Understanding the "Meta Game" of Crypto: The Core Driving Forces Behind Market Narratives and Behavioral Changes

Each meta-game is different; they have similarities, but none are exactly the same.

Each meta-game is different; they have similarities, but none are exactly the same.Original Title: “Understanding the Meta-game”

Author: MIDAS CAPITAL

Translated by: Deep Tide TechFlow

Introduction

The concept of the meta-game is one of the more obscure concepts in the crypto space; it lacks a specific definition and does not have a fixed structure. It is something that is understood by those who know it. However, once you see it, it is hard to unsee it. In today’s article, I will attempt to unravel my perspective on it, hoping that readers can gain a clearer understanding of the meta-game and how to think about it.

Before we begin, it is important to note that the concept of the meta-game was popularized by Cobie in his article Trading the Metagame. Well-known traders like Dan from Light Crypto and CMS Holdings have also mentioned this concept in various podcasts. This idea is not new, but I hope to provide some new insights and build a structure around it.

Understanding the meta-game through the branch of behavioral economics known as game theory is the best way. It involves understanding the rules of the game, the best response functions of your opponents, and your optimal response function given all other information. We will use intuition and look at data to analyze these games and understand how to play each game with an optimal strategy.

It is important to understand that each meta-game is different. They have similarities, but none are exactly the same. Therefore, it is crucial to have an overarching framework and develop strategies based on that. This is what we will explore today.

What is the Meta-game?

I will not define the meta-game. It is more useful to explain how its mechanisms work and the framework through which we understand it. The meta-game has several components, which can be summarized as follows:

- Fundamental Mechanism

- Behavioral Changes

- Best Response Function

- Reflexive Loop

The fundamental mechanism can be seen as the foundation of the meta-game, which can be broken down as follows:

- Catalyst, usually (but not limited to) price movements—this triggers a narrative that changes with the price. The reasons for price movements can often be traced back to protocol upgrades, KPIs, or other events/indicators.

- The essence of the catalyst is the fundamental mechanism, which supports a reflexive loop.

Behavioral changes are the ways market participants express their views in response to the catalyst.

The best response function is how you, as a trader, should respond to the catalyst, how other market participants perceive the catalyst, and how they will respond to it. The best response function involves considering position size, entry, and exit.

The reflexive loop can be categorized as follows:

- Market participants identify the fundamental mechanism → engage in the game → prices behave in accordance with the game rules → the rules become increasingly apparent → more participants identify the fundamental mechanism → more players enter the game → and so on.

These four components provide a high-level overview of how the meta-game develops, evolves, and dissipates.

Theoretical Framework

Below is a flowchart that details how to start from identifying the meta-game, to understanding it, and then hoping to extract value from it. Let’s work through this in more detail. First, some theory, and then we will look at some examples and data.

Step 1: Identify potential meta-games, observe/look for the following:

- Developing narratives, sentiment analysis, anomalous price behavior.

- Positioning oneself as a protocol or sector solving known problems.

- Widely known and understood binary events.

Step 2: Identify the fundamental mechanism

Given the catalyst and its perceived nature, how does it drive changes in market participant behavior?

There are two types of fundamental mechanisms: self-reinforcing and self-defeating.

Self-reinforcing: A persistent fundamental mechanism where the catalyst is ongoing, thus the meta-game will exist for a while. For example, BTC ETF inflows/outflows—given that data is released daily, this can be seen as a repeated interaction game.

Self-defeating: A fundamental mechanism that drives a behavior, leading to the rapid dissipation of the meta-game. For example, Facebook rebranding to META—this is a one-time event and can be viewed as a single interaction game.

Step 3: Hypothesize about the duration of the meta-game

- The nuances of the fundamental mechanism determine the duration of the game, as well as entry and exit strategies.

- Generally speaking, self-reinforcing meta-games lead to the creation of sub-meta-games, while self-defeating meta-games tend to dissipate as quickly as they appear.

Step 4: Quantify the persistence of the fundamental mechanism

- It is necessary to hypothesize whether the game is self-reinforcing or self-defeating, and then find data that either substantiates or invalidates these hypotheses.

- For example, if we are playing a Meme meta-game, looking at relative trading volume (as a proxy for attention) is useful.

- For instance, if we are playing the BTC ETF meta-game, observing ETF inflows/outflows, their sources, and how prices respond to these data points is helpful.

- This is largely determined by the intuition of data issues.

Step 5: Use quantifiable metrics and general market strength to guide exits.

- There is no specific or repeatable exit strategy.

- The timing of exits varies for each meta-game; generally, intuition is key.

- Looking at data, market cap, relative trading volume, etc., is helpful—but ultimately, it is a discretionary choice.

Examples of Meta-games

Let’s look at some current and past examples of meta-games, along with the relevant logic and data. In this section, we will examine a self-reinforcing meta-game (ETH Killer trade), a self-defeating meta-game (Facebook rebranding to META), and a currently ongoing meta-game (BTC ETF liquidity).

Example 1: ETH Killer Meta-game

I assume this is a meta-game that most readers are very familiar with; it was one of the trades of the 2021 bull market. Below is a table outlining the basic parameters of the meta-game.

If the table is unclear, I will take a moment to explain this meta-game in detail. Let’s recall the bull market of 2021. Retail investors came here to gamble, ETH fees were high, and scaling solutions were lacking, while Solana and Avalanche positioned themselves as solutions to the problem (i.e., faster and cheaper transactions)—this is the fundamental mechanism.

The fundamental mechanism is self-reinforcing (reflexive); as long as we are in a bull market, ETH fees will remain high, thus the reasons to go long on ETH will persist throughout the bull market. As SOL and AVAX outperformed ETH, trading became clearer, and more participants engaged in trading. The nature of the fundamental mechanism supported an upward reflexive loop.

Given the persistence of the meta-game, it spawned sub-meta-games, which are derivative games of the main game. Specifically, the boom of SOL and AVAX DeFi and the emergence of FOAN trading. Market participants positioned Phantom, Harmony, Cosmos, and Near as new Alt L1 trades. Mechanically, those who felt they missed the main game found sub-games that intersected with the main game to participate in.

Generally, sub-meta-games yield smaller returns and do not last as long as the main game.

- Major → Main meta-game; Minor → Sub-meta-game

- Start, End, Duration → Time parameters

- Mechanism → Description of the fundamental mechanism

- Returns vs. Index → Performance metrics relative to a major or fundamental mechanism theme

- Absolute Returns → Performance metrics in absolute terms

The parameters of the game are largely subjective; it is objectively clear that X outperforms Y, but when to start and end is subjective. The same subjective logic can be applied to the choice of index; how do we define outperformance? The function of the table is merely to approach some form of objective truth.

Below are two charts—SOL vs. ETH and AVAX vs. ETH. They show the relative trading volume and relative price performance of SOL and AVAX against ETH, with data sourced from the Binance Futures API. The idea is simple: use relative trading volume as a proxy for relative interest and see how this matches with relative price performance.

Notably, in the second half of 2021, finding long-term excess returns in this meta-game was significant. I assume this was because the price drop in the summer of 2021 paused all games, while the narrative attracted more participants. When the market rebounded, the direction of capital allocation became clear. This may be motivated reasoning, but I believe it is somewhat accurate.

To think about exit strategies, we need to revisit the assumptions about the fundamental mechanism. This meta-game is a solution to a persistent problem (high ETH fees), a problem based on the bull market. Therefore, the most basic exit strategy is to sell when we believe we are nearing the end of the bull market.

Example 2: Facebook Rebranding to Meta

On October 28, 2021, Facebook rebranded to META, triggering a speculative frenzy around crypto projects related to the metaverse, which is a rather obvious fundamental mechanism. The difference between this fundamental mechanism and the previous one lies in its duration. Example 1 is self-reinforcing, while Example 2 is self-defeating; by this, I mean the catalyst in Example 2 is a one-time event. This slightly changes the rules of the game, let me explain.

