Covalent Network: The Forgotten Gem of the Decentralized Infrastructure Track

Covalent is a leading project in a rapidly developing track, with various business metrics in a phase of rapid growth.

Covalent is a leading project in a rapidly developing track, with various business metrics in a phase of rapid growth.Author: Mint Ventures

1. Report Highlights

1.1 Core Investment Logic

Covalent is a leading project in a rapidly developing sector, with various business metrics on a fast upward trajectory and revenue data expanding. In terms of revenue levels, Covalent has several times the income of the current leading project in the sector, The Graph, suggesting it has achieved a better PMF (Product Market Fit). However, since its revenue streams have not yet been on-chain, there may be a significant cognitive gap among market investors regarding this.

In terms of new business, its developing Ethereum Wayback Machine serves as a long-term blob DA (blob is a new data storage structure after Ethereum's EIP4844 upgrade, storing data that does not need to be permanently stored on-chain) solution, which aligns well with current market trends.

Regarding the team, the founding team possesses professional backgrounds and entrepreneurial experiences that match the sector, and the investors include various leading industry players, including public chain foundations, major exchanges, and key clients.

1.2 Main Risks

If other centralized blockchain data service providers with larger user bases, such as Alchemy, Infura, Quicknode, etc., enter the downstream data indexing service sector from RPC and offer similar data indexing services, it may squeeze Covalent's market share and pricing. For instance, Alchemy completed the acquisition of the data indexing platform Satsuma in September 2023.

Data indexing is a relatively niche sector with low awareness among general investors, and currently, it has not attracted investor attention. This trend may continue in the absence of hot events in the sector.

1.3 Valuation

Covalent has significant valuation appeal compared to the leading project in the sector, The Graph.

2. Project Overview

2.1 Business Positioning

Covalent provides blockchain data indexing services, offering a unified blockchain data API that allows developers to query across multiple blockchains.

Before explaining the data indexing service, it is necessary to briefly describe its upstream services—blockchain nodes and blockchain RPC.

Blockchain Nodes:

Blockchain nodes are the fundamental elements that make up the blockchain network, with each node storing a complete copy of the blockchain (or, in some cases, a partial copy, such as light nodes). Nodes synchronize and validate all transactions and blocks through consensus mechanisms, ensuring data consistency and security across the network.

Blockchain RPC:

RPC is a service interface that allows external clients to interact with blockchain nodes. It acts as a middle layer, providing a set of standardized commands or function calls, enabling developers to perform operations such as reading data, sending transactions, and executing smart contract functions.

Blockchain Indexing:

Blockchain indexing is a data service based on blockchain nodes and RPC. It reads data from blockchain nodes via RPC, processes and organizes this data, and creates an efficient query database. This allows users and applications to quickly retrieve the information they need without having to perform complex queries directly from the blockchain nodes.

In summary, the relationship among nodes, RPC, and indexing services is as follows: blockchain nodes are the source of data, RPC services are the channels to access this data, while indexing services act as data processing factories, optimizing data retrieval and usage.

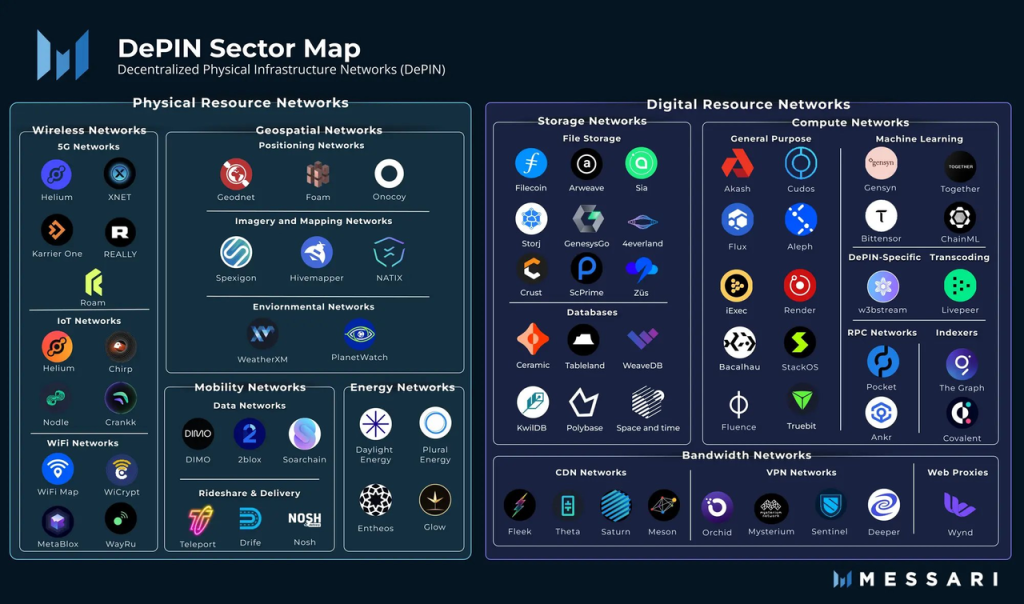

In the blockchain data indexing sector, there are both centralized service providers, such as @Bitquery_io, @etherscan, @MoralisWeb3, @blockvisionhq, and decentralized service providers, with The Graph being the most well-known.

Additionally, in the Depin sector mapping released by Messari in 2023, data indexing is also included under the Depin category, classified as part of the "digital resource network" category, with both The Graph and Covalent appearing as representative projects in the diagram.

Image Source: Messari

Image Source: Messari

2.1.1 User Groups

Covalent's clients are primarily B-end, including Dapp projects such as various DeFi applications, as well as many centralized crypto companies, such as Consensys (investment dashboard), CoinGecko (asset market), Rotki (tax tools), NFTX (NFT curation), and Rainbow (crypto wallet).

2.1.2 Value Proposition

The economic scale of the blockchain world is growing exponentially: more ecosystems, more L1s, and more Rollups.

An increasing number of users and economic activities mean more transactions and more data, all of which are distributedly stored by blockchain nodes. This implies decentralization, openness, and accessibility of data, but also complexity, bulkiness, and inefficiency in data retrieval. The size of data on the Ethereum blockchain alone has exceeded 1TB, facing the "read and parse scalability" issue.

When applications (such as wallets, NFT markets, or more complex web3 products) require data from multiple blockchains with different output formats, the situation becomes even more complicated. Covalent has built a protocol that standardizes data from various blockchains, known as the "Unified API." This unified API allows users and dApps to access all on-chain data in a structured manner, enabling them to integrate it into existing products without the need for cumbersome data processing.

