Cancun upgrade completed, LRT track catalyzing Ethereum ecosystem?

Is Liquid Restaking a catalyst for the Ethereum ecosystem or, as many say, a Ponzi scheme?

Is Liquid Restaking a catalyst for the Ethereum ecosystem or, as many say, a Ponzi scheme?With the completion of the Cancun upgrade, the prices of Ethereum and its related ecosystem tokens have recently performed well. At the same time, modular concept projects and Ethereum Layer 2 projects have successively launched their mainnets, further boosting the current market's optimism towards the Ethereum ecosystem. The narrative of Liquid Restaking has also begun to attract capital attention due to the explosive popularity of the EigenLayer project.

However, is the transition from ETH -> LST → LRT a catalyst for the Ethereum ecosystem, or is it just a nested structure as many people say?

This research report provides a detailed explanation of the current situation, opportunities, and future of the LRT track ecosystem. Currently, many LRT protocols have not issued tokens, and there is significant project homogeneity. However, the most promising projects are KelpDAO, Puffer Finance, and Ion Protocol, which have distinct development paths compared to other LRT protocols. The future of the LRT track remains a rapidly growing niche market. Huobi Research Institute predicts that only a few leading projects will emerge in the future.

This presentation was written by the Research team under HTX Ventures. HTX Ventures is the global investment arm of Huobi HTX, integrating investment, incubation, and research to identify the best and most promising teams globally.

Background of the LRT Track

Due to the approaching Cancun upgrade, the prices of Ethereum and its related ecosystem tokens have recently performed well. At the same time, modular concept projects and Ethereum Layer 2 projects have successively launched their mainnets, further boosting the current market's optimism towards the Ethereum ecosystem.

Liquid staking projects occupy a significant share in the Ethereum ecosystem, while another narrative—re-staking—has begun to attract capital attention due to the explosive popularity of the EigenLayer project.

The concept of "re-staking" was first proposed by Eigenlayer in June 2023. It allows users to re-stake already staked Ethereum or liquid staking tokens (LST) to provide additional security for various decentralized services on Ethereum and earn extra rewards. Based on the re-staking services provided by Eigenlayer, projects related to Liquid Restaking Tokens (LRT) have emerged.

Is LRT a Nested Structure? Let's Look at the Evolution Path of LRT

LRT, or Liquid Restaking Tokens, refers to a "re-staking certificate" obtained after staking LST.

So,

How is this re-staking certificate LRT born?

Is the transition from ETH -> LST → LRT really a nested structure as many people say?

This requires tracing back the evolution path of LRT.

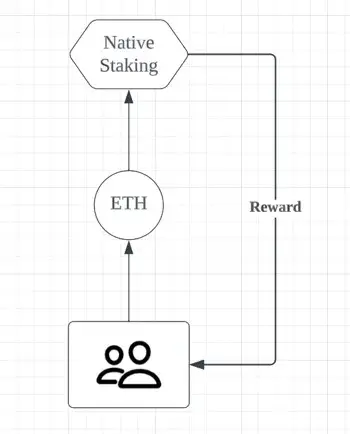

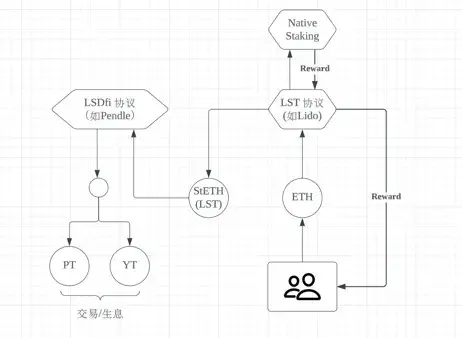

Phase 1: Native Staking on Ethereum

After Ethereum upgraded to the PoS mechanism, to maintain the security of the Ethereum network, miners' identities transformed into validators, responsible for storing data, processing transactions, and adding new blocks to the blockchain, earning rewards in the process. To become a validator, one must stake at least 32 ETH and have a dedicated computer connected to the internet year-round.

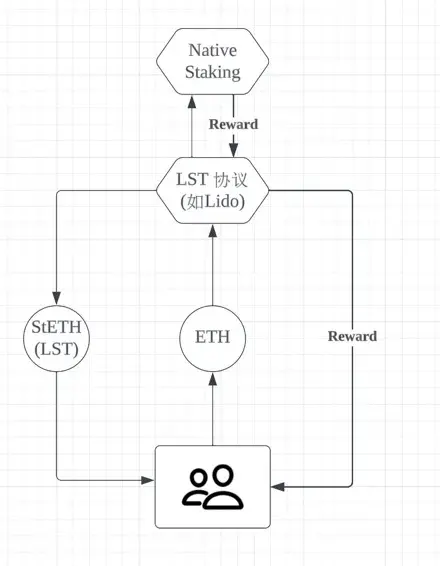

Phase 2: Birth of LST Protocols

Due to the official staking requirement of at least 32 ETH and the inability to withdraw for a considerable period, staking platforms emerged to address two main issues:

Lowering the threshold: For example, Lido allows staking any amount of ETH without technical barriers.

Releasing liquidity: For instance, staking ETH on Lido yields stETH, which can participate in DeFi or be exchanged for ETH at an approximate equivalent.

