From the perspective of token economics, here are the "cryptocurrency trading knowledge" that must be understood before the arrival of a bull market

To understand whether a coin is rising or falling, we must understand supply and demand.

To understand whether a coin is rising or falling, we must understand supply and demand.Original Title: Tokenomics 101 - valuable knowledge before the 2024-2025 bullrun

Original Author: Route 2 FI

Original Compiler: Luccy, BlockBeats

Editor's Note: In this article, crypto researcher Route 2 FI explores the fundamental concepts of tokenomics and some reference standards. From the perspective of supply and demand, it delves into the issuance, distribution, and market performance of tokens. By comparing different scenarios of tokens like Bitcoin and Ethereum, as well as considerations of governance, yield, and expectations, it comprehensively explains the mechanisms and driving factors behind tokens. BlockBeats compiles the original text as follows.

Today's article is about tokenomics, which may be valuable for you when looking for new projects to determine whether they are worth buying.

Many people talk about tokenomics, but only a few truly understand it.

If you are considering whether to buy a crypto asset, understanding tokenomics is one of the most useful first steps you can take to make an informed decision. This newsletter will introduce some basics to help you learn how to analyze projects on your own.

To understand whether a coin is going up or down, we must understand supply and demand. To better understand this, let's take BTC as an example, starting from the supply side.

Supply

· How many BTC tokens are there?

Answer: 19.2 million BTC

· How many tokens will there be in total?

Answer: 21 million BTC

· How often are new tokens released to the market?

Answer: The increase in token supply over time is referred to as "emission," and the rate of emission is important. You can find information about this in the token's whitepaper.

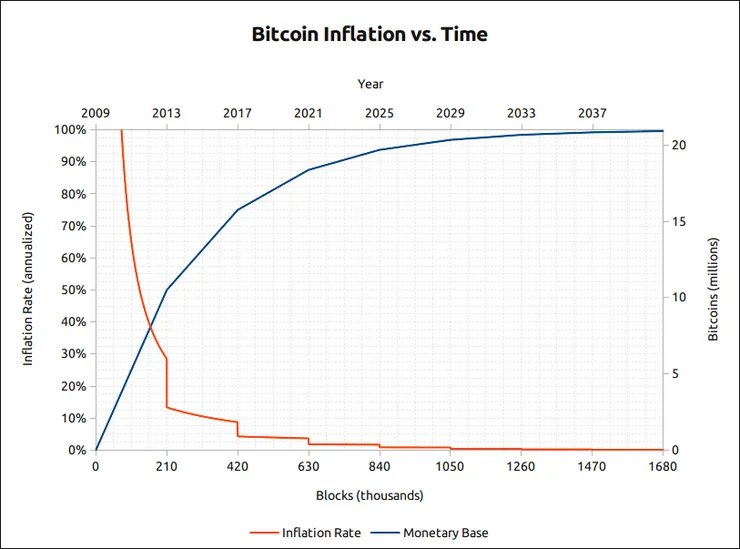

Every 10 minutes, BTC miners validate a block of BTC transactions. The current reward for validating a block of BTC is 6.25 BTC. Therefore, approximately 900 BTC are released to the market each day.

On average, the block creation rate will "halve" once every four years (known as "halving"), until eventually, in 2140, the reward for mining a block will be only 0.000000001 BTC.

In other words, by early 2030, nearly 97% of BTC is expected to be mined. The remaining 3% will be produced over the next century, until 2140.

The current inflation rate of BTC is 1.6% and will gradually approach zero.

This means that if fewer tokens exist, the token price should rise, and conversely, if more tokens exist, the price should fall.

This is easy to understand for BTC, but when we look at other tokens, such as ETH, it becomes a bit more complicated because there is no cap on the number of Ethereum. However, as long as Ethereum's gas fees remain at a reasonable level, it is effectively a net deflationary asset.

Important Metrics

· Circulating Supply: The number of tokens that exist today

· Total Supply: On-chain supply minus burned tokens

· Max Supply: The maximum number of tokens that can exist

· Market Cap: Today's token price x Circulating Supply

· Fully Diluted Market Cap: Today's token price x Max Supply

Another important aspect to consider regarding supply is token distribution. This is not a major issue for BTC, but it is something to consider when evaluating new tokens you are thinking of buying.

