After the completion of the Cancun upgrade, can the high Gas fees of Ethereum be "brought down"?

Ethereum mainnet users cannot feel the changes brought by the Cancun upgrade.

Ethereum mainnet users cannot feel the changes brought by the Cancun upgrade.Author: Jason Jiang, OKLink Research Institute

This article was first published on March 13 on TechFlow Deep Tide and Techub, with the original title being "OKLink Research Institute: The Cancun Upgrade Cannot 'Bring Down' Ethereum's High Gas Fees". The content of this article represents personal opinions and does not constitute any recommendations for potential investment targets, nor does it constitute any investment advice.

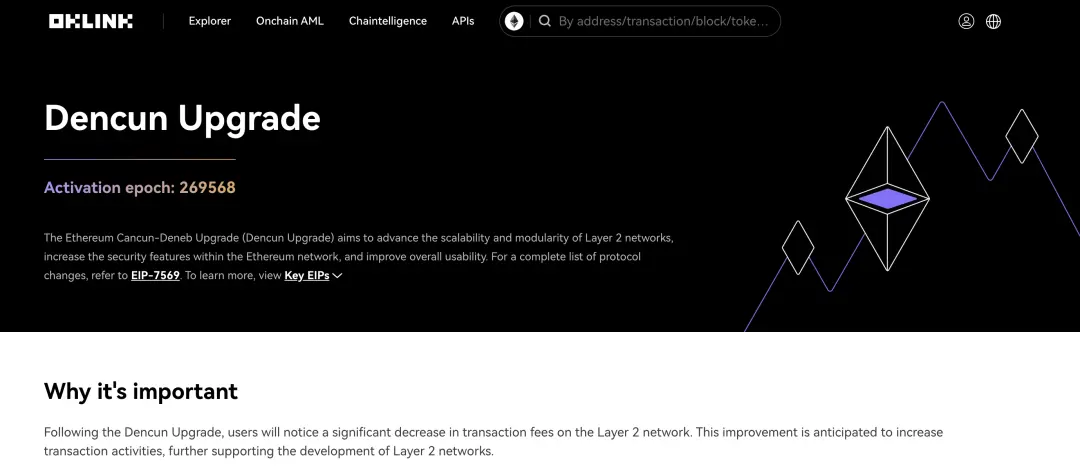

The Cancun upgrade will be activated on the Ethereum mainnet on March 13, marking another key milestone in the history of Ethereum's development. However, compared to previous major upgrades, perhaps due to the recent market frenzy, the Cancun upgrade has not attracted enough "attention." Coupled with the rapid rise of the Bitcoin and Solana ecosystems, Ethereum seems to have inadvertently fallen back into a "siege."

Can Ethereum's Gas Fees Decrease After the Cancun Upgrade?

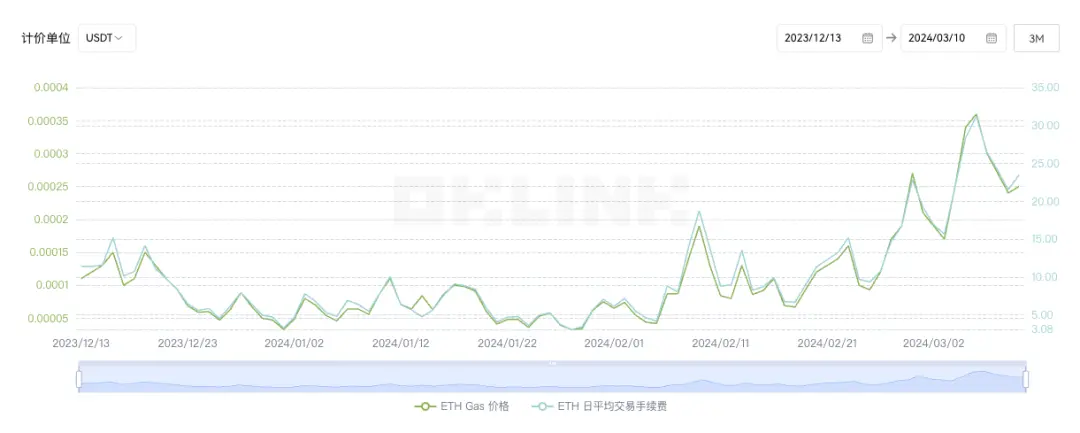

Thanks to the strong market performance, the on-chain activity of the Ethereum network has been continuously rising recently. The direct manifestation of increased on-chain activity is the continuous rise in Ethereum's on-chain transaction fees. According to OKLink data, the average Gas price for Ethereum transactions has increased by nearly 236% over the past two months, with the average transaction fee exceeding $20 in the past week. On March 6, the average transaction fee even reached $31.22, setting a new high since June 2022.

