In-depth analysis of the reasons for Ethena's success and the risks of the death spiral

The reason for Ethena's success as a CeFi product lies in its provision of short liquidity for the perpetual contract market of centralized exchanges, but one must be cautious of the death spiral risk in the mechanism design.

The reason for Ethena's success as a CeFi product lies in its provision of short liquidity for the perpetual contract market of centralized exchanges, but one must be cautious of the death spiral risk in the mechanism design.In recent days, the market has been ignited by Ethena, a stablecoin protocol that can provide an annual yield of over 30%. Many articles have introduced the core mechanisms of Ethena, so I won't elaborate on that here. In simple terms, Ethena.fi tokenizes "Delta neutral" arbitrage trading of ETH by issuing stablecoins that represent the value of Delta neutral positions. Their stablecoin USDe also collects arbitrage profits - hence they claim this is a type of internet-native bond that provides internet-native yields. However, this scenario inevitably reminds us of the last crypto cycle's turning point from bull to bear, which was triggered by the algorithmic stablecoin UST issued by Terra. At that time, it quickly attracted deposits with a 20% annual yield subsidized for UST lenders through its ecosystem's native lending protocol, Anchor Protocol, and collapsed rapidly after facing a bank run. Learning from this lesson, the explosive popularity of USDe (the stablecoin issued by Ethena) has sparked widespread discussion in the crypto community, with the skepticism of DeFi opinion leader Andre Cronje drawing significant attention. Therefore, I hope to delve deeper into the reasons behind Ethena's explosive growth and the risks inherent in its mechanisms.

Reasons for Ethena's Success as a CeFi Product: The Savior of Centralized Exchange Perpetual Contract Markets

To discuss the reasons for Ethena's success, I believe the key lies in its potential to become the savior of the perpetual contract market for centralized cryptocurrency exchanges. First, let's analyze the current issues faced by the perpetual contract markets of mainstream centralized cryptocurrency exchanges, which is the lack of short positions. We know that the main functions of futures are speculation and hedging. Since most speculators are extremely bullish on the future price movements of cryptocurrencies during periods of optimistic market sentiment, this leads to a situation where the number of long positions significantly exceeds that of short positions in the futures market. This situation results in a problem: the funding rate for long positions in the perpetual contract market increases, raising the cost of going long and suppressing market vitality. We know that for centralized cryptocurrency exchanges, the perpetual contract market is the most active trading area, and its trading fees are one of the core sources of revenue. Therefore, finding short positions for the perpetual contract market during a bull market is crucial for exchanges to enhance their competitiveness and increase revenue.

Here, it may be necessary to supplement some basic knowledge about the principles of perpetual contracts and the role and collection method of funding rates. A perpetual contract is a special type of futures contract. We know that traditional futures contracts usually involve delivery, which involves the transfer of equivalent assets and the associated clearing and settlement, increasing the operational costs for exchanges. Additionally, for long-term traders, approaching the delivery date involves actions like rolling over positions, and the price fluctuations of the marked assets tend to be larger as the delivery date approaches, as the market liquidity of the old underlying asset gradually deteriorates, introducing many hidden trading costs. To reduce these costs, perpetual contracts were designed. Unlike traditional contracts, perpetual contracts do not have a delivery mechanism, hence there is no expiration date, allowing users to hold positions indefinitely. The key to this feature lies in how to ensure that the price of perpetual contracts is correlated with the price of the underlying asset. In futures contracts with delivery, the source of correlation is delivery itself, as the delivery mechanism transfers physical assets (or equivalent assets) according to the agreed price and quantity in the contract. Therefore, theoretically, the price of futures contracts will converge with the spot price at delivery. However, since perpetual contracts do not have a delivery mechanism, an additional design element is introduced to ensure correlation, which is the funding rate.

We know that prices are determined by supply and demand. When supply exceeds demand, prices rise, and this is also true in the perpetual contract market. When there are more long positions than short positions, the price of perpetual contracts will be higher than the spot price, and this price difference is usually referred to as the basis. When the basis becomes too large, a mechanism is needed to counteract this basis, which is the funding rate. In this design, when a positive basis occurs, meaning the contract price is higher than the spot price, it indicates that there are more long positions than short positions. At this point, longs need to pay fees to shorts, and the rate is proportional to the basis (not considering that the funding rate consists of a fixed rate and a premium). This means that the greater the deviation, the higher the cost for longs, which suppresses the motivation to go long and restores the market to a balanced state, and vice versa. With this design, perpetual contracts have a price correlation with the spot market.

