Coinbase Weekly Report: What Caused This Round of Decline? What Is Its Impact on Future Trends?

Spot Bitcoin ETFs experienced a second week of capital outflows, despite the macro environment remaining favorable for more inflows after the FOMC meeting.

Spot Bitcoin ETFs experienced a second week of capital outflows, despite the macro environment remaining favorable for more inflows after the FOMC meeting.Original Title: Weekly: Pause and Effect

Authors: David Duong (Head of Institutional Research), David Han (Institutional Research Analyst)

Overview

- In the U.S., the first week of net outflows from spot Bitcoin ETFs in two months was concentrated around the Grayscale Bitcoin Trust (GBTC).

- We expect the current deflationary trend in the U.S. to remain unchanged, with financial conditions continuing to loosen and the market supported by the Federal Reserve's quantitative tightening plan reduction.

- Following the meme coin frenzy and the Dencun upgrade, there has been a surge in on-chain activity across many networks, particularly on Solana and Ethereum's Layer 2 (L2) solutions like Base, leading to a decline in chain performance.

Market Observation

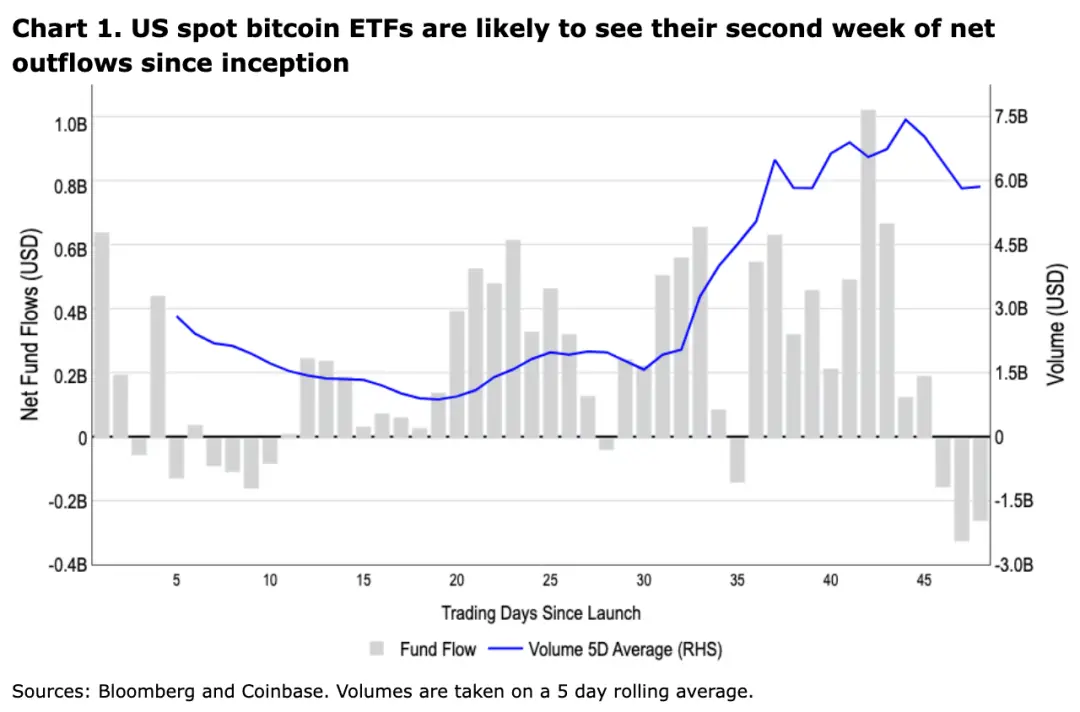

The cryptocurrency market's attention remains focused on capital flows rather than fundamentals, as U.S. spot Bitcoin ETFs experienced their first week of net outflows in two months (amounting to $836 million from March 18 to 21). Few seem to understand what caused the surge in outflows from the Grayscale Bitcoin Trust (GBTC), which saw a total net outflow of $1.83 billion over four days, averaging $458 million per day. In contrast, the average daily outflow from GBTC over the past three weeks was only about $290 million. Additionally, in the previous weeks, we observed positive inflows into other funds offsetting GBTC's outflows, indicating that we were witnessing some capital shifts at that time.

Since mid-February, one of the potential sources of selling pressure we have anticipated is that Genesis Global Holdco LLC may sell 35.9 million GBTC shares (worth $2.1 billion). Recall that Genesis received permission from the U.S. Bankruptcy Court for the Southern District of New York on February 14 to sell its GBTC shares. Of these shares, approximately 31.2 million were pledged by Gemini Trust Company to the Gemini Earn Program. However, the court ruled that Genesis had never properly collateralized these shares to borrow from Earn users, allowing Genesis to sell these shares at market value to repay creditors, whether in cash or Bitcoin. A Wall Street Journal report on March 18 indicated that a creditor-supported pending proposal could return up to 77% of the shares held by customers in physical form.

Note that this is not the same event as Genesis using 30.9 million GBTC shares as collateral to borrow 1.2 billion GBTC shares from 23.2 million Earn users during Q3 2022. Gemini recently reached a settlement with Genesis to return all these assets in physical form, with 97% expected to be paid out in the coming weeks, pending court approval.

It remains unclear whether the recent GBTC outflows are related to these sales, as there have been no direct public documents announcing this information. Currently, we can only infer that the scale and scope of changes in GBTC's circulating shares align with the latest developments regarding Genesis's payment obligations. More importantly, given that most creditor payments will be made in cryptocurrency rather than cash, we believe the market's impact on Bitcoin's performance should ultimately be net neutral.

So far, there appears to be no unusual activity in BTC spot trading volumes on global centralized exchanges, despite average trading volumes of around $35 billion on March 19 and 20, which is higher than the previous four-week average daily trading volume of $25 billion (on working days). If these GBTC sales have indeed been completed, we believe the macro environment remains conducive to more inflows into spot Bitcoin ETFs following the Federal Reserve meeting that ended on March 20. Interest rates are expected to remain unchanged, but at the same time:

- According to the dot plot, it chose not to change its forecast for three rate cuts in 2024 (although it raised the points for 2025 and 2026),

- It raised its 2024 real GDP growth forecast from 1.4% to 2.1%, and

- It hinted that the reduction of its quantitative tightening plan would "begin soon."

We believe that the Fed's decision to cut rates in May or June is currently less important than the direction it has established in relation to the market. We expect that as the Fed reduces the number of bonds it cuts from its balance sheet each month, financial conditions in the U.S. will continue to loosen, the deflationary trend will remain unchanged, and the market will be supported as a result.

Meanwhile, ETH's performance this week has been slightly different from BTC's, following reports that the Ethereum Foundation received inquiries from an unidentified "national authority" around February 26, 2024. So far, no information regarding the jurisdiction or content of this inquiry has been made public. On Twitter, a partner at Willkie Farr & Gallagher stated, "It is extremely common for crypto protocol foundations to receive mandatory information requests." The public prediction market has reduced the likelihood of the U.S. spot ETH ETF being approved before March 31 from 48% a month ago to 17%. However, we believe that despite the effective exclusion of approval possibilities, ETH still seems to be performing quite well.