“For more data, please follow the OKLink Cancun Upgrade special page. For details, please click https://www.oklink.com/cn/eth/dencun-upgrade or read the original text.”

Faced with Gas fees that can reach dozens of dollars, many hope that the upcoming Cancun upgrade will improve this situation—however, there is a clear misunderstanding in this regard. The core of the Cancun upgrade is the EIP-4844 proposal, which aims to reduce L2 data storage costs by introducing additional Blob data storage space (previously, data storage costs accounted for over 90% of L2 transaction Gas fee consumption), thus lowering the Gas fees for Ethereum L2, rather than directly reducing the Gas fees for the Ethereum mainnet.

This means that only users conducting transactions on the L2 layer can enjoy the Gas fee reductions brought by the Cancun upgrade; other Ethereum mainnet users will not experience any "direct positive impact." Currently, the Gas consumption of the L2 layer accounts for about 10% of the daily Gas consumption of the Ethereum mainnet. Even if this portion of Gas fees can be reduced by more than ten times as the market expects, it may still be difficult to have a significant impact on the Ethereum mainnet Gas fees in the current booming market, let alone reduce Ethereum transaction fees to $0.01 as Eric.eth suggested (although Eric believes that "L2 is Ethereum").

Image source: X, erci.eth

For Ethereum L2, although a reduction in Gas fees after the upgrade is inevitable, considering the intensified competition among L2 projects for Blob space after the upgrade, as well as the anticipated surge in overall L2 activity, we believe that the positive impact of the Cancun upgrade on reducing Gas fees may be difficult to meet market expectations in the long run (the current market generally believes that Gas fees for Ethereum L2 will decrease by ten times or even more after the Cancun upgrade).

Nevertheless, the Cancun upgrade remains the most noteworthy event for Ethereum in 2024. It not only marks the beginning of the "the Surge" era in Ethereum's roadmap but will also attract more users and projects into Ethereum L2, becoming an important node for the explosion of the L2 ecosystem in this cycle.

Another widely recognized positive factor is the expectation of the approval of Ethereum spot ETFs. Compared to the widespread attention on the Bitcoin spot ETF application process, the Ethereum spot ETF has not stirred much excitement. On one hand, the short-term outlook for the approval of Ethereum spot ETFs is unclear; a senior ETF analyst at Bloomberg recently lowered the probability of Ethereum spot ETFs being approved in May from 60% to 30%. In addition to the unclear distinction of whether Ethereum itself is a security or a commodity, the currently popular Ethereum staking services may also hinder the SEC's decision: last February, the SEC ordered the crypto exchange Kraken to stop offering staking services in the U.S., and months later, it sued Coinbase Global, claiming that its staking program was equivalent to unregistered securities.

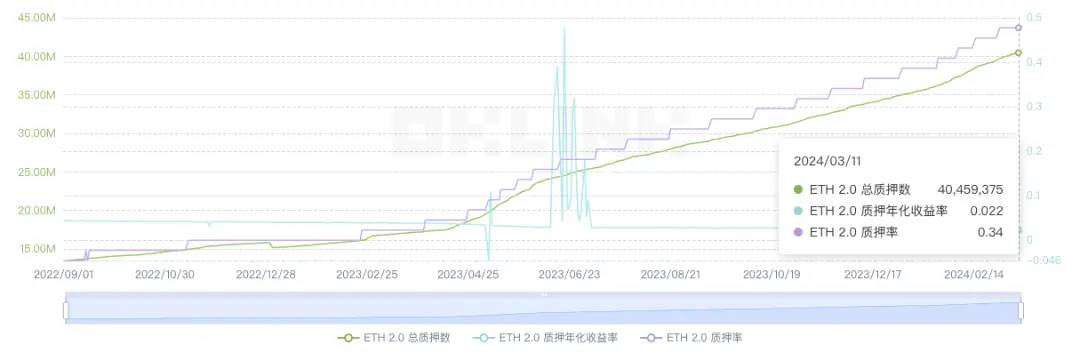

“Despite the continuous decline in staking annualized returns, as of March 2024, the total amount staked across the Ethereum network exceeds 40 million, with a staking rate of 34%. The continuous rise in the staking rate reflects the confidence of stakers in the long-term prospects of the Ethereum ecosystem.”

On the other hand, although we believe that the SEC will eventually approve the Ethereum spot ETF application due to pressure, it may not bring enough "surprises" compared to the Bitcoin spot ETF. The performance of the Ethereum futures ETF launched last October has been impressive: within hours of listing, it only had a trading volume of a little over a million dollars, in stark contrast to the hundreds of millions of dollars in trading volume generated shortly after the launch of Bitcoin futures and spot ETFs. Such a "disappointing" performance makes it difficult for us to maintain high expectations for the popularity of the Ethereum spot ETF after its launch, but this will not prevent Wall Street from offering ETF products.