In simple terms, it's like "group buying."

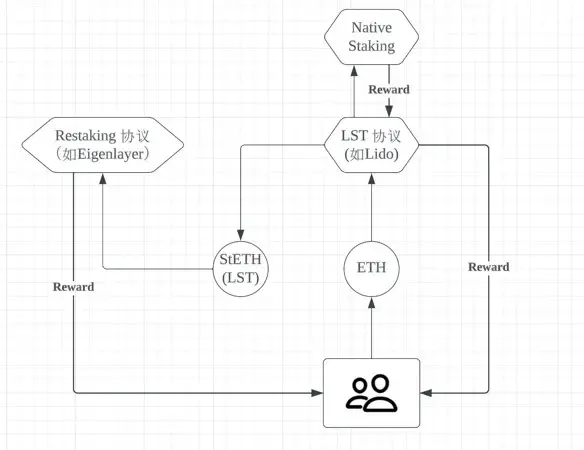

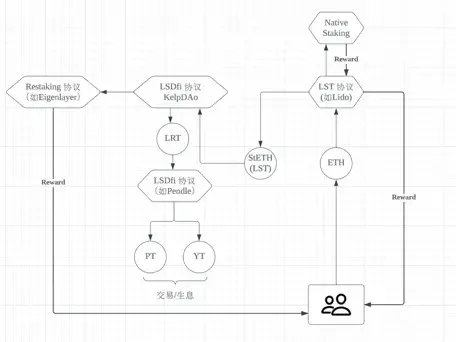

Phase 3: Birth of Restaking Protocols

With the development of the Ethereum ecosystem, it became apparent that liquid staking token assets (LST) could be staked on other networks and blockchains to earn more returns while also contributing to the security and decentralization of the new networks.

The most representative project is Eigenlayer, whose re-staking logic mainly consists of two parts. First, it shares security within the ETH ecosystem, and second, users seek higher returns.

Re-staking can share security with sidechains and middleware (DA Layer/bridges/oracles, etc.), further maintaining the network security of Ethereum. Security sharing allows a blockchain to enhance its own security by sharing the value of validation nodes from another blockchain.

From the user's perspective, it's about staking for returns and re-staking for even more returns.

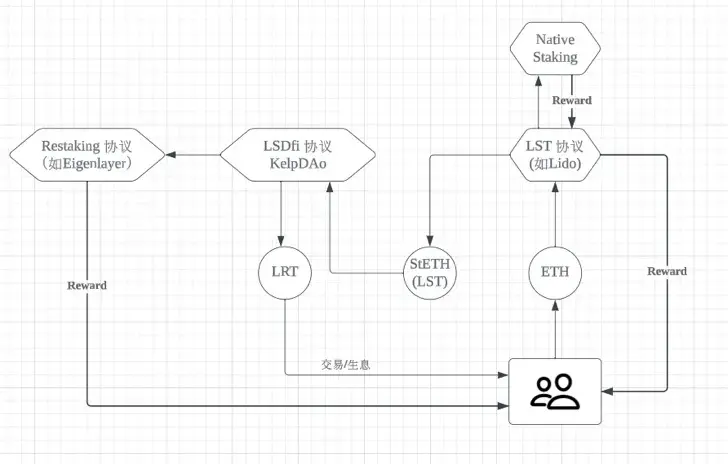

Phase 4: Birth of LRT

With the introduction of re-staking protocols, it was discovered that LST could be re-staked to earn interest, but once LST tokens were staked, their liquidity seemed to be locked. At this point, some projects identified an opportunity to help users place LST assets into re-staking protocols to earn returns while issuing a "re-staking certificate" that users could use for more financial operations, such as collateral and lending, to resolve the liquidity lock issue in re-staking. This "re-staking certificate" is LRT.

Phase 5: Pendle Protocol Boosting the Explosion of LRT

Once users obtain LRT, they may want to perform a series of financial operations. So where should these LRT go, and what financial operations should be conducted? At this point, Pendle provides a very clever solution.

Pendle is a decentralized interest trading market that offers trading of PT (Principal Token) and YT (Yield Token).

With the emergence of yield-bearing dollars and the recent liquid restaking tokens (LRT), the types of yield-bearing tokens have gradually expanded, allowing Pendle to continuously iterate and support yield trading for these cryptocurrencies. Pendle's LRT market is particularly successful because it essentially allows users to pre-sell or position for long-term airdrop opportunities (including EigenLayer). These markets have quickly become the largest on Pendle and are far ahead:

Through the customized integration of LRT, Pendle allows Principal Tokens to lock in base ETH yields, EigenLayer airdrops, and any airdrops related to the re-staking protocols issuing LRT. This creates an annual yield of over 30% for Principal Token purchasers.

On the other hand, due to the way LRT is integrated into Pendle, Yield Tokens allow for a form of "leveraged point farming." Through Pendle's exchange function, we can swap 1 eETH for 9.6 YT eETH, accumulating EigenLayer and Ether.fi points as if holding 9.6 eETH.

In fact, for eETH, Yield Token purchasers can also earn double points from Ether.fi, which is essentially "leveraged airdrop farming."

