Analysis: Why is there a significant mismatch between the initial scale and trading volume of Hong Kong's crypto ETFs?

From a more macro and long-term perspective, Hong Kong's approval of Bitcoin and Ethereum spot ETFs is an important development in the global crypto market. This policy will have a long-term impact on the financial landscape of the Chinese community and is also a significant step towards the further legalization of cryptocurrencies in the global financial system.

From a more macro and long-term perspective, Hong Kong's approval of Bitcoin and Ethereum spot ETFs is an important development in the global crypto market. This policy will have a long-term impact on the financial landscape of the Chinese community and is also a significant step towards the further legalization of cryptocurrencies in the global financial system.Author: Tom Analysis, SoSo Value Research Fellow

The Hong Kong Securities and Futures Commission has officially announced the approved list of virtual asset spot ETFs, which includes the Bitcoin spot ETFs and Ethereum spot ETFs under Huaxia (Hong Kong), Harvest International, and Bosera International. These 6 spot ETF products will open for subscription from April 25 to 26, and will be listed on the Hong Kong Stock Exchange on April 30.

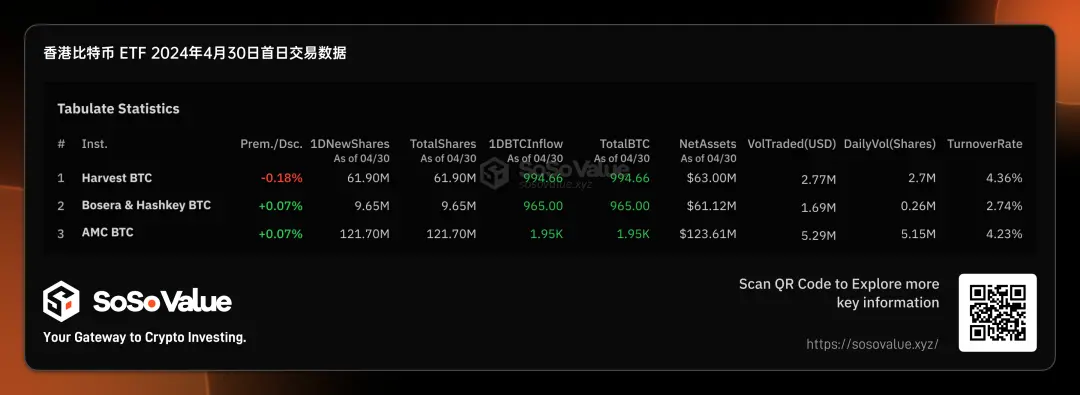

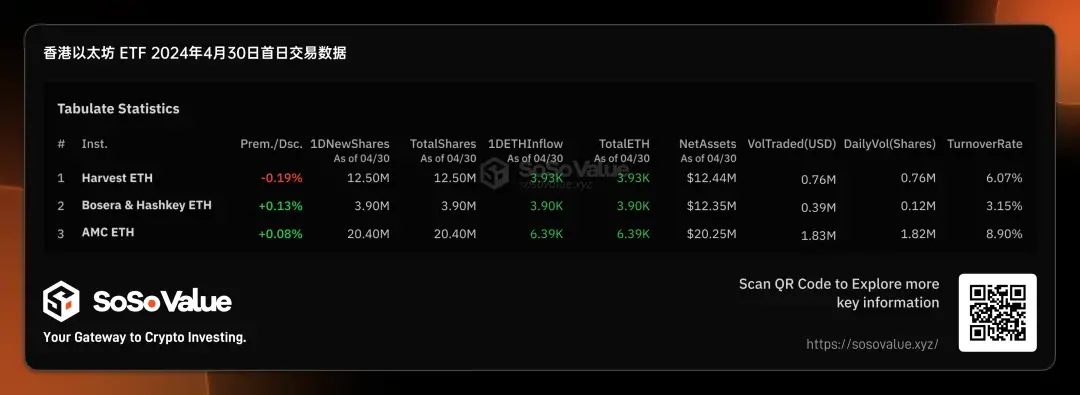

Through the subscription process, the 6 Hong Kong spot ETFs have achieved a good initial scale. According to SoSo Value data, the total net value of 3 Bitcoin ETFs is $248 million, and the total net value of 3 Ethereum ETFs is $45 million, totaling nearly $300 million; whereas the total net value of the US Bitcoin spot ETF products, excluding the Grayscale (GBTC) that converted from a trust to an ETF, was only $130 million on the first day. However, in terms of trading volume on the first day, Hong Kong's crypto ETFs were far smaller than their US counterparts. According to SoSo Value data, the trading volume of the 6 Hong Kong crypto ETFs on the first day, April 30, was only $12.7 million, significantly lower than the $4.66 billion trading volume on the first day of US ETFs.

