a16z: What is DUNA? How will it promote the future of web3?

Here is everything you need to know about decentralized unincorporated nonprofit organizations (DUNA) in Wyoming.

Here is everything you need to know about decentralized unincorporated nonprofit organizations (DUNA) in Wyoming.Original Title: The DUNA: An Oasis For DAOs

Authors: Miles Jennings, David Kerr

Source: DAOSquare

Everyone active in web3 has heard the term "DAO," which stands for Decentralized Autonomous Organization. DAOs are key tools for keeping blockchain networks open and have been striving to become the benchmark for web3, but there is an unavoidable topic: law and regulation.

This week, Wyoming passed a new bill that brings DAOs into the realm of legal entities. This will allow blockchain networks to operate within the applicable laws without compromising their decentralized attributes. This is a significant breakthrough as it provides much-needed protection for DAOs and empowers them to keep blockchain networks open.

Wyoming has a long history of supporting innovative legal entity structures. The state was the first to adopt Limited Liability Companies (LLCs), the first to adopt Unincorporated Nonprofit Associations (UNAs), and the first to introduce a subset of its LLC regulations for DAOs. The new Wyoming law incorporates many of the provisions proposed in the model legislation we released.

This new entity structure is likely to become the industry standard for blockchain networks created in the United States. Therefore, here is everything you need to know about the Wyoming Decentralized Unincorporated Nonprofit Association (DUNA).

1. What is DUNA?

On March 7, 2024, SF50, the "Wyoming Decentralized Unincorporated Nonprofit Association Act," was signed into law, effective July 1, 2024. This bill is closely related to Wyoming's existing Unincorporated Nonprofit Association Act but is specifically designed for decentralized organizations.

Just as Wyoming's previous DAO law (W.S. 17-31 Decentralized Autonomous Organization Supplement) can be seen as a "Digital LLC," SF 50 can be viewed as a "Digital UNA."

Additionally, it can be seen as the Web3 version of a Town Council. The purpose of a Town Council is to protect the standards and operations of the town by enforcing community rules and agreements, ultimately serving its citizens and the interests of their homes and businesses.

Similarly, the purpose of DUNA is to protect and support the underlying blockchain network, but like a Town Council, it is not a company itself.

2. Why is DUNA Necessary?

Entrepreneurs around the world are using blockchain technology to build a better internet, which is the foundation for returning the internet to its open network roots. However, if we allow companies to own these networks, we will ultimately fall back into the current situation we face: our entire digital world being controlled by a few giant companies.

Blockchain technology provides a reliable solution to this problem. It makes it possible to create open blockchain networks that resemble public infrastructure rather than proprietary technology, meaning anyone can build on these networks, just as anyone can currently use open internet networks (like email and websites) to build businesses.

DAOs consist of community members who manage the affairs of open blockchain networks. They are key tools to ensure that the network remains open, non-discriminatory, and does not unfairly extract value. DUNA helps them achieve this by addressing three key challenges faced by DAOs. It grants DAOs legal status, enabling them to contract with third parties and possess corporate attributes, while allowing DAOs to become taxpayers and providing limited liability for their members' actions. All of this aligns with other forms of legal entities and is protected under U.S. law.