On-chain: Scalability

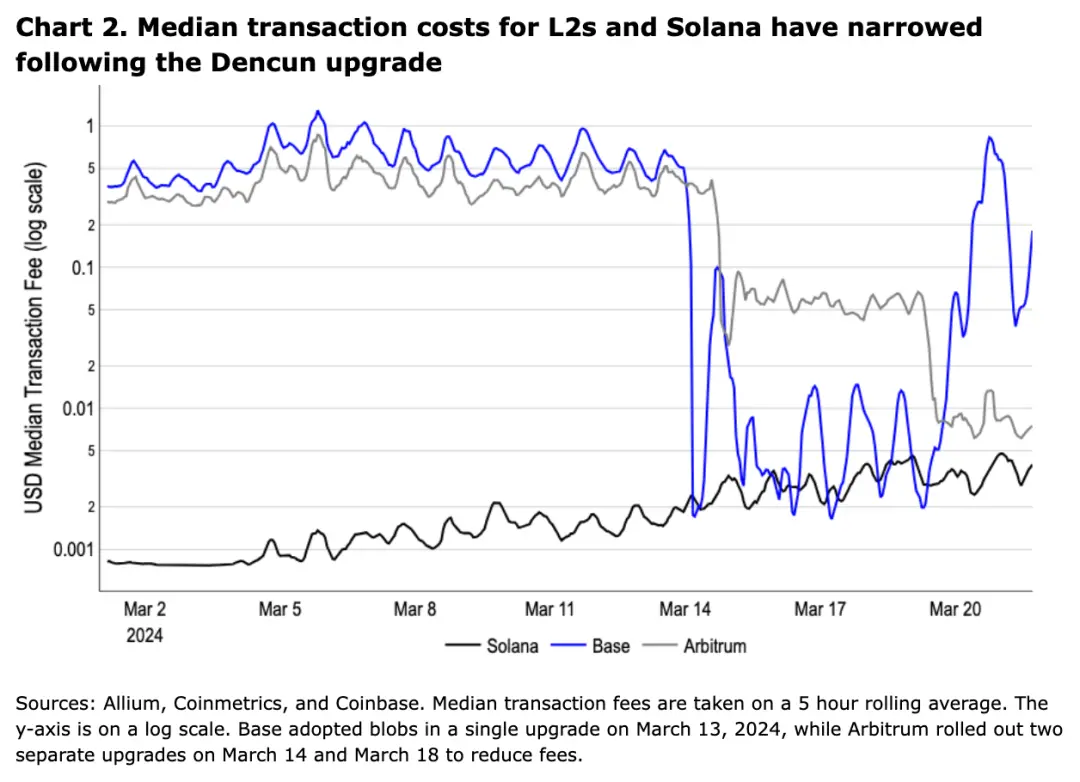

Following the meme coin frenzy and Ethereum's Dencun upgrade, there has been a surge in on-chain activity across many networks. The increase in activity is most evident on Solana and certain Ethereum Layer 2 (L2) solutions, such as Base, especially as the Dencun upgrade significantly reduced its fees. Generally, during low congestion periods, the median transaction fees on these networks have remained below $0.01 (see Figure 2).