Additionally:

· Do large holders own most of the tokens?

· What does the unlock schedule look like?

· Did the protocol distribute most of the tokens to early investors in the seed round?

My point is: don't invest in garbage coins like KASTA created by The Moon Carl without researching tokenomics and end up losing money. In my opinion, @UnlocksCalendar and @VestLab are good resources to check unlock schedules.

To quickly summarize the important aspects of supply, check:

· Circulating Supply

· Total Supply and Max Supply

· Token Distribution

· Unlock Schedule.

That said, relying solely on supply is not enough to decide whether a token is worth buying. So next, let's talk about demand.

Demand

Okay, we know that the supply of BTC is 21 million tokens, and the inflation rate of BTC is about 1.6%, which is decreasing each year. So why isn't the price of BTC $100,000 yet? Why is it only "40K" dollars?

Well, simply put, having a fixed supply alone does not give BTC value. People also need to believe that BTC is valuable and that it will be valuable in the future.

Let's break down demand into three components:

· Financial Utility (the return on investment of the token)

· Real Utility (value)

· Speculation

Financial Utility: How much income or cash flow can holding the token generate? For proof-of-stake tokens, you can stake tokens to generate passive yield.

This is not possible for BTC unless you wrap it into WBTC, but then it is no longer regular BTC. If holding a token benefits holders through rewards from staking yields or providing LP in liquidity mining, then demand will naturally increase.

But remember, the yield must come from somewhere (token inflation), so when you see those really high annualized projects (think of the OHM-fork season in 2021), it's wise to remain somewhat skeptical.

Real Utility: For many projects, the fact is they have no value. This can be debated, but BTC is valuable because it can serve as a store of value and a unit of exchange. BTC is referred to as digital currency, an alternative to fiat currency controlled by central banks. Ethereum is a digital currency with multiple uses through decentralized finance applications (dApps).

You can actually do things with ETH, not just hold, send, or receive it. To determine whether there is real utility, you must consider who the team members are, what advisors they have, and their backgrounds. What companies support them, what are they building, and are they solving a real problem, etc.

Speculation: This includes narratives, memes, and beliefs. Essentially, it is a belief in the future that others will want to buy it after you do.

The speculative aspect of demand is difficult to analyze and predict. BTC has no return on investment and no staking opportunities, but it has a strong narrative. People believe it could be a long-term store of value. BTC also has a huge advantage in that it is the first cryptocurrency.

When you hear people talk about cryptocurrencies, the first thing they mention is BTC. A strong community can drive demand, so always remember to research the community on Twitter and Discord before investing.

In my opinion, speculation is one of the biggest driving factors in cryptocurrency. Don't underestimate how far a token can go under the right narrative, meme, and following. Think of DOGE, SHIB, ADA, and XRP.

Most crypto tokens are highly correlated and move together. If what you hold is anything other than BTC and ETH, it should be based on the supply and demand aspects of tokenomics that make you believe it will perform well.

Another important aspect when valuing a token is the tokenomics trilemma: the balance between yield, inflation, and lock-up periods: proof-of-stake projects want to offer high staking yields to attract users, but high annual percentage rates can lead to inflation and selling pressure. On the other hand, if staking yields are not attractive enough, it may be difficult to attract users.

One way to encourage people to hold tokens is to offer higher yields for longer lock-up periods; the downside is that if the lock-up period is too long, people will simply avoid participating in the project. Another thing is that the day of unlocking will come, leading to massive sell-offs as investors want to take profits.

If you find supply/demand difficult to understand, just try to think about it simply:

What would happen if the Ethereum Foundation decided to print 100 million new ETH tokens tomorrow? The answer: the price would crash due to increased supply and decreased demand.

What would happen if Michael Saylor announced he wanted to buy 100,000 BTC in the next six months? The answer: the price would rise because supply would decrease and demand would increase.