We have observed a significant mismatch between the initial scale and the first-day trading volume of Hong Kong crypto ETFs. How large can Hong Kong's crypto spot ETFs grow, what impact can they have on the crypto market, and how should investors seize related investment opportunities? The author will analyze this through the supply and demand relationship of Hong Kong ETFs.

Figure 1: Overview of Hong Kong Crypto Spot ETF Data (Data Source: SoSo Value)

Demand Side: Mainland Chinese investors are not allowed to purchase, limiting incremental funds and resulting in low trading volume

The Hong Kong crypto ETF still has strict restrictions on investor qualifications, and mainland investors cannot participate in trading. Taking Futu Securities as an example, they require that the account holder be a non-mainland & non-US resident to trade. The anticipated mainland funds through the southbound stock connect to trade are currently not allowed, and it is expected to be difficult to open up for a considerable period.

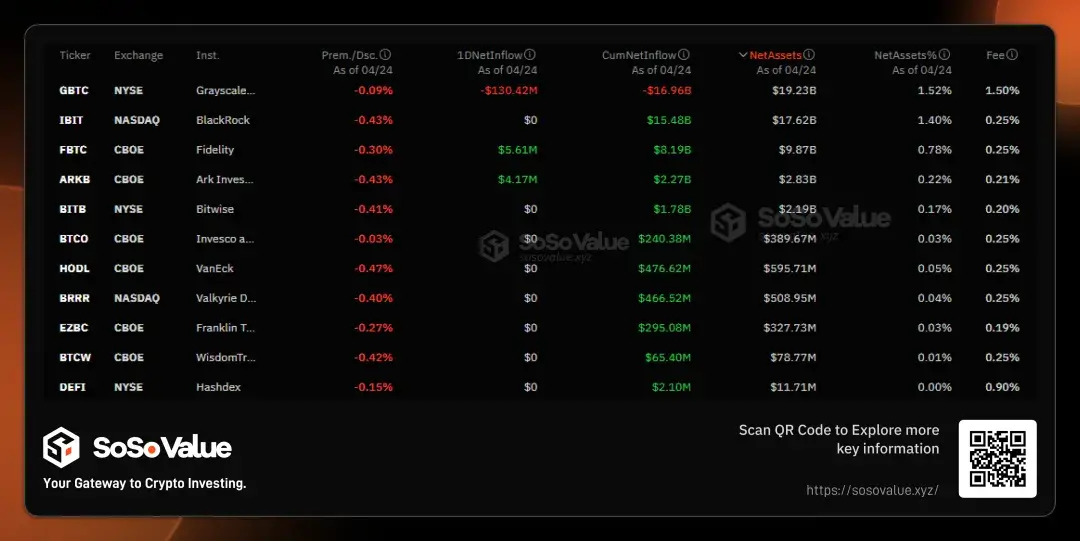

In terms of fees, Hong Kong's crypto ETFs are not advantageous compared to US ETFs, making them less attractive for institutions looking to hold long-term. According to SoSo Value data, among the 11 US Bitcoin spot ETFs, except for Grayscale and Hashdex, the largest ones like IBIT and CBOE have management fee rates around 0.25%, while the 3 Bitcoin ETFs in Hong Kong have relatively higher comprehensive fee rates: Huaxia at 1.99%, Harvest at 1.00%, and the lowest, Bosera, at 0.85%. Even with short-term management fee reductions, there is still no fee rate advantage. Given the fee differences, for institutional investors optimistic about the crypto market and looking to hold long-term, US Bitcoin ETFs have lower holding costs.