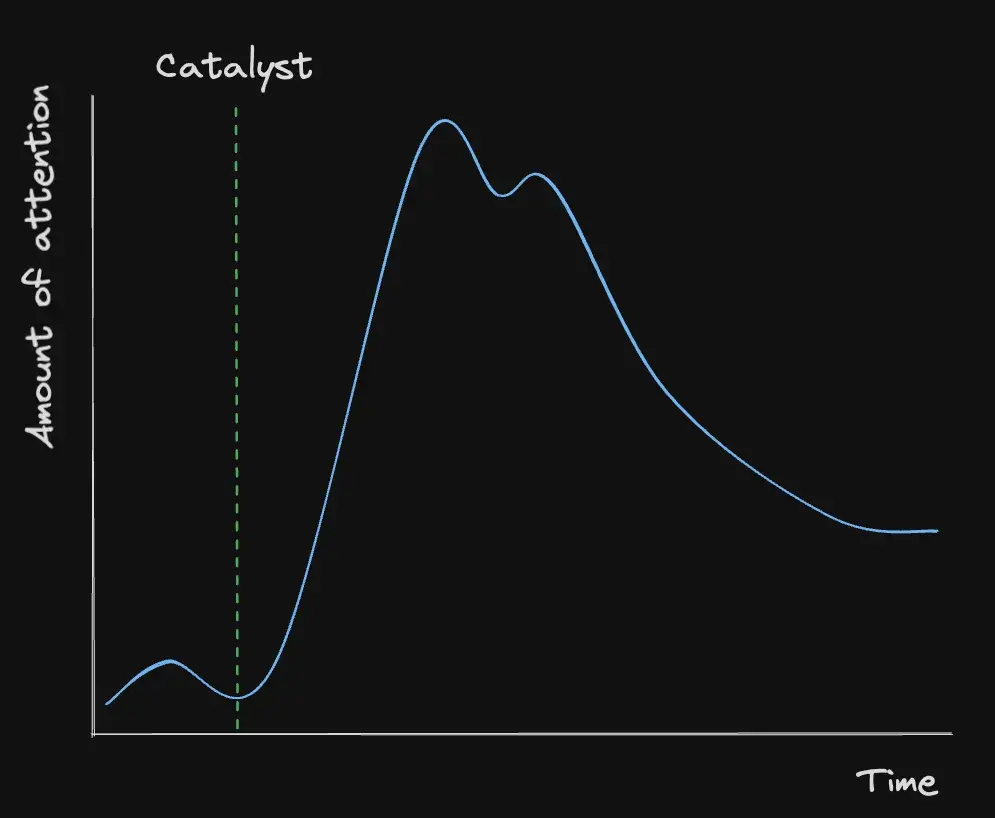

Look at the chart below—it shows the changes in attention over time. If we assume each project has some equilibrium share of the attention economy, we have a baseline. After the one-time catalyst, we see a massive re-rating in the attention economy share of metaverse tokens. This drove anomalous price fluctuations, attracting more attention. However, as the catalyst gradually faded, the meta-game began to rapidly disintegrate. This can also be understood from a vulnerability perspective; over time, the coordination point becomes more fragile in the face of external forces (i.e., the price movements of major currencies)—to a large extent, Bitcoin’s 9% drop on November 26 marked the end of this frenzy. Over time, the ability of a one-time catalyst to serve as a coordination point is diminishing—this is reflected in the subsequent decline in attention.

Before the rebranding, Axie Infinity had already undergone a semi-closed development, and the concept of the metaverse was gaining traction in Silicon Valley. All the elements were in place, and the META rebranding was just the spark that ignited the fire. The main beneficiaries of the meta-game were Decentraland ($MANA) and Sandbox ($SAND)—they were immediately repriced.

Again, to consider exit strategies, we need to revisit the assumptions about the fundamental mechanism. That is, the fundamental mechanism of a one-time catalyst is self-defeating. Therefore, one should actively seek ways to exit trades. If we look at the chart below, we can see it reflects the above-structured example, where relative trading volume can be used as a proxy for the attention economy share. Additionally, understanding market structure is also important; the trading volume of $SAND and $MANA cannot sustainably be three times that of $BTC, which violates logical principles.

Example 3: BTC ETF Meta-game

Note that this section was originally written at the end of March, and updates on this meta-game can be found at the end of this section.

This is an example of a currently ongoing meta-game; most cryptocurrency market participants are engaging in this trade. Its fundamental mechanism is bullish ETF inflows, for the following reasons:

- We are approaching the halving, and the number of coins flowing into ETF products is several times the new supply. This makes the narrative of limited supply + tokens more attractive.