Using Pendle, users can lock in airdrop yields valued in ETH (based on market expectations for EigenLayer and LRT protocol airdrops) and engage in leveraged liquidity mining. Given the speculation surrounding potential airdrops to LRT holders this year, Pendle is likely to continue dominating this market segment. In this sense, $PENDLE provides a good risk exposure for the success of LRT and EigenLayer in vertical fields.

Summary:

The above text explains how LRT was born. So,

Is the transition from ETH -> LST → LRT really a nested structure as many people say?

The answer to this question needs to be discussed on a case-by-case basis.

If, within a single DeFi ecosystem, staking LST generates a re-staking certificate, then that certificate is staked again, and a governance token is issued under the pretext of locking liquidity, allowing the secondary market to speculate and feed back the expected value of re-staking, this is indeed a nested structure. Because allowing the next level of funds to feed back into the previous level of assets overdraws the market's expectations for a token, without any real value growth occurring.

Now let's look at the classic re-staking model centered around Eigenlayer + Pendle.

Through Eigenlayer,

Users repeatedly stake LSD to EigenLayer.

The repeatedly staked assets are provided to AVS (Actively Validated Services) for protection.

AVS provides validation services for application chains.

Application chains pay service fees. The fees are divided into three parts, distributed as staking rewards, service income, and protocol revenue to stakers, AVS, and EigenLayer.

Through Pendle,

Users can lock in airdrop yields valued in ETH (based on market expectations for EigenLayer and LRT protocol airdrops).

Leveraged liquidity mining.

LRT, as a yield-bearing asset, has excellent application scenarios.

The essence of this model is to share the security of Ethereum, and projects that share security through this mechanism need to pay for the service, resulting in positive capital inflow into the ecosystem. This is definitely not a nested structure but a very reasonable economic model.

In simple terms, the core driving force behind the launch of this round of LRT narrative has two key conditions:

The yield-generating ability of the underlying assets of LRT.

The application scenarios of LRT.

Firstly, the yield-generating ability of the underlying assets of LRT is provided by Eigenlayer, including Eigenlayer's airdrops and its utility service income, which will be detailed further below.

Secondly, the application scenarios of LRT are well exemplified by Pendle.

In the following text, we will focus on introducing Eigenlayer, the most core project of re-staking, and summarize other LRT projects.

Ecosystem Situation of the LRT Track (Key Introduction)

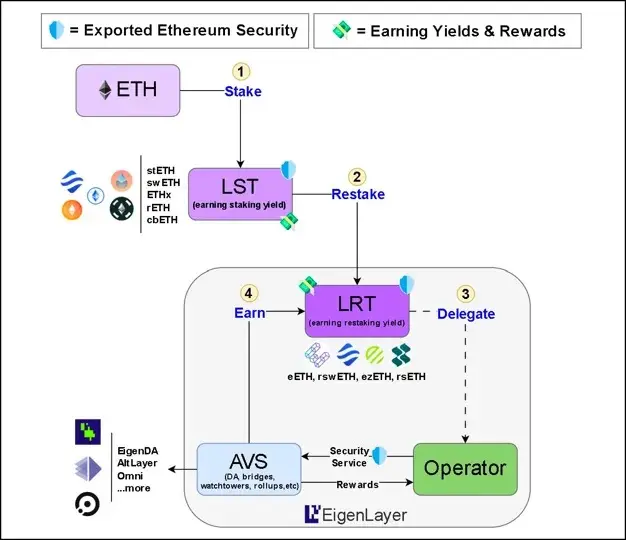

EigenLayer - Re-staking Middleware

Introduction to EigenLayer

EigenLayer is a re-staking collective on Ethereum, a set of middleware in smart contracts on Ethereum that allows stakers of the consensus layer Ether (ETH) to choose to validate new software modules built on the Ethereum ecosystem.

EigenLayer effectively paves the way for expressive innovation in the Cosmos stack for L2 mining by providing an economic rights platform that allows any staker to contribute to any PoS network. By lowering costs and complexity, EigenLayer is "renting" economic security from existing stakers on Ethereum to provide security for multiple applications.

In summary: EigenLayer allows re-stakers to participate in validating different networks and services through a set of smart contracts, saving costs for third-party protocols while enjoying Ethereum's security, providing multiple returns and flexibility for re-stakers.

Product Mechanism

For middleware projects, EigenLayer can help them achieve rapid cold starts for networks, even if they later issue their own tokens, they can switch to a self-token-driven model. EigenLayer acts as a security service provider. For DeFi, various derivatives can be built based on EigenLayer.

- EigenLayer's product logic in the entire LST/LRT ecosystem

- User flowchart through EigenLayer

Detailed Explanation of EigenLayer AVS

Another important new concept in EigenLayer is AVS (Actively Validated Services).