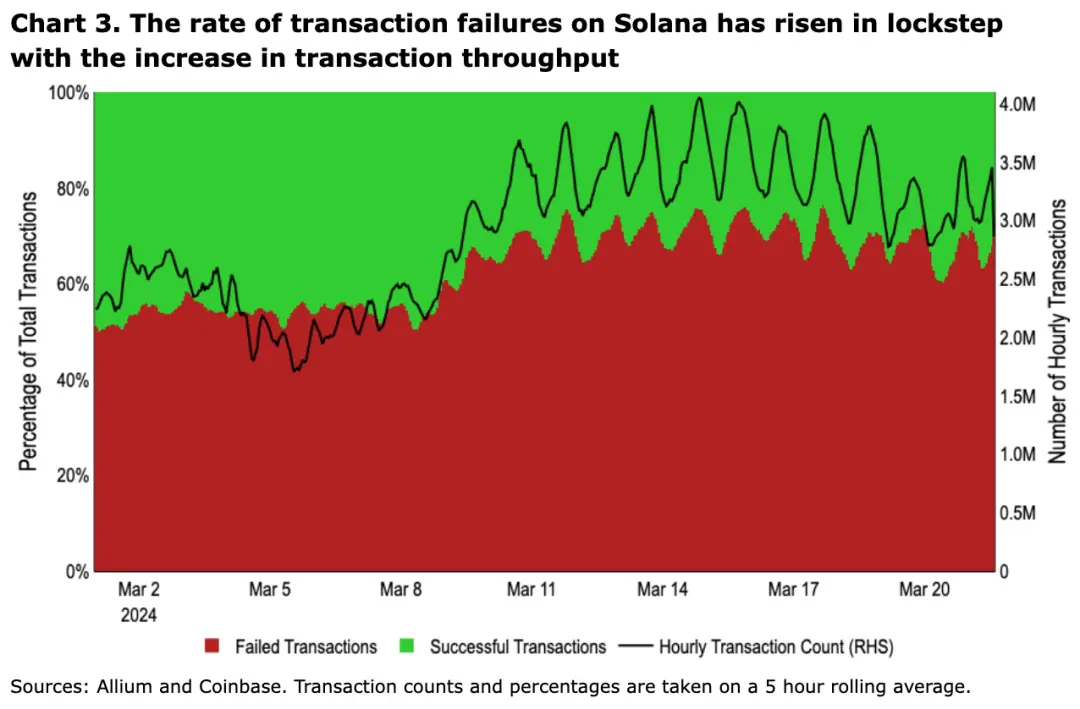

However, high transaction volumes can affect network performance in different ways. During congestion, transaction fees on Base soared to pre-Dencun levels, causing some underpriced transactions to remain pending until market fees returned to their target execution rates (unlike Solana, which does not have transaction expirations). Overall, Ethereum and its many L2s can ensure transactions are packed in block space by bidding higher than other transactions, leading to higher median transaction costs during congestion periods. In contrast, Solana, due to its lack of computation unit-based pricing (i.e., fees are not directly related to resource consumption) and absence of effective priority fee mechanisms, has been able to maintain lower median fees consistently. However, this approach incentivizes users to send spam transactions to increase the likelihood of their transactions being packed, which, as you have recently seen, has led to a significant number of dropped and failed transactions on Solana.

During high transaction volumes, if transactions are not included in a block before their block hash expires, transactions on Solana may be dropped (i.e., never included in a block). Additionally, a relatively high number of failed transactions is often due to rollbacks of on-chain smart contracts (e.g., poorly set slippage tolerances). Longer confirmation times from overloaded networks greatly increase the likelihood of prices exceeding predetermined ranges during exchange transactions, particularly for volatile and illiquid assets like meme coins. Since these occur off-chain, it is not easy to obtain precise metrics for dropped transaction counts and actual confirmation times from ledger history.

For both blockchains, their scalability roadmaps remain long, and they face different trade-offs along the paths they have taken. The Base team is considering directly increasing its chain's target capacity in the short term, as data fees remain low (the blob count per Ethereum block is still below target). The next major bottleneck focuses on optimizing execution, particularly in handling state growth. However, addressing long-term state growth issues may take some time, which could lead to sustained price spikes during congestion periods in the near future.

The v1.18 client version that Solana Labs plans to release in mid-April may also address some of their existing issues through an upgraded scheduler mechanism, although this scheduler upgrade is optional. The Solana Foundation has been pushing for a more optimized architecture, including implementing priority fees (integrating them into dapps), optimizing the use of computation units, and other mechanisms that can improve overall network performance against Sybil attacks. That said, we believe Solana's uptime during these heavy load periods demonstrates the progress the network has made over the past few years.

