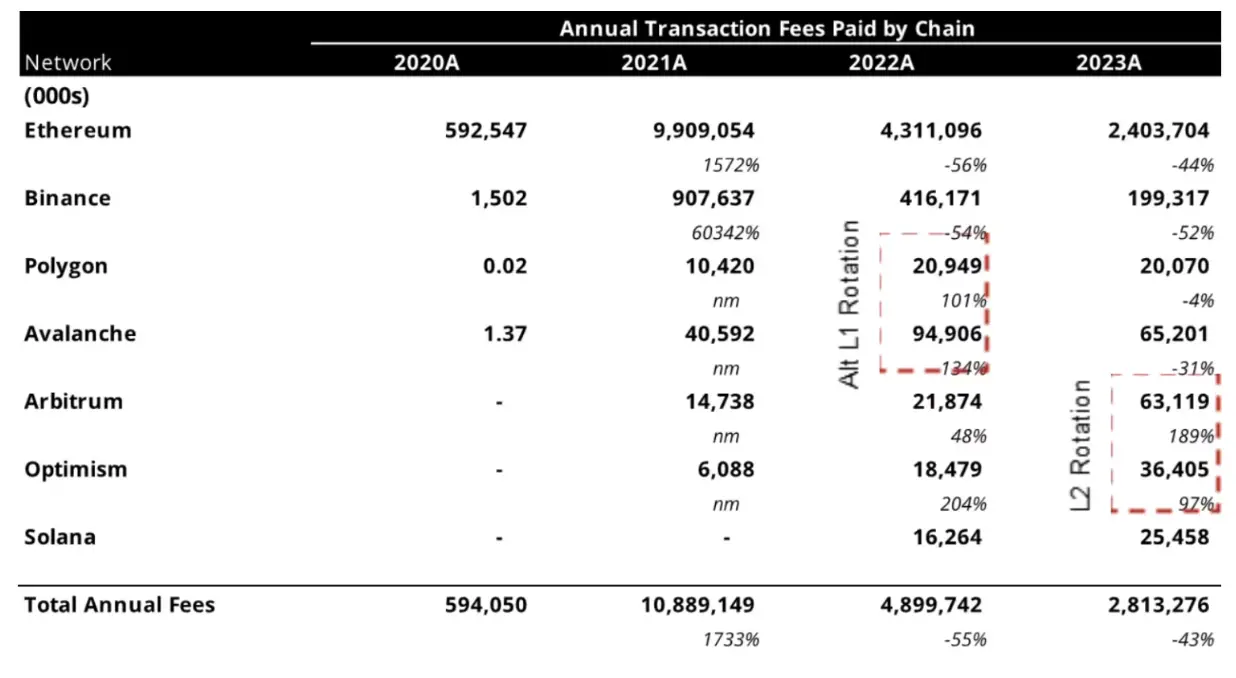

As shown in the previous article on block space business models, the total demand for block space on top-tier fee-charging blockchains reaches billions of dollars annually and follows a power-law distribution:

Source: Will Nuelle, Galaxy Ventures

Since September 2022, the daily transaction fees paid by users are as follows (the time series is displayed on a logarithmic scale):