Image Source: Covalent Documentation

Image Source: Covalent Documentation

The indexing layer of the blockchain should be as flexible as possible to accommodate the diversity of various products and services that will be launched in the market over the next few years, while minimizing trust. Covalent's value proposition in data indexing includes:

- Verifiable data. Trustless data verification is achieved through cryptographic proofs, allowing Covalent to decentralize its infrastructure by enabling anyone to enter the network as a Block Specimen producer and incentivizing them to remain honest through staking and slashing mechanisms.

- Scalability. Covalent is a plug-and-play solution suitable for new EVM blockchains and application chains, with an onboarding time of less than a week. For non-EVM blockchains, data can be extracted from chain clients by following the block specimen standards.

- Data composability. Covalent's standardized data model allows developers to package, mix, and fork data as if they were handling assets, regardless of the data chain.

- No-code solution. The no-code functionality of Covalent's unified API provides solutions for analysts, developers, and other non-technical users at the visualization layer. Users can create pivot-table-like content on the underlying data to obtain information such as 24-hour trading volume, historical NFT floor prices, and aggregated wallet token balances across networks.

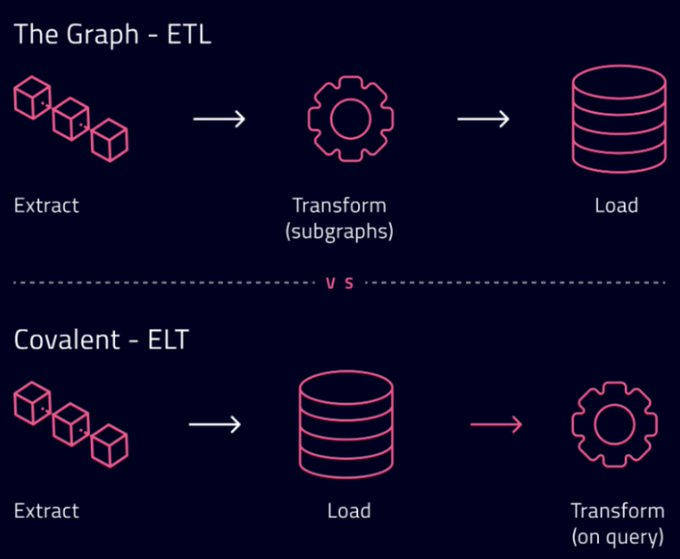

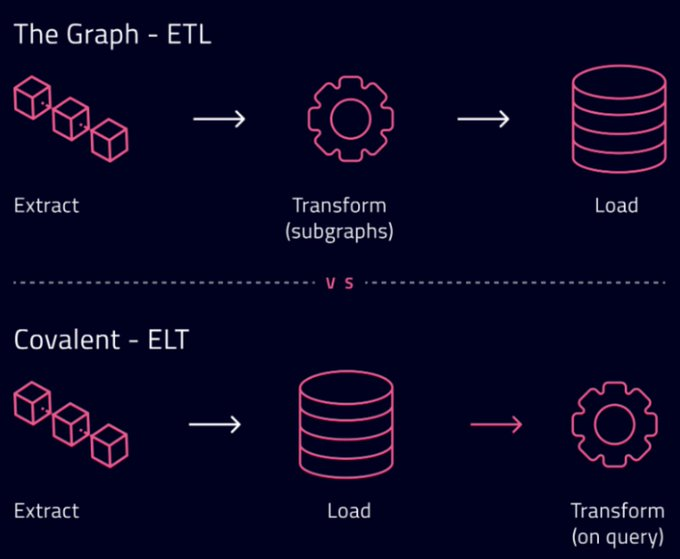

- Flexibility. Covalent follows the Extract-Load-Transform (ELT) data integration model, extracting data from blockchains and loading it into data warehouses. Customers can then transform it as needed during queries to provide the required data. In contrast, The Graph's subgraph-based indexers follow the Extract-Transform-Load model, where extracted data is first transformed into subgraphs for specific use cases, resulting in less flexibility.