- The approval of ETF products legitimizes crypto assets as an asset class and provides a channel for a whole new base of investors to purchase BTC.

Similar to the ETH Killer meta-game (Example 1), this meta-game is self-reinforcing. ETF products trade seven days a week, so BTC’s price loosely trades as the beta of these ETF flows. Given the fundamental mechanism, we can make some assumptions about ETF flows and prices:

- ETF inflows are favorable for BTC prices.

- ETF outflows are unfavorable for BTC prices.

As a basic model, this is a fairly straightforward game. However, as with all things in life, the devil is in the details. Given that GBTC was originally a closed-end fund, the vast majority of outflows come from GBTC—expected to slow down after entering the second half of the year. Under other conditions, the outflows from GBTC will decrease, thus net inflows should be boosted—bullish.

Current Thoughts on this Meta-game:

I see this as a reflection on my original BTC ETF meta-game thesis. Since I initially wrote this section, a lot has happened, especially the halving has occurred, and ETF flows have decreased and occasionally turned negative. I believe this meta-game is still ongoing, but the reflexivity is operating in the opposite direction; that is, ETF inflows have turned into outflows, and prices have responded. The relationship between ETF flows and BTC price performance seems quite clear in both directions.

It is worth noting that ETF flows and prices are not mechanically correlated; like all meta-games, this is to some extent a shared illusion. As ETF flows find equilibrium, it is likely that daily flows will be zero, and I expect this meta-game to dissipate. Notably, the level of attention given to ETF flows is related to their scale; days of large inflows and outflows will make headlines, while ordinary days will generally go unnoticed. As this meta-game moves further into the rearview mirror, I expect only outlier days to attract attention.

In the near future, we may see an ETH ETF meta-game similar to the BTC ETF meta-game. Under other conditions, I expect:

- As the likelihood of ETF approval becomes clearer, ETH trading will increase; we can use the approval probabilities and statements from Bloomberg ETF brethren as a representation of this.

- The risk decreases after ETF approval, as the market analyzes the inflows and outflows of ETF and ETHE (Grayscale product).

- If inflows are comparable to BTC (which I doubt), this is bullish. Insufficient inflows are bearish and may be bullish for Solana.

Assuming the fees for ETH ETF products will be similar to those of BTC ETF, I am not entirely sure what the outcome of higher fees will be; the principle of Occam's Razor suggests this will be bearish. BTC price action and BTC ETF inflows lay the groundwork for good performance of ETH ETF, which is somewhat of a foregone conclusion; when we start trading the ETH ETF meta-game, I believe the market will price it based on BTC ETF performance. If there are large outflows from BTC ETFs between and after ETH ETF approval, I believe the ETH ETF will falter. Other interesting points to watch include whether ETH in the ETF will be staked and whether ETF holders will receive that yield, which seems unlikely due to "well, securities law, Howey test, etc.," but if so, it would be a surprise.

Some Overall Thoughts

Market behavior has certain patterns or logic, and assets that violate these patterns will quickly revert to the mean. The logic/rules are largely dynamic, but the speed at which the Overton window (i.e., policy window) changes is slower than most people think. Additionally, there are some laws that are as inviolable as gravity.

The meta-game is not just an investment framework; it is more like a mental model, and it is difficult to build a solid structure around the development, evolution, and behavior of these games because they are all different. Identifying these games and theorizing how they will evolve requires a certain degree of intuition, which is honed through market timing and fundamental principles thinking.

I have detailed a self-defeating, a self-reinforcing, and a currently ongoing meta-game; other examples include:

- Meme, 2021 (self-defeating)

- ETH Merge, 2022 (self-defeating)

- Crypto x AI, 2024 (self-reinforcing)

- SOL killers, 2024 (ambiguous)

- Meme, 2024 (self-defeating)

- RWA, 2024 (self-reinforcing)

- New tokens, 2024 (volatile)

- BTC ETF beta, 2024 (self-reinforcing)

There are many types of meta-games, each distinct. However, the basic procedures are the same: identify the meta-game, understand its fundamental mechanisms, infer the duration of the meta-game, and then plan how to best extract value.