Arthur Hayes: How will the cryptocurrency market trend before and after the Bitcoin halving?

The halving will drive up the price of Bitcoin in the medium term; however, the price trends before and after may be negative.

The halving will drive up the price of Bitcoin in the medium term; however, the price trends before and after may be negative.Author: Arthur Hayes, Founder of BitMEX

Translator: Deng Tong, Jinse Finance

Ping, Ping, Ping, this is my phone reminding me to monitor the nighttime snowfall at various ski resorts in Hokkaido. While this sound brings me immense joy in January and February, in March, it only brings FOMO.

I left Hokkaido at the beginning of March, having spent the past few ski seasons there. My recent experiences tell me that Mother Nature starts to heat up the ski resorts around March 1st. I am a beginner skier who only enjoys the driest and deepest slopes. However, this season has seen a significant change. There was a brutal warm spell in February that dispersed the snow. Cold weather didn’t return until the end of the month. But in March, temperatures dropped again, with 10 to 30 centimeters of fresh snow accumulating every night. That’s why my phone keeps buzzing.

Throughout March, I sat in various hot and humid countries in Southeast Asia, continually checking the app foolishly, ruining my decision to leave the ski slopes. The mild weather in April finally arrived, and my FOMO came to an end.

As readers know, my skiing experiences serve as a metaphor for my macro and cryptocurrency trading books. I previously wrote that the termination of the Bank Term Funding Program (BTFP) on March 12 would lead to a global market crash. The BTFP was canceled, and the anticipated vicious sell-off in the cryptocurrency space did not occur. Bitcoin decisively broke through $70,000, reaching around $74,000 at its peak. Solana continued to rise alongside various dog and cat Memecoins. My timing was off, but like the ski season, the unexpectedly favorable conditions in March will not repeat in April.

While I love winter, summer also brings joy. The arrival of summer in the Northern Hemisphere brings me the pleasure of sports, and I rearrange my time for tennis, surfing, and kiteboarding. Due to the policies of the Federal Reserve and the Treasury, summer will see a new influx of fiat currency liquidity.

I will briefly outline my thought process regarding how and why the risk asset market will experience extreme weakness in April. For those brave enough to short cryptocurrencies, the macro setup is favorable. While I won’t fully short the market, I have closed several dogshit coin and meme coin trading positions for a profit. From now until May 1, I will be in a non-trading zone. I hope to return in May with dry powder, ready to deploy for the true beginning of the bull market.

The Con

The Bank Term Funding Program (BTFP) ended weeks ago, but the non-Too-Big-to-Fail (TBTF) banks in the U.S. have not faced any real pressure since then. This is because the high priests of fraudulent finance have a series of tricks to secretly print money to rescue the financial system. I will peek behind the curtain and explain how they expand the dollar supply, which will support a broad rise in cryptocurrencies—until the end of this year. While the ultimate outcome is always money printing, there are periods in this process where liquidity growth slows, providing negative catalysts for risk markets. By carefully studying this series of tricks and estimating when rabbits will be pulled from hats, we can estimate when the free market will be allowed to operate.

Discount Window

The Federal Reserve and most other central banks operate a tool known as the discount window. Banks and other covered financial institutions in need of funds can pledge eligible securities to the Federal Reserve in exchange for cash. Overall, the discount window currently only accepts U.S. Treasuries (UST) and mortgage-backed securities (MBS).

Let’s assume a bank has been messed up by a group of peers and baby boomers running it. The UST it holds was worth $100 when purchased but is now worth $80. The bank needs cash to meet deposit outflows. A dogshit bank unable to repay can utilize the discount window instead of declaring bankruptcy. The bank exchanges the $80 UST for $80 in cash because, under current rules, the bank receives the market value of the pledged securities.

To abolish the BTFP and eliminate the associated negative stigma without increasing the risk of bank failures, the Federal Reserve and the U.S. Treasury are now encouraging troubled banks to use the discount window. However, under the current collateral terms, the discount window is not as attractive as the recently expired BTFP. Let’s return to the example above to understand why.

Remember, the value of the UST dropped from $100 to $80, meaning the bank has an unrealized loss of $20. Initially, the $100 UST was backed by $100 in deposits. But now the UST is worth $80; therefore, if all depositors flee, the bank will be short $20. Under BTFP rules, the bank receives the face value of the underwater UST. This means that the $80 UST will be exchanged for $100 in cash when delivered to the Federal Reserve. This restores the bank's solvency. But the discount window only provides $80 for the $80 UST. The $20 loss still exists, and the bank remains insolvent.