Image Source: Covalent Documentation

Image Source: Covalent Documentation

2.2 Business Logic

2.2.1 Product Mechanism

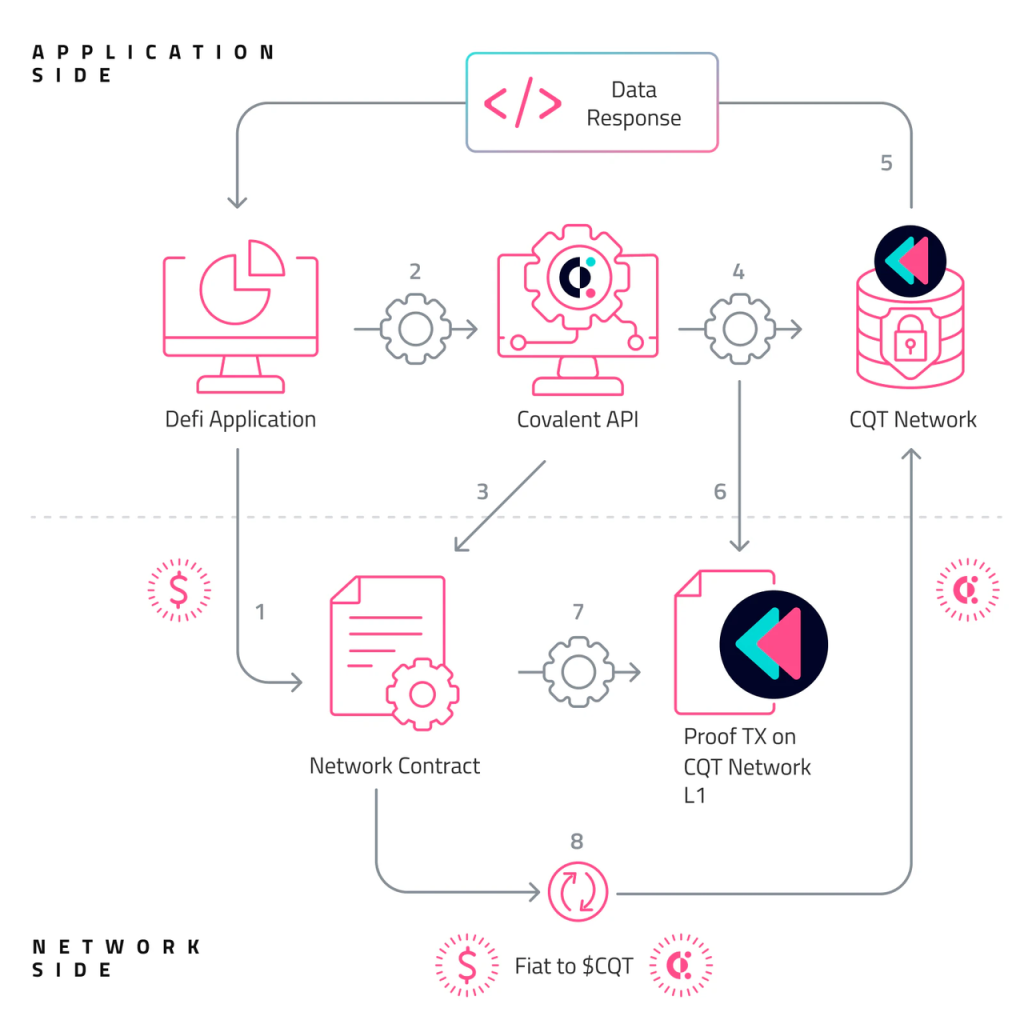

Covalent's current core product is the Unified API, which transmits data between two modules: client and server. Through the API, the server can control its system and respond to client requests. Users (such as application developers or analytics companies) extract data from the API, while data providers (currently mainly Covalent itself, with plans to open to third parties later) retain ownership. Although many companies have built server-side infrastructure to provide access to blockchain data, most self-built server-side solutions are limited to the RPC layer, often only retrieving raw blockchain data from the target chain.

Covalent's Business Process, Image Source: Covalent: A Unified API for Retrieving Blockchain Data

Covalent's Business Process, Image Source: Covalent: A Unified API for Retrieving Blockchain Data

The so-called "raw blockchain data" refers to information that can be directly queried from the blockchain via RPC. In contrast, deeper data analyses, such as complex queries, data correlation analyses, and historical data trend analyses, typically require more advanced data processing and indexing services, which are provided by Covalent and The Graph.

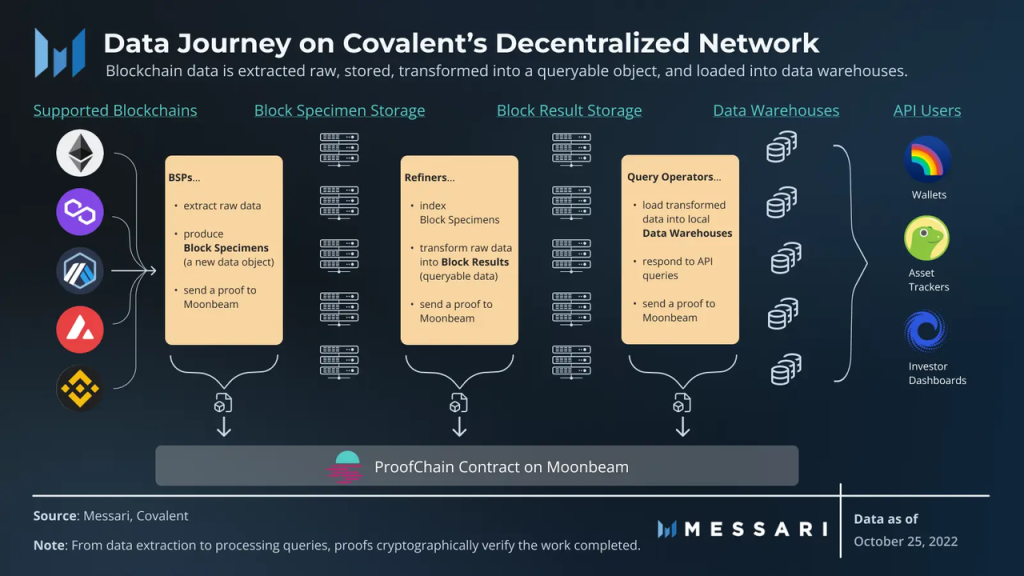

Covalent's protocol is more in-depth than traditional methods: it extracts data from various blockchains, uploads this data to storage instances*, indexes and transforms the stored data objects, and loads the data into local data warehouses for API users to query. Throughout the process, it sends proofs to the Moonbeam network to verify the completion of each step. In short, Covalent ensures and standardizes all extracted blockchain data cryptographically, allowing developers to query from any chain in a unified manner, hence the name Unified API.

Storage instance: A data instance that includes database software and associated memory structures and background processes. A database server can run multiple instances, with each instance managing its own data and processes.

Based on the Unified API, Covalent has also launched corresponding toolkits for customer integration and product presentation.

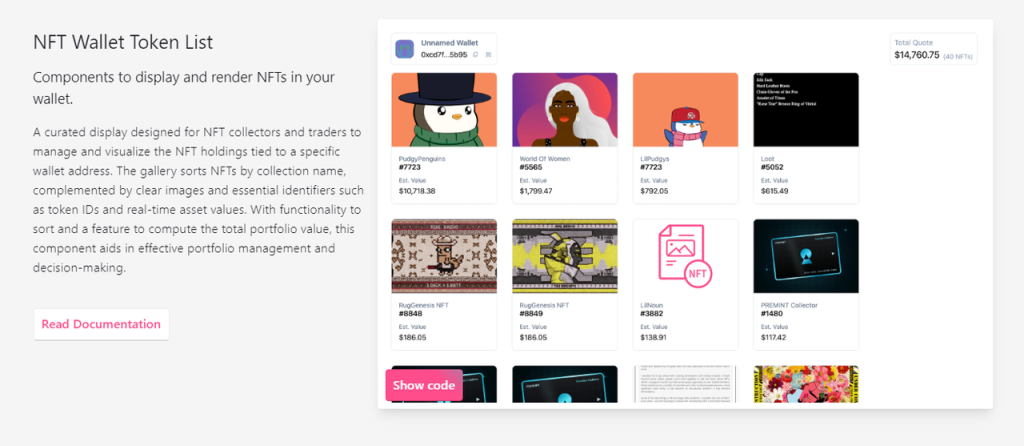

GoldRush

GoldRush is an open-source modular blockchain explorer and toolkit provided by Covalent, which can be integrated into various Dapps and Web3 applications.

Use Case Scenarios:

- NFT markets like Blur or NFTx. Each NFT transaction on the platform can link to a block explorer like Etherscan for querying, which takes users away from your platform, interrupting the user experience, and block explorers can be overly technical and difficult for many general users to understand.

- Web3 games face the same challenges: users should not have to stop in the game to verify and check transactions on a block explorer. Many in-game transactions are unique and complex, and block explorers cannot capture these details or present them in a correct and intuitive manner.

In similar scenarios, as a Blur or web3 game provider, you can directly integrate Covalent's GoldRush module into your application to present various data in a user-friendly manner and provide interactivity.

Image Source: https://www.covalenthq.com/products/goldrush/?component=NFTWalletTokenListView

Image Source: https://www.covalenthq.com/products/goldrush/?component=NFTWalletTokenListView

After briefly explaining Covalent's industrial mechanism, let's see how it integrates with the token mechanism.

2.2.2 Decentralized Design

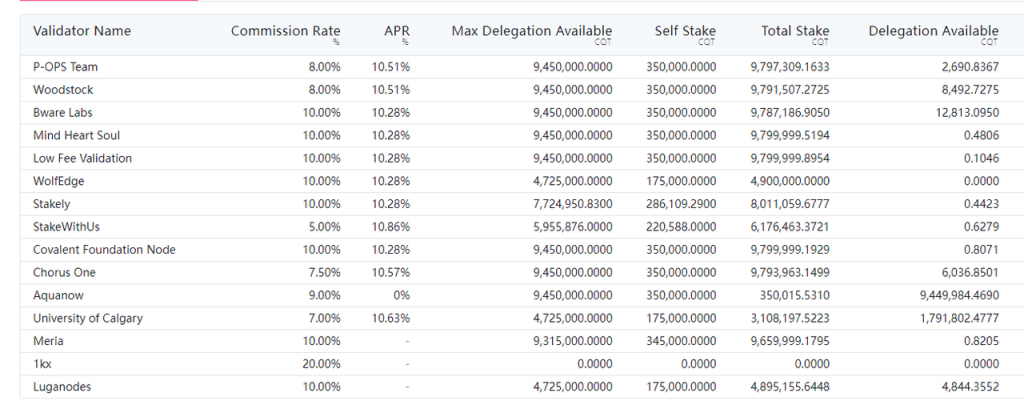

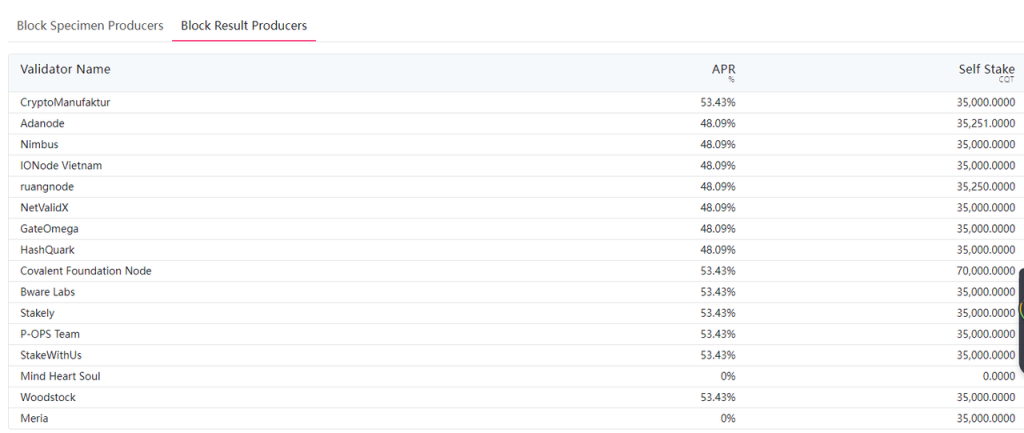

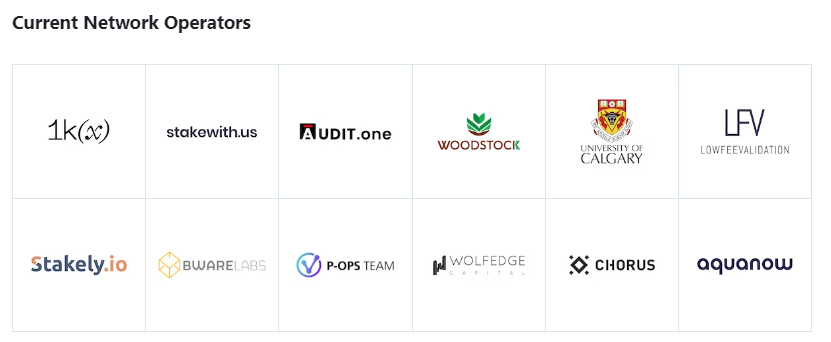

Covalent's decentralized network will have multiple network participants, referred to as "operators." Currently, only two network operator roles are active: Block Specimen Producers (BSP) and Refiners. As of December 2023, Covalent has 15 BSPs, including Chorus One, Woodstock, StakeWithUs, and 1kx.

BSPs extract raw blockchain data and create a data object called a Block Specimen. The BSP standard commitment allows blockchain data to be composable and reusable outside the execution environment. BSPs then upload the block specimens to storage instances, create hashes (or proofs) of the stored block specimens, and publish the proofs to Covalent's ProofChain smart contract on Moonbeam. Once the proof is recorded on Moonbeam, other network nodes can verify the work of the BSP.

The proof and data storage solution based on Moonbeam is only temporary; Covalent plans to launch its own L1 for accounting and will migrate the staking of CQT tokens to Ethereum, with the migration expected to begin by the end of February this year.

The roles set for Covalent's decentralized data indexing network operators are fourfold:

- Block-Specimen Producer (BSP), which is live. When BSPs upload raw blockchain data to storage instances, they can choose to run the instance locally or pay a storage operator to run it. Storage operators should enhance the availability of the proof data through IPFS loading and local storage. Below is the staking situation for BSPs, with the current staking APR at 10%+.

https://www.covalenthq.com/staking/#/

https://www.covalenthq.com/staking/#/

- Refiner, which is live. Refiners take block specimens from storage instances, convert the raw data into queryable data objects called Block Results, and publish proof of their verification work. Below is the list of stakers for Refiners:

https://www.covalenthq.com/staking/#/

https://www.covalenthq.com/staking/#/

- Query Operator, which loads the transformed data into local data warehouses before responding to API queries.