Crypto and Traditional Market Performance

(As of March 21, 2024, 4 PM ET)

| Asset | Price | Mkt Cap | 24 hour change | 7 day change | BTC correlation | |-------------|----------|---------|----------------|--------------|-----------------| | BTC | $65,450 | $1.28T | -0.72% | -8.39% | 100% | | ETH | $3,448 | $410B | +1.86% | -11.16% | 79% | | Gold (Spot) | $2,181 | - | -0.24% | +0.87% | 42% | | S\&P 500 | 5,241.53 | - | +0.32% | +1.77% | 16% | | USDT | $1.00 | $104B | - | - | - | | USDC | $1.00 | $31.41B | - | - | - |

| Asset | MTD flow (US$B) | YTD flow (US$B) | AUM (US$B) | Bitcoin held (BTC M) | |--------------------|-----------------|-----------------|------------|----------------------| | Spot BTC ETFs (US) | $3.9B | $11.4B | $54.4B | 0.83M |

Source: Bloomberg

Coinbase Exchange and CES Insights

The cryptocurrency market experienced significant sell-offs in the first half of this week. With no clear catalysts, many market participants attributed the weakness to the market moving too quickly and needing a correction. At the CES trading desk, buyer liquidity was skewed to the long side as traders sought to capitalize on this weakness. By midweek, sufficient leverage had been cleared from the system through liquidations and long sell-offs, bringing perpetual futures funding costs back to a more reasonable level below 20%. Cheaper funding and the dovish signals from the U.S. Federal Open Market Committee (FOMC) meeting helped trigger a relief rally in major coins and altcoins.

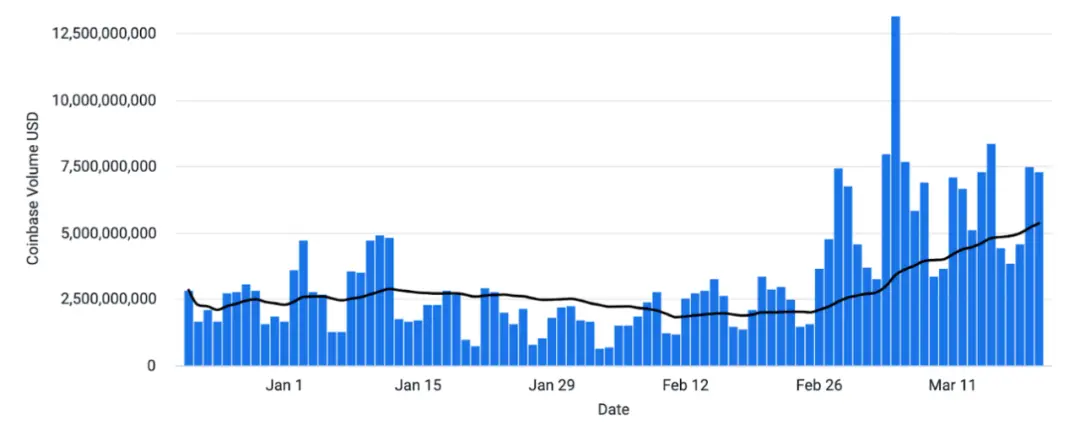

Trading volumes on Coinbase platform (USD)