Has Bitcoin and Solana "Crowded Out" Ethereum's Space?

We cannot determine whether the Cancun upgrade and spot ETFs can help Ethereum regain market attention, but the rise of the Bitcoin and Solana ecosystems has made it a fact that Ethereum cannot maintain a "monopoly" in crypto innovation.

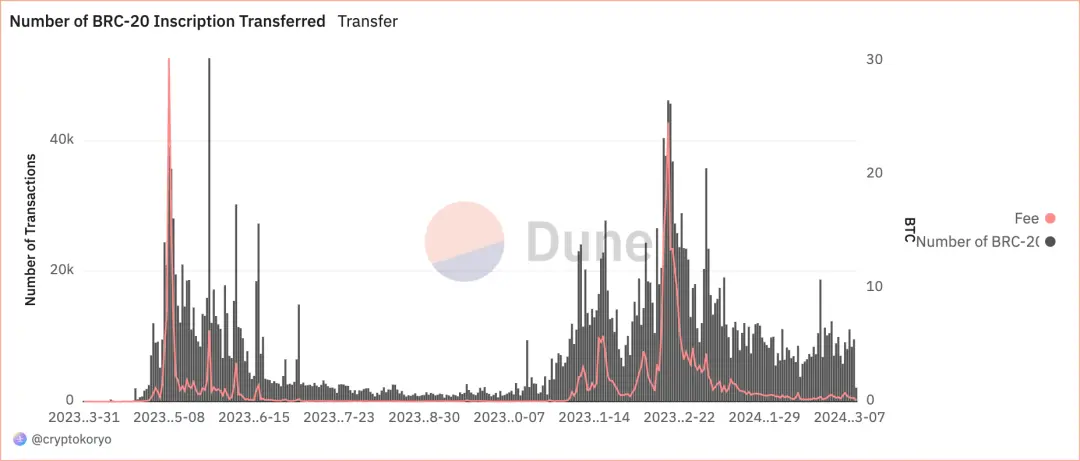

The emergence of the Ordinals protocol marks a turning point in Bitcoin's development: it has given Bitcoin, originally known as "digital gold," the potential to build a rich on-chain ecosystem. Over the past year, the Bitcoin ecosystem has flourished, with the market size of the BRC20 sector alone exceeding $4 billion, averaging nearly a 40-fold increase annually.

The enormous wealth effect has filled the market with expectations for the Bitcoin ecosystem. However, due to significant technical limitations, including transaction throughput restrictions and block confirmation time delays, the Bitcoin ecosystem cannot support large-scale applications in the short term; coupled with a relatively singular ecological narrative, there have been no other continuously attention-grabbing sub-sectors apart from inscriptions. These factors mean that although the Bitcoin ecosystem has great potential, it will not directly impact the Ethereum ecosystem in the short term. More importantly, for Bitcoin, retracing the development path of the Ethereum ecosystem is certainly not the most suitable approach; exploring more native scenarios like inscriptions around its asset attributes may be the key to ushering in a second spring for the Bitcoin ecosystem.

Compared to the Bitcoin ecosystem, Solana is seen by many as Ethereum's strongest "challenger." Although Ethereum remains the place where the smartest people in the crypto market are willing to spend the most time and effort, it must be acknowledged that Solana's technological innovations indeed start from a higher point than many blockchain architectures, including Ethereum. Before Solana, no blockchain could handle the transaction volume required by traditional financial market business needs while providing sufficiently low transaction fees and fast transaction capabilities.

“Solana Beach is where the founders of Solana surfed together while working at Qualcomm, and it is also the origin of the name Solana. Image source: The New York Times.”

However, Ethereum and Solana are not a mutually exclusive choice, just like Android and iOS: Ethereum is like Android, placing more emphasis on modularity and distributed capabilities, while continuously providing an improving development environment and infrastructure for more developers; Solana, on the other hand, is like iOS, focusing more on providing a more integrated experience for users and developers, seamlessly connecting the complexities required by different L2s.

Although Ethereum and Solana compete, they can also coexist. After all, Ethereum aims to build a decentralized global computer network, while Solana's first slide during its seed round promotion stated: "Solana is the Nasdaq of the blockchain space."

Perhaps in the short term, Solana will become Ethereum's biggest challenger in the crypto ecosystem, but in the longer term, Solana will actually fill the technological and application gaps that Ethereum has in adapting to the Web2 financial market, accelerating the breakout and large-scale adoption of Web3 technology. From this perspective, Solana may be more like a Web3 pioneer rather than a destroyer of Ethereum.

However, we may still be unable to determine who has a greater imaginative space between Ethereum and Solana in the future: this will largely depend on who can discover more scenarios and users that can realize value spillover beyond the native Crypto narrative.

Maybe it will be Ethereum, maybe it will be Solana, or perhaps it will be another public chain—who knows?