Given that the Federal Reserve can unilaterally change collateral rules to balance the treatment of assets between the BTFP and the discount window, by greenlighting the use of the discount window for insolvent banks, the Federal Reserve continues to conduct an invisible bank bailout. Thus, the Federal Reserve essentially resolves the BTFP issue; the entire UST and MBS balance sheet of the insolvent U.S. banking system (which I estimate to be $4 trillion) will be supported by funds printed through the discount window when needed. This is why I believe that after the BTFP ended on March 12, the market did not force any non-TBTF banks into bankruptcy.

Bank Capital Requirements

Banks are often required to fund governments that issue bonds at yields below nominal GDP. But why would private profit-making entities buy something with a negative real yield? They do so because bank regulators allow banks to purchase government bonds with little or no down payment. When banks with insufficient capital buffers against their government bond portfolios inevitably collapse due to the emergence of inflation and falling bond prices as yields rise, the Federal Reserve allows them to use the discount window in the aforementioned manner. Thus, banks prefer to buy and hold government bonds rather than lend to businesses and individuals in need of funds.

When you or I buy anything with borrowed money, we must pledge collateral or equity to cover potential losses. This is prudent risk management. But if you are a vampire squid zombie bank, the rules are different. After the 2008 Global Financial Crisis (GFC), global bank regulators attempted to force banks worldwide to hold more capital, creating a more robust and resilient global banking system. The rule set codifying these changes is known as Basel III.

The problem with Basel III is that government bonds are not considered risk-free. Banks must put up a small amount of capital for their massive sovereign bond portfolios. It turns out that these capital requirements are problematic during times of stress. During the market crash in March 2020, the Federal Reserve issued a decree allowing banks to hold UST without collateral backing. This enabled banks to intervene and store trillions of dollars in UST in a risk-free manner… at least in terms of accounting treatment.

When the crisis subsided, the Supplementary Leverage Ratio (SLR) exemption for UST was restored. Predictably, as UST prices fell due to inflation, banks went bankrupt due to insufficient capital buffers. The Federal Reserve conducted bailouts through the BTFP and now the discount window, but this only compensates for losses incurred during the last crisis. How can banks ramp up and absorb more bonds at the currently unattractive high prices?

The U.S. banking system loudly proclaimed in November 2023 that due to Basel III forcing them to hold more capital in their government bond portfolios, Bad Gurl Yellen could not shove more bonds down their throats. Therefore, some concessions must be made, as there are no other natural buyers for U.S. government debt at negative real yields. Here’s how banks politely express their unstable situation.

Demand from some traditional buyers for U.S. Treasuries may have weakened. Since last year, the asset value of bank securities portfolios has been declining, with banks holding $154 billion less in U.S. Treasuries than a year ago.

The Powell-led Federal Reserve saved the day once again. At a recent U.S. Senate banking hearing, Powell suddenly announced that banks would not face higher capital requirements. Remember, many politicians have called for banks to hold more capital to prevent a repeat of the regional banking crisis in 2023. Clearly, banks are lobbying hard to eliminate these higher capital requirements. They have a strong argument—if you, Bad Gurl Yellen, want us to buy dogshit government bonds, then we can only profit through infinite leverage. Banks around the world manage various types of governments; the U.S. is no exception.

To add to the mix, the International Swaps and Derivatives Association (ISDA) recently issued a letter advocating for UST to be exempt from the SLR I mentioned earlier. Essentially, if banks are not required to make any down payment, they can hold trillions of dollars in UST to finance the U.S. government deficit on a future basis. I expect the ISDA proposal to be accepted as the U.S. Treasury ramps up debt issuance.

