U.S. Judge "Takes Sides" with SEC in Coinbase Lawsuit, Favorable for Base Ecosystem?

The court will question the lack of regulatory transparency and registration capability, thereby prompting the SEC to seek more specific solutions.

The court will question the lack of regulatory transparency and registration capability, thereby prompting the SEC to seek more specific solutions.Written by: Kaori, BlockBeats

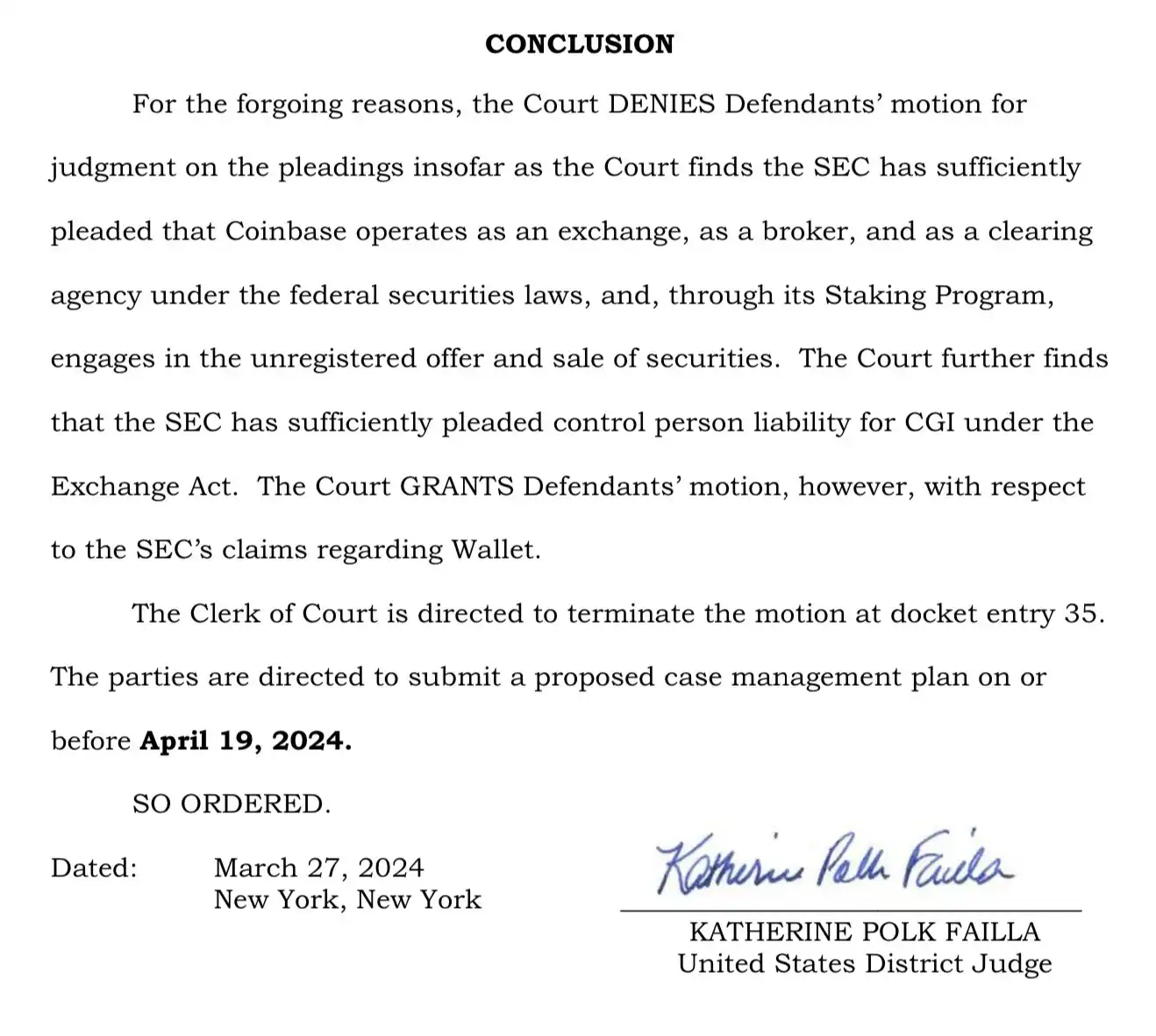

On March 27, in an 84-page ruling, the U.S. District Court for the Southern District of New York denied Coinbase's motion to dismiss in the case brought by the SEC for failing to register as a securities business.

The ruling was authored by U.S. District Judge Katherine Failla, who found that the SEC had made "reasonable" allegations against Coinbase, allowing the SEC to continue its claims that Coinbase operates as an unregistered trading platform, broker, and clearing agency, and "participates in unregistered securities offerings and sales" through its staking program. The court set a deadline of April 19 for both parties to agree on a case schedule.

Following the announcement, Coinbase's stock price had dropped over 10% as of the time of writing.

Coinbase's "Fight to the End" with the SEC

In June of last year, the SEC sued Coinbase, accusing it of providing trading and staking services to the public in violation of federal securities laws, and also claimed that Coinbase Wallet acted as an unregistered brokerage. In the same week, the SEC also sued Binance, but that lawsuit was settled by the end of last year.