Returning to the initial analysis, we know that in an extremely optimistic market, the funding rate for longs is very high, which suppresses the motivation to go long. This also suppresses market vitality and reduces the revenue for exchanges. Typically, to alleviate this situation, centralized exchanges need to introduce third-party market makers or become the counterparty in the market themselves (as can be seen in the disclosures following the FTX incident, this is a common phenomenon), allowing the funding rate to return to a competitive state. However, this also introduces additional risks and costs. To hedge against these costs, market makers need to hedge the short risks in the perpetual contract market by going long in the spot market. This is essentially the nature of Ethena's mechanism, but due to the large market scale at this time, it exceeds the capital limits of a single market maker, or in other words, it brings high single-point risks to market makers or exchanges. To share this risk, or to raise more funds to stabilize the basis and make their perpetual contract market's funding rate more competitive, centralized exchanges need more interesting solutions to raise capital from the market. At this moment, the arrival of Ethena is timely!

We know that the core of Ethena lies in accepting cryptocurrencies as collateral, such as BTC, ETH, stETH, etc., and shorting their corresponding perpetual contracts in centralized exchanges to achieve Delta risk neutrality, earning the native yields of the collateral and the funding rates from the perpetual contract market. The stablecoin USDe they issue is essentially similar to a warrant share of an open market maker fund that engages in Delta risk-neutral cryptocurrency arbitrage. **Holding a *share* is equivalent to obtaining the dividend rights of that fund. Users can easily access this high-threshold track to earn considerable yields through this product, while centralized exchanges gain broader short liquidity, reduce funding rates, and enhance their competitiveness**.

Two phenomena can support this view. First, this mechanism is not unique to Ethena; the UXD in the Solana ecosystem actually adopted this mechanism to issue its stablecoin assets. However, it failed to gain the expected influence because it collapsed before establishing liquidity with centralized exchanges. Various reasons, apart from the reversal of the entire crypto cycle leading to a low interest rate environment for perpetual contracts, include the significant impact of the FTX collapse. Second, upon closely observing Ethena's investors, a significant proportion comes from centralized exchanges, which also proves their interest in this mechanism. However, amidst the excitement, we must not overlook the risks involved!

Negative Funding Rates Are Just One Possible Trigger for a Bank Run; Basis Is the Key to the Death Spiral