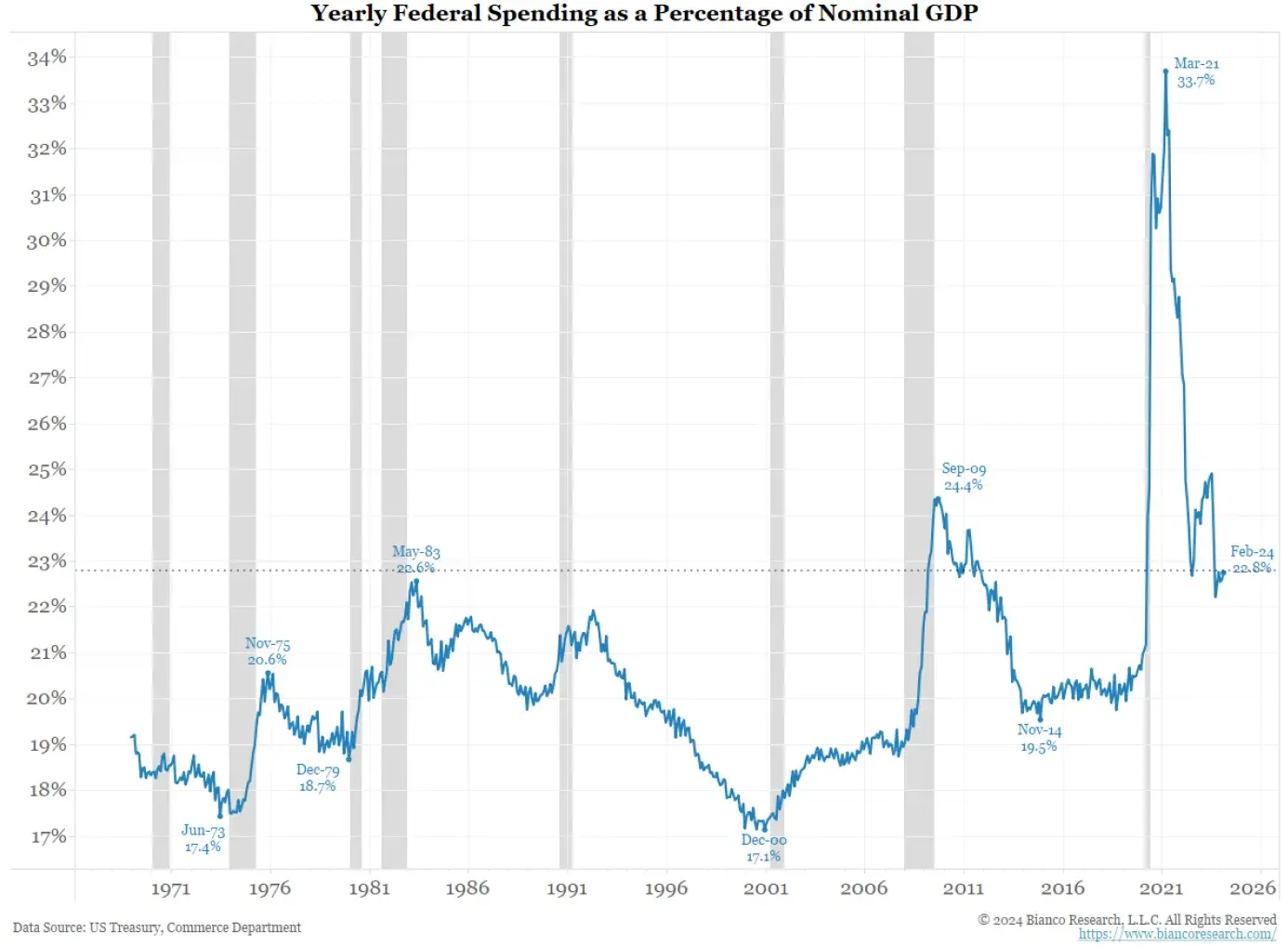

This excellent chart from Bianco Research clearly illustrates the extent of waste by the U.S. government, evidenced by record-high deficits. The reasons for the higher deficit spending in the last two periods are the 2008 Global Financial Crisis and the pandemic lockdowns dominated by the baby boomer generation. The U.S. economy is growing, but the government is spending like it’s a recession.

In summary, relaxing capital requirements and potentially exempting UST from the SLR in the future is a covert way of printing money. The Federal Reserve does not print money; rather, the banking system creates credit money out of thin air and buys bonds, which then appear on their balance sheets. As always, our goal is to ensure that government bond yields do not rise above the nominal GDP growth rate. As long as real rates remain negative, assets like stocks, cryptocurrencies, and gold will continue to rise in price when measured in fiat currency.