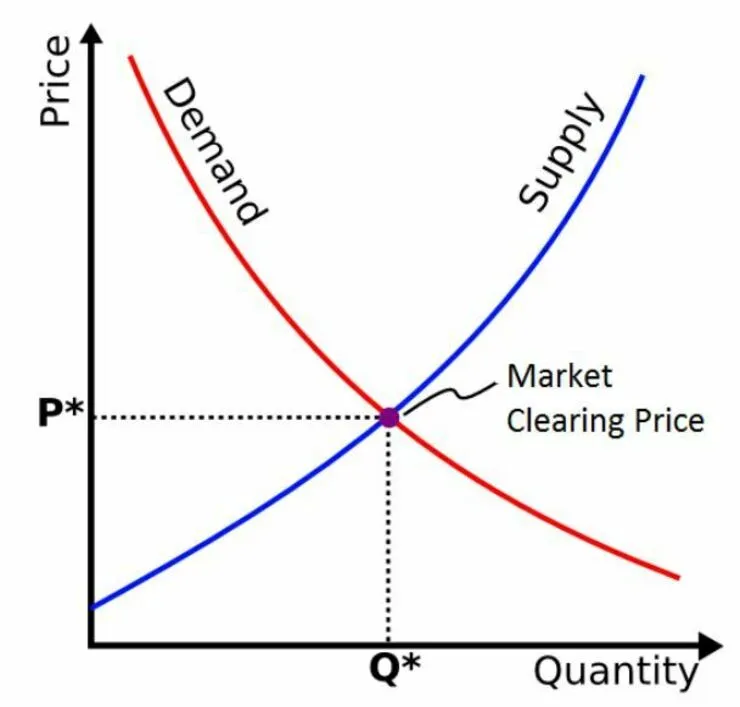

Just consider this model below:

Prices will always tend to balance according to the supply and demand curve.

Is ETH worth $100 or $10,000? Is BTC completely worthless or worth $300,000?

No one really knows, and because cryptocurrencies have no intrinsic value compared to stocks, it remains very difficult for investors to determine prices.

This makes crypto assets very volatile and speculative. But it also provides huge opportunities for the few who actually take the time to engage with cryptocurrencies.

What should a new project or protocol focus on?

Let's take a look at the structure of Curve (CRV).

Essentially, Curve incentivizes LPs and encourages participants to engage in governance through their tokenomics. For Convex, the ultimate goal here is to acquire as much veCRV as possible to maximize CRV rewards.

After clearly setting goals, the project's founders should further investigate the actual value proposition of the token: what value can participants holding the token derive from it? For example:

· Staking

· Governance

· Store of value

And more. Nowadays, it is common to see founders propose tokens composed of multiple value propositions. Of course, this can lead to higher demand for the token.

A perfect example is GMX, which has multiple value propositions such as governance (the ability to inspire participants' true preferences), claiming (the ability to convert held GMX into GMX over a period), and holding (receiving protocol revenue).

Along with these value propositions, there are functional parameters, which relate to the variables that determine the token's functional capabilities, the simplest examples being transferability or burnability. For the team, ensuring that the token's functional parameters do not conflict with its value propositions is absolutely critical. For example, a token intended for value transfer should have functionalities that ensure its fungibility. Here are some functional parameters of tokens:

· Transferability (transferable + non-transferable): GMX and esGMX, respectively.

· Burnability (burnable + non-burnable): BNB and SBTs, respectively.

· Fungibility (fungible + non-fungible): ERC20 and ERC721 (NFT), respectively.

· Exchange Rate (floating + fixed): MKR and DAI, respectively.

Sometimes, teams deliberately decide that a token is assigned conflicting value propositions or functionalities. In such cases, the token can be divided into two or more types. A well-known case is AXS, which transitioned from an initial single-token model to a multi-token model.

Initially, AXS had three value attributes: value transfer, governance, and holding. The conflict here arises because if participants decide to transfer AXS's value in-game, it means giving up governance and holding rights, which creates issues for the game economy. To solve this problem, they released a "new" token SLP, which then became the preferred value transfer tool in the game. You may also recall the same dual system in STEPN's GMT and GST.

However, implementing a dual-token system can make tokenomics design overly complex, and sometimes it may be important to consider using external tokens as auxiliary tokens to ensure smoother interactions. A typical example is ARB, which is primarily used for governance.