Looking ahead, the sources of demand may mainly come from two areas: 1) Hong Kong retail investors. For retail investors with a Hong Kong ID, the threshold for purchasing Hong Kong crypto ETFs is lower. For example, purchasing US Bitcoin spot ETFs requires professional investor qualifications (PI), which necessitates proof of an investment portfolio of HKD 8 million or total assets of HKD 40 million. The Hong Kong Bitcoin spot ETFs allow retail trading, and the trading hours are more aligned with Asian schedules, which is an important increment. 2) Traditional investors interested in Ethereum. The Hong Kong Ethereum spot ETF is the first global launch, so investors who have substantial difficulties holding coins but are optimistic about Ethereum's prospects may bring incremental interest to the Ethereum ETF.

Figure 2: US Bitcoin Spot ETF Fee Rates (Data Source: SoSo Value)

Figure 3: Hong Kong Crypto Spot ETF Fee Rates (Data Source: SoSo Value)

Supply Side: In-kind redemption method increases ETF share supply, enhancing initial scale

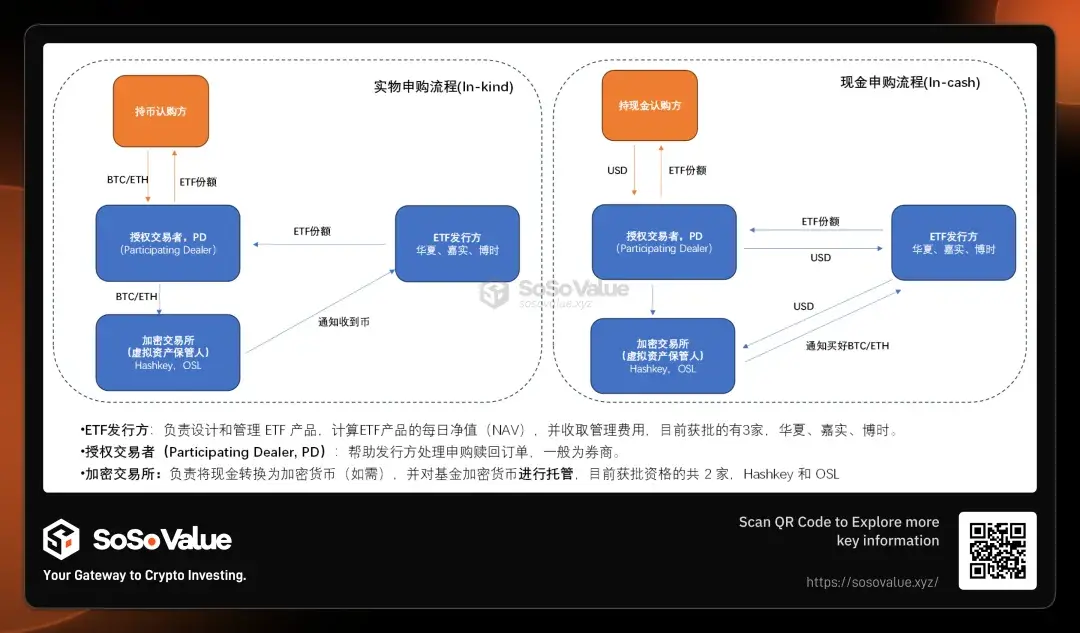

The biggest difference between Hong Kong crypto spot ETFs and US Bitcoin spot ETFs is that, in addition to cash redemption (in-cash), there is an additional in-kind redemption method. This directly determines that, in terms of ETF share levels, Hong Kong crypto ETFs may have more suppliers.

In-kind redemption means that when investors subscribe (create) or redeem ETF shares, they can use cryptocurrencies (Bitcoin or Ethereum) for exchange instead of cash. During subscription, investors provide a certain amount of cryptocurrency to the ETF in exchange for ETF shares; during redemption, investors return ETF shares in exchange for the corresponding cryptocurrency.

Referring to Figure 2's comparison of the Hong Kong cryptocurrency subscription process, we can see two major differences brought by in-kind subscriptions compared to cash subscriptions:

1) Holders can directly use coins for subscription: For some large holders, such as miners, it is easy to convert their coins into ETF shares, and the ETF shares can subsequently support cash redemption or be sold directly on the Hong Kong Stock Exchange for cash, providing very flexible handling options.

2) For the crypto market, in-kind subscriptions do not bring incremental funds into the market; they merely transfer cryptocurrencies between different accounts. In contrast, cash subscriptions would bring actual buying pressure to on-chain crypto assets.

