No longer the era of "easy money": A detailed analysis of the new characteristics and new patterns in the cryptocurrency industry

In this round, we can clearly feel that "the funds are not as sufficient."

In this round, we can clearly feel that "the funds are not as sufficient."Author: DaPangDun

1. This Bull Market is Different

Many people should have noticed that this bull market is significantly different from the previous one, mainly reflected in:

- The wealth effect is insufficient, and there is no broad-based rally like the last round; the choice of assets is very important, and one can easily incur losses, with the vast majority of cryptocurrencies underperforming BTC.

- The performance of value coins often lags behind that of Memecoins, with many value coins listed on exchanges experiencing a continuous decline.

- There is severe fragmentation among sectors, with funds only circulating within their own ecosystems, and rotation is not smooth, giving the market a feeling of lack of synergy.

- The airdrop industry has become highly competitive due to scripted and clustered development, leading to various impacts.

- The narrative led by BTC is not as "rapid and violent" as before, presenting a relatively cold state, and DEFI seems to be less favored in the BTC narrative.

- Although Web3 games received massive funding in the last round, they have not produced any blockbuster hits.

After observing these phenomena, I tried to explore the reasons behind them. We refer to the last bull market as the "water release bull" because of the massive liquidity injection globally (mainly in the US), with a very obvious overflow effect of funds. In this round, we can clearly feel that "funds are not so abundant." Is this feeling correct? We can find clues from the following sets of data.

2. Changes in Funds

2.1 US M2 Data

First, let's look at the five-year M2 data for the US. The green shaded area represents the M2 changes during the last bull market, while the yellow area represents the M2 changes in this round.

Combining the price changes of BTC during the corresponding periods, we can see:

1) During the last bull market, M2 showed a continuous growth trend, corresponding to a sustained rise in BTC prices (some periodic corrections are market adjustments and short-term fluctuations). Before M2 supply approached its peak, the market entered a downward channel due to "exhaustion of potential" and gradually entered a bear market.

2) During this bull market, M2 has hardly changed, and even showed a downward trend in the early stages. Therefore, this round is indeed not a "water release bull," and funds have not shown an increase. Thus, the viewpoint that the market feels insufficient funds is correct. Currently, BTC prices are reaching new highs, which, in my view, resemble a process of "value return," rather than a part of market FOMO.

2.2 Stablecoin Data

The changes in stablecoins usually reflect the inflow and outflow of external funds. Due to the special property of stablecoins being "active money," when stablecoins are continuously growing, it indicates that they are attracting funds from outside the ecosystem, which will produce a noticeable price effect.

Through Defillama, I retrieved data from 2021 to the present, and we can clearly see:

The current amount of stablecoins within the ecosystem is only about 10 billion USD more than the last BTC peak, still about 28.7 billion USD short of the previous high of 187 billion USD.

Of course, we need to be more rigorous. The SEC approved the BTC ETF on January 11, 2024, which is believed to bring significant incremental funds to Crypto. Therefore, we need to consider this part of the incremental funds that has not yet been reflected in stablecoins, as they represent real purchasing power.

I have compiled the holdings of Grayscale's GBTC and the total holdings of all larger BTC ETFs as follows:

From the overall holdings, the increment is approximately 850991 - 655800 = 195191 BTC. If we calculate the holding price at 50,000 - 60,000 USD, the incremental funds are approximately between 9.8 billion and 11.7 billion USD.

If we express the incremental purchasing power of the ETF in the form of stablecoins, we can see that the current number of stablecoins in Crypto has still not reached the peak of the last bull market, although the difference is not significant. Considering that the ETF has only been around for four months, from a long-term perspective, we can indeed maintain a certain degree of optimism.

2.3 Crypto Market Cap Data

The Crypto market cap generally reflects the "funding heat" of the entire industry, that is, the market's attention and interest in the industry.

From the chart below, we can see: the last peak was 3.009T, and the current market cap is 2.439T, accounting for 81%. Although this bull market is clearly not over, the market is still very cautious from a data perspective.

We need to deeply realize: although we can have optimistic expectations for future "interest rate cuts and liquidity injections" and ETF incremental funds, the current market funds are indeed not abundant!

