On the eve of the upheaval, a deep penetration operation in the stablecoin market initiated by Ethena

Combining yield and scalability, USDe may become a high-yield stablecoin with limited short-term scale that follows market trends in the long term.

Combining yield and scalability, USDe may become a high-yield stablecoin with limited short-term scale that follows market trends in the long term.Author: Chen Mo cmDeFi

Source: PANews

Core viewpoint: A crypto-native synthetic dollar stablecoin, a structured passive income product that balances between centralized and decentralized structures, which holds assets on-chain and maintains stability through Delta neutrality while earning yields.

- The background of its birth is that centralized stablecoins represented by USDT & USDC dominate the stablecoin market, while the collateral of decentralized stablecoin DAI gradually tends to be centralized, and algorithmic stablecoins LUNA & UST collapsed after massive growth to the top five stablecoins by market cap. The birth of Ethena strikes a compromise and balance between the DeFi and CeFi markets.

- The OES service provided by institutions holds assets on-chain and maps the amounts to centralized exchanges to provide margin, retaining the characteristics of DeFi by isolating on-chain funds from exchanges to reduce risks such as fund misappropriation and insolvency. On the other hand, it retains the characteristics of CeFi to obtain sufficient liquidity.

- The underlying yield consists of staking rewards from Ethereum liquidity derivatives and funding rate income obtained by opening hedging positions on exchanges. It is also referred to as a structured yield product for universal funding rate arbitrage.

- Currently incentivizing liquidity through a points system.

Its ecological assets include:

- USDe - A stablecoin that can be minted by depositing stETH (more assets and derivatives may be added in the future).

- s USDe - A voucher token obtained after staking USDe.

- ENA - Protocol token/governance token, currently flowing into the market through point redemption each period, locking ENA can yield greater point acceleration.

Research Report

1/6 • How to Mint and Redeem USDe Stablecoin

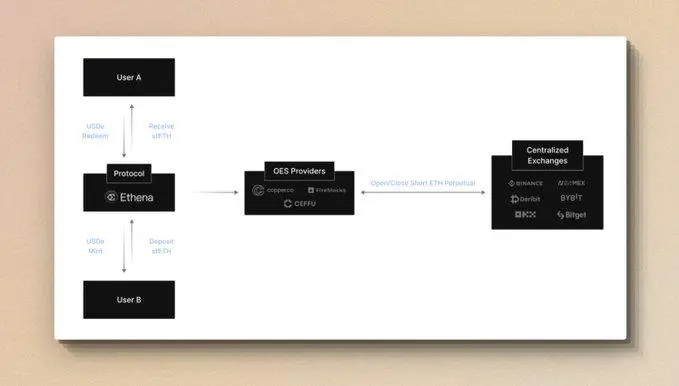

By depositing stETH into the Ethena protocol, USDe can be minted at a 1:1 ratio to the dollar. The deposited stETH is sent to a third-party custodian, and the balance is mapped to the exchange through "Off-exchange Settlement." Ethena then opens a short ETH perpetual position on CEX to ensure that the collateral value remains Delta neutral or unchanged in dollar terms.

- Ordinary users can obtain USDe from permissionless external liquidity pools.

- Recognized institutional parties that have passed KYC/KYB screening and are whitelisted can mint and redeem USDe directly through the Ethena contract at any time.

- Assets are always retained in a transparent on-chain custody address, thus not relying on traditional banking infrastructure and not being affected by fund misappropriation or bankruptcy of exchanges.