Source: Will Nuelle, Galaxy Ventures

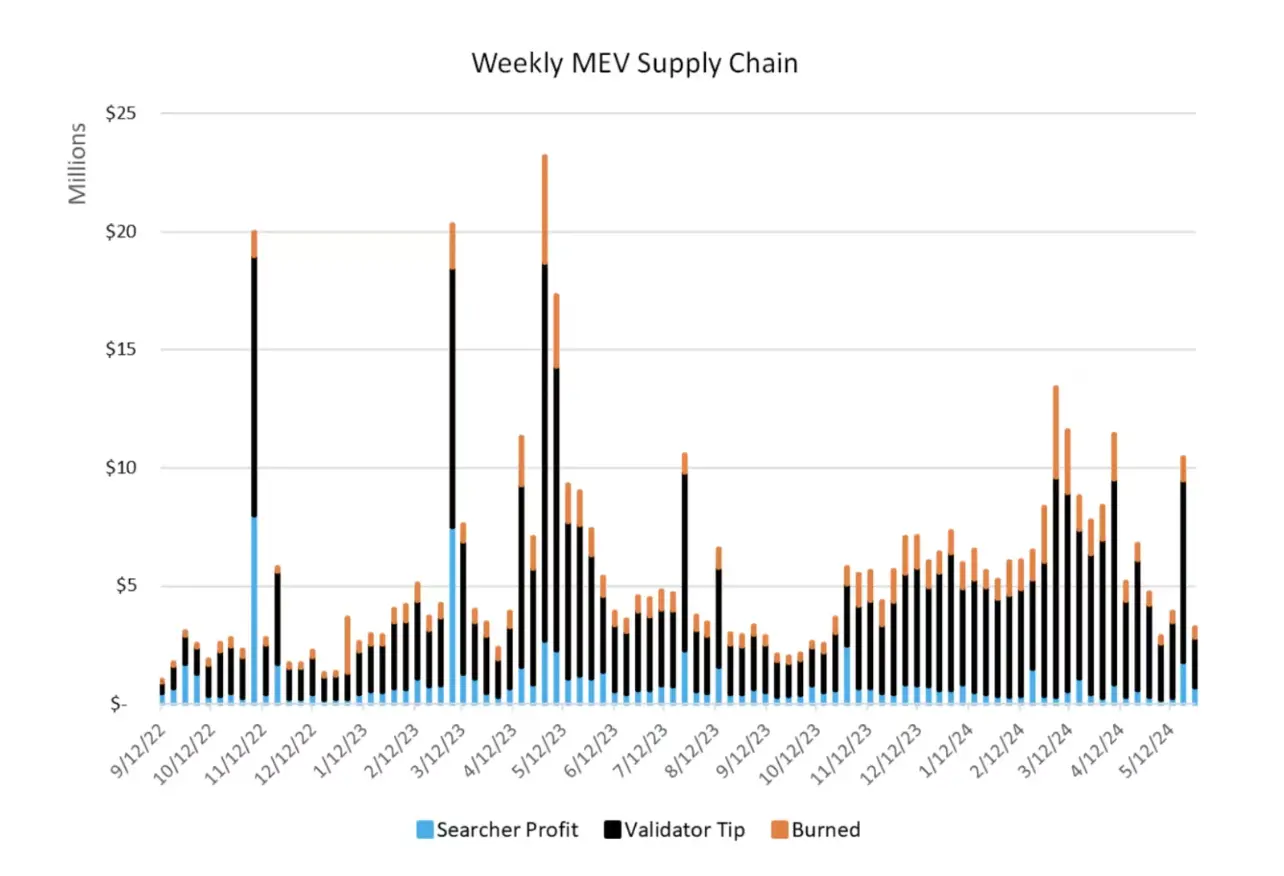

MEV is a permanent feature of blockchains and a permanent consumer of block space. The following chart shows MEV on Ethereum (the only chain with good public MEV data) as of the end of February 2024, distributed among MEV searcher profits, validator tips, and burned ETH. These figures do not include DeFi-CeFi arbitrage, which is essentially statistical rather than atomic and occurs both on-chain and off-chain.

Source: Will Nuelle, Galaxy Ventures

Searchers look for MEV opportunities and pay transaction fees for the chance to have their transactions included in blocks. Competition among searchers forces them to pay higher transaction fees than normal blockchain transactions to ensure inclusion, so a significant portion of the transaction fees paid for MEV ends up in the pockets of validators, resulting in slightly higher final earnings for validators compared to staking ETH. A portion of this is burned according to EIP-1559, ultimately benefiting all ETH holders; some becomes the profit from searchers' work. In 2023, the complete MEV supply chain averaged weekly earnings of $6.6 million, peaking at over $20 million in May (excluding profits from CeFi-DeFi arbitrage).