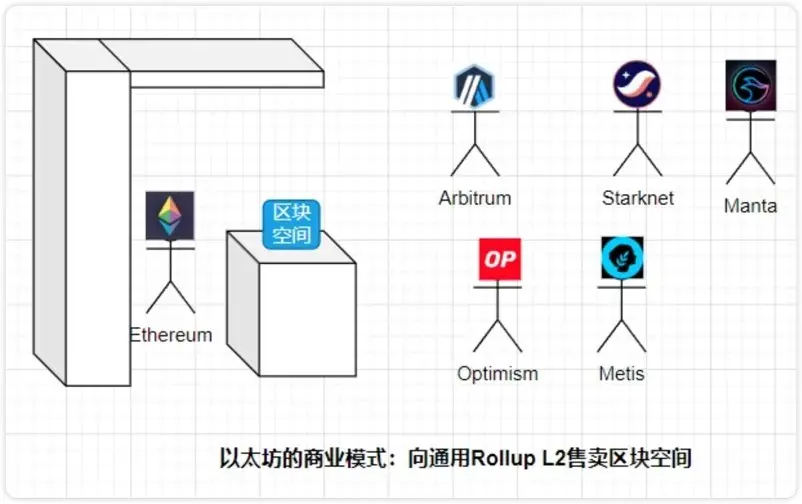

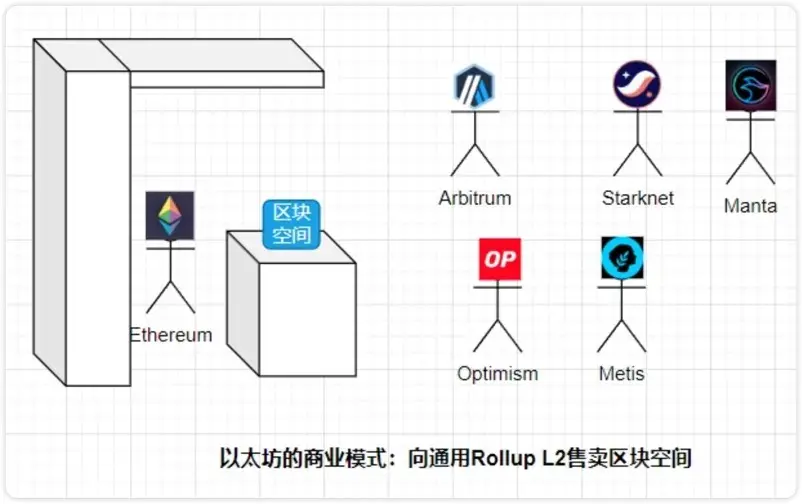

Restaking is easy to understand, but AVS is a bit complex. To understand EigenLayer's AVS, one must first understand Ethereum's business model. If we observe the relationship between the Ethereum mainnet and Ethereum ecosystem Rollup L2s from a business perspective, Ethereum's current business model is to sell block space to general Rollup L2s.

Image Source: Twitter 0x Ning 0x

General Rollup L2s pay GAS to package L2's state data and transactions, verifying availability through the smart contracts they deploy on the Ethereum mainnet, and then storing it on the Ethereum mainnet in the form of calldata, which is finally ordered and included in blocks by Ethereum's consensus layer. The essence of this process is that Ethereum actively verifies the consistency of Rollup L2 state data.

EigenLayer's AVS simply abstracts this specific process into a new concept—AVS.

Now let's look at EigenLayer's business model. It abstracts and encapsulates the economic security of Ethereum's PoS consensus through re-staking into a "lite version" (low-spec model), thus weakening consensus security but also reducing costs.

Because it is a lite version of AVS, its target market is not general Rollup L2s with very high consensus security requirements, but various Dapp Rollups, oracle networks, cross-chain bridges, MPC multi-signature networks, trusted execution environments, etc., which have lower consensus security needs. Isn't this a perfect Product Market Fit (PFT)?

Image Source: Twitter 0x Ning 0x

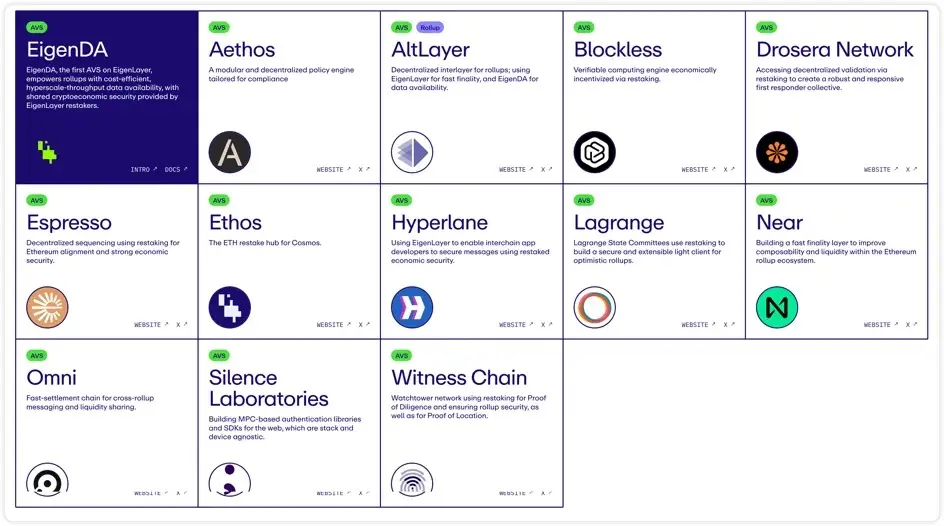

AVS Active Validation Service Provider Projects

Currently, there are about 13 AVS projects incorporated into EigenLayer, and more AVS service providers are joining through EigenLayer's Dev documentation. These projects are highly tied to the RaaS concept, mostly serving the security, scalability, interoperability, and decentralization of Rollup projects, with some extending to the Cosmos ecosystem.

Among them, we are familiar with EigenDA, AltLayer, Near, etc. Below, we list the characteristics of AVS-related projects.

Ethos: Ethos primarily bridges Ethereum's economic security and liquidity to Cosmos. Cosmos Consumer chains typically use native staking tokens to ensure network security. Although ATOM staking provides some cross-chain security (ICS), Ethos is connecting Ethereum's economic security and liquidity with Cosmos. Ethos is inspired by Mesh Security (allowing the use of another chain's staking tokens on one chain), thereby enhancing economic security without needing additional nodes. The benefit of this structure is that ETHOS is likely to receive token airdrops (and income) from partner chains. Meanwhile, ETHOS tokens will also be airdropped to ETH re-stakers on Eigenlayer.

AltLayer: A new project launched in collaboration with Eigenlayer, Restaked rollup introduces three types of AVS: 1) fast finality; 2) decentralized ordering; 3) decentralized validation. The token economics of ALT is very clever, as it requires staking ALT alongside re-staked ETH to protect these three AVS.

Espresso: Espresso focuses on decentralized Layer 2 ordering. AltLayer has actually integrated Espresso, allowing developers deploying on the AltLayer stack to choose between using AltLayer's decentralized validation solution and Espresso Sequencer.

Omni aims to integrate all Ethereum Rollups. Omni introduces a "unified global state layer" protected through EigenLayer's re-staking. This state layer integrates cross-domain management of applications.

Hyperlane aims to connect all Layer 1 and Layer 2. Using Hyperlane, developers can build cross-chain applications, and Hyperlane Permissionless Interoperability allows Rollups to connect to Hyperlane without cumbersome governance approvals.

Blockless adopts a network-neutral application (nnApp) that allows users to run a node while using the application, contributing resources to the network. Blockless will provide a network for EigenLayer-based applications to minimize accidental slashing.

Other noteworthy AVS projects:

Lagrange: A competitor to LayerZero, Omni, and Hyperlane, its cross-chain infrastructure can create universal state proofs across all major blockchains.

Drosera: An "event response protocol" to contain vulnerabilities, which detects and acts to mitigate vulnerabilities when a hacking attack occurs.

Witness Chain: Uses re-staking functionality for Proof of Diligence to ensure Rollup security, as well as Proof of Location to establish physical node decentralization.

Summary of EigenLayer Product Features

The product features of EigenLayer can be summarized as follows:

EigenLayer is a "super connector," linking Staking, infrastructure middleware, and DeFi across three major sectors.

EigenLayer plays a bridging role in Ethereum re-staking, extending the security of Ethereum's crypto economy. The market demand and supply for EigenLayer are very solid.

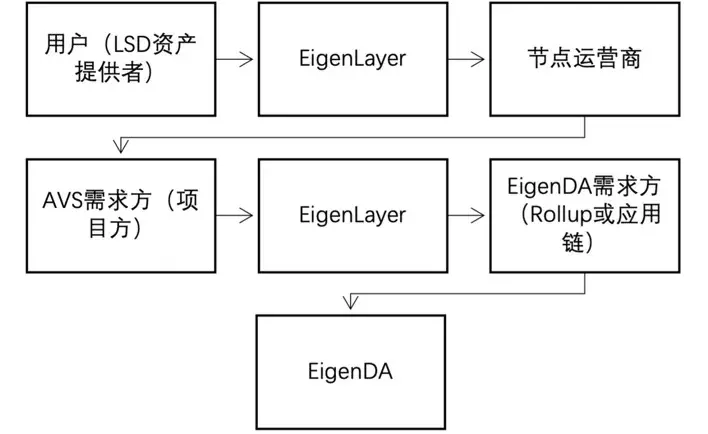

EigenDA is a pioneering exploratory version of the scaling solution Danksharding under Ethereum's Rollup-centric Roadmap. In simple terms, it's the "youth version of sharded storage."