- Delegator, who receives rewards for fulfilling their duties after confirming each proof for a specific period. Before payment, a group of Delegators is randomly selected from the overall pool of network operators to serve as Delegators during the audited period.

Currently, the operators are all roles set by Covalent Foundation's whitelist, which will gradually open to more applicants:

All of the above operators collaborate in a distributed, censorship-resistant manner to achieve data storage, classification processing, query response, and responsibility supervision. In the final network structure, each role has a corresponding token incentive mechanism.

2.2.3 Other Businesses

Ethereum Wayback Machine (EWM)

After the implementation of Ethereum's improvement proposal EIP4844, a new data structure called "blob" will be introduced. Blob data is primarily used to store information that does not need to be permanently retained on the blockchain but needs to be propagated through the network in a short time. For example:

- Batch transaction data: For applications that need to process a large number of transactions (e.g., CEX exchanges processing batch withdrawals), blob data can contain information about these batch transactions, allowing them to be processed effectively as a whole.

- Zero-knowledge proofs: Complex cryptographic proofs, such as zk-SNARKs, may require the transmission of a large amount of auxiliary data. Blob data can be used to store this auxiliary information for validating proofs without occupying too much space on the main chain.

- Off-chain state: For certain scalability solutions, such as state channels or sidechains, it may be necessary to periodically submit snapshots or proofs of off-chain states to the Ethereum main chain. Blob data can be used to contain this state data.

- Large datasets: For decentralized applications (DApps) that need to process large datasets, such as decentralized social media platforms or data markets, blob data can be used to store user-generated content or other large datasets.

- Batch signature information: In some cases, it may be necessary to verify a large number of signatures, such as in multi-signature or batch authorization operations. Blob data can contain this signature information.

As a form of temporary storage on the Ethereum network, whether to retain blob data and for how long is determined by the nodes themselves, which constitutes the "long-term data availability issue" of blob data.

Covalent's Ethereum Wayback Machine is an open-source solution launched to address long-term data availability. Its purpose is to provide decentralized, cryptographically secure historical data for the demand side of blob data, which can be understood as a DA solution.

Regarding the specific technical mechanisms of the Ethereum Wayback Machine, due to space limitations, I will not elaborate here. We only need to know that the Ethereum Wayback Machine also utilizes Covalent's network and data indexing mechanisms to ensure the accessibility and availability of historical blockchain data. By using the Ethereum Wayback Machine, anyone can reconstruct a comprehensive representation of the blockchain and create a database with a standardized model based on it.

For more information about the Ethereum Wayback Machine, you can visit https://www.covalenthq.com/blog/the-ethereum-wayback-machine/.

The product is currently under development and has not yet been officially launched.

It is worth mentioning that the project Ethstorage, which also targets decentralized blob storage, received a $7 million investment at a $100 million valuation in its seed round in July 2023.

Based on the above explanations of product mechanisms and decentralized design, we can summarize Covalent's business model.

2.2.4 Business Model

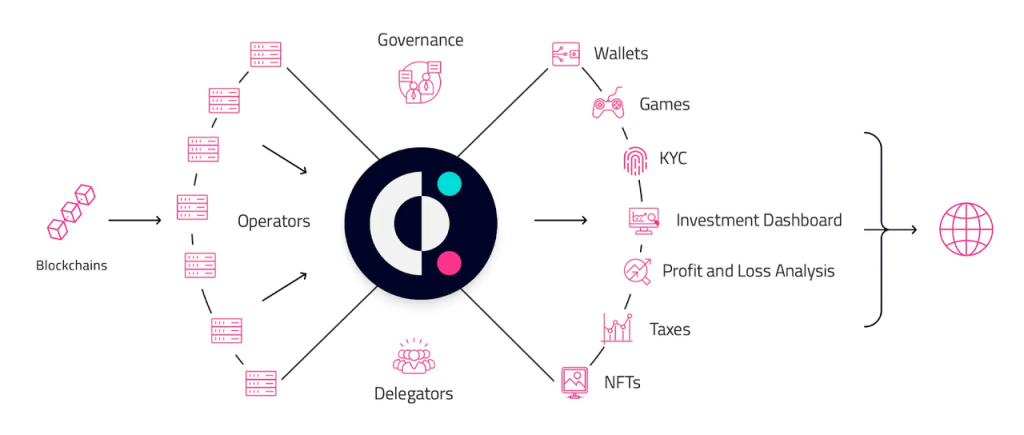

Covalent's business model derives from demand-side payments for data needs (initially through Covalent), with fees paid to network operators, who need to stake the project token CQT to provide services. The specific process is as follows:

When individuals call the API, they will pay in stablecoins priced in USD, such as USDC. The contract will then use these USDC to purchase CQT on the secondary market, driving demand for the token. The CQT is then allocated to the wallets of nodes as rewards for responding to API queries.

- Applications/developers recharge stablecoin assets into the smart contract of the Covalent protocol.

- Applications query the Covalent API.

- Before sending the corresponding query request to the operators, it checks whether there are sufficient funds in the recharge account.

- The query request is sent to the query operator to fulfill the request.

- The required data is sent back to the application.

- The Moonbeam ledger records the data being used, which operators fulfilled the request, and their costs.

- The balance between the network contract, CQT, and the work performed will be reconciled.

- USD funds are deducted from the developer's recharge account, exchanged for CQT through a market purchase mechanism, and then settled with the validator's unsettled balance.

The greater the network's profits, the more operators will want to enter the network, increasing the demand for CQT staking, and the volume of staking and payments will create buying pressure for the CQT token. Of course, operators selling CQT for stablecoins will also create selling pressure on CQT.

Clearly, Covalent's business situation is determined by external demand for data indexing; the more developers and institutions that have data needs, the better its business development will be.

Note that the business switch of "buying into CQT to allocate to operators" has not yet been activated. However, according to official statements, this switch will be activated soon, and the process will be displayed on-chain. At that time, buybacks will occur on Sushiswap, where CQT currently has the majority of its liquidity, facilitating user oversight.

So, what is Covalent's current business status? We will analyze it based on the number of supported chains, user data, pricing and fee situations, and customer situations.

2.3 Business Situation

2.3.1 Number of Blockchains Supported by Indexing Services

Currently, Covalent provides comprehensive historical transaction data for over 211 chains.