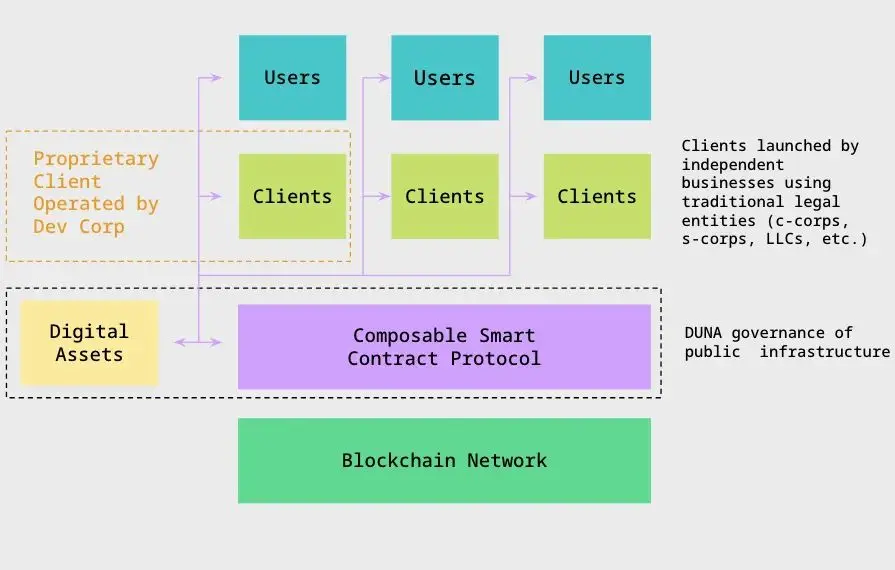

DUNA addresses these challenges without increasing additional risks to consumers. DUNA can be used for decentralized governance of open blockchain networks, but anyone building consumer-facing applications (like social media apps, car services, or music streaming apps) on top of these open networks will continue to use traditional legal entity forms, such as corporations or LLCs. While this paradigm includes the use of corporations, the fundamental difference is that corporations no longer control the underlying networks; they only control user-facing applications. This distinction significantly reduces their ability to extract value like web2 companies.

The future of web3: proprietary clients operating on a common internet entity framework, but built on public infrastructure composed of smart contract protocols and blockchain networks run by DAOs.

3. Why Should DAOs Use DUNA?

DAO membership and participation currently face some legal risks. DAOs that fail to use a legal entity cannot possess legal rights, such as the inability to pay taxes, and face potential liability risks. Meanwhile, the lack of a legal entity also threatens the privacy of DAO members. Due to these risks, the failure to use a legal entity hinders the decentralization of blockchain networks, limits their growth, and obstructs the development of economic models for such systems.

If DAOs fail to adopt a legal entity, these risks could lead to worse outcomes until a better solution emerges. For example, regulatory actions and class-action lawsuits in the U.S. claim that DAOs without legal entities are merely general partnerships. While there are several strong arguments to challenge these claims, this classification would be disastrous for DAO members, exposing them to unbearable tax risks and legal liabilities. As things stand, the advantage lies with regulators and plaintiffs. If their theory spreads and succeeds, it could even be the death knell for decentralized governance.

DUNA prevents the worsening of this situation, addresses the key challenges faced by DAOs, and significantly reduces the risks faced by DAO members. It provides DAOs with legal status, enabling them to contract with third parties, open bank accounts, and provides simple tools for the service process. It allows DAOs to pay taxes and meet their information reporting requirements. It protects the privacy of DAO members from federal government intrusion. And it provides liability protection for DAO members.

It achieves all these needs without interfering with how DAOs currently launch and operate, protecting the fundamental principle of decentralization and allowing DAOs to effectively develop the ecosystem of their underlying blockchain networks.

4. If DUNA is a Nonprofit Organization, Can They Engage in Profit-Making Activities?

The answer is yes. According to Wyoming law, both UNAs and DUNAs can engage in profit-making activities. This would include operating decentralized trading protocols, decentralized social media protocols, and everything else you can think of.

Wyoming's DUNA regulations also clarify that reasonable compensation can be paid for any services provided to the DUNA ecosystem. This feature is expected to enable DUNAs to compensate members who contribute to their growth without extracting value from users. This is crucial as it ensures that blockchain networks can operate in a decentralized manner and compete with centralized business networks.

For example, using this feature, a DAO could pay its members for governance participation. In this case, the rationale for DUNA rewarding people for voting or delegating may be that, according to regulations, DUNA has no centralized management, thus relying on its members to manage all its affairs. Therefore, to ensure proper management of DUNA, significant participation is necessary, and DUNA can compensate members to achieve this.

While Wyoming courts will ultimately determine what compensation is reasonable, there are many real examples from nonprofit organizations that can draw conclusions. Additionally, the uniqueness of blockchain networks provides a solid foundation for discussions about the reasonableness of member compensation. For instance, since blockchain networks are typically open-source and anyone can "fork" (copy) them, the continued adoption and development of a specific blockchain network that collects fees and distributes compensation to members effectively represents user tacit approval of the reasonableness of compensation for that network; otherwise, they would start an alternative network (e.g., through a fork).

Nevertheless, the qualifier "reasonable" does impose a ceiling on the value that blockchain networks can extract from users for member compensation. While those looking to design vertically integrated and centralized blockchain products and services may find this barrier to value extraction confusing, this concept aligns with the spirit of blockchain networks rather than opposing it. If web3 blockchain networks ultimately extract value from users in the same way that web2 business networks do (e.g., Apple taking a 30% cut from App Store products), then Web3 will fail. Wyoming's approach supports the spirit of web3 while still providing cash flow for digital asset holders. This is a significant breakthrough.