EigenLayer Ecosystem Related Projects

Overview of Ethereum LRT Projects

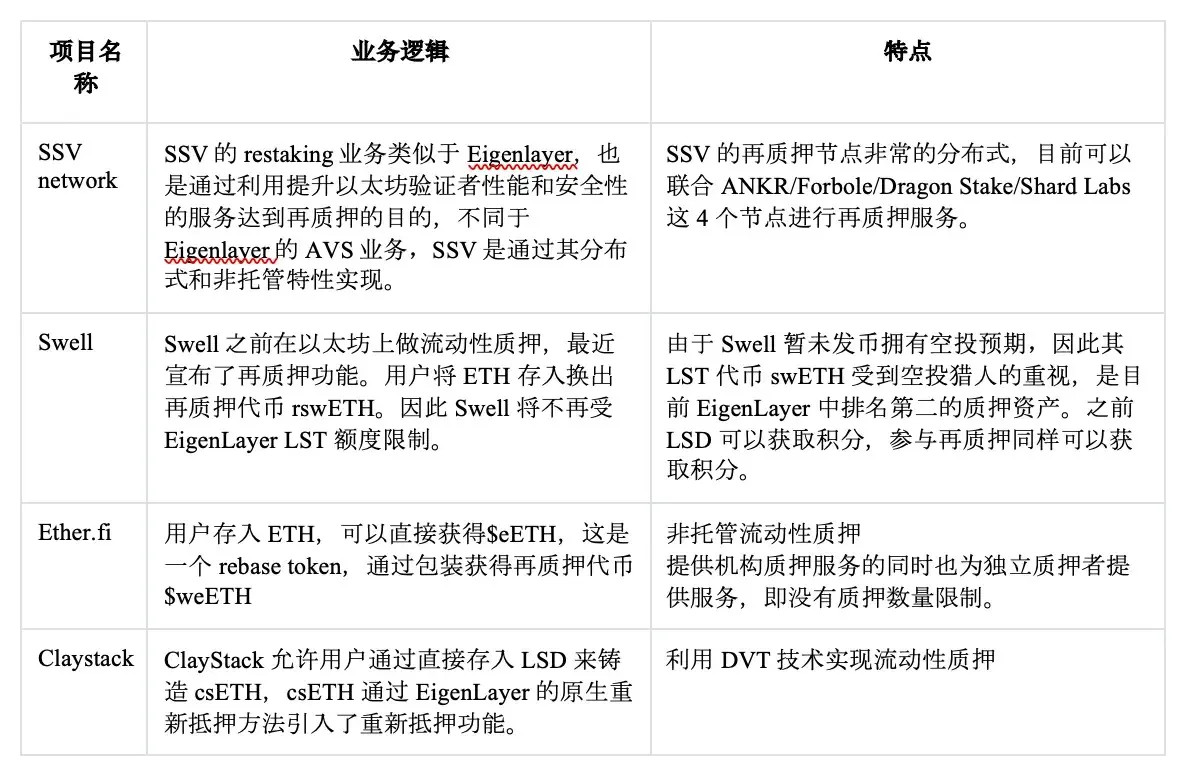

Currently, there are about 15 LRT protocols on Ethereum, with 9 already launched and 6 still in testing. Most LRT protocols rely on Eigenlayer to obtain re-staking yields and can be divided into three main categories:

Liquid-LSD Restaking: This type involves managing users' staked LST uniformly in external re-staking protocols like Eigenlayer, where users receive collateral certificate tokens called Liquid Restaking Tokens (LRT) (protocols include KelpDAO, Restake Finance, Renzo). This type of protocol suffers from significant homogeneity, with limited technology and innovation.

Liquid Native Restaking: Native liquid re-staking refers to projects like etherf.fi or Puffer Finance that provide small ETH node services, staking the ETH within the node to EigenLayer for re-staking.

Protocols that optimize on the basis of the Eigenlayer protocol, providing security and validation services while also conducting LRT business (protocols include SSV). The development of these protocols mainly depends on their competitive relationship with Eigenlayer, needing to find breakthroughs to attract nodes.

Most LRT protocols will innovate their mechanisms based on three points:

Providing stronger security than Eigenlayer;

Eigenlayer has allocation strategy issues: As the number of AVS increases, re-stakers need to actively choose and manage allocation strategies for operators, which will be extremely complex. LRT protocols will offer users the best allocation strategy solutions.

EigenLayer's LST deposits have a cap, while native ETH deposits currently have no limits, but most users find it difficult to obtain them, as they require users to have 32 ETH and run an Ethereum node integrated with EigenLayer to operate EigenPods. Some LRT protocols will lift this restriction.

Specific projects and their situations are as follows:

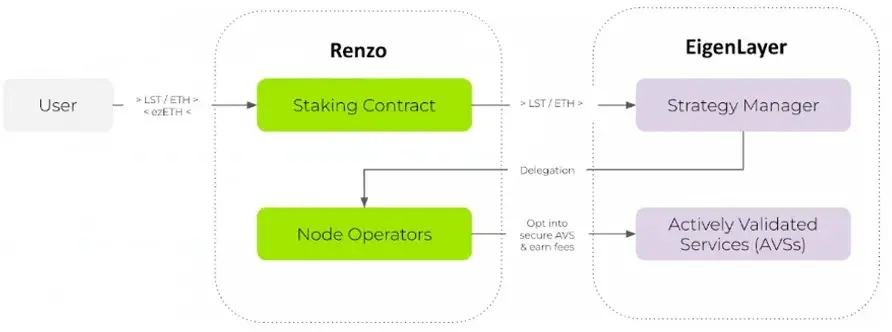

Renzo

Renzo has optimized on Eigenlayer, abstracting the complex process of re-staking for end users, so re-stakers do not have to worry about actively choosing and managing operators and reward strategies. It helps users build portfolios to invest in higher-yield AVS allocation strategies. Additionally, there is no upper limit on the amount of tokens deposited in Renzo, which has become one of the main factors for Renzo's TVL surge.

Funding Situation: Announced completion of $3.2 million seed round financing in January, led by Maven 11, with participation from SevenX Ventures, IOSG Ventures, OKX Ventures, and others.