2.3.2 Number of Users

2.3.3 Fee Situation

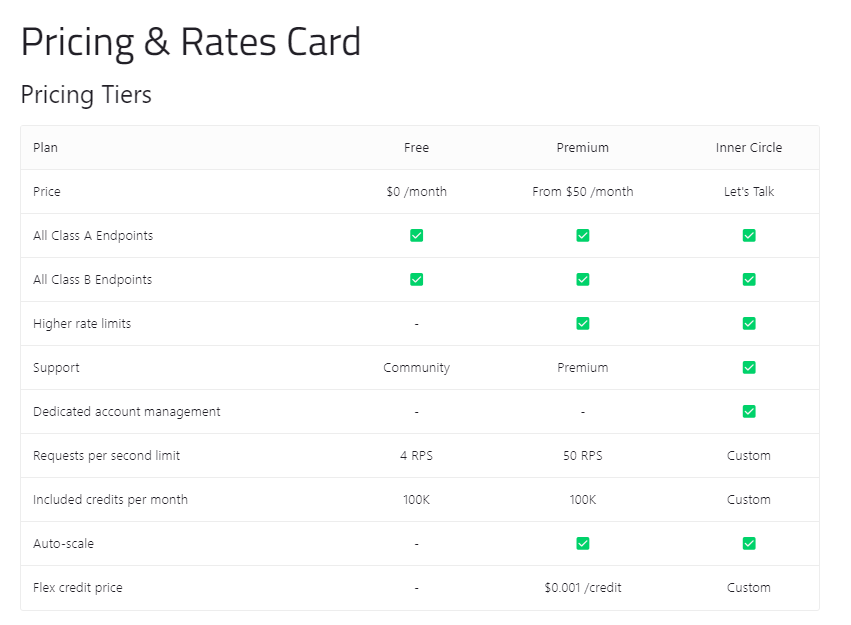

1. Pricing

According to Covalent's pricing list, the platform's minimum consumption unit is "credits," with different query behaviors corresponding to different credit amounts.

Image Source: https://www.covalenthq.com/docs/unified-api/catalog/

Image Source: https://www.covalenthq.com/docs/unified-api/catalog/

Taking a small wallet project as an example, we can estimate its indexing service consumption for one month:

This wallet supports three chains: Ethereum, Polygon, and Optimism, with the corresponding daily active data as follows:

- Ethereum (7,000 daily active users)

- Polygon (3,000 daily active users)

- Optimism (1,000 daily active users)

The application uses the balances_v2 endpoint to provide data to users, consuming 1 credit for each balance call.

This corresponds to a consumption of 11,000 credits/day, 330,000 credits/month.

Assuming it is a premium member, the corresponding consumption would be: premium membership $50/month + (330,000 - 100,000) * $0.001 = $230/month.

2. 2023 Revenue Situation and Comparison with The Graph

Regarding Covalent's overall revenue situation in 2023, I verified the data with the official team, and the feedback was as follows:

- Covalent's revenue from data indexing in 2023 was $600,000, and 2023 was also the first year Covalent officially began commercialization, with initial revenue in January being zero.

- The number of paying users is over 150, with institutions and project parties being the main paying users.

- Revenue is expected to achieve 100% growth in 2024.

In contrast, The Graph, the leading project in decentralized data indexing, has only achieved an annualized revenue of over $100,000 in the past three months.

Data Source: https://thegraph.com/explorer/network?chain=mainnet

Data Source: https://thegraph.com/explorer/network?chain=mainnet

Additionally, the team stated that Covalent's revenue stream data will be launched in the coming weeks, allowing users to see Covalent's revenue situation.

2.3.4 Customer Situation

Covalent's customer base is primarily B-end, with major customer categories including:

Wallets and Data Dashboards: Popular wallets and data dashboards like Rainbow and Zerion use Covalent API to aggregate historical balances and profits of DeFi and NFT assets for their users.

Market Data: Dashboards like CoinGecko can display price trends, liquidity, and asset investment returns.

Cross-chain Projects: Cross-chain liquidity aggregators (like Li Finance) access asset price information across different networks.

Crypto Taxation: Portfolio trackers (like Rotki) can extract cross-chain historical balance and pricing data for tax reporting.

DeFi: Projects like Aave, Balancer, Paraswap, Curve, Lido, Frax, Yearn, etc., integrate user data from different chains.

CEX: To comply with tax regulations, exchanges extract users' historical transaction data to generate reports.

Traditional Finance and Custodial Institutions: The world's largest wealth management firm Fidelity, one of the Big Four accounting firms Ernst & Young, and Jump Crypto.

AI Training and Decision-Making: Providing on-chain data for projects like Nomis.cc (multi-chain identity and reputation protocol) and Network3 (distributed computing protocol) to help train and make decisions for large models.

Other Internet Services: For example, some financial websites that wish to display NFT and DeFi positions across different networks. These clients will be able to leverage Web3 without investing in additional infrastructure (i.e., running nodes, writing smart contracts). Instead, they will be able to access on-chain data using SQL.

Analysts: Covalent's no-code solution reduces the friction for analysts in building complex dashboards and conducting downstream analyses regarding compliance, risk, or taxation. In analyst mode, all requests and responses turn into an Excel-like experience that can be exported as CSV and Tableau.

Additionally, Metamask, Infura, and Linea's parent company @Consensys are also Covalent's clients.

Besides Covalent's direct sales channels, since last year, Covalent has begun collaborating with other upstream RPC service providers like Chainstack, QuickNode, and Infura to offer data indexing services to their users through these partners. Currently, the user payment amount generated through the Infura channel has already reached six figures.

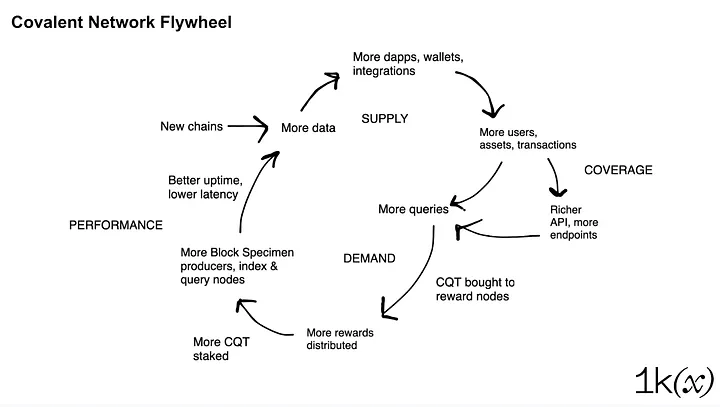

2.3.5 Business Flywheel

Image Source: https://medium.com/1kxnetwork/indexing-the-universe-of-blockchains-with-covalent-7a9686783dc1

Image Source: https://medium.com/1kxnetwork/indexing-the-universe-of-blockchains-with-covalent-7a9686783dc1

In a report written by Covalent's investment firm 1KX, a self-reinforcing flywheel for Covalent's business development was envisioned. In simple terms: low latency, rich data indexing → more B-end clients, Dapps, wallets, and institutions integrating → more C-end user requests → larger indexing volume and rich indexing demand → more CQT buyback distribution rewards → more network nodes and CQT staking → better, richer data services and low latency.

