Comparative analysis of Farcaster/FT/UXLINK/Cyber, how to find the North Star metric for SocialFi?

From the perspective of social network forms, Farcaster and UXLINK have relatively stronger social attributes, which can keep the entire economy sufficiently resilient.

From the perspective of social network forms, Farcaster and UXLINK have relatively stronger social attributes, which can keep the entire economy sufficiently resilient.Written by: Sirius & Joe, Deep Tide TechFlow

Social products have always been a controversial field, whether in traditional internet or on-chain, with ongoing debates about social applications. As Marx famously said, "Man is the sum of all social relations." Abstracting the underlying logic of social products, we can derive the following logic: the core of a social product is to help users establish some form of social relationships, generate interactions, convey information, and expand their social networks on the application. If this is achieved, it can be considered a successful social product.

Therefore, based on different forms of social networks, countless well-known products have emerged in the traditional internet, such as Facebook, WeChat, Soul, etc. They build social networks targeting various social scenarios like acquaintances, strangers, and campuses, which are social products in the traditional internet.

For Web3 social products, due to characteristics like financialized asset issuance, the social network adds the "Fi" attribute. How to issue assets based on social networks, or how to build social networks through assets, is the core point of Web3 SocialFi projects. Moreover, the decentralized anti-censorship liberal ideology imposes higher demands on project teams regarding content control, making the SocialFi track one of the most challenging types of products to build among all Web3 products.

In this article, we will analyze several well-developed SocialFi products on the market, including Farcaster, FriendTech, UXLINK, and CyberConnect, and explore the growth paths of SocialFi products.

From User Address Count to Asset Value: How to Determine the True Growth of SocialFi?

As mentioned earlier, the core of SocialFi lies in the combination of social networks and assets. Whether issuing assets based on social networks or establishing social networks based on assets is the fundamental logic of SocialFi products. Next, we will analyze the aforementioned products from the perspectives of social networks and asset issuance, and then compare indicators across various dimensions of these products.

Social Network Forms

The social network topology in Farcaster is similar to that of Twitter, both being attention-based social networks with a relatively open structure. FriendTech, on the other hand, refines and strengthens the social network on top of Twitter, forming a closed network centered around individual nodes. Compared to Farcaster and FriendTech, which inherit Twitter's attention-centric online social network, UXLINK focuses on real-world social networks, bringing acquaintance-based social interactions on-chain. As for CyberConnect, it forms social networks through on-chain activities.

Asset Issuance Aspect

Farcaster positions itself as a foundational layer for social interactions, relatively lacking strong "Fi" attributes, but possessing a stronger community culture attribute, resulting in the core asset $degen. FriendTech v1 has taken asset issuance to the extreme, creating a Ponzi flywheel through Bonding Curve design, endowing each KOL's social network with asset bubbles, with the value in the Twitter social network fully reflected by the liquidity of room keys. UXLINK, compared to the first two, is more balanced; its dual-token model design provides greater stability and health to the entire system, allowing for more sustainable incentives for users to create value within the social network. CyberConnect, however, governs solely through its native token, relatively lacking incentives for social network expansion.

After completing the qualitative analysis, we need to begin the quantitative analysis. We will first select basic indicators from the social and asset layers for judgment. In terms of social attributes, we will use the number of active users on the protocol as an indicator; while for the asset layer, we will select the market value of the protocol's core asset as an indicator.

Social Attributes

Number of Active Addresses on the Protocol

Farcaster's DAU began to grow rapidly in February this year, declined in March, and then saw an influx of new users.

FriendTech

In the v1 version, users were active to earn points for airdrops. From the end of last year to April this year, due to the delay in token issuance by FriendTech, user confidence declined, leading to user loss. After the v2 token issuance, the majority of users chose to abandon the platform.

UXLINK has shown astonishing growth this year, reaching nearly 500K addresses in May, quietly surpassing the user base of other protocols by several times.

CyberConnect's user count experienced a rebound in the first half of this year, but relatively lacked momentum afterward.

Overall, UXLINK is undoubtedly the hottest blockchain social infrastructure at present, with on-chain activity far exceeding that of the other three major competitors in the SocialFi field. According to UAW (Unique Active Wallets), UXLINK's active wallet count reached 729.5K, ranking first among all Social Media Dapps.

In contrast, the UAW of the other three mainstream SocialFi products during the same period is far lower than that of UXLINK. Although this indicator mainly reflects the short-term on-chain activity of each product, it also proves that the attention of current Web3 social players has been significantly attracted to UXLINK.

Asset Attributes

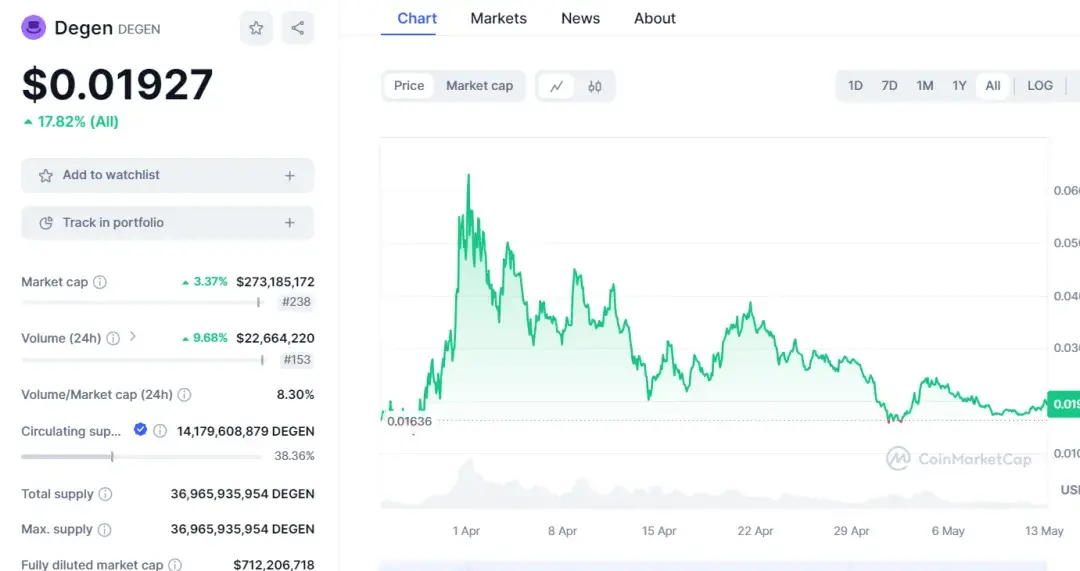

- Farcaster's asset attributes are relatively weak; here we select the community-generated asset degen as a representative asset. In April, its price surged with the popularity of the base ecosystem, but recently it has declined as the ecosystem cooled down.

FriendTech's token price remained relatively stable after the v2 token issuance, digesting the airdrop selling pressure.

- CyberConnect's token was issued over two years ago, and its price increased in the first half of this year due to hype in the track, but then it fell back to a low point.

- UXLINK has not issued any assets yet, so it will not be compared here.

In summary, UXLINK ranks first among current Web3 SocialFi products in terms of user count due to its astonishing social network expansion rate, while FriendTech attracts players eager to earn money through its innovative asset issuance mechanism.

Deep Factors Behind the Surface: Focusing on the North Star Metric

If we abstract user behavior in social products, we can describe it with the following pattern: "Users expand their social networks within the product and engage in interactions to complete information transmission." With the addition of asset attributes, the behavior can be expanded to include asset transactions alongside information transmission. In SocialFi products, information exchange often accompanies asset transactions, bringing ecological activity to the entire economy, and the products themselves can gain revenue from the economic activities within the ecosystem. Therefore, in this article, we select protocol revenue as the North Star metric to measure a social product.

- FriendTech experienced a peak upon release due to its innovative asset issuance mechanism, but as the heat declined, the economic activity within the ecosystem continued to decrease. However, after the v2 token issuance, the airdrop and innovative club design reignited interest.

- Farcaster saw a strong growth wave this year with the explosion of the base ecosystem, and the influx of new users led to an increase in protocol revenue.

- CyberConnect's revenue approached zero after the airdrop, indicating that users do not have strong genuine social needs on this product.

- UXLINK's economy is relatively early, and there is no data available, so it is not listed here.

In SocialFi, if we say that one must choose between "Social" and "Fi," then products centered around "Fi" will prevail in competition. After all, in Web3, transactions are the fundamental needs of all users.

Mapping Indicators to Products: How Should Product Design Optimize?

We can see that the rise of the aforementioned representative SocialFi products and the activity of their economies are strongly correlated with asset issuance behavior. This reflects that for Web3 products, focusing on asset issuance is the first principle, and transactions are the underlying needs of users. All SocialFi products should consider how to embed users' transaction behaviors into their social networks.

For CyberConnect, there are no transaction scenarios present in the product. The initial user activity was driven by airdrop rules rather than genuine social needs, which explains the significant drop in economic activity after the airdrop ended.

For Farcaster, during the ice age, the decentralized front-end retained many liberal users who were averse to Twitter's speech censorship, preserving the spark for resurgence. As a quality alpha gathering place on the base chain, it became active with the rise of the base ecosystem.

For FriendTech, it initially attracted users to engage in social behavior through airdrops. In v2, it helped influencers create clubs to issue tokens for monetization, providing ordinary users with tradable assets to maintain economic activity. However, the trading behavior is not very evident, and the Farcaster team seems to downplay the "Fi" attributes.

From the perspective of token issuance, FriendTech and UXLINK have the most user-friendly designs, making it easier to create wealth effects that attract users. In terms of social network forms, Farcaster and UXLINK have relatively stronger social attributes, allowing the entire economy to maintain sufficient resilience. Therefore, we can look forward to the performance of both after their launch and pay attention to asset issuance based on acquaintance social networks.