Pantera Partners: How should founders of Web3 projects optimize token distribution?

Successful token distribution requires allocating the majority of tokens to community holders and future incentives for the core team.

Successful token distribution requires allocating the majority of tokens to community holders and future incentives for the core team.Original Title: Optimizing Your Token Distribution 2023

Original Author: Lauren Stephanian, Partner at Pantera Capital

Original Compiler: Luffy, Foresight News

Two years ago, we published the report "Optimizing Token Distribution," an analysis of token distribution models aimed at helping founders think more critically about network token allocation. The trends in the crypto space are rapidly changing, and with renewed market enthusiasm, more and more founders are beginning to draft their own token distribution models and issue tokens. This report combines the latest data with our updated analytical framework to provide valuable references for founders.

As a reminder, protocol founders typically raise funds to issue tokens to private investors and their communities. These tokens generally represent governance rights, allowing holders (insiders, private investors, and the community) to participate in the decision-making processes of products, services, or protocols. Protocols usually have a fixed token supply, and teams must carefully allocate tokens, optimizing the recipient groups and distributing tokens to users and partners.

In our exploration in 2022, we utilized data extracted from private pitch platforms, public media posts, blogs, and GitHub READMEs dating back to 2014 to explore the main trends in token distribution. Now, two years later, we have improved the dataset and further explored the latest trends in token distribution.

Please note: This report was published in March 2024 and used publicly available information as well as aggregated and anonymized private data points. The authors of this report have not independently verified the accuracy of these token distributions.

Key Trends in Token Distribution

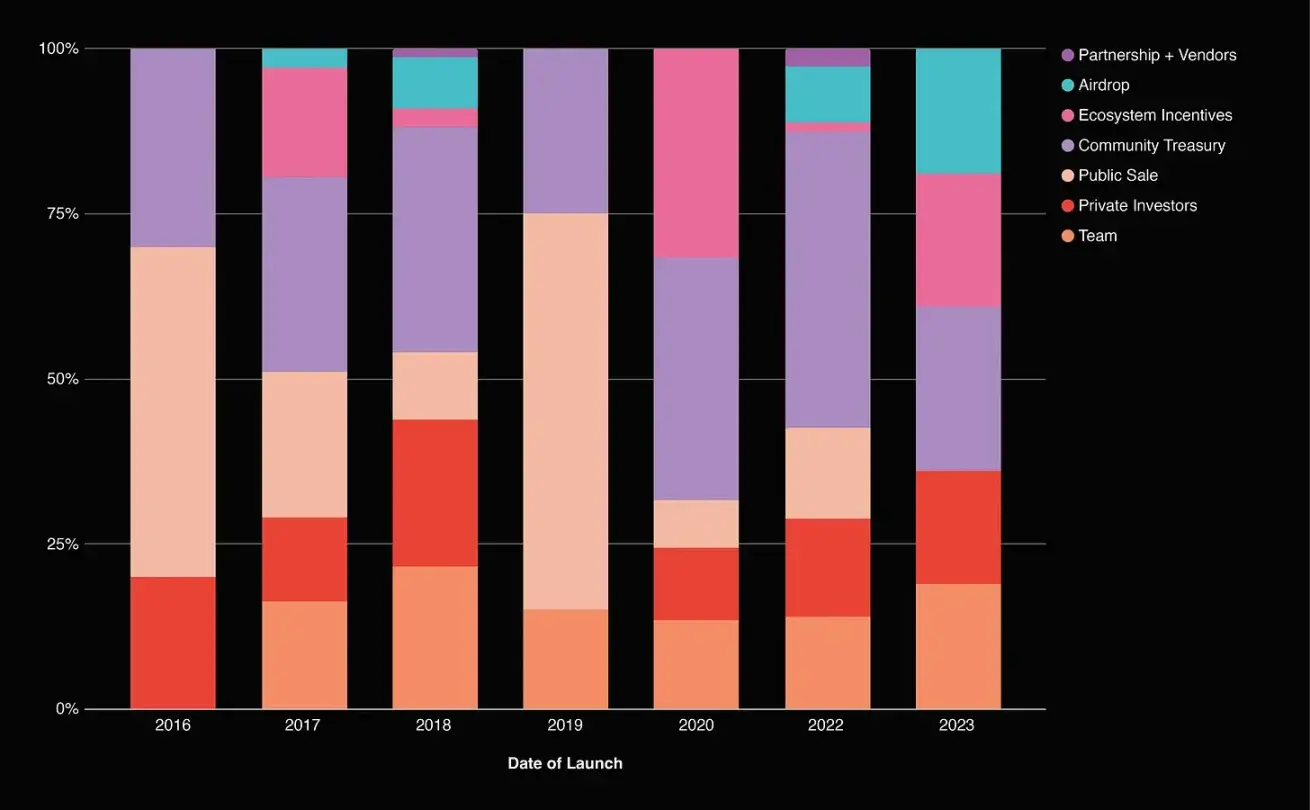

Token distribution can be divided into seven main parts:

· Core Team

· Private Investors

· Community Treasury

· Ecosystem Incentives

· Airdrops

· Public Sale

· Partners and Vendors

We have compiled token distributions from over 150 projects and protocols to analyze the apparent trends in the field more comprehensively.

Team

This is the token allocation reserved for founders, past and future employees, and advisors. These tokens typically have the longest lock-up periods, usually aligned with those of investors.

The above chart of team allocation includes core contributors, future contributors, and advisors. For a more detailed understanding of core team allocations, see the chart below, which indicates a gradual increase in core team allocation shares.

Core Team Allocation

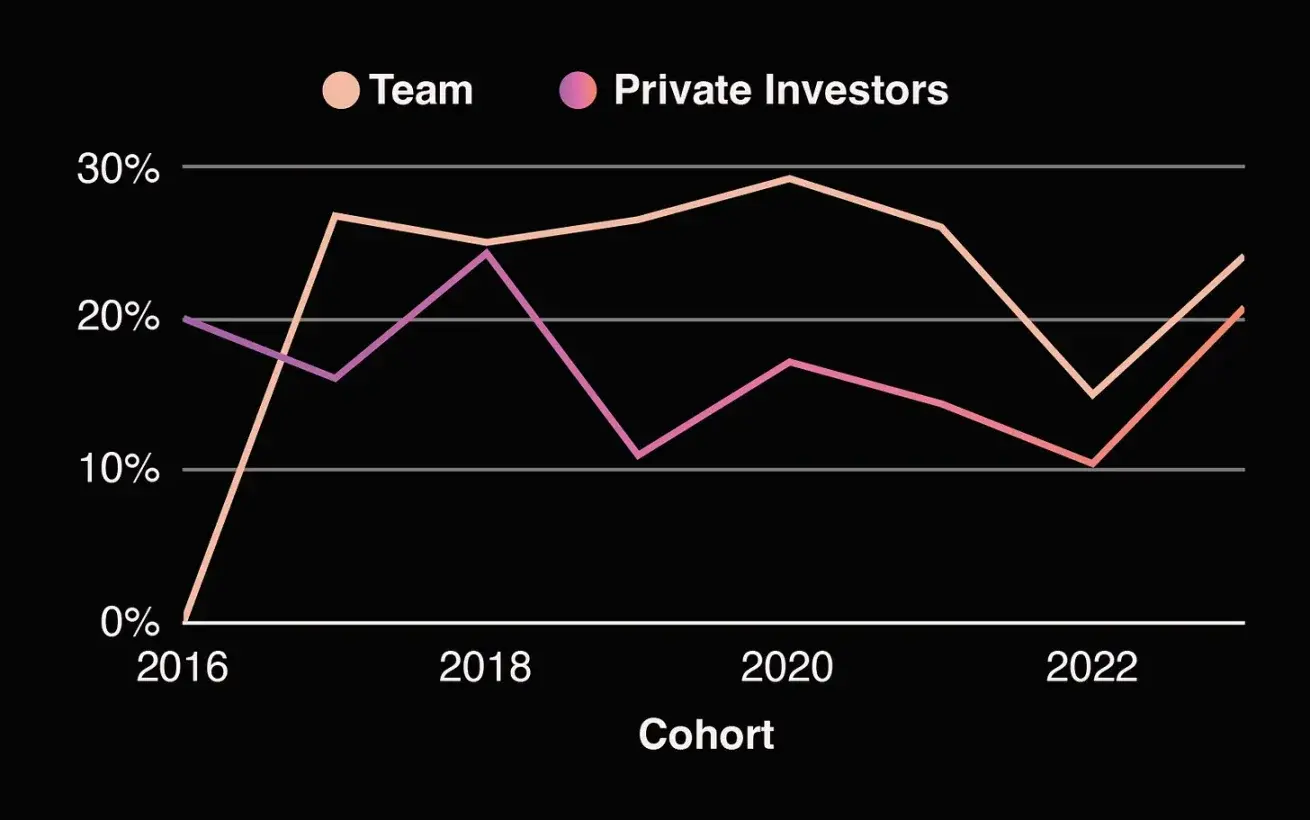

Team allocation appears to have some correlation with our position in the market cycle, which is not surprising but still worth noting. As the total market capitalization of cryptocurrencies grows, the funds allocated to teams also increase, while when market capitalization shrinks, the funds allocated to teams decrease.

Team Allocation vs. Cryptocurrency Market Capitalization, Source: Market Cap

Private Investors

This is the share allocated to capital providers who purchase rights to future tokens or equity, which are then converted into tokens. These tokens have lock-up restrictions, usually consistent with those of the core team.

Private Investor Token Allocation

Interestingly, although we expected the allocation for investors to be inversely proportional to that of the team, in reality, this ratio has also been on the rise over the past year. Currently, this ratio is roughly at the level of 2018.

Comparison of Team and Private Investor Allocations

Initially, I thought this might be related to large-scale financing at the end of 2023, but from the industry financing data, this doesn't make much sense, as the increase in valuations has outpaced the increase in financing amounts.

Median Financing Amount

Median Valuation

This may relate to founders raising funds they do not urgently need after waiting for the recent bear market to end.

Public Investors

This is the token allocation sold to the public. Public sales of tokens were previously known as "ICOs," sold at the time of token issuance and fully circulating.

Predictably, due to regulatory risks, the share of public sales has gradually approached zero.

Token Allocation for Public Sales

Airdrops

The disappearance of the public sale token model raises the question: how to distribute tokens to the community? One potential method is airdrops.

Airdrop Allocation

Treasury

These tokens will be reserved for future distribution through governance. Treasury tokens are often viewed as the project's "reserve pool"—allocated to different stakeholders through voting proposals.

Treasury allocations fluctuate over time, peaking in 2022. After that, there has been a downward trend, and we may see a reduction in treasury allocations due to increases in other categories.

Ecosystem Incentives

These tokens are designated for growth programs at launch, allowing users to profit from a pre-specified token pool. Incentives have become an alternative to public sales, including growth programs and liquidity mining.

The allocation ratio for ecosystem incentives is declining, but given the rapid growth of airdrop ratios, many founders are likely viewing incentives as a larger category, so you could argue that this decline is closely related to the significant increase in airdrops.

Ecosystem Incentive Allocation

Partners and Vendors

These tokens include pools of funds used to pay for legal, rent, third-party marketing, and other expenses. The decline may simply be due to these expenses being unclassified and confused with treasury allocations.

Token Distribution by Project Type

Each type of project has its unique allocation patterns.

Here are the specific performances of various types of projects. Note that these are post-pandemic averages.

Not surprisingly, DAOs tend to allocate more tokens to their treasury/foundation, while L1 prioritizes airdrops and (at least before 2023) public sales. L2 tends to prioritize ecosystem growth incentives, which may later also be used for airdrops. DApps spend the most on community incentives, but not necessarily through airdrops, but rather through liquidity mining and other means.

Now, we will delve deeper into each subcategory.

DAO

Over time, we have seen some changes in DAO allocations. Community funding has remained high over the years, while team allocations have gradually decreased, and foundation allocations have increased. Unfortunately, we do not have enough data after 2023 to calculate averages.

DAO Token Allocation Breakdown

2022 "Typical" DAO Token Allocation

DApp

In examining DApp token distributions, we can see that team allocations have been slowly decreasing over time (with a significant drop after 2014), while investor allocations and airdrop allocations have been increasing.

DApp Token Allocation Breakdown

Infrastructure: L1 and L2

Due to their similarities, the chart below combines L1 and L2 token allocations. We can see that public sale allocations have decreased over time. Community allocations have fluctuated slightly over the years, while investor and team allocations have both increased in 2023. A significant portion of token allocations in 2023 has been used for airdrops.

L1 and L2 Token Allocation Breakdown

Upon closer inspection of the differences between typical L1 and L2 token allocations, you will find that L2 tends to reserve less funding for ecosystem growth pools while allocating more for public sales and airdrops. L2 teams also tend to receive a smaller allocation ratio.