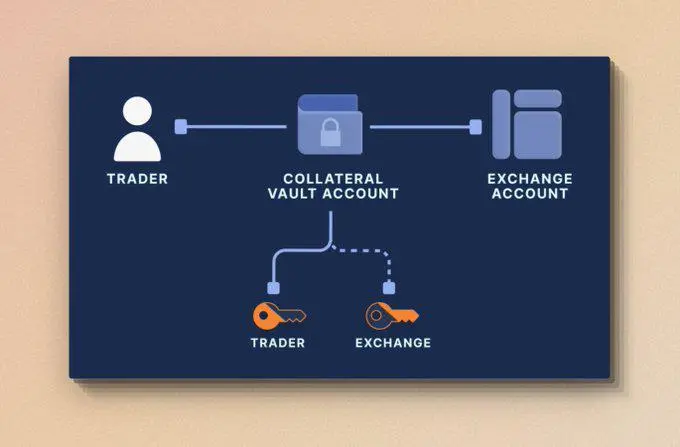

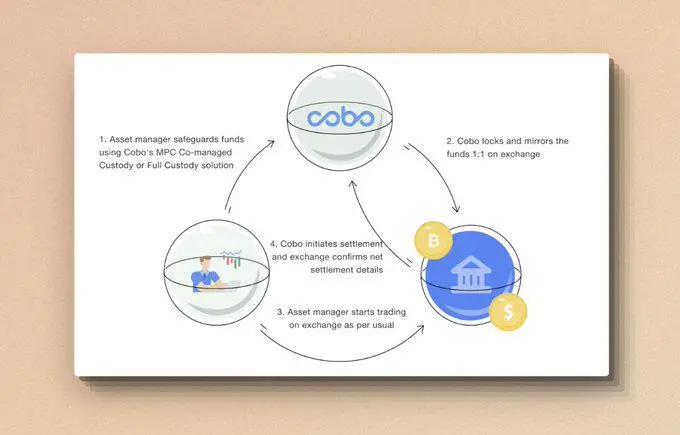

2/6 • OES - The Fund Custody Method of ceDeFi

OES (Off-exchange Settlement) is a method of off-exchange fund custody settlement that balances on-chain transparency and traceability with the use of funds in centralized exchanges.

- Utilizing MPC technology to construct custody addresses, user assets are stored on-chain to maintain transparency and decentralization, jointly managed by users and custodians, eliminating counterparty risk from exchanges and significantly reducing potential security issues and fund misuse. This maximizes the assurance that assets are held by the users themselves.

- OES providers typically collaborate with exchanges, allowing traders to map asset balances from their jointly controlled wallets to exchanges to complete related transactions and financial services. For example, this allows Ethena to hold funds off-exchange while still using these funds on exchanges to provide collateral for Delta hedging derivative positions.

MPC wallets are currently seen as the perfect choice for a consortium to control a single crypto asset pool. The MPC model distributes individual keys as separate units to respective wallet users, jointly managing the custody address.

3/6 • Profit Mechanism

- Ethereum staking rewards from liquidity derivatives.

- Funding rate income obtained by opening short positions on exchanges, basis spread income.

"Funding rate" is the payment made periodically to traders holding long or short positions based on the difference between spot prices and perpetual contract markets. Therefore, traders will pay or receive funding based on the demand for holding long or short positions. When the funding rate is positive, longs pay shorts; when the funding rate is negative, shorts pay longs. This mechanism ensures that the prices of the two markets do not deviate significantly over time.

"Basis" refers to the price discrepancy that occurs because spot and futures are traded separately. The deviation in their prices is called the basis spread, and as the futures contract approaches expiration, the futures price typically converges towards the corresponding spot price. At expiration, traders holding long contracts need to purchase the underlying asset at the predetermined contract price. Therefore, as the futures expiration date approaches, the basis should converge towards zero.

Ethena uses mapped funding balances on exchanges to devise different strategies for arbitrage, providing diversified yields for on-chain USEe holders.

