Ethena is making a strong entrance. Can it continue the Luna legend? Leading the stablecoin track, will it spark a new storm?

What innovations does Ethena have?

What innovations does Ethena have?Author: Ken

Editor: Little Octopus

World Chain Niubite (niubite.com) shares that Binance's recent new coin mining projects have significantly improved in quality, such as AEVO, ETHFI, and Ethena. Both the mining returns and the subsequent performance of the tokens after listing have been quite impressive.

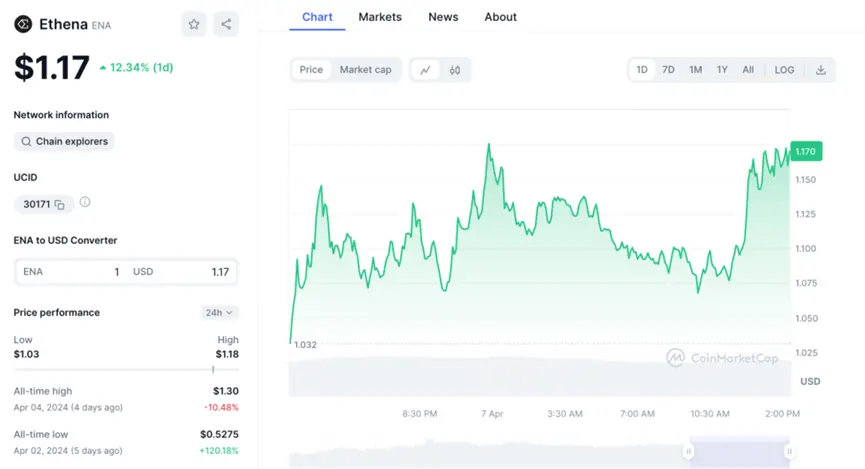

Take the algorithmic stablecoin Ethena (ENA), which launched on April 2nd, for example. Its price has increased by 120% from its low since its launch.

What innovations does Ethena have?

1. Innovations of Ethena

The inspiration for the Ethena project comes from Arthur Hayes, the founder of BitMEX, in his article "Dust on Crust" published last year.

In the article, he mentioned his vision for a new generation of stablecoins, which is to create a stablecoin supported by an equal amount of BTC spot longs and futures shorts.

Ethena Labs turned Arthur's vision into reality, but instead of using BTC as the main underlying asset, they chose ETH.

In other words, Ethena is a synthetic dollar protocol built on Ethereum, which launched a dollar stablecoin USDe, with ENA as its platform token.

USDe is actually an algorithmic stablecoin, and its minting mechanism is different from USDT and USDC. The stablecoin USDe minted through the Ethena protocol does not have USD as its underlying asset, but rather ETH.

Specifically, the collateral for USDe consists of an equal amount of spot ETH longs and futures ETH shorts, which allows for hedging, commonly referred to as "hedging."

Therefore, regardless of whether the ETH price rises or falls, USDe can maintain its "stability," which in professional terms means achieving "Delta neutrality."

Moreover, these ETH assets are not stored in centralized exchanges but are held on platforms like Copper, CEFFU, and Cobo, which helps mitigate risks such as exchange insolvency or misappropriation.

2. Sources of Income

The competition in the stablecoin sector is very fierce. How can USDe gain more market share against established stablecoins like USDT, USDC, and DAI?

The biggest highlight of USDe is its yield. Users who stake USDe can share in the dual income from the collateral assets.

First, 2024 is the year of staking, with more and more projects in the staking and re-staking sector. The underlying assets of USDe (such as ETH) can at least obtain relatively stable staking returns through these staking platforms. For example, ETH can be staked on platforms like Lido to earn around 4% annualized returns, ensuring a basic level of stable income.

Secondly, users can earn certain funding rates on these futures platforms. Although funding rates are an unstable factor, for short positions, the time when funding rates are positive is predominant in the long run, which also means that overall returns will be positive.

Let's take a look at Ethena's specific APY (Annual Percentage Yield).

According to statistics from the defillama platform, Ethena's Median APY is around 5% at its lowest and reaches about 55% at its highest, far exceeding the yields offered by other DeFi platforms.

3. Financing

Ethena has raised a total of $20.5 million through two rounds of financing, with the most recent round occurring on February 16 of this year, completing a $14 million financing at a valuation of $300 million.

The investment team behind Ethena is quite impressive, including Binance Labs, OKX Ventures, Dragonfly, etc., with both OKX Ventures and Dragonfly participating in both rounds of financing.

We also see traditional financial giants like Paypal and Franklin in the Ethena investment team.

Additionally, founders from multiple CEX platforms and derivatives trading platforms have also participated in Ethena's investment.

4. TVL and Revenue

According to statistics from the defillama platform, Ethena's TVL growth rate is very rapid. At the beginning of this year, it was only over $8,600, and it has now reached $1.857 billion. In just three months, the TVL has increased 21 times, thanks in large part to the significantly higher APY offered by the Ethena platform compared to others.

Currently, the minting volume of USDe has also surpassed 1.9 billion.

According to data from the defillama platform, the average monthly revenue of the Ethena platform can reach over $18 million, with daily revenue averaging over $230,000. Compared to the profitability of other DeFi platforms, Ethena's profitability can be considered quite strong. Of course, whether this high yield can be sustained remains to be seen.

5. Risks

The risks faced by Ethena mainly come from:

1. Staking Platform Risks

Putting USDe's underlying assets on staking platforms to earn returns naturally comes with some risks, such as the staking platform being hacked, which is not a risk faced solely by USDe.

2. Futures Contract Platform Risks

Such as platform malfeasance, hacking, etc.

3. Funding Rate Risks

Although the funding rate for short positions is positive most of the time, there is also the possibility of it turning negative. If the comprehensive yield after weighted staking returns is negative, it would have a significant impact on the "stablecoin."

In summary, although algorithmic stablecoins are not an original concept of Ethena, compared to Luna, Ethena has many innovations. For example, Ethena uses a model of holding spot ETH longs and futures ETH shorts to achieve the stability of USDe's value.

Currently, the market share of stablecoins has exceeded $150 billion and continues to grow, with USDT alone surpassing $100 billion, while Ethena's USDe is currently less than $2 billion, still over 50 times smaller than USDT.

Moreover, if the issuance of USDT is determined by the project party, the issuance of USDe is determined by users. Ultimately, the scale of USDe will be decided by users. If Ethena can continue to provide high yields, it will attract more users to mint, and if this model can be sustained, the scale of USDe may exceed our expectations. As the scale of USDe grows larger and the platform continues to operate smoothly, the application scenarios for USDe will increase, and it may even become a foundational stablecoin embedded in more DeFi applications.

As for ENA, as the platform token of Ethena, it will capture the value brought by the development of the Ethena platform. As the scale of USDe grows and its usage scenarios become richer, the price of ENA will naturally rise. Currently, ENA's market capitalization has surpassed $1 billion, and if it benchmarks against LUNA's market cap of over $10 billion, the future potential for ENA is still very large. Of course, whether Ethena's innovative model can be sustained remains to be seen, and we will wait and see.

P.S. This article does not constitute any investment advice.