In July of the same year, Coinbase submitted a response document and a motion to dismiss in its lawsuit against the SEC, addressing the regulator's accusations of illegally operating an unregistered securities exchange.

Coinbase's Chief Legal Officer Paul Grewal stated that the company does not list securities and that the process used for token listings is entirely consistent with the SEC's review in early 2021, marking Coinbase's formal response to this legal dispute and signaling the start of a lengthy legal battle.

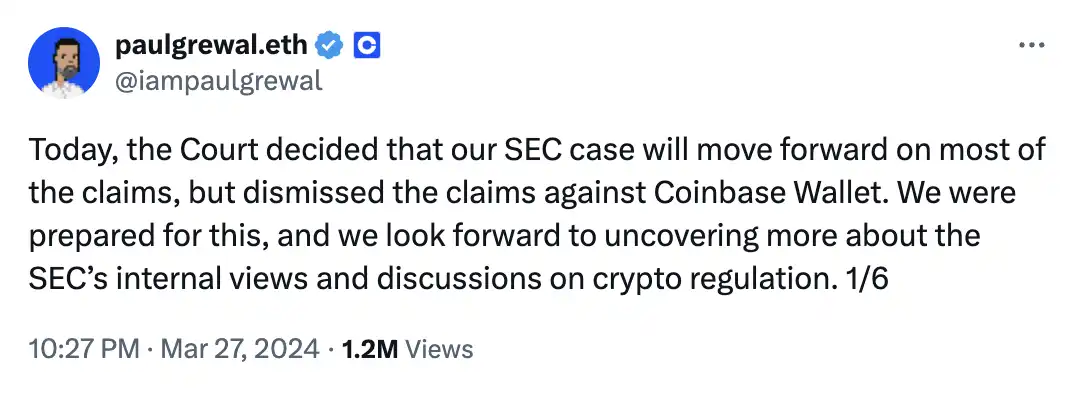

What happened last night was another key development in the confrontation between Coinbase and the SEC. Paul Grewal stated last night, "Today, the court decided that our SEC case will proceed on most claims, but dismissed the claims against Coinbase Wallet. We were prepared for this and look forward to learning more about the SEC's internal views and discussions on cryptocurrency regulation."

Meanwhile, an SEC spokesperson stated, "We are pleased that another court has confirmed that while the term 'cryptocurrency' may be relatively new, the framework used by courts to identify securities has been applicable for nearly 80 years."

However, this is not entirely negative news for Coinbase or the cryptocurrency sector.

In March of this year, in opening remarks submitted to the Third Circuit Court of Appeals, Coinbase requested that the appellate court direct the SEC to begin drafting cryptocurrency rules. Coinbase argued that the SEC violated the Administrative Procedure Act by failing to engage in rulemaking and not providing detailed reasons for rejecting Coinbase's rulemaking petition.

"The SEC does not have the statutory authority to extend the existing securities regime to digital assets, but if the SEC insists on moving forward without congressional authorization, then decisions must be made and enforced through forward-looking rulemaking," Coinbase stated.

Therefore, yesterday's ruling is favorable for promoting clarity in cryptocurrency rulemaking. Similar to the Binance case, the judge may support the SEC in specific cases and impose fines on Coinbase. However, the court will question the lack of regulatory transparency and registration capabilities, thereby pushing the SEC to seek more specific solutions, which is a positive outcome for Coinbase.

The Outcome May Not Be So Bad

At the same time, another noteworthy point from yesterday's court ruling, which the market reacted positively to, is that Judge Failla dismissed the SEC's claim that Coinbase acted as an unregistered broker through its wallet application.

Coinbase argued that Wallet does not "engage in routing activities," "cannot control users' crypto assets or transactions conducted through Wallet," and that users "are the sole decision-makers in transactions," while Wallet "merely provides the technical infrastructure for users to arrange transactions on other DEXs in the market." This ruling is a true recognition of the technology discussed here, thus opening up more market possibilities for Base and on-chain DeFi.

In late February of this year, Coinbase announced the launch of two new wallet solutions—smart wallets and embedded wallets—aimed at making it easier for new users to enter the on-chain space and overcome user experience barriers in creating crypto wallets. These solutions will be added to the Coinbase Wallet SDK, allowing users to create and use wallets without needing long seed phrases. One of the goals set for Base in its 2024 roadmap is to make smart wallets the default option.

After this ruling, crypto KOLs expressed that "Jesse (the head of the Base protocol) is dancing joyfully on Base."

On March 27, Coinbase Vice President Max Branzburg posted on social media, stating, "In the future, Coinbase will store more enterprise and customer USDC balances on Base. This allows Coinbase to manage and protect customer funds with lower fees and faster settlement times, without compromising the Coinbase user experience. Coinbase is excited to continue moving business on-chain and hopes other companies will follow suit."

With the overall increase in Base's ecosystem TVL and Coinbase's strong support for Base, the market generally holds an optimistic view of the outcome of this case ruling, believing that Coinbase will ultimately prevail, and that this will serve as a catalyst for the Base narrative.