4/6 • Yield and Sustainability

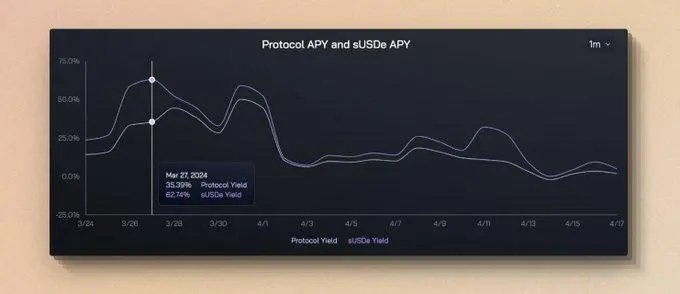

In terms of yield, the protocol has achieved an annualized yield of up to 35% in the past month, with the yield allocated to s USDe reaching 62%. The difference here is due to the fact that USDe is not entirely converted to s USDe through staking, and it is practically impossible to achieve a 100% staking rate. If only 50% of USDe is staked and converted to s USDe, then this portion of s USDe captures 100% of the total yield with only 50% of the staked amount. Because the application scenarios of USDe will enter DeFi protocols like Curve and Pendle, this not only meets the needs of different application scenarios but also potentially enhances the yield of s USDe.

However, as the market cools down and the long funds in exchanges decrease, the funding rate income will also decline. Therefore, after entering April, there has been a noticeable downward trend in overall yields, with the Protocol Yield currently reduced to 2% and sUSDe Yield down to 4%.

Thus, in terms of yield, USDe is relatively dependent on the conditions of the futures market in centralized exchanges and will be constrained by the scale of the futures market. When the issuance of USDe exceeds the corresponding capacity of the futures market, it will no longer meet the conditions for the continued expansion of USDe.

5/6 • Scalability

The scalability of stablecoins is crucial, referring to the conditions and possibilities for increasing the supply of stablecoins.

Stablecoin protocols like Maker are often limited in scalability due to over-collateralization requirements, needing more than $1 in collateral to mint $1. Ethena's uniqueness lies in the fact that its main constraint on scalability will be the Open Interest of the ETH perpetual market.

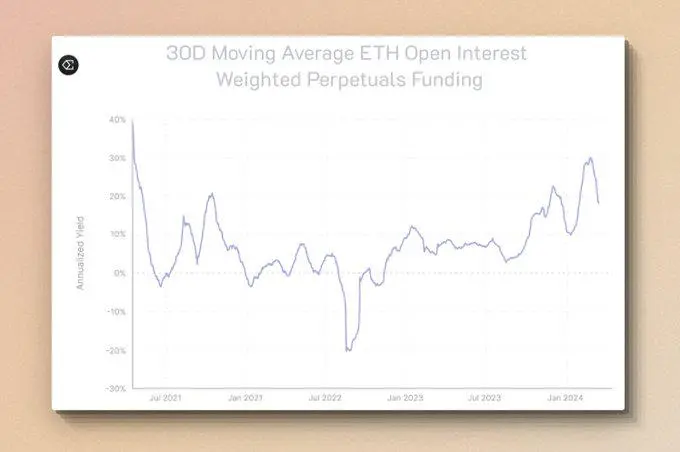

Open Interest refers to the total number of open contracts in exchanges. Here, it specifically refers to the total value of open positions in ETH perpetual contracts on centralized exchanges. Currently, this figure is about $12 billion (as of April 2024). This number reflects the current holding levels of market participants in ETH.

Comparing Ethena's starting phase at the beginning of 2024, ETH Open Interest has grown from $8 billion to $12 billion, and recently Ethena has also supported the BTC market, where BTC Open Interest is around $30 billion. The issuance of USDe is approximately $2.3 billion, which of course is influenced by various factors, such as the natural growth of market users, and the price increases of ETH and BTC. However, it should be noted that the scalability of USDe is closely related to the scale of the perpetual market.

This is also why Ethena collaborates with centralized exchanges. In 2023, the stablecoin project UXD Protocol on the Solana chain adopted a similar Delta-neutral approach to issue stablecoins but chose to execute hedging strategies on decentralized exchanges. However, due to limited on-chain liquidity, when the issuance of stablecoins reached a certain scale, it meant needing to conduct larger short operations, ultimately leading to negative funding rates and incurring substantial additional costs. Additionally, UXD used the leverage protocol Mango on the Solana chain for shorting, which was later attacked on-chain, leading to project failure due to multiple reasons.

So, can the market cap of USDe reach that of USDT? DAI? What level?