Typical L1 Token Allocation: Only 2022 data is provided due to a lack of 2023 data

Typical L2 Token Allocation: Data from 2022 and 2023

Interviews

All of the above charts show historical averages over time. This time, we will share some anecdotal data from founders during the early token issuance period to understand their regrets and satisfactions regarding token distribution.

Here are their comments:

Livepeer

Livepeer was founded in 2017, long before DAO governance tools emerged, when cryptocurrencies were still in their infancy.

"I am generally satisfied with the way tokens were distributed, initially through an algorithm we created called Merklemine, which was decentralized and open. Then, tokens were continuously distributed through inflation to node operators and other active participants in the network. This kept the tokens in the hands of those directly helping the network while also allowing access for everyone and enabling thousands of users to discover Livepeer through the process of receiving tokens via MerkleMine.

As for what changes I would make, it would have been great to utilize DAO governance tools for community governance finances if they had been more mature and available when the network launched six years ago. This would have helped future ecosystem growth by allowing tokens to be sent directly to video developers and others who did not directly receive network rewards. But at that time, these tools were still immature and complex to build, so it was not a priority. We did not want to have centralized control over token distribution, so we did not retain a treasury managed by a large company."

------ Livepeer Founder Doug Petkanics

Well-Known DApp Founded in 2018

"I think the token distribution itself ultimately worked out well for us, and I rarely think: what if…?

But if I could go back, I would place more emphasis on raising funds from the following groups: 1) those capable of actively engaging in quantitative trading, 2) those willing to speak their minds, and 3) those actively participating in governance.

As founders, one of the best things we did was not to take too high a share—this allowed us to compensate important participants in the network and still have room."

------ Founder of a well-known DeFi protocol established in 2018

What is the "Best" Way?

After the release of the 2022 report, it was pointed out that averages are not always the best benchmarks. Therefore, it would be interesting to reverse-engineer some of the most notable and recent cross-category token issuances.

Reverse Analysis of Top Projects' Token Issuances

Layer 2

OP Market Cap (as of March 2024)

Looking at Optimism, they have a large fund dedicated to RPGF, which is a new strategy to incentivize builders to participate in their platform. The fund typically provides a certain amount of funding to investors and core contributors, with airdrops being an important component.

Optimism Token Allocation, Source: https://community.optimism.io/docs/governance/allocations/

Layer 1

Celestia is a Layer 1 protocol. They allocate most of their tokens to investors and a significant portion to ecosystem developers. Incentive allocations also make up a considerable part.

Celestia Token Allocation, Source: https://docs.celestia.org/learn/staking-governance-supply

DApp

GMX Market Cap (data as of March 2024)