MEV Strategies

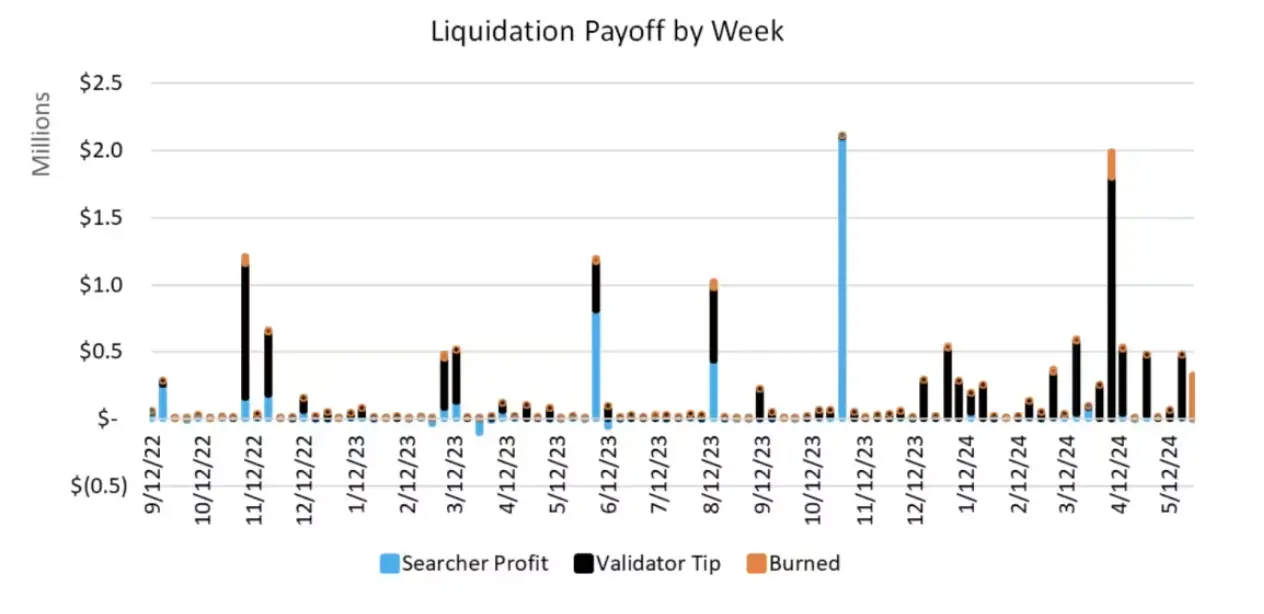

Different MEV strategies have varying returns and profit margins. Data shows that sandwich trading is a parasitic form of MEV that generated $212 million in revenue on Ethereum last year by initiating front-running and back-running trades against careless DEX users. Atomic arbitrage is more profitable as it balances prices in DEX pools, generating a total revenue of $126 million in 2023. Liquidation (the rewards for clearing bad debts in lending protocols like Maker, Aave, and Compound) generated only $7 million in revenue in 2024. Additionally, there are other forms of MEV, but they are more customized than systematic.

Source: Will Nuelle, Galaxy Ventures

CeFi-DeFi arbitrage is a more challenging strategy to quantify, and there is no public data to measure the profits from CeFi-DeFi arbitrage (as the CeFi part is opaque). Galaxy's tracked data indicates that CeFi-DeFi arbitrage earned approximately $98.5 million in 2023, but only accounted for about 60% of the market share. This is based on simulated CeFi quote data but could be higher or lower depending on specific builder strategies. Note that the confidence interval for CEX-DEX arbitrage is quite large.

Interestingly, the gross margins of different strategies indicate which strategies yield more profit for Ethereum/validators and which yield more profit for searchers. The gross margins for arbitrage and sandwich strategies are 18.6% and 14.2%, respectively, indicating that these strategies (i) are highly competitive and (ii) accumulate more value in fees for the base layer (Ethereum). Meanwhile, liquidation strategies have a gross margin of 51.1% but struggle to scale, making them less competitive (and less relevant in this discussion). CeFi-DeFi arbitrage has some scale, but it is less competitive due to deeper moats in order flow, builder concentration, and general statistical arbitrage complexity.