In a market where funds are not so abundant, using limited money to do more things and allocate to different roles will inevitably intensify the competition within the market. This is also the inherent reason we can see various "changes." In this scenario, the development status and logic of various parts of the industry have changed, and the industry will enter a new pattern.

3. Industry Observation

3.1 Almost No Broad-Based Rally

Although funds have not reached the previous peak, they are still relatively close. Why do many cryptocurrencies perform poorly and there is no obvious broad-based rally?

I attempted to analyze the market capitalization of various cryptocurrencies (mainly the top 100) at the previous peak and the market capitalization share of cryptocurrencies in this round, resulting in the following data:

Based on the corresponding total market cap data of Crypto at that time, we can create a comparative chart of the share data:

From the above chart, we can see: in this round, the tendency for funds to "focus on the top" is more evident.

If we think more carefully, we will also find:

1) This round has added many high market cap low circulation cryptocurrencies, which on one hand divert funds, and on the other hand increase the degree of market cap bubble;

2) Many "old coins" still maintain a relatively high market cap under the operation of market makers;

In such a situation, where is the funding to create a broad-based rally?! And because there is no broad-based effect, in the competition, people tend to be conservative and choose more stable top cryptocurrencies, further exacerbating the lack of funds for other cryptocurrencies.

New Pattern Judgment

We need to wait for the continuous increment brought by the ETF to gather more consensus within the ecosystem, and we also need to wait for a new era of liquidity injection to boost liquidity within the ecosystem.

3.2 No One is Taking the Risk

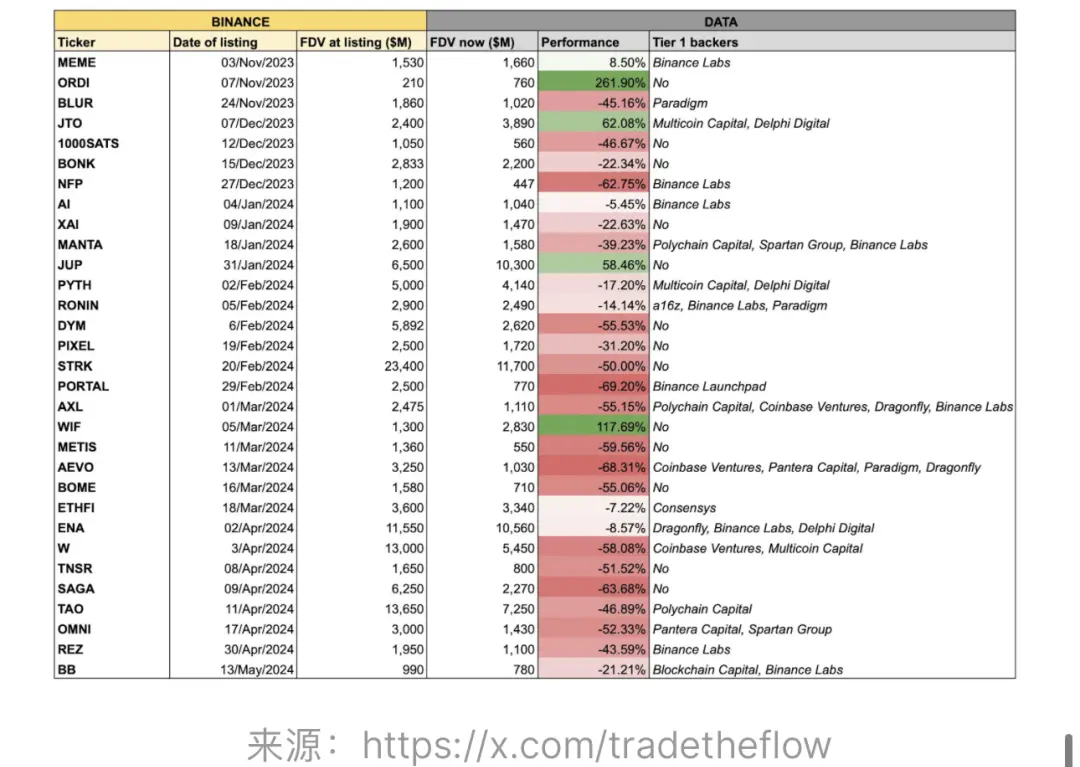

The phrase "no one is taking the risk" has become very popular recently. The vast majority of "VC coins" peaked upon listing. Binance recently published an article titled "Low Float & High FDV: How Did We Get Here?" which highlighted:

1) Aggressive valuations have overdrawn potential, leaving retail investors with little profit space.