Therefore, the subscribers of Hong Kong crypto ETF shares include both traditional cash subscribers and large coin holders. Although the specific shares of in-kind and cash subscriptions have not yet been disclosed by various firms, according to OSL's public communications, the proportion of the first batch of in-kind subscriptions may exceed 50%, which explains why the initial fundraising scale of Hong Kong crypto ETFs can reach nearly $300 million, thanks to in-kind subscriptions. However, on another level, these in-kind subscription ETF shares may turn into sell orders in subsequent secondary market trading.

Figure 4: Comparison of Hong Kong Crypto Spot ETF In-kind vs Cash Subscription Processes

Comprehensive Supply and Demand: Focus on Premium/Discount Rates to Seize Investment Opportunities

Based on the comprehensive analysis of supply and demand mentioned above, unlike US Bitcoin spot ETFs, we can track the daily net inflow of funds into the ETF (Total Net Inflow, specific reference can be made to https://sosovalue.xyz/assets/us-btc-spot) to intuitively assess the impact of the Bitcoin ETF's incremental funds on crypto asset prices. The supply and demand dynamics of Hong Kong crypto spot ETFs are more complex, and the data published by various fund companies cannot clearly distinguish between in-kind and cash redemption volumes. In this context, we believe that the premium/discount rate in the public market (Hong Kong Stock Exchange trading) may be a better observation indicator.

As analyzed above, in on-exchange trading on the Hong Kong Stock Exchange, the premium/discount is the best reflection of the forces of supply and demand. If the ETF trades at a discount, it indicates that the selling pressure is stronger, leading to oversupply, and market makers are incentivized to purchase ETF shares at a discount on the Hong Kong Stock Exchange and then redeem shares from the ETF issuer off-exchange to profit from the price difference, resulting in a decrease in the overall net asset value of the ETF and capital outflow, which is negative for the overall crypto market. The entire process can be summarized simply as: ETF discount --> stronger selling pressure --> potential redemption --> negative impact on the crypto market. Conversely, if the ETF trades at a premium --> stronger buying pressure --> potential subscription --> positive impact on the crypto market.

According to SoSo Value data, as of the market close on April 30, except for Harvest Bitcoin Spot ETF (3439.HK) and Harvest Ethereum Spot ETF (3179.HK), which generated negative premiums of -0.18% and -0.19% respectively, all other products had positive premiums, with a maximum positive premium of 0.33% during trading, indicating restrained selling pressure and relatively strong buying pressure on the first day. Considering the influence of market makers on the first day of ETF listing, this premium/discount data can be continuously monitored. If it can maintain a positive premium, it is expected to continuously attract investor subscriptions, especially from coin-holding investors, which would push the scale of Hong Kong crypto spot ETFs beyond the estimated value of $500 million; whereas if it turns to a negative premium, caution should be exercised regarding arbitrage trades redeeming ETF shares, leading the ETF issuer to sell cryptocurrencies, which could drive the crypto market downward.

Figure 5: Supply and Demand Impact Mechanism of Hong Kong Crypto Spot ETF (Data Source: SoSo Value)

Hong Kong Crypto ETFs also provide an important value for investors: increasing a pathway for the conversion and circulation of crypto assets with tradable financial assets

The rapid approval of Hong Kong's crypto spot ETFs, while potentially having less short-term impact on the crypto market than US spot ETFs, provides a pathway for crypto assets to be converted into traditional financial assets through the in-kind redemption mechanism of Hong Kong crypto ETFs in the medium to long term. By using in-kind subscriptions, cryptocurrencies can be converted into ETF shares, and since ETF shares have fair value and liquidity priced by traditional financial markets, holding crypto asset ETFs can serve as proof of assets in traditional financial markets, allowing for various leveraged operations, such as borrowing against them, constructing structured products, etc. This further opens the pathway between crypto assets and traditional finance, allowing the value of crypto assets to be more fully reflected and realized.

From a more macro and long-term perspective, the approval of Bitcoin and Ethereum spot ETFs in Hong Kong is an important development for the global crypto market. This policy will have a long-term impact on the financial landscape in Chinese-speaking regions and is an important step towards the further legalization of cryptocurrencies within the global financial system.