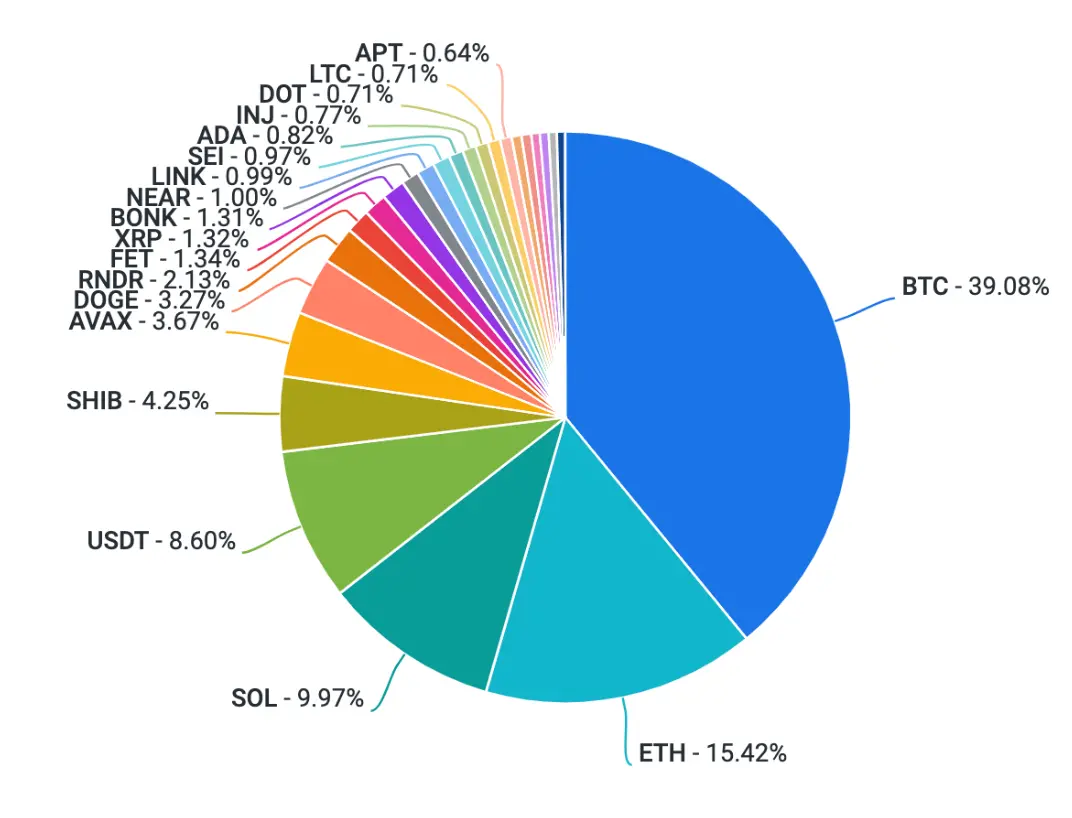

Trading volumes on Coinbase platform by asset

Funding Rates

| 3/21/2024 | TradFi | CeFi | DeFi | |-----------|--------|----------------|--------| | Overnight | 5.35% | 5.00% - 10.75% | 15.30% | | USD - 1m | 5.50% | 5.25% - 11.00% | | | USD - 6m | 5.75% | 5.50% - 11.50% | | | BTC | | 1.50% - 5.00% | | | ETH | | 3.00% - 8.00% | 1.66% |

Notable Crypto News

Institutional

- Bernstein raises Bitcoin year-end price target to $90,000 (Coindesk)

- JP Morgan states that despite recent corrections, Bitcoin remains in the "overbought zone" (The Block)

- BlackRock begins asset tokenization by launching a digital liquidity fund (Cointelegraph)

Regulatory

- SEC is conducting a deep analysis of crypto companies in the Ethereum investigation (Fortune)

General

- Bitcoin Flash plummets to $8.9 on BitMEX (Coindesk)

- Solana declared the most popular blockchain so far this year by CoinGecko Research (The Block)

Coinbase

- What is the actual use of cryptocurrency? (Coinbase Blog)

Global Outlook

Europe

- The EU has released a draft regulatory standard for stablecoin issuers, which will be part of the MICA regulatory framework (The Block)

- The UK's Financial Conduct Authority (FCA) plans to introduce market abuse rules for the cryptocurrency market this year (FCA)

Asia

- Hong Kong launches a new round of e-HKD pilot to explore the programmability and tokenization of central bank digital currency (The Block)

- South Korean cryptocurrency exchange trading volume surpasses stock market (CoinDesk)

- Japan's Government Pension Investment Fund is exploring diversification through "illiquid assets" such as BTC, gold, forests, and farmland (Bloomberg)

- Thailand approves tax exemption on token gains for personal income tax (CoinTelegraph)

- Southeast Asian super app Grab launches cryptocurrency payments in Singapore (The Block)

Major Events in the Coming Week