2) Continuous unlocking has made it nearly impossible for tokens to have upward space.

These factors have led to retail investors having little motivation to take risks.

The chart below shows the FDV situation of recent Binance listings and the performance of the cryptocurrencies:

From the above table, we can derive the following data:

The average FDV of listed cryptocurrencies is 4.2 billion USD, which far exceeds the FDV data of Binance listings during the last bull market.

It seems we have found the reason for "no one is taking the risk," but if we change our perspective and look at it from the angle of "competition," we might see another layer of reason for "Low Float & High FDV."

In Low Float & High FDV, High FDV is key; Low Float is merely a way to control the market. By continuously unlocking over the long term, it alleviates short-term selling pressure.

For a project token, the parties involved mainly include: the project party, VC, exchanges, market makers, and secondary market users (I have not included airdrop participants here to simplify the structure).

Consider this question: Who benefits from High FDV?

1) For the project party, they obviously want a high FDV, as it represents future value and returns.

2) VCs also want a high FDV, as it can generate sufficient investment returns and a strong portfolio; some VCs may sell part of their investments at a discount through OTC transactions to realize profits, as most people are still very interested in "discounts," and a high FDV allows for good profits even after discounts.

3) Exchanges are a "complex" part; from a trading perspective, the level of FDV is not particularly important; however, many exchanges are also investment institutions for projects, especially large exchanges that can obtain early undervalued tokens, so they may also hope for a high project FDV, unless this phenomenon severely impacts their trading (a significant portion of exchange profits comes from trading fees).

4) Market makers typically operate according to a given plan and may not care about the level of FDV; their model is to earn profits through quantitative programs, etc.

5) For secondary market users, a high FDV is clearly a bad thing, as it overdraws future expectations, and after purchasing, they still have to bear the risks brought by continuous unlocking.

This constructs "a world where only retail investors are likely to get hurt," so "why take the risk?!"

New Pattern Judgment

For project tokens, it is clear that blindly pushing up the FDV of the project is not a good strategy. The project party needs to have a more reasonable FDV positioning and token release/distribution plan to demonstrate higher vitality.

Exchanges need to save themselves by allocating limited customer resources to higher-quality project tokens, thus maintaining more active trading data and better market performance.

VCs need to have more reasonable valuations for projects, especially when researching project testing or participation data, they need to fully consider the "witch content" in the data to achieve more accurate valuations. (In the future, providing witch data analysis services to VCs may become a startup opportunity.)

3.3 Memecoins > Value Coins

The phenomenon of no one taking the risk has led to a series of impacts. Users will change their previous logic of participating in Crypto when investing. For example, instead of choosing value coins (usually referred to as "high FDV coins"), they prefer to choose Memecoins, which have three obvious advantages over value coins:

1) Memes usually have low valuations and high potential space.

2) Memes are generally fully circulated, so there is no need to worry about unlocking pressure. Therefore, once market makers push them up, there will generally be people following.

3) The token distribution of most Memes is very fair, giving ordinary users a chance to participate early.

However, we also need to recognize that:

1) The short-term hype of Memes is not a new phenomenon; there was also a Meme craze in the last round, giving birth to globally renowned Memes like Doge and Shib. However, most Memecoins provide emotional value, which has issues such as "fast transfer, high volatility, and lack of durability." The vast majority (or 99.9%) of Memes are fleeting.

2) Among the current top 50 cryptocurrencies, Memecoins occupy four positions (DOGE/SHIB/PEPE/WIF), while the vast majority are still firmly held by value coins.

New Pattern Judgment

The hype of Memes is limited. Truly valuable value coins will still experience a "value return" after solving some of their own issues.

3.4 Airdrop Anomalies

The airdrop industry was not booming in the last round. After several large airdrops, especially after Arb, airdrops began to enter the "multi-account era," and the airdrop track became one of the hottest tracks, with about 50% of KOLs on Twitter participating in this track. Subsequently, the industry changed rapidly, with specialization, clustering, and automation gradually evolving and maturing, leading to the emergence of dedicated studios, automated interaction systems, and proxy interaction services. Due to the special nature of airdrops, it has become the most fiercely competitive track.

1) "Airdrop farming" has become an essential skill for users.

Let's look at several charts, including: daily new addresses cross-chain numbers for Arb/Starknet/daily transaction numbers for L0/daily new addresses cross-chain numbers for Zksync.

It is evident that after the project party releases snapshots or suspected snapshot information, the data shows a significant decline, proving that most participating addresses are involved in the project solely for the purpose of airdrops. Based on the estimated value of active users in Crypto, it is clear that single users have multiple accounts.

2) Specialization, automation, and strategization have become mainstream.

When an industry has excess profits, it will inevitably attract competition. For airdrop farming, single users with multiple accounts will eventually reach a limit, so automation has become the first development direction. Automated clicking, automated simulation operations, automated contract interactions, etc., quickly became development priorities, leading to a large number of studios; subsequently, participants found that blind interactions were not only insufficient in dimension but also not cost-effective, leading to the emergence of "professional interaction solutions" and "professional dimension analysis." In this context, "witches" have become the "sword of Damocles" hanging over every airdrop user, thus deeper strategic theories such as "simulating real users" and "effective interactions" have gradually been proposed.

3) The game of spear and shield.

In the airdrop track, there are two related parties: the project party and the users. Among the users, there are "ordinary users" and "clustered users."

For project parties, they need farmers to "provide" good project data to facilitate project financing, but they also hope to incentivize airdrops to "real users." On one hand, this rewards genuine participants, and on the other hand, it can reduce early selling pressure after airdrop distribution (as clustered users typically sell immediately, showing no faith in the project).

For users, since they have no opportunity to participate in the primary market, one possible way to obtain tokens is to strive for the project's airdrop. They need to earn profits through farming. Although clustering has a high threshold (some proxy farming services have greatly lowered this threshold), once successful, they can potentially earn several times, dozens of times, or even hundreds of times the manual profits, so they are motivated to develop clustering.

However, the emergence of clustered users is detrimental to ordinary users, as it leads to the creation of a large number of accounts (you can observe that many projects now have millions of participating addresses), significantly reducing the profits for ordinary users. Therefore, they are motivated to see project parties investigate and eliminate clustered users.

Thus, the "mutual benefit" that existed between project parties and users in the early, low-volume, immature stage has evolved into a "love-hate relationship."

In this process, due to the increasingly strong dominant position of project parties, they have gained an advantage in the competition, leading to many "anomalies."

1) Early projects tended to use "standard screening" to eliminate some low-quality interaction addresses and then "distribute evenly," trying to ensure that participants achieve a high level of satisfaction.

2) Hop boldly began analyzing "batch addresses" on GitHub, initiating the "witch-hunting era."

3) Some project parties have adjusted the distribution of airdrops by increasing airdrops for other dimensions (such as developers and contributors).

4) Project parties have gradually become more aggressive: some projects continuously PUA users but ultimately provide very low distribution amounts; some projects even exploit user data and "break promises," while others have initiated "community reporting" (mobilizing the masses) tactics to address witch issues. Some project parties are even unwilling to disclose screening criteria… Such "anomalies" will continue.

5) During this period, data analysis methods have also gradually upgraded from manual screening and standard filtering to AI analysis of clusters, spanning multiple chains.

The competition continues, and the airdrop track has entered deep waters.

New Pattern Judgment:

Clustering has indeed had a huge impact on this track, leading to extreme internal competition in the airdrop industry. The difficulty of obtaining airdrops will continue to increase, and this track will certainly still exist, but excess returns will gradually decrease until they approach the industry average level.

For project parties, it is essential to deeply collaborate with "truly professional witch analysis teams" (professional data analysis teams are not necessarily professional witch analysis teams) to discover clustering traces from multiple dimensions.

For clustered users, they need to conduct in-depth research on participation strategies while fully considering risks, forming small clusters, diversifying, and meeting the screening standards.

For ordinary users, they should conduct thorough project research and participate in projects with a better cost-performance ratio given their limited time/funds. They should extend strategies based on a "symbiotic approach" that is deeply tied to the project (a community of interests) and fully explore blue ocean sub-tracks within the airdrop space.

3.5 The Coldness of BTC Ecosystem Narrative

The most important mainline in this round is the narrative of the BTC ecosystem, which includes not only the ETF but also the resulting ecological demand. However, unlike the narrative brought by DEFI + NFT in the last round, we see many BTC-L2s and various DApps based on BTC, but the narrative of BTC in this round still feels relatively cold, reminiscent of "loud thunder but little rain." After conducting in-depth research, I have made the following "reasonable" analysis of the reasons:

1) Different quality. BTC holders are significantly different from ETH holders, as they have a very high demand for "security" and "fund control," which makes them wary of various L2s and have low acceptance. Many people only recognize BTC's value storage property and do not believe that BTC should participate in financial activities. This requires a long educational process, such as Babylon's "Time-Lock based BTC staking scheme," which is doing such education.

2) High technical difficulty. Due to the complexity of BTC technology and the lack of scalability of the BTC mainnet, developing based on BTC, especially native development, is particularly challenging. Therefore, many projects cannot be launched quickly or elegantly, and various issues may arise throughout the process, leading to a lack of user experience.

3) SanDEFI is path-dependent. Many people believe that as long as DEFI is built on BTC, it can replicate the glory of the last round. This is an illusion created by "path dependence." Let's look at a few sets of data:

This is the TVL distribution chart on ETH. We can see that the main part has shifted from "MakerDAO + Uniswap + Opensea" to "Eigenlayer + Lido Finance."

The former represents DEFI + NFT, which are on-chain activities generating a lot of fees and are very active funds, while the latter consists entirely of "staked funds," which are inactive funds.

We can also verify the activity of funds from the fees, as shown in the chart below:

It is already evident on ETH that user investment tendencies have shifted from active investment to passive investment. Therefore, expecting the BTC ecosystem to thrive simply because there is DEFI is unrealistic in the short term.

New Pattern Judgment:

The BTC ecosystem narrative needs time to develop. DEFI is merely foundational infrastructure but may not necessarily lead the development of this round.

Activating BTC holders to use BTC is of utmost importance. The staking and restaking tracks will be key to achieving this. Native staking solutions will enable the secure use of BTC, while the yields from restaking will attract continuous development in this process.

3.6 Exploration in the Gaming Industry

Games were a star track in the last round, receiving massive funding and once considered one of the keys to achieving Web3 mass adoption. However, even now, we have not seen such effects. While there is the factor of "good game development takes time," I believe the core issue of "Web3 game economics" has not been resolved.

The most eye-catching game in the last round was the wildly popular "running shoes," but it only had a lifecycle of about "2-3 months," making this economic model unsustainable.

Of course, we can see many explorations in the gaming track, such as:

1) Emphasizing the combination of "playability" and "economics." Overemphasizing economics will inevitably turn games into short-lived Ponzi schemes. Moreover, Crypto users particularly value "economics," and once the economics decline, they will shift their focus. Since the number of people within the ecosystem is limited, attracting more outsiders through "playability" is essential for the long-term development of games.

2) No longer overly pursuing data, with more prudent designs for token economic models. Various means are used within games to control the release and consumption of tokens, aiming to extend the game's lifecycle as much as possible.

Taking Big Time and Pixels as examples, the former has seen participation and profitability from many users after six months, while the latter has seen similar results after three months.

New Pattern Judgment

The gaming industry is continuously exploring. With many games set to launch in the second half of the year, in the current market lacking hotspots, we may witness an explosion in the gaming track.

The simple "buying native tokens strategy" may likely fail in this round, as gaming projects will focus on maintaining long-term sustainability. Therefore, allowing game participants to profit during the gaming process may be a better strategy than pushing up token prices. However, at the same time, the profit space for single accounts will be greatly compressed, so studios may have more advantages.

4. Conclusion

In my limited understanding, the fundamentals of this round of the industry (the main tone) have changed, and the endogenous logic of many tracks has undergone significant changes. What we can do, and must do, is to "adjust our understanding" to adapt to the "new pattern of industry development." Here, "we" includes not only ordinary users like you and me but also other participants in the industry.

As the industry matures, the degree of competition will further intensify. Stagnation and complaints are meaningless; considering from the perspective of competition may help find that "balance point."