2.4 Team, Financing, and Partner Situation

2.4.1 Founders and Team

Covalent was founded and is led by Ganesh Swami and Levi Aul.

Ganesh is a physicist with over 10 years of data analysis experience; his first company went public on the New York Stock Exchange, and he is also a professional Everest climber. Levi established the first Bitcoin exchange in Canada and was one of the members of the IBM team that built CouchDB. The team currently consists of approximately 40-60 people, including network architects, data scientists, and software engineers.

Overall, the backgrounds and experiences of the founding team align well with the current project and have a strong track record of entrepreneurial success.

2.4.2 Financing Situation

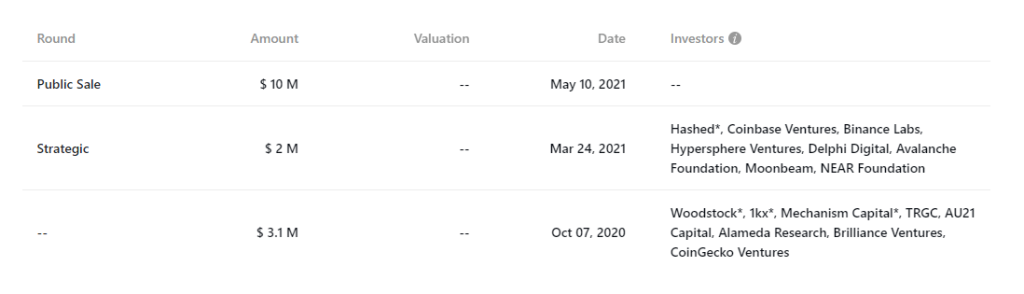

The project has undergone four rounds of financing, with a total amount of approximately $15.5 million.

Image Source: https://www.covalenthq.com/token/

Image Source: https://www.covalenthq.com/token/  Image Source: rootdata

Image Source: rootdata

The investors are also quite prestigious, gathering various top Web3 institutions, including Hashed, Dephi Digital, etc., with both major exchanges Binance and Coinbase having invested.

However, the project's last financing round was in May 2021, and it has been over two years since then.

2.4.3 Important Partners

In addition to various public chains and clients being important partners, at the decentralized RPC summit in Istanbul in November 2023, Infura announced its partnership with Covalent, along with other institutions such as Microsoft, Tencent, and Pokt network.

Through this partnership, Infura will integrate Covalent's API into its existing service suite, ensuring developers have a seamless and efficient experience, eliminating entry barriers, and accelerating development cycles.

2.5 Summary of Project Overview

Overall, Covalent is a leading project in a rapidly developing sector, with various business metrics on a fast upward trajectory and revenue data expanding. In terms of revenue levels, Covalent has several times the income of the current leading project in the sector, The Graph, suggesting it has achieved a better PMF (Product Market Fit). However, since its revenue streams have not yet been on-chain, there may be a significant cognitive gap among market investors regarding this.

In terms of new business, its developing Ethereum Wayback Machine serves as a long-term blob DA solution, which aligns well with current market trends.

Regarding the team, the founding team possesses professional backgrounds and entrepreneurial experiences that match the sector, and the investors include various leading industry players, including public chain foundations, major exchanges, and key clients.