Source: Will Nuelle, Galaxy Ventures

Source: Will Nuelle, Galaxy Ventures

A Stable Relationship Between MEV and Block Space Demand

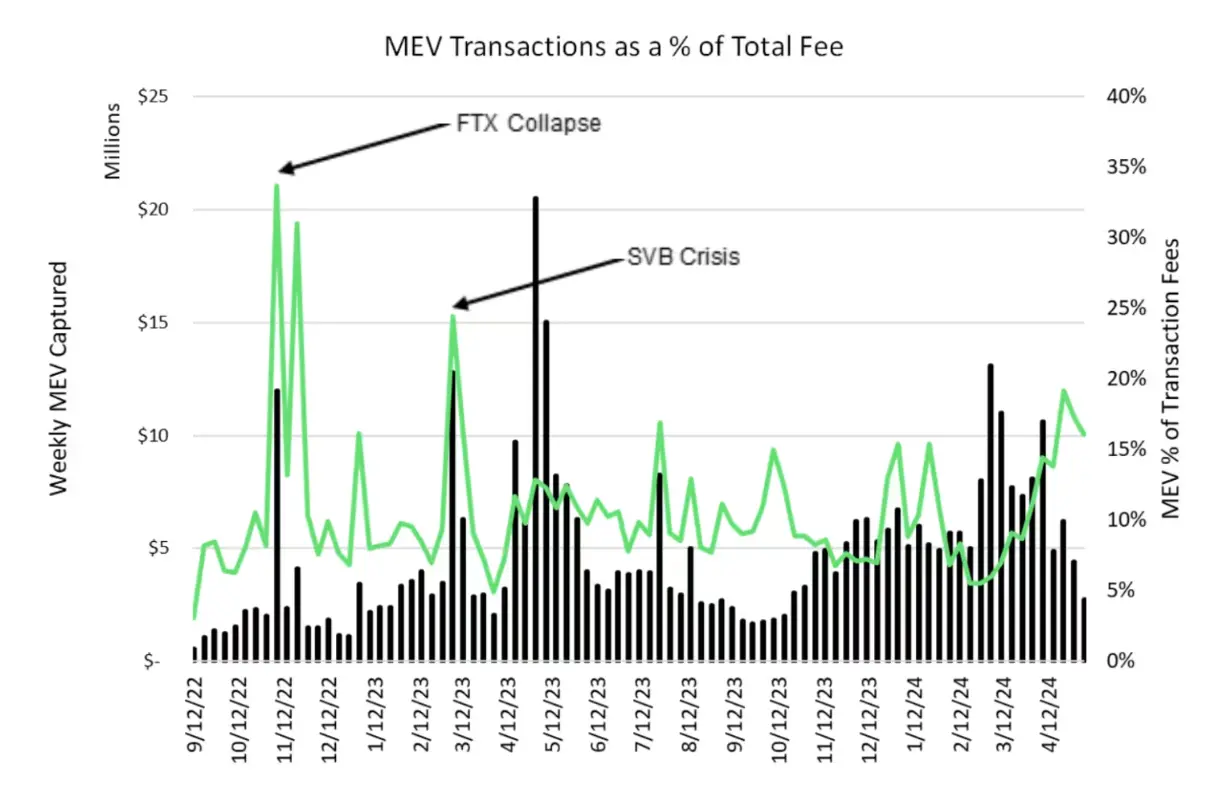

The percentage of transaction fees paid as MEV has remained stable over time, neither rising nor falling. As shown in the chart above, the weekly percentage of MEV in block space hovers around 10%. During weeks of significant price and trading volume fluctuations, such as the FTX collapse, this percentage can rise to 30% of transaction fees. During the week of the Silicon Valley Bank crisis, MEV also reached 25% of transaction fees. This is a mean-reverting time series that fluctuates very similarly to financial markets. In fact, MEV activity may be closely related to volatility itself.

Source: Will Nuelle, Galaxy Ventures

Source: Will Nuelle, Galaxy Ventures

In other words, if the transaction fee consumption for a given week is $100 million, we can simply predict that 90% comes from exogenous demand for using applications, while 10% is generated endogenously from risk-free profits due to state changes that week. If 30% is created by MEV and 70% by non-MEV, it is reasonable to believe that the following week will likely return to normal. We will closely monitor this situation to see how it changes over time.

It is worth noting that this invariance of around 10% applies only to financial applications on the blockchain (DEXs and lending protocols). These applications generate MEV, unlike stablecoin applications or games. If the dominance of financial applications declines over the long term, then the relevance of MEV will also decline unless new forms of stablecoin or game MEV are discovered.

Conclusion: MEV Currently Plays a Minor Role but Will Be Important in the Future

While MEV has the potential to disrupt protocol incentives and is a permanent consumer of block space, its actual financial contribution to Ethereum is relatively small, accounting for only 10% of transaction fees. During weeks of black swan market events like FTX or Silicon Valley Bank, this percentage may rise to 25% or higher, but this is an exception rather than the norm, and historically, this percentage has returned to a stable state. So what role does MEV play in the block space business model? In some ways, it acts as a demand multiplier, increasing exogenous demand for using applications by 1.1-1.3 times.

Nonetheless, the impact of MEV on future block space consumption could be significant. Blockchains like Solana and Monad have much cheaper transaction fees, and compared to high-fee chains like Ethereum, the proportion of block space consumed by MEV on low-fee chains may be larger. A simple example illustrates this:

Source: Will Nuelle, Galaxy Ventures

The most profitable blockchains in the future are likely to be those that possess both of the following characteristics: (a) lower transaction fees that stimulate demand for network activity, and (b) primarily utilize network activity in the form of validator/sorter/burn capturing MEV.

The existence of phenomena like MEV is yet another reason why block space represents an unprecedented business model. Its unique characteristics make it a compelling business model worthy of long-term investment. Finally, we reiterate the advantages and disadvantages of block space:

Advantages:

- Strong net income margins. The sale of block space is the only business model with zero operating costs. Ethereum's net income margin fluctuates significantly, but since January 2023, its average net income margin has been 33.9%.

- Easy to generate network effects. Generally, SaaS products lack network effects, while social media applications and marketplaces do. As more applications and capital join, block space improves, continuously driving up transaction fees with network effects. Network effects can generate additional revenue through MEV.

- Block space scales over time. Some block space will benefit from scaling, such as L2s, which have further growth potential.

- Exogenous demand multiplier effect of MEV. MEV is a feature that always exists in blockchain systems. While MEV may undermine consensus, it contributes significantly to ecosystem fees. For every $1 in transaction fees on Ethereum, approximately $0.10-$0.30 in MEV fees is generated.

Weaknesses:

- Lower gross margins, but improving. The cost of producing a unit of block space (e.g., 1M gas) is high and may require more than 66% of the future profits from that block space. Block space is a low-margin business.

- Strong cyclicality. Revenue from selling block space is highly cyclical. It depends on market conditions and is often closely related to market volatility.