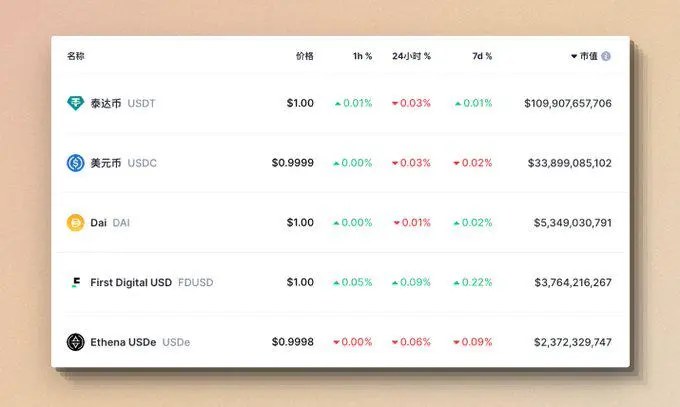

Currently, the market cap of USDe is around $2.3 billion, ranking 5th in the overall stablecoin market cap, already surpassing most decentralized stablecoins, but still $3 billion short of DAI.

Currently, ETH Open Interest is close to historical peak levels, and BTC Open Interest has reached historical highs, so the expansion of USDe's market cap must increase corresponding short positions in the existing market, which poses certain challenges for the current growth of USDe. As the main source of income for USDe, the funding rate is the mechanism used in perpetual contracts to adjust prices to align with the spot market, typically achieved through periodic payments from longs to shorts or from shorts to longs. When USDe is over-issued and the number of shorts in the market increases, it may gradually push the funding rate down, even turning negative. If the funding rate decreases or turns negative, it may reduce the income Ethena can obtain from the market.

In the absence of changes in market sentiment, this is a typical market supply-demand balance issue that needs to find a balance between expansion and yield. If market sentiment shifts towards a bull market, with rising prices and bullish sentiment, the theoretical capacity for issuing USDe will increase. Conversely, if market sentiment shifts towards a bear market, with declining prices and reduced bullish sentiment, the theoretical capacity for issuing USDe will decrease.

Combining yield and scalability, USDe may become a high-yield stablecoin with limited short-term scale, following market trends in the long term.

6/6 • Risk Analysis

Funding rate risk - When there are insufficient longs in the market, or when USDe is over-issued, there may be a situation of negative funding rate income, requiring Ethena to pay fees to longs as a short. Although Ethena concludes based on historical data that the market is positive most of the time. Additionally, Ethena uses LSTs (e.g., stETH) as collateral for USDe, which can earn an annualized yield of 3-5% in stETH to provide an additional margin of safety against negative funding rates. However, it is worth noting that similar protocols have previously attempted to expand the scale of synthetic dollar stablecoins but failed due to inverted yields.

Custody risk - Fund custody relies on OES and centralized institutions providing services. The bankruptcy of exchanges may lead to losses for unsettled profits, and the bankruptcy of OES institutions may cause delays in fund access. Although OES has adopted MPC and a streamlined approach to safeguard funds, there remains a theoretical possibility of funds being stolen.

Liquidity risk - If there is a need to quickly close positions or adjust positions at a specific moment, a large amount of funds may face liquidity issues, especially during market stress or panic. Ethena attempts to mitigate and address this issue by collaborating with centralized exchanges, such as through progressive liquidation, gradual position closure, or other facilitative policies to alleviate market shocks. This partnership may provide significant flexibility and advantages, but it also introduces centralized risks.

Asset anchoring risk - stETH is theoretically anchored 1:1 with ETH, but there have been instances of temporary decoupling in history, mainly before the Shanghai upgrade. In the future, there may still be unknown risks at the level of Ethereum's liquidity derivatives. Asset decoupling may also trigger liquidations on exchanges.

To address the series of risks mentioned above, Ethena has established an insurance fund, with funds sourced from the protocol's revenue distribution in each cycle, with a portion allocated to the insurance fund.