5. What Impact Will Using DUNA Have on Securities Law?

According to the Howey Test (which determines whether U.S. securities law should apply to digital asset transactions), three elements must be met. There must be (1) an investment of money, (2) in a common enterprise, and (3) a reasonable expectation of profits primarily based on the efforts of others.

Proponents of blockchain technology have long argued that these elements are not met for the vast majority of digital asset transactions. Most of these arguments will remain valid and can even be strengthened by adopting the DUNA legal entity form for DAOs.

For example, using DUNA can largely resolve the debate raised by the third element of Howey. First, DUNA is essentially a decentralized entity form, whose underlying structure does not include management functions, nor does it have employees or directors. Second, DUNA members have no legal obligation or right to maximize the organization's profits. In summary, these characteristics greatly negate any claims that members may have a "reasonable expectation of profits primarily based on the efforts of others" when purchasing digital assets. Finally, as mentioned above, the nonprofit nature limits DUNA's ability to distribute organizational profits to its members but does allow it to compensate members for their contributions to the organization. Therefore, any compensated member is necessarily profiting from their own efforts rather than from the management efforts of others.

Nevertheless, the U.S. Securities and Exchange Commission (SEC) may attempt to argue that DUNA meets the "common enterprise" requirement of Howey because DUNA membership is priced in the digital assets of the DAO. However, based on DUNA's decentralized structure, many rebuttal arguments can be made. Additionally, regulators have sought to designate DAOs as general partnerships or unincorporated associations under common law, which at least suggests that categorizing DUNA as a "common enterprise" is contradictory. Finally, the rights of DUNA members are largely a product of DUNA's governing principles, which are typically rights specified in the underlying governance and protocol smart contracts that constitute the DAO, regardless of whether the DAO formally adopts the DUNA structure; these rights will exist. Therefore, if the underlying governance smart contracts are insufficiently defined as a "common enterprise," there is no reason to argue that the existence of DUNA would change that conclusion.

While the SEC's theories regarding the applicability of U.S. securities law to digital asset transactions are vague and constantly evolving, the fact remains that they are still bound by the Howey Act and subsequent cases. Under this act, DAOs can support their communities' arguments against the application of securities law to the digital assets of DAOs by adopting DUNA.

6. What Impact Will Using DUNA Have on Taxes?

For anyone who has ever consulted a tax advisor about DAO tax issues, the specific circumstances and context of a project are the most important factors in forming answers to specific questions, and generalized statements cannot replace specific advice for a project.

Like LLCs and UNAs, DUNAs can eliminate the complexities of DAOs operating under the U.S. tax framework, as they can be taxed as corporations. Corporate tax treatment allows UNAs and DUNAs to fulfill their tax obligations without disclosing individual members and avoids the complexities of pass-through taxation, addressing the common issues faced by blockchain network DAOs. Additionally, the U.S. has signed numerous tax treaties with many countries and regions, providing an environment where domestic entities can clearly define tax obligations, which is a significant advantage for DAOs composed of members from multiple countries.

It is important to clarify that all of the above means that DAOs will bear tax obligations arising from their activities, which may differ from currently existing activities, but ultimately these tax expenditures will significantly reduce the risks associated with membership and provide clarity in an uncertain tax environment. By paying taxes somewhere and bringing it within the scope of U.S. taxation, DAOs can address the enormous unknowns surrounding their operations and member risks.

7. Why Haven't More DAOs Adopted the UNA Entity?

Since the DUNA structure was only recently introduced, there has not yet been any in-depth criticism of this structure. However, prior to this, some arguments against using UNAs (the statutory predecessor of DUNA) had been raised. Below is a summary of these arguments and the corresponding counterarguments in light of Wyoming's passage of DUNA.

In short, arguments against using UNAs can either be resolved by DUNA or lack persuasiveness. While DAOs will continue to face uncertainty even with the adoption of the DUNA structure, it is undeniable that the uncertainty factors surrounding DAOs will be significantly reduced. While some may hope for a perfect legal entity structure to emerge that would provide legal special treatment for DAOs and blockchain technology, this is an unrealistic approach that would hinder progress from the outset.

- Nonprofit status limits flexibility. Some argue that UNAs are not a suitable structure for DAOs due to their nonprofit characteristics. This is a fundamental misunderstanding of the term "nonprofit." By law, both UNAs and DUNAs can engage in profit-making activities. Furthermore, they allow for compensation to members. Wyoming's DUNA regulations explicitly state that reasonable compensation is permitted (including in exchange for participation in DUNA governance).

- Undermines decentralization. Some believe that UNAs introduce centralized risks. While UNAs typically rely on "managers" to handle daily affairs, DAOs can easily limit these powers. In any case, any concerns about centralization have been addressed by DUNA, which is specifically designed for large decentralized organizations. It applies regardless of whether the number of members is 1,000 or 10 million. Additionally, DUNA considers a baseline structure that does not include management functions, allowing for the selection of administrators with limited authority to perform specific tasks authorized by members. For most DAOs, this type of activity has already been exercised by protocol foundations without introducing greater centralization risks. Therefore, this classification makes DUNA compliant with the decentralization standards set by U.S. securities law.

- Jurisdictional choice. Some argue that DAOs do not belong to any jurisdiction and therefore should not choose to establish an entity in any jurisdiction (including UNA). This argument has many issues; simply put, it is a fantasy that does not consider the consequences it brings. Not utilizing the laws of any jurisdiction means one could be subject to the laws of all jurisdictions. Therefore, this approach benefits potential attackers (including individual plaintiffs and governments), allowing them to sue in the jurisdiction most favorable to them. This is not a theoretical discussion; it has already begun to play out in regulatory lawsuits against Ooki DAO, as well as class-action lawsuits against Compound DAO, Lido DAO, and others. Currently, these actions are primarily taking place in California, with the theoretical basis being that such DAOs are general partnerships. In the case of Ooki DAO, the court has ruled that Ooki DAO is a general partnership, and if this decision is widely replicated, it would be the death knell for web3 decentralized governance. If DAOs ignore this risk, they are disregarding the danger.

- Destruction of permissionless nature. Some argue that using legal entities would undermine the permissionless nature of DAOs because it requires DAO members to join a legal entity. According to the definition of DUNA, this is incorrect. Holders of DAO digital assets do not need to join their DUNA and can freely choose not to join. Instead, the terms of DUNA membership are determined by the DAO according to its governing principles.

- Unclear use cases/unproven in court. Some argue that since existing UNA legislation did not consider the use of blockchain networks, state legislatures may not intend for blockchain networks to use this structure, and the use of UNA by blockchain networks has not been tested in court. These arguments are no longer relevant because DUNA is specifically designed for decentralized organizations and considers the use of blockchain networks. Furthermore, the use of unincorporated structures by DAOs has already led courts to apply them to general partnership statutes, which should be the significant risk for DAOs to maintain an unincorporated status.

8. How Does A16Z CRYPTO Plan to Support the Adoption of DUNA?

a16z crypto will be dedicated to promoting the widespread adoption of DUNA in web3, making it an industry standard. These efforts will include:

- 1) Developing decentralized governance proposals for the DAOs we are currently involved with to help them adopt DUNA.

- 2) Assisting our existing portfolio companies in adopting DUNA structures related to their decentralization goals.

- 3) Where appropriate, as an investment condition, requiring potential portfolio companies in the U.S. to agree to adopt DUNA structures when decentralizing and adopting decentralized governance. Additionally, a16z crypto intends to invest significant effort in providing resources for entrepreneurs, law firms, accounting firms, and other advisors to facilitate the adoption of DUNA structures.

Adopting the DUNA entity structure can resolve most of the uncertainties currently faced by DAO members when participating in DAO activities. Therefore, we hope that through our efforts, DAO members will be empowered to contribute more and enhance the fundamental principle of decentralization in Crypto. For a16z crypto, this means unleashing the full potential of its engineering and research teams to promote the interests of DAOs.

9. Where Can I Learn More?

For background and more information on DAOs, UNAs, and DUNAs, please refer to:

- The Legal Framework for DAOs (October 2021). Provides background on DAOs, explores the challenges they face, introduces UNAs as an excellent choice for DAO structures, and reviews the history of that structure.

- The Legal Framework for DAOs -- Part Two: Entity Choice Framework (June 2022). Provides a comprehensive argument for why UNAs are the only suitable entity structure for blockchain network DAOs.

- The Legal Framework for DAOs -- Part Three: Model Decentralized Unincorporated Nonprofit Association Act (March 2024). Introduces DUNA, presents model legislation for adopting DUNA, and provides a detailed analysis of the provisions of the model legislation.