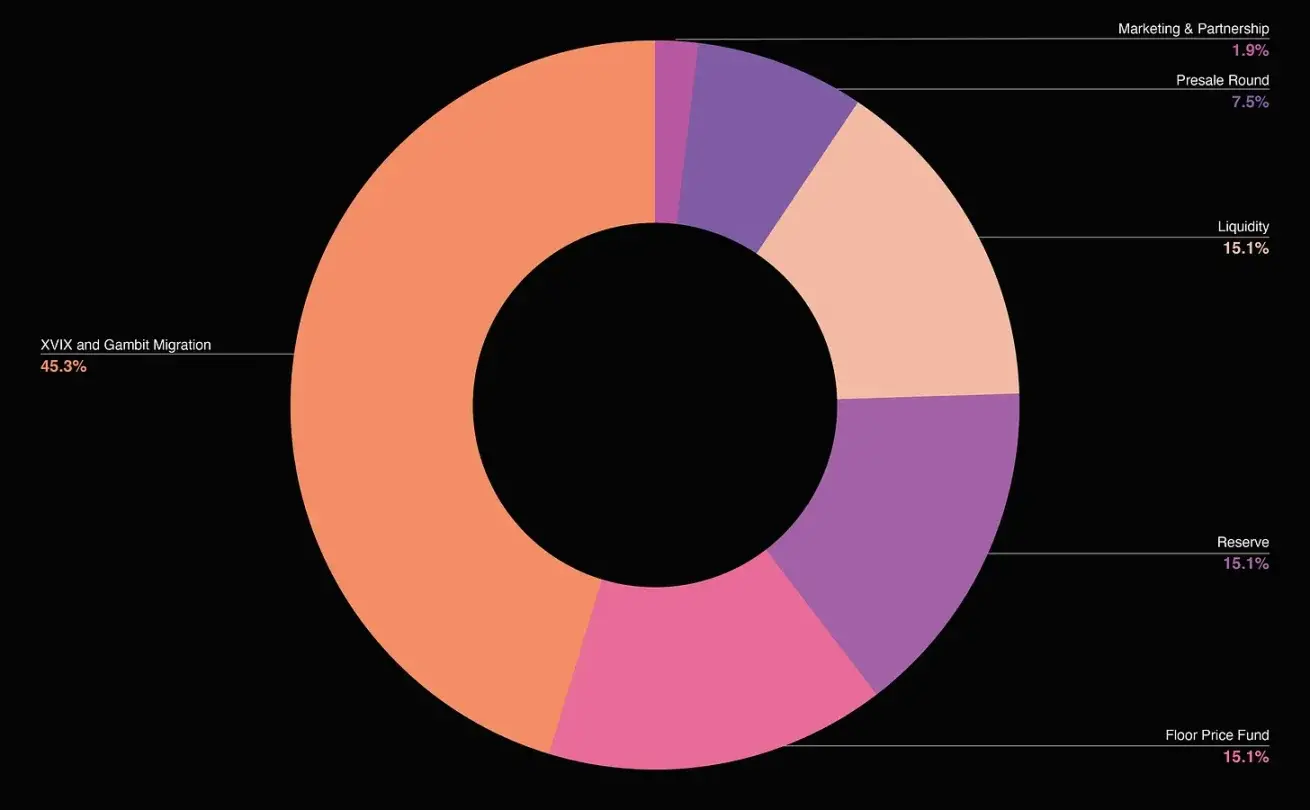

GMX, as a DeFi DApp, has a more complex token allocation, with a significant portion allocated to meet the long-term operational needs of the DApp, particularly related to maintaining product functionality, such as liquidity reserves.

GMX Token Allocation, Source: https://tokenomicsdao.substack.com/p/tokenomics-101-gmx

Conclusion

With the recent bull market, there have been significant changes in token distribution over the past year.

Team

· In 2023, the average allocation received by teams was 24%.

· Team allocations are correlated with market timing, and in this bull market, teams will have greater influence.

· Team and investor allocations are not necessarily inversely proportional; in fact, both have been on the rise in this bull market.

Private Investors

In 2023, private investors received an average allocation ratio of 20%.

Community Treasury

In 2023, the average allocation ratio for community treasuries was 28%.

Public Sale

In 2023, the proportion of public sales was nearly zero.

Ecosystem Incentives

In 2023, the average allocation ratio for ecosystem incentives was 8%.

Airdrops

· In 2023, the average allocation ratio for airdrops was 20%.

· Airdrops have become an important component of community building, and airdrop strategies are crucial.

Successful token launches require allocating a significant portion of tokens to community holders and future incentives for the core team.

In a bull market, teams have the upper hand as venture capital firms rush to participate. Founders reduced ownership in the last bear market, but the current ownership percentage has returned to the levels seen in the last bull market of 2021. One of the challenges that founders in the crypto space need to address is balancing incentives and the semi-retirement of core team members at the time of initial token vesting.

Additionally, the popularity of airdrops has grown exponentially, leading to a range of engagements from crypto users—both good and bad. Over time, crypto users have become increasingly sophisticated: users not only set up wallets on protocols but also bridge protocols, participate in trading, submit code requests on the protocol's GitHub, and more—often leaving builders feeling frustrated.

The crypto space is ever-changing, and we continually see innovations in marketing, ecosystem development, financing, and team compensation. Interestingly, we seem to have accepted the reality of earning tokens through participation in protocols, but the question remains how to extend participation time and familiarize users with using your platform.

One evolution of the airdrop framework is the points system, which can be used to incentivize activities while retaining full control for the founding team. This may be detrimental to the community, as it allows founders to incentivize user participation without fully committing to token distribution.

RPGF is also an emerging topic, serving as a way to incentivize the building of public goods—providing tools for the ecosystem to make it easier to access or build. Public goods are extremely important for Layer 1 and Layer 2, but they are often not supported by venture capital. RPGF is used to incentivize the construction of these public goods and enhance the entire ecosystem, categorized under ecosystem growth. So far, it has allocated over $300 million to more than 1,000 entities.