IOSG: Why do we invest in ether.fi? What is the future development trend of LRT?

Recently, there has been a lot of discussion around EigenLayer's restaking and LRT (Liquid Restaking Token). Users are betting on the potential airdrop expectations of various protocols, making restaking the hottest narrative in the Ethereum ecosystem. This article will briefly discuss the author's thoughts and views on LRT.

Recently, there has been a lot of discussion around EigenLayer's restaking and LRT (Liquid Restaking Token). Users are betting on the potential airdrop expectations of various protocols, making restaking the hottest narrative in the Ethereum ecosystem. This article will briefly discuss the author's thoughts and views on LRT.Author: Jiawei Zhu, IOSG Ventures

Part.1 Insight

Why do we invest in ether.fi? What is the future development trend of LRT? This article is original content from IOSG and is intended for industry learning and communication purposes only. It does not constitute any investment advice. Please cite the source if referenced, and contact the IOSG team for authorization and reprint guidelines.

Recently, there has been much discussion around EigenLayer's restaking and LRT (Liquid Restaking Token), with users betting on the potential airdrop expectations of various protocols, making restaking the hottest narrative in the Ethereum ecosystem. This article will briefly discuss the author's thoughts and views on LRT. The Underlying Logic of LRT

LRT is a new asset class derived from the multi-party market around EigenLayer. While LRT and LST share a similar goal of "liberating liquidity," LRT is more complex than LST due to the different underlying asset compositions, and it has diversity and dynamic characteristics.

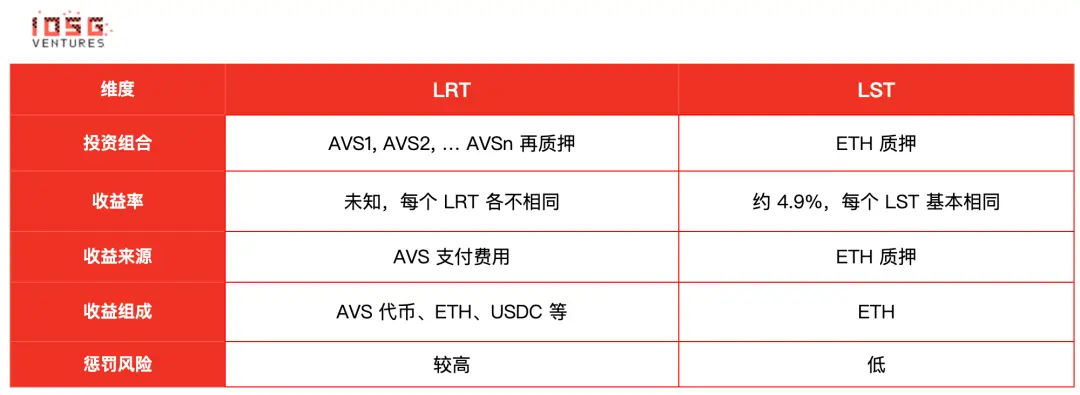

Considering ETH as the base, if Ethereum staking under LST is viewed as a money market fund, then LRT can be seen as a Fund of Fund for asset managers regarding AVS. Comparing LST and LRT is a quick way to understand the underlying logic of LRT.

Source: IOSG Ventures

- 1. Portfolio

The investment portfolio of LST consists solely of Ethereum staking, while LRT's portfolio is diverse, allowing funds to be allocated to different AVS to provide them with economic security, naturally resulting in varying risk levels. Different LRT protocols have different fund management methods and risk preferences. In terms of fund management, LST is passively managed, while LRT is actively managed. LRT may offer different management strategies corresponding to different levels of AVS (e.g., EigenDA compared to newly launched AVS) to suit users' return/risk preferences.

- 2. Yield, Sources, and Composition

The yields of LST and LRT, as well as the sources and compositions of these yields, differ:

The yield of LST currently stabilizes around 4.9%, derived from the combined earnings of Ethereum's consensus layer and execution layer, composed of ETH.

The yield of LRT is currently uncertain but primarily comes from the fees paid by various AVS, which may consist of AVS tokens, ETH, USDC, or a mix of the three. Based on our discussions with some AVS, most will reserve a few percentage points of their total token supply as incentives and security budgets. If an AVS has launched before issuing tokens, it may also pay in ETH or USDC, depending on the specific situation. (Thus, restaking can be understood as the process of re-staking ETH to mine third-party project tokens.)

Since it is AVS token-based, the risk of token volatility is greater than that of ETH, and the APR will fluctuate accordingly. AVS may also experience rotation in entry and exit situations. Such factors will introduce uncertainties to LRT's yields.

- 3. Penalty Risks

Ethereum staking has two types of penalties: Inactivity Leaking and Slashing, such as missing block proposals and double voting, with highly deterministic rules. If operated by professional node service providers, correctness can reach around 98.5%. However, LRT protocols need to trust that the AVS software is coded correctly and that there are no objections to the penalty rules to avoid triggering unexpected penalties. Due to the diversity of AVS and the fact that most are early-stage projects, this inherently carries uncertainty. Additionally, AVS may undergo rule changes as their business evolves, such as iterating more features, etc. Furthermore, from a risk management perspective, considerations must include the upgradability of AVS Slasher contracts and whether the penalty conditions are objective and verifiable. Since LRT acts as an agent managing user assets, it needs to comprehensively consider these aspects and carefully choose partners.

Of course, EigenLayer encourages AVS to undergo complete audits, including the AVS code, penalty conditions, and the logic of interaction with EigenLayer. EigenLayer also has a multi-signature veto committee to conduct final reviews and oversight of penalty events.

Rapid Growth of LRT in the Short Term

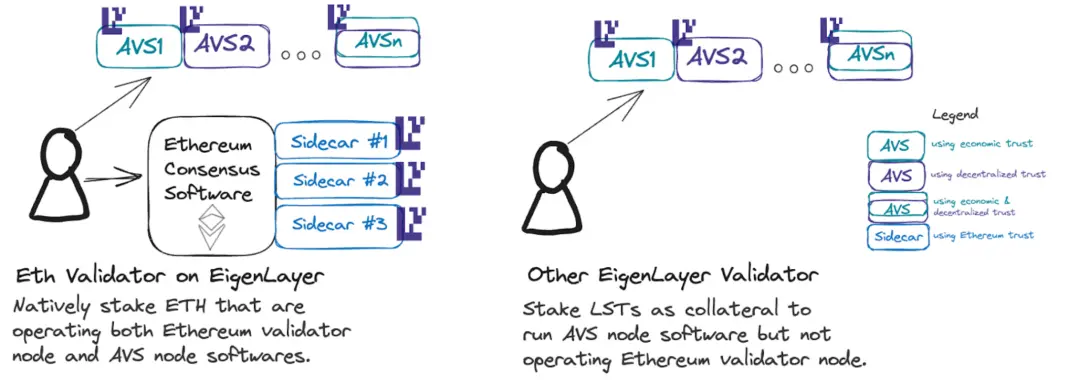

Source: EigenLayer EigenLayer adopts a phased approach to the restaking of LST, while there are no restrictions on Native Restaking. Limiting LST may be a form of hunger marketing, but more importantly, it promotes the growth of Native Restaking. After the restriction on LST, users wishing to restake can only turn to third-party LRT protocols for Native Restaking, which greatly promotes the development of LRT protocols. Currently, ETH flowing into EigenLayer through LRT accounts for about 55% of EigenLayer's total TVL. Additionally, an implicit point is that Native Restaking can provide Ethereum Inclusion Trust, which is a third trust model offered and advocated by EigenLayer, in addition to Economic Trust and Decentralization Trust. This means that Ethereum validators can not only commit to Ethereum through staking but also run AVS and make commitments to AVS. Most of these commitments are related to MEV. One use case is "future block space auctions." For example, oracles may need to provide price feeds during specific time periods; or L2 may need to publish data to Ethereum every few minutes, etc., and they can pay proposers to reserve future block space.

The Competitive Landscape of LRT

First, to make the liberated liquidity useful, the integration of DeFi is a major point of competition among LRT protocols.

As mentioned above, while theoretically AVS needs to calculate the economic security required to reach a certain security threshold, most AVS currently incentivize by taking a portion of their total token supply. Due to the rotation and entry/exit of different AVS, incentives depend on the price of AVS tokens, making the uncertainty of LRT assets much greater than that of LST (LST has a stable "Risk-free rate" and good expectations for ETH prices), making it difficult to become a "hard currency" like stETH in mainstream DeFi protocol integration and compatibility.

After all, as a staking protocol, the liquidity and TVL of LRT will be the primary criteria of concern for DeFi protocols, followed by brand, community, etc. Liquidity is primarily reflected in the exit time cycle. Generally speaking, exiting from EigenPod takes seven days, and subsequently exiting from Ethereum staking also requires some time. Protocols with larger TVLs can establish better liquidity; for example, the Liquidity Pool Reserve operated by Etherfi can provide quick withdrawals (i.e., eETH -> ETH).

However, it is still early to discuss the integration of mainstream DeFi before the mainnet of EigenLayer goes live, as many factors remain unknown.

On another note, recently Ether.fi tweeted about the meme token $ETHFIWIFHAT to create buzz for the token launch, sparking imagination. Swell is using Polygon CDK, EigenDA, and AltLayer to build zkEVM L2, with its LRT rswETH as the Gas token. Renzo is focusing on multi-chain integration on Arbitrum, Linea, and Blast. It is believed that various LRT protocols will subsequently launch their differentiated strategies.

However, whether LST or LRT, the degree of homogeneity is relatively high. Although LRT has more room for maneuver compared to LST, even if an LRT launches a new idea to the market, competitors have the capability to imitate. The author believes that the moat lies in consolidating and enhancing TVL and liquidity. Etherfi currently has the highest TVL and best liquidity; assuming all LRT protocol airdrop expectations are fulfilled, Etherfi will have a greater advantage in attracting new funds. (In this regard, the adoption of institutional users should not be overlooked, as 30% of Etherfi's TVL comes from institutional users.)

After the airdrop events conclude, the landscape of LRT could very well be reshuffled, with competition among LRT protocols for users and funds becoming more intense (for example, after Etherfi's airdrop distribution, some funds may immediately flow to other platforms). Before EigenLayer fully launches its mainnet and AVS begins to provide yields, LRT's stickiness to users is not very strong.

Sustainability of LRT

The sustainability of LRT can actually be viewed as the sustainability of the EigenLayer system, as the yields from Ethereum staking will always exist, while AVS may not. A frequently asked question is: with the current TVL of 11 billion, how can EigenLayer provide matching yields (e.g., 5% annually)? The author believes there are several points:

Although EigenLayer's TVL reached 11 billion before the full launch of the mainnet, even surpassing AAVE, there will certainly be a period of mean reversion correction after the airdrops of a series of related protocols conclude. Overall, the yields to consider in the short term do not need to be that high.

Secondly, the yields, durability, and volatility provided by each AVS token differ, and each staker's risk preferences and pursuit of returns also vary. In this process, there will also be spontaneous market dynamics (more ETH staked to a certain AVS will decrease the yield, prompting stakers to turn to other AVS or other protocols), so it cannot simply be calculated using a percentage of the entire TVL.

From a medium to long-term perspective, the driving force for the sustainable development of the EigenLayer ecosystem lies in the demand side, meaning there needs to be enough AVS to pay for economic security, and it must be sustainable, which is also related to the quality of the AVS's own business. Currently, apart from AltLayer and 12 other early AVS partners, a series of AVS have already announced collaborations. The author has learned that dozens of AVS are waiting in line for integration. Of course, this is also related to the quality of the AVS projects, the performance of the tokens, and the design of incentive mechanisms, and it is currently impossible to provide definitive comments.

Summary

Finally, regarding the future landscape of LRT, the author has the following views:

Despite the intense competition, LRT remains the preferred direction for investment layout in the primary market of the EigenLayer ecosystem. When investing in AVS within EigenLayer, the investment logic should consider the middleware's investment logic, which does not change simply because it uses EigenLayer to launch the network; it is just a different way of implementing the product. In the future, there may be dozens or even hundreds of AVS built on EigenLayer, so the concept of AVS is not rare. The direction of node service providers has already been firmly occupied by some mature companies. LRT is clearly closer to users, serving as an abstraction layer between users and EigenLayer, possessing both Staking and DeFi attributes, and having a greater voice in asset allocation within the ecosystem. In the overall layout of the EigenLayer ecosystem, we also focus on developer tools, anti-slashing key management, risk management, public goods, and other areas.

Currently, the proportion of participation in EigenLayer restaking through LRT and LST is approximately 55% and 45%. We expect that as EigenLayer gradually develops, the advantages of LRT in unlocking liquidity will become apparent, and this ratio may reach around 70-30 (assuming some conservative whales and institutions holding stETH still choose to passively hold stETH). Of course, the risks of LRT should not be overlooked; due to the nested asset structure, we also need to be cautious of systemic risks such as depegging in extreme market conditions. In the long run, we hope to see AVS in the EigenLayer ecosystem thrive, providing LRT with a relatively stable underlying structure and yield.

Part.2 Progress of IOSG's Post-Investment Projects

DAO Maker announces expansion to Solana network, set to launch 4 Solana IDO projects

* Market Maker

DAO Maker tweeted about its expansion to the Solana network, adding a $2 million SOL liquidity pool on Raydium, and is set to launch 4 Solana IDO projects, with YOURAI going live on Raydium next Tuesday.

Cosmos ecosystem project Saga adds CryptoPunks and BAYC holders as airdrop recipients

* Protocol

The Cosmos scalability protocol Saga tweeted that it has added CryptoPunks and BAYC holders as recipients of the SAGA token airdrop.

Arbitrum plans to invest $400 million to promote blockchain games

* Layer2

The Arbitrum Foundation announced plans to invest 200 million ARB (approximately $400 million) over the next two years to promote gaming projects on its blockchain. The new proposal suggests allocating the majority of the funds (160 million ARB) to incentivize publishers and developers to create new games on Arbitrum, with an additional 40 million ARB to support infrastructure projects, such as creating "tools needed to support games within Arbitrum." The Arbitrum Foundation will seek approval from its DAO for this plan. Arbitrum: ArbOS "Atlas" has launched, blobs are now effective

* Layer2

ArbOS "Atlas" has launched, and blobs are now effective, reducing the cost of data publishing. Additional gas reductions for Arbitrum One will go live on March 18.

EigenLayer will continue to adopt a phased approach to launch the mainnet in the coming weeks

* Restaking

EigenLayer posted about the mainnet launch, announcing that it will continue to adopt a phased approach to launch the mainnet starting now and over the next few weeks. Key steps include the final migration of the testnet, pausing web applications and contracts, gradual operator registration, launching EigenDA, and completing the mainnet launch, followed by the emergence of the AVS ecosystem.

Coinbase International to launch dYdX on the Cosmos network

* Layer1

Coinbase International Exchange will add support for dYdX on the Cosmos network, with updates on launching COSMOSDYDX-USDC transfers and trading to be provided in the coming weeks.

Swell Network to launch its L2 rollup chain, plans to launch mainnet in the second half of this year

* Restaking

The liquidity re-staking protocol Swell Network will launch its Layer 2 rollup chain and plans to launch the mainnet in the second half of this year. This Layer 2 network utilizes the "restaked rollup" framework developed by AltLayer, differing from traditional Layer 2 designs, and is developed using Polygon's chain development kit (CDK) with support from AltLayer. This network aims to provide Swell users with benefits such as native re-staking yields, better scalability, and lower fees. The upcoming token from Swell will be used for governance.

Derivatives network Vega partners with EigenLayer to create a crypto points derivatives market

* Restaking

Derivatives network Vega has established a derivatives market for crypto points, initially partnering with EigenLayer. This market aims to allow users to hedge the value of their points. Points are typically used in airdrops, based on participation in activities, and may eventually convert into tokens. The new market offered by Vega supports permissionless market creation, allowing anyone to open trading markets for any points project.

Polkadot plans to launch Agile Coretime in the next version, has now launched the Polkadot Alpha program

* Restaking

Polkadot announced the launch of the Polkadot Alpha program ahead of Agile Coretime, aimed at helping more teams turn blockchain ideas into projects. The Polkadot Alpha program will be open to teams at various stages of development, including: parachain teams, infrastructure providers, and Dapp teams, with applications currently open. Previously, Parity developer Joyce announced on the Polkadot forum that Agile Coretime will be launched in the next runtime version (Polkadot 1.2.0) and will undergo OpenGov voting for launch on Kusama.