To ensure smoother interactions, ARB uses ETH as a means to pay transaction fees, as transactions occurring on L2 are bundled together and sent to L1 state. Without introducing this external token (ETH) as a means to pay transaction fees, the following situation would occur: ARB would be used to pay transaction fees (gas fees), and operators would then have to exchange ARB for ETH to validate on L1, incurring further gas fee losses, creating a contradiction for ARB's growth.

In the above sections, I have introduced the general dynamics of tokenomics and various driving factors that teams should consider. Now let's take a look at token supply, as this directly affects token prices (which is what degens want). The structure of token supply is as follows:

· Max Supply

· Allocation Percentage (sales, investors, team, marketing, treasury, etc.)

· Distribution of Allocations: allocations for initial, vesting, and reward issuance.

Max supply is important because it determines the maximum cap the team can issue tokens. Unrestricted tokens may not have a good price distribution. This does not directly affect price, but factors affecting the issuance rate, as well as whether the token is deflationary or inflationary, are factors that influence price.

For a limited max supply, such as CRV (3 billion tokens), prices can rise. As the network grows, demand for the token increases, forming a high-demand area with limited supply. The issue with this type of max supply is that if token distribution is not rapid, it may be difficult for future new contributors to provide incentives.

On the other hand, having an unlimited max supply can avoid concerns about future incentives running out. Of course, the downside here is that there may be a decline in token prices in the long run, as there is essentially unlimited supply unless external models are used to reduce circulation (e.g., staking, burning, etc.), leading to a long-term downward trend regardless of growth.

In terms of allocation, it is usually based on a percentage of the max supply, effectively determining the maximum supply percentage that should be allocated to each category. The main categories are: team (including founders, developers, marketing, etc., essentially the individuals responsible for building the project), investors (those participating in early/seed/private rounds), treasury (operational costs such as R&D, reserves, etc.), community (airdrops, LP rewards, mining rewards, etc.), public sales (ICO, IDO, IEO, LBP, etc.), and marketing (including advisors, influencers, agents, etc.).

These are some key elements that projects consider; however, these elements are essentially unique to each project and can be simplified or further categorized based on their "strategies."

It is worth noting that during the rise of DeFi in 2020-21, teams realized that allowing higher rewards for their communities or increasing the float of initial holders through airdrops could lead to network growth and a thriving sustainable token economy.

Finally, distribution. The initial supply is the initial float released to the open market at "launch," or what some call TGE. The allocations in this category are usually a part of the treasury, public sales, and the notorious airdrops we see everywhere.

For tokens that are to be unlocked, these are usually locked for x months/years, typically applicable to investors, treasury, and team tokens, which can decide the duration and when to start unlocking. Usually, unlocking prevents large-scale token sell-offs, especially since participants in this portion are often investors who purchased at valuations below the listing price.

So why does all this matter?

Simply put, token demand and value capture mean that theoretically, market participants should gain value by holding the token.

Let's take CRV as an example again. We need to identify and understand the meta-demand of CRV. Let's break down its value proposition: it is a governance token. Participants can use their CRV to vote on how much CRV is issued weekly. Why is this important? How does it capture value? Because market participants holding CRV are entitled to 50% of the project fees. Therefore, the more CRV they hold, the more income they receive. This makes CRV's ultimate meta-demand the ability to maximize user profits while encouraging them to hold, creating a good mechanism that induces positive behavior (user holding) and captures value (receiving rewards).

Returning to the beginning, many tokens struggle to regain their value. This has sparked projects' interest in capturing value by generating profits for market participants through holding.

Nowadays, there are many creative token models in the space. I think another great example is how Cosmos successfully addressed the hype around airdrops.

I have discussed this before, but you may remember that staking ATOM, OSMO, KUJI, INJ, and TIA may qualify you for most airdrops in today's Cosmos ecosystem.

This has led to a significant increase in the number of stakers in the Cosmos ecosystem. With promises of more airdrops in the future, they will not stop staking. This incentive encourages people to hold tokens rather than sell. With a 21-day un-staking period, un-staking becomes quite cumbersome, so people are more inclined to hold.

A DeFi Degen described the Cosmos ecosystem's practice as (3,3) (the OHM Ponzi scheme), and to some extent, he is right.

Want to learn more about tokenomics?

Here are 4 great threads that delve into tokenomics: