In-depth analysis of the relationship between Layer1 project valuation, profitability, and token issuance

This article compares the profitability of PoW and PoS blockchains, the differences between Ethereum and Solana, and the importance of blockchain profitability to investors.

This article compares the profitability of PoW and PoS blockchains, the differences between Ethereum and Solana, and the importance of blockchain profitability to investors.Original Title: 《Blockchain Profitability \& Issuance - Does It Matter ?》

Written by: DONOVAN CHOY, THOR, HYPHIN

Compiled by: Kate, Mars Finance

A report exploring different schools of thought on blockchain profitability.

Introduction

How profitable are PoW (Proof of Work) and PoS (Proof of Stake) blockchains? How does Ethereum compare to Solana? Is blockchain profitability important for investors? What does Vitalik do with Ethereum's gas fees?

Crypto Twitter has recently been embroiled in these questions. This article attempts to unravel these big-picture issues surrounding L1 valuation in Web3.

PoW Ethereum Profitability

Suppose we want to determine which L1 token has the highest upside potential. The first step in the research is to understand the potential profitability of the blockchain. So, if you ask a Wall Street analyst how profitable blockchain is, they might calculate it like this:

Revenue (Total Transaction Fees) - Costs (Total Token Issuance) = Profit

When applied to PoW Ethereum:

The conclusion is simple: Ethereum PoW is unprofitable, and its business model is fundamentally broken. 100% of transaction fees are paid to miners, resulting in zero revenue for Ethereum. Worse still, the ETH issuance incentivizing blockchain validation is very high, making the chain unprofitable. Of course, we know in hindsight that ETH's price increased, but the price surge during those years was purely driven by speculative fervor rather than intrinsic factors.

EIP -1559 and Post-Merge Updates

As of 2024, there are mainly two criticisms of the above simple analysis. The first criticism points out that many changes have occurred since PoW, while the second criticism raises more subjective structural arguments (which will be discussed further in the next section).

What Has Changed?

Since EIP -1559 in August 2021, Ethereum gas fees have been divided into base fees and priority fees. The base fee is burned, making ETH scarcer and thus increasing its value, leading to an underestimation of its "real" value. On the other hand, the priority fee is paid as a tip to validators.

Since the merge in September 2022 and the transition to PoS, token issuance has significantly decreased.

Since Flashbot released the MEV-Boost software for PoS Ethereum, users have been paying additional block inclusion fees to validators, leading to an underestimation of revenue.

In summary, there are four variables affecting the profitability of the Ethereum network:

- Base Fees (Burned)

- Priority Fees (Paid to Validators)

- MEV (Paid to Validators)

- ETH Issuance/Inflation (Paid to Validators)

When we update the table above:

- Since EIP -1559, a portion of network transaction fees has been burned, as shown by the fees paid by users minus the portion paid to validators.

- 2023 is the first full year in which the network has achieved "profitability," largely due to the transition to PoS.

- MEV payments are all paid to validators, so ETH holders see no revenue.

Conclusion: Ethereum PoW was once very unprofitable, and its business model is fundamentally broken. However, due to the more efficient gas pricing from EIP -1559 and the significant reduction in token issuance since the merge, Ethereum is now operating a profitable business.

Note that PoW miners/PoS validators also spend on electricity and hardware, but this is omitted here as it is an external cost borne by validators rather than the "network." Since March 2024, blob fees are also a revenue item paid to Ethereum by L2 rollups, but this is relatively small and thus omitted as well.

Is Token Issuance a Cost?

The second criticism argues that viewing token issuance as a cost is completely wrong. Notable figures like Jon Charbonneau and Kyle Samani have made this argument, especially Anatoly, as seen in a recent debate with Justin Drake on Bankless.

Viewing token issuance as a cost implies that token holders are diluted—just like the Federal Reserve dilutes your dollar savings by printing money. But this is not the case, as users have the right to earn the network's inflation token issuance on PoS chains through liquid staking platforms like Lido. Additionally, ETH stakers can also earn priority fees and MEV payments.

If you have this mindset, then the question you should ask yourself is: What is the actual net yield of the ETH I invest in a liquid investment platform? Since I can easily obtain cash flow, why should I, as an ETH holder, care whether Ethereum is "profitable"?

Consider a thought experiment: all the money printed by the central bank is equally and effectively distributed to every citizen. In this case, no one would be worse off or better off. The Gini coefficient remains unchanged, and everyone's nominal holdings are higher, but the same amount of actual value is chasing the same amount of goods and services. Of course, the real world is not like this. When the printing press is running, the inflated money supply reaches different participants in the economy at different times, benefiting those who receive the new money supply first (known as the Cantillon effect). But this is essentially what is happening in the PoS blockchain economy.

Therefore, when everyone receives an equal amount of cash flow from the central bank's printing press, being obsessed with the "profitability" of the U.S. economy is meaningless, just as it is meaningless to focus on the "profitability" of the Ethereum blockchain.

And it doesn't stop there. If the logic of this analysis is correct and token issuance is not a cost, then it means that non-stakers are actually being diluted because they do not receive token issuance.

So the key analytical question is: What is the difference in value flow between Ethereum holders and Ethereum stakers?

Here are a few points to note:

- Priority fees, MEV payments, and ETH issuance now shift from "cost" items to "revenue" items.

- Due to the burning from EIP -1559 and the transition to PoS, ETH holders remain net positive. However, ETH stakers gain a larger share of value by contributing to network validation.

- For stakers here, a negligible cost item is the ~10% commission rate for staking on Lido.

In summary, a "non-profitable" blockchain may seem alarming, but stakers still receive net benefits from the value flow. The simple revenue - costs = profit framework mentioned above makes sense in TradFi because shareholders have legal claims to dividend payments or assets. However, stocks are different from L1 tokens, so the macroeconomic perspective of "blockchain profitability" is less relevant.

Solana Network Profitability and Value Flow

Now let's take a look at Solana.

- Solana's transaction fee model divides fees into voting transactions and non-voting transactions. Voting transactions are the voting signatures submitted by validators to the network consensus, while non-voting transactions are the primary indicators tracking network activity, as they refer to SOL transfers between different Solana accounts/smart contracts. Both are counted as revenue items here.

- From the network's POV, Solana is fundamentally unprofitable.

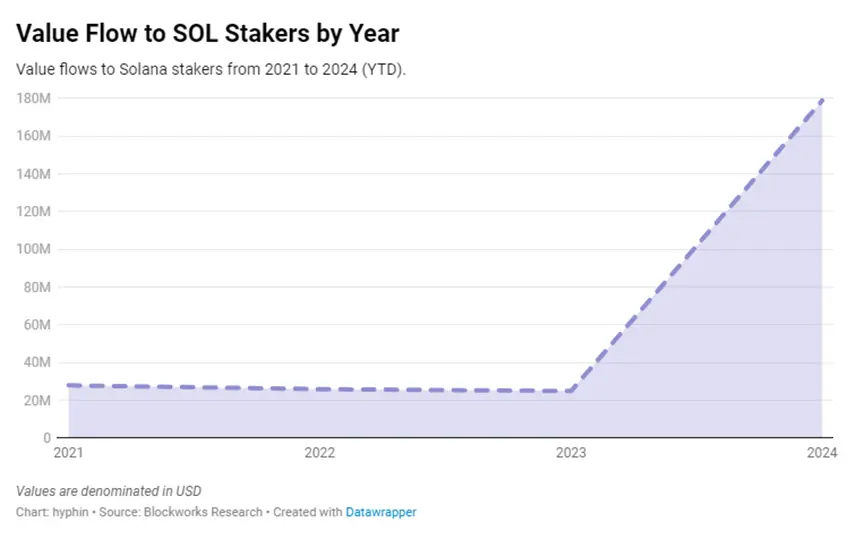

But as Solana's supporters tend to believe, the above valuation model is irrelevant because SOL holders can earn network issuance through staking. So, let's look at the value flow to SOL holders and stakers:

- As expected, due to the significant dilution of SOL holders' value from network issuance, the value flow for holders is negative. However, SOL stakers are net positive when receiving network issuance.

- Due to Solana's very cheap gas fees, the network suffers from anomalous incentives for junk transactions based on first-in-first-out. To mitigate this issue, Solana developers offer users the option to pay 50% of the priority fee to block builders (called "leaders"), with the remaining 50% burned. Both are included in revenue items, as SOL stakers gain value from both. Notably, governance changed this a week ago, allocating 100% of priority fees to validators.

A Brief Note on PoW Consensus

To bring this back to the point, value accumulation only applies to PoS chain L1 tokens.

In the case of PoW chains like Bitcoin (or pre-merge Ethereum), there is no such value accumulation because there is no "Lido" where you can choose to enter and receive a share of Bitcoin issuance. Bitcoin's issuance is a direct expense of the network, similar to the Federal Reserve printing dollars, diluting the actual value of anyone holding dollars.

Worse still, 100% of Bitcoin issuance is paid to miners, who spend significant electricity to provide services in exchange for rewards. Miners will sell Bitcoin to cover their operating costs, thus putting selling pressure on the market. In summary, if you hold Bitcoin, you are not only diluted by the token issuance rewards, but your holdings are also subject to significant selling pressure from miners.

All of this makes Bitcoin look like a terrible digital asset built on a broken token economics foundation. However, this conclusion stems from trying to force the same valuation model used for ETH onto BTC. Bitcoin maximalists might argue that this commits a serious analytical error by treating BTC and ETH as the same type of asset, whereas BTC is more like a commodity-like currency asset.

If that is the case, then valuing Bitcoin would require a different model that reasonably prices Bitcoin's monetary premium rather than simply using the revenue - costs = profit framework.

Bitcoin Monetary Inflation @ _BashCo

Conclusion

Regardless of which side of the debate you stand on, it is undeniable that in an ideal world, token issuance would be zero, or at least close to zero. As Polynya points out here, even if token holders have a simple way to avoid dilution, there is still a value loss for non-stakers. All non-stakers bear the inflationary pressure of token issuance—including those who keep tokens in cold wallets for security reasons, off-chain cryptocurrency investors, and those deploying L1 tokens into higher-risk DeFi activities, etc.

The main thought leaders in the Ethereum community often side with the debate that "token issuance is a cost," while alt-L1s stand on the other side. Given the significant efforts Ethereum developers are currently making to make ETH deflationary, along with ongoing discussions around further reducing ETH issuance, it is easy to understand why Ethereum leaders emphasize viewing issuance as a cost.

On the other hand, alt-L1s often have much higher token inflation rates, and chains like Solana tend to have much higher staking rates compared to Ethereum, which may explain the motivation for interpreting token issuance as a cost.