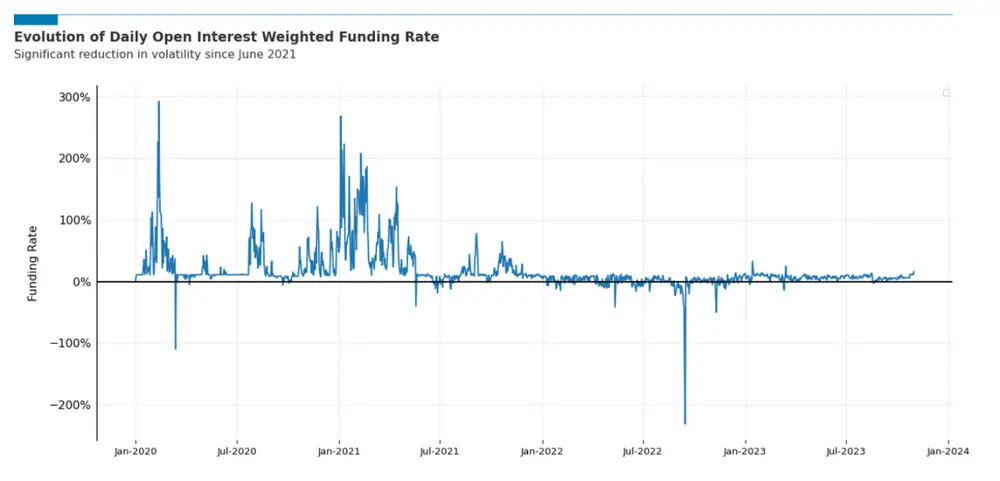

We know that for stablecoin protocols, the tolerance for bank runs is crucial. In most discussions about the risks of Ethena, we have already understood the damage that the negative interest rate environment in the cryptocurrency futures market poses to the value of USDe's collateral. However, this damage is usually temporary. Cross-cycle backtesting results indicate that, under normal circumstances, negative interest rate environments do not last long and are not easy to occur, as has been thoroughly demonstrated in the economic model audit report from Chaos Labs publicly released by Ethena. Moreover, the damage caused by negative funding rates to collateral value is gradual, as the collection of contract fees typically occurs every 8 hours. According to backtesting results, even under the most extreme -100% rate estimation, the maximum conceptual loss within any 8-hour period is 0.091%. In the past three years, negative funding rate phenomena have occurred only three times, with an average duration of 3-5 weeks. The negative rate recovery period in April 2022 lasted about three weeks, with an average level of -3.3%. In June 2022, it also lasted about three weeks, with an average level of -4.8%. If we include the extreme funding rates from September 11 to 15, this period lasted five weeks, averaging -17.9%. Considering that during other times the rates were positive, this means Ethena has ample opportunity to "store water" during rainy days, accumulating a certain Reserve Fund to cope with negative rate situations, thereby reducing the erosion of collateral value by negative rates and preventing collateral ratios from falling below 100%. Therefore, I believe the risk of negative rates is not as significant as imagined, or that through certain mechanisms, this risk can be greatly alleviated. It can be said that this is just one possible trigger for a bank run. Of course, if we question the statistical significance, that is not the scope of this discussion.

However, this does not mean that Ethena will have a smooth journey. After reading some official or third-party analysis results, I believe we have overlooked a fatal factor, which is the basis. This is precisely the key vulnerability for Ethena when facing bank run phenomena, or the key to the death spiral. Looking back at two very typical bank run phenomena regarding stablecoins in the cryptocurrency market, the collapse of UST and the bank run decoupling of USDC in March 2023 due to the bankruptcy of Silicon Valley Bank, we can see that in the current development of internet technology, the spread of panic is extremely rapid. The speed of bank runs triggered by this panic is very fast. Usually, when panic occurs, a large number of redemptions will be faced within just a few hours or days. This poses a challenge to the tolerance of stablecoin mechanisms for bank runs. Therefore, most stablecoin protocols choose to allocate highly liquid assets as collateral, not solely pursuing high yields, such as short-term U.S. Treasury bonds, so that in the event of a bank run, the protocol can sell collateral to obtain liquidity to cope. However, considering that Ethena's collateral types consist of cryptocurrencies with price volatility risks and their futures contracts, this poses a significant challenge to the liquidity of both markets. When Ethena's issuance reaches a certain scale, in the event of large-scale redemptions, whether the market has sufficient liquidity to unwind the arbitrage combination to obtain liquidity to meet redemption demands is the main risk it faces.

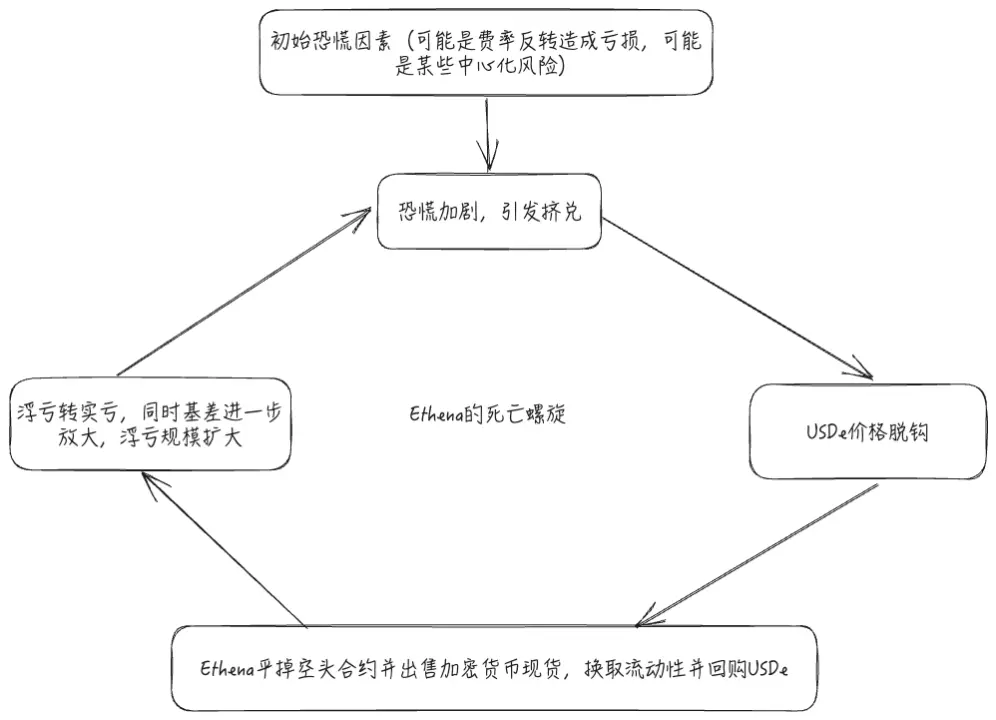

Of course, the liquidity issue of collateral is a problem that all stablecoin protocols will face. However, Ethena's mechanism design will introduce additional negative feedback mechanisms to the system, which means it is more susceptible to the risk of a death spiral. The so-called death spiral refers to when a bank run occurs, constrained by a certain factor, it amplifies the effects of panic, triggering a larger-scale bank run. The key here is the basis. The basis refers to the price difference between futures contracts and the spot market. Ethena's collateral design is essentially an investment strategy that shorts the basis in a cash-and-carry arbitrage. Holding the spot and shorting equivalent futures contracts, when the positive basis expands, it means that the price increase of the spot will be less than that of the futures contract, or the price decrease of the spot will be greater than that of the futures price. This investment combination will face floating loss risks. However, when a bank run occurs, users will sell large amounts of USDe in a short time, leading to a significant price decoupling in the secondary market for USDe. To stabilize this decoupling, arbitrageurs need to actively close their open short contracts in the collateral and sell the spot collateral to obtain liquidity to repurchase USDe from the secondary market, reducing the market circulation of USDe and restoring its price. However, with the closing operations, floating losses turn into actual losses, leading to a permanent loss of collateral value, and USDe may be in a state of insufficient collateralization. Meanwhile, the closing operations will further amplify the basis because closing short futures contracts will push up their futures prices, while selling the spot will suppress spot prices. This will further widen the basis, and the amplification of the basis will cause Ethena to face greater floating losses, which will accelerate user panic, leading to a larger-scale bank run until an irreversible outcome is reached.

This death spiral is certainly not alarmist. Although backtesting data indicates that the basis tends to revert to the mean in most cases, and after a period of development, the market will always reach a balanced state, this is not a suitable counterpoint for the above argument. Users have a very low tolerance for price fluctuations in stablecoins. For an arbitrage strategy, users may tolerate a certain degree of drawdown risk, but for stablecoins that serve as a store of value and medium of exchange, user tolerance is extremely low. Even for yield-bearing stablecoins that promote yields as their core selling point, the project’s publicity inevitably attracts a large number of users who do not understand the complex mechanisms and participate based on a literal understanding (this is also one of the core accusations faced by UST's founder Do Kwon, namely fraudulent promotion). These users are the core group that triggers bank runs and are also the ones who suffer the most significant losses, making the risk considerable.

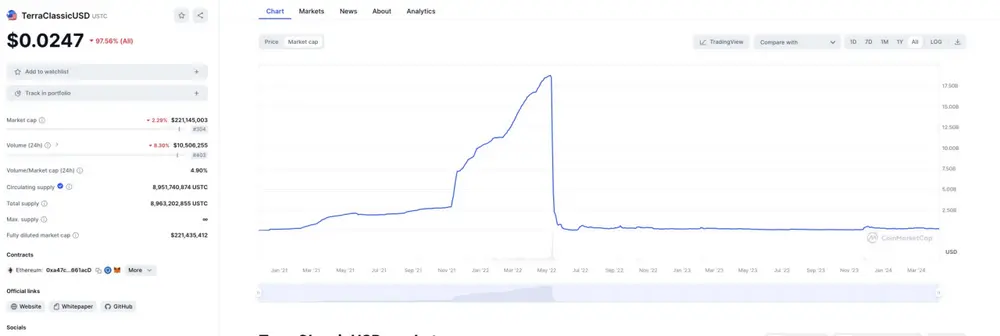

Of course, when there is sufficient liquidity for shorts in the futures market and longs in the spot market, this negative feedback will be somewhat alleviated. However, considering the current issuance scale of Ethena and the high subsidies that come with its deposit-absorbing capabilities, we must remain vigilant about this risk. After all, with Anchor providing a 20% savings subsidy, the issuance of UST skyrocketed from 2.8 billion to 18 billion in just five months. During this period, the entire cryptocurrency futures market scale could not keep pace with such growth. Therefore, it is reasonable to believe that the scale of Ethena's open contracts will soon explode to an exaggerated proportion. Imagine if over 50% of the short positions in the market are Ethena; their closing will face extremely high friction costs because there will be no shorts in the market that can bear such a large-scale closing in the short term. This will make the amplification effect of the basis more pronounced, and the death spiral will be more intense.

I hope that the above discussion can help everyone gain a clearer understanding of the risks associated with Ethena and maintain a sense of reverence for risk, not to be blinded by high yields.