Bad Gurl Yellen

My article "Bad Gurl" delves into how the U.S. Treasury, led by Bad Gurl Yellen, is increasing the issuance of short-term Treasury bills (T-bills) to exhaust the trillions locked in the Federal Reserve's reverse repo program (RRP). As expected, the decline in the suggested retail price coincided with the rise in stocks, bonds, and cryptocurrencies. But now the suggested retail price has dropped to $400 billion, and the market is wondering what the next source of legal liquidity to boost asset prices will be. Don’t worry, Yellen isn’t done yet, shouting, "Loot is about to drop."

RRP Balance (White) vs. Bitcoin (Yellow)

The flow of legal funds I will discuss focuses on U.S. tax payments, the Federal Reserve's Quantitative Tightening (QT) plan, and the Treasury General Account (TGA). The timeline discussed is from April 15 (the tax due date for the 2023 tax year) to May 1.

Let me provide a quick guide on their positive or negative impacts on liquidity to help you understand what these three things mean.

Tax payments eliminate liquidity from the system. This is because taxpayers must withdraw cash from the financial system, often by selling securities, to pay their taxes. Analysts expect that due to receiving substantial interest income and strong stock market performance, tax payments for the 2023 tax year will be elevated.

QT eliminates liquidity from the system. As of March 2022, the Federal Reserve allowed approximately $95 billion in UST and MBS to mature without reinvesting the proceeds. This led to a decline in the Federal Reserve's balance sheet, which is known to reduce dollar liquidity. However, what we care about is not the absolute level of the Federal Reserve's balance sheet but the speed at which it is declining. Analysts like Joe Kalish from Ned Davis Research expect the Federal Reserve to reduce QT by $30 billion per month at the May 1 meeting. As the pace of the Federal Reserve's balance sheet decline slows, the slowdown in QT will be beneficial for dollar liquidity.

When the TGA balance rises, it eliminates liquidity from the system, but when the TGA balance falls, it adds liquidity to the system. The TGA balance increases when the Treasury receives tax payments. I expect that with the tax processing on April 15, the TGA balance will be far above the current level of about $750 billion. This is negative for dollar liquidity. Don’t forget that this year is an election year. Yellen's job is to ensure her boss, President Joe Biden, is re-elected. This means she must do everything possible to stimulate the stock market, making voters feel wealthy and attributing this great achievement to Biden's slow "genius" economics. When the RRP balance eventually drops to zero, Yellen will spend the TGA, likely releasing an additional $1 trillion in liquidity into the system, which will boost the market.

The unstable period for risk assets is from April 15 to May 1. During this time, tax payments will eliminate liquidity from the system, QT will continue at the currently high pace, and Yellen has not yet started to reduce the TGA. After May 1, the pace of QT will slow, and Yellen will be busy cashing checks to lift asset prices. If you are a trader looking for the right time to establish shameless short positions, April is the best time. After May 1, it will return to the regular schedule… initiated by the financial shenanigans of the Federal Reserve and the U.S. Treasury, leading to asset inflation.

Bitcoin Halving

The Bitcoin block reward is expected to halve on April 20. This is seen as a bullish catalyst for the cryptocurrency market. I agree it will push prices higher in the medium term; however, the price action before and after may be negative. The narrative that halving is beneficial for cryptocurrency prices is deeply entrenched. When most market participants agree on a particular outcome, the opposite usually occurs. This is why I believe Bitcoin and cryptocurrency prices will generally plummet before and after the halving.

Given that the halving occurs when dollar liquidity is tighter than usual, this will add fuel to the frenzy of selling off crypto assets. The timing of the halving further reinforces my decision to refrain from trading before May.

So far, I have realized full profits on positions in MEW, SOL, and NMT. The proceeds have been deposited into Ethena's USDe and staked for substantial returns. Before Ethena, I held USDT or USDC and earned nothing, while Tether and Circle reaped all the Treasury yields.

Will the market overcome my bearish inclination and continue to rise? Yes. I have always been passionate about cryptocurrencies, so I welcome mistakes.

When I do a two-step at Token2049 Dubai, do I really want to see my most speculative junk coin positions? Absolutely not.

So, I dumped them.

No need to be sad.

If the dollar liquidity scenario I discussed above comes to fruition, I will be more confident in mimicking various dogshit. If I miss out on a few percentage points of gains but absolutely avoid losses to my portfolio and lifestyle, that is an acceptable outcome. With that, I bid you farewell. Remember to put on your dancing shoes, and I’ll see you in Dubai to celebrate the cryptocurrency bull market.