Business Logic:

Users stake ETH or LST into the Renzo protocol and receive an equivalent value of $ezETH;

Renzo stakes LST into Eigenlayer's AVS nodes, but Renzo adjusts the weight of the LST staked on the nodes to achieve optimal returns.

Current Status: Tokens have not yet been issued; $ezETH belongs to its LRT token. Due to its re-staking yields, its price is higher than ETH, with 217,817 minted and a TVL of $777.7 million. Regarding fees, they will be charged appropriately based on re-staking yield conditions. Community situation: Currently, it has 51.7K followers on Twitter.

KelpDAO

KelpDAO is an LRT project supported by Stader Labs, with a business model similar to Renzo. Unlike Renzo, KelpDAO offers a withdrawal method for rsETH that allows redemption of $rsETH at any time through an AMM liquidity pool, while Renzo requires over 7 days.

Business Logic:

Users deposit stETH and other LST into the Kelp protocol to exchange for rsETH tokens, and the Node Delegator contract stakes LST into Eigenlayer's Strategy Manager contract.

KelpDAO interacts with EigenLayer, allowing users to earn EigenLayer points through re-staking while also extracting liquidity to use LRT for earning, while enjoying the yield from LST.

Current Status: Tokens have not yet been issued; TVL is $718.76 million, performing better than Restaking Finance. The protocol does not charge any fees, which is currently a significant advantage for KelpDAO. Community data: 23.6K followers on Twitter, with limited interaction.

Restake Finance ($RSTK)

RSTK is the first modular liquid re-staking protocol on EigenLayer, helping users place LST into Eigenlayer projects. The overall business logic lacks innovation or competitiveness. The token economic model does not offer much novelty. The token price saw a significant rise for a period due to the popularity of the re-staking concept and Eigenlayer projects but has recently performed poorly.

Business Logic:

Users deposit LST generated from liquid staking into Restake Finance;

The project helps users stake their LST into EigenLayer and allows users to generate reaked ETH (rstETH) as a re-staking certificate;

Users take rstETH to various DeFi platforms to earn returns while also earning EigenLayer reward points (considering EigenLayer has not yet issued tokens).

Token Functions:

Governance

Staking to receive protocol income dividends.

Current Status: TVL reached $15.5 million, with 4,090 rstETH in circulation and over 2,500 unique addresses, with more than 750 users. Community data: 12.8K followers on Twitter, with limited interaction.

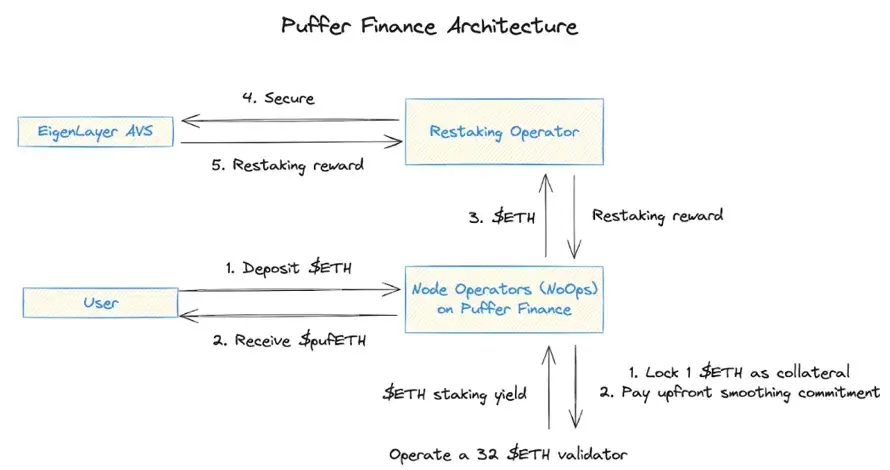

Puffer Finance

Due to investment from Binance Labs, Puffer has recently gained popularity. Puffer Finance is a liquid staking protocol that prevents slashing and belongs to the Liquid Native Restaking category. Puffer Finance has raised a total of $6.15 million in seed funding led by Jump Crypto. Puffer will also develop a Layer 2 network.

Advantages:

Eigenlayer requires 32 ETH for re-staking nodes, while Puffer's re-staking feature lowers the threshold to 2 ETH, aiming to attract smaller nodes.

Security features include secure-signer & RAVe (remote attestation verification on-chain).

Business Logic:

- Users stake $ETH to receive $pufETH; Puffer's Node Operators divide the $ETH into two parts, one part is staked to Ethereum validators, and the other part participates in Eigenlayer's re-staking.

Current Status: Staking functionality has been developed, with a total of 365,432 pufETH minted and a TVL of $1.40 billion. Community situation: Currently, it has the highest number of Twitter followers among LRT protocols, with 213.7K.

Liquid Staking + Re-staking Services

These projects originally held a place in the liquid staking track and have now transitioned to the re-staking track. Their advantages include: 1. The protocol already has a large amount of staked ETH, which can be directly converted into re-staking tokens; 2. The user base is locked in, and users do not need to search for LRT protocols. Currently, Swell and Ether.fi have become leaders among LRT projects on the Eigenlayer network based on deposit volume.

Other LRT Protocols

Conclusion

Currently, many LRT protocols have not issued tokens, and there is significant project homogeneity. However, the most promising projects are KelpDAO, Puffer Finance, and Ion Protocol, which have distinct development paths compared to other LRT protocols.

Based on the ranking of tokens issued by some LRT protocols, ether.fi has the largest quantity, followed by Puffer Finance and Renzo.

From a practical interest perspective, LRT resembles a speculative leverage created for liquidity. Leverage means that the original asset still only exists once, but through token mapping and the locking of rights, the original ETH can be leveraged repeatedly, resulting in multiple derivative certificates.

These derivative certificates greatly activate liquidity in favorable conditions, making it more conducive to market speculation.

However, the various protocols issuing derivatives are interconnected due to liquidity; holding A can lend B, and lending B can activate C. If protocol A encounters issues and has a large scale, the resulting risks can be cascading.

Future Predictions for the LRT Track

Overall, the LRT track is a rapidly growing niche market. The LST track can provide stable returns of around 5%, which is indeed attractive during bear markets. The returns of the LRT track will depend on the capabilities of projects like Eigenlayer that provide re-staking services, and ultimately, the returns will determine whether users can maintain ongoing attention and capital accumulation in the LRT track. The LRT track is still in its early stages, but project homogeneity is severe, and the track has limited capacity for funds, predicting that only a few leading projects will emerge in the future.

Risks:

Slashing risk: The risk of losing staked ETH increases due to malicious activities.

Centralization risk: If too many stakers shift to EigenLayer or other protocols, it may pose systemic risks to Ethereum.

Contract risk: There may be risks associated with the smart contracts of various protocols.

Multi-layered risk accumulation: This is a key issue of re-staking, combining the existing staking risks with additional risks, forming multi-layered risks.

Future Opportunities:

Multiple combinations of LRT with other DeFi protocols, such as lending.

Enhanced security: Utilizing DVT technology can help reduce node operation risks, such as SSV and Obel.

Multi-chain expansion: Developing LRT protocols across multiple Layer 2 or PoS chains, such as @RenzoProtocol and @Stake_Stone;

About Us

This presentation was written by the Research team under HTX Ventures. HTX Ventures is the global investment arm of Huobi HTX, integrating investment, incubation, and research to identify the best and most promising teams globally. As a pioneer in the blockchain industry for a decade, HTX Ventures promotes cutting-edge technology and emerging business models within the industry, providing comprehensive support for cooperative projects, including financing, resources, and strategic consulting, to build a long-term blockchain ecosystem. Currently, HTX Ventures has supported over 200 projects across multiple blockchain tracks, with some quality projects already launched on Huobi trading. At the same time, HTX Ventures is one of the most active fund-of-funds (FOF) investors, collaborating with top global blockchain funds such as IVC, Shima, and Animoca to build the blockchain ecosystem.

References:

- SevenX Ventures: The Landscape and Opportunities of LRT Liquid Restaking

https://foresightnews.pro/article/detail/51837

- The Re-staking Token (LRT) Narrative Reignited: Finding High-Potential Project Opportunities in Endless Liquidity Nesting

https://www.techflowpost.com/article/detail_15548.html

- Liquid Staking Landscape

https://docs.google.com/document/d/1gtVgo9n2JbnZR-HFYbnsJ9nmPUGt4SYUdPXZdNHeQBY/edit

- Behind Pendle's Surge: Speculating on Airdrops, Leveraging, and Winners in the EigenLayer Re-staking Narrative

https://www.techflowpost.com/article/detail_16101.html

- Overview of the Re-staking Track: Which Projects Should Not Be Missed in the "Staking Year"?

https://s.foresightnews.xyz/article/detail/52874

- Is the Spring Breeze of the Re-staking Market Coming? A Review of Potential Projects in the Re-staking Track

https://www.odaily.news/post/5192591

Interpretation of LRT: https://twitter.com/0xNing0x

Interpretation of LRT (HaoTian): https://twitter.com/tmel0211

Disclaimer

HTX Ventures has no relationship with the projects or other third parties mentioned in this report that would affect the objectivity, independence, or fairness of the report.

The materials and data cited in this report come from compliant channels, and HTX Ventures considers the sources of the materials and data reliable, having conducted necessary verification of their authenticity, accuracy, and completeness, but HTX Ventures does not guarantee their authenticity, accuracy, or completeness.

The content of the report is for reference only, and the conclusions and opinions in the report do not constitute any investment advice regarding the relevant digital assets. HTX Ventures is not liable for any losses resulting from the use of this report's content, unless explicitly stipulated by laws and regulations. Readers should not make investment decisions solely based on this report, nor should they lose their ability to make independent judgments based on this report.

The materials, opinions, and speculations contained in this report reflect the researchers' judgments as of the date of the report's finalization, and there may be updates to opinions and judgments based on changes in the industry and data information in the future.

The copyright of this report is solely owned by HTX Ventures. If you wish to quote content from this report, please indicate the source. For extensive quotations, please inform in advance and use within the permitted scope. Under no circumstances should this report be quoted, abridged, or modified in any way that contradicts its original intent.