3. Token Model

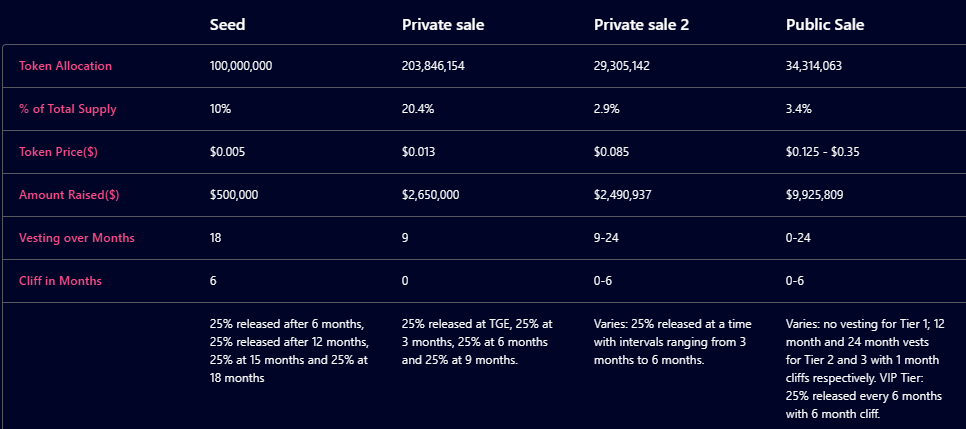

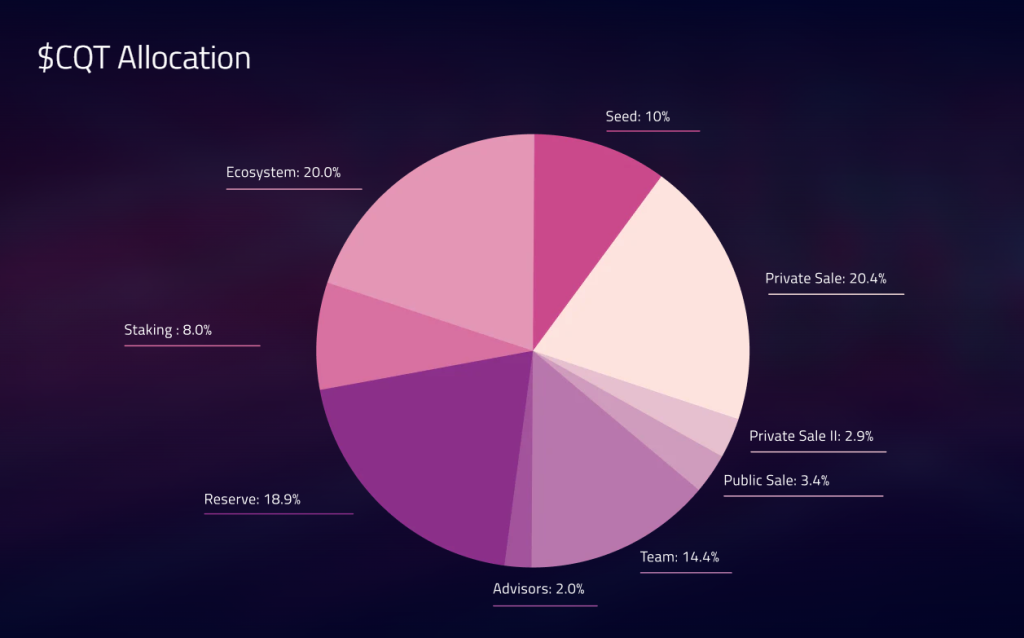

3.1 Total Token Supply and Distribution

Covalent has a total token supply of 1 billion, with the specific distribution as follows:

- Token Sale: 33.4%

- Team and Advisors: 16.4%

- Reserves: 18.9%

- Staking Rewards: 8%

- Ecosystem: 20%

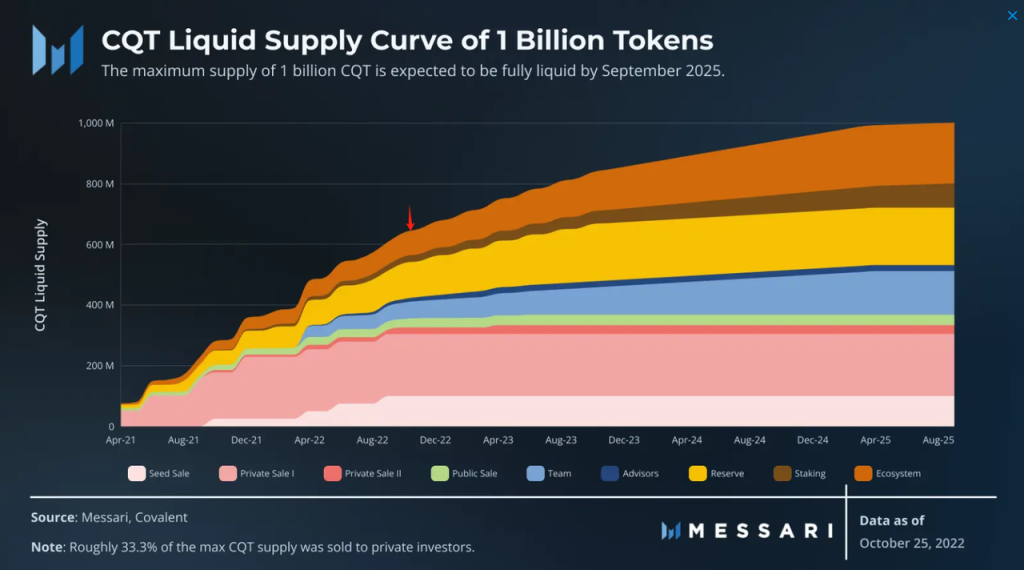

Currently, the token circulation rate is 62.5%, positioned as follows:

Data Source: https://messari.io/report/covalent-a-unified-api-for-retrieving-blockchain-data

Data Source: https://messari.io/report/covalent-a-unified-api-for-retrieving-blockchain-data

3.2 Token Use Cases and Demand

- Governance: Token holders vote on proposals to change system parameters, such as new data sources, specific geographical locations, and data modeling requirements.

- Staking and Validation: $CQT is a staking asset. Validators earn fees by ensuring the integrity of network data. Token holders can delegate to validators and earn rewards by participating in security mechanisms.

- Economic Settlement within the System: Paying users pay stablecoins to purchase data services, which are exchanged for CQT from the market and distributed to staking and operational network operators.

- Staking Rewards: Staking CQT itself will also earn staking incentives, but this portion of income lasts only for four years, aimed at activating early network participants, while the costs of long-term network operations will be maintained by payments generated from actual user demand.

Overall, the economic model design of the token is reasonable, especially considering the payment and budgeting tendencies of enterprise clients: enterprise clients do not wish to hold tokens that are subject to volatility on their balance sheets, namely CQT.

4. Market and Competitor Situation

4.1 Market Layering

There are many participants and layers in the on-chain data market, which we need to categorize.

Among them, service providers based on RPC that offer basic, native on-chain data include centralized representatives like Infura, Alchemy, Quicknode, etc., while decentralized RPC service providers include Pocket network. In fact, they are upstream of Covalent, and Covalent network operators also obtain raw data from them.

Covalent belongs to the data indexing layer, which is the processing and re-output layer after obtaining data. In this layer of competition, there are competitors such as @Bitquery_io, @etherscan, @MoralisWeb3, @blockvisionhq, but they are all centralized, while the decentralized indexing service provider that has introduced tokens is The Graph.

The relative value of the decentralized data indexing layer lies in providing stronger censorship resistance, openness, and verifiability of data sources and construction methods. The distributed working method also makes the system less prone to single points of failure.

4.2 Competitor Comparison

Compared to The Graph, Covalent's differences mainly lie in:

- Different Data Processing Methods

Covalent follows the Extract-Load-Transform (ELT) data integration paradigm, where the network extracts data from the blockchain and loads it into data warehouses. Customers then transform it as needed during queries to support the required data. In contrast, subgraph-based indexers (The Graph) follow the Extract-Transform-Load paradigm, where extracted data is first transformed into subgraphs for specific use cases.

Specifically, the benefits include:

- Flexibly handling downstream demand changes. Since data is non-destructively normalized (extracted-loaded) before querying (transforming), users only need to change the query to obtain different types of analytical data. If the protocol's smart contract is upgraded, Covalent users only need to re-query the comprehensive dataset without needing to modify and re-index subgraphs as in the ETL paradigm.

- Flexibly handling upstream demand changes. As blockchains become more heterogeneous, the Block Specimen standard ensures that Covalent's unified API can query directly, even for chains with different transaction receipt formats and non-EVM chains. In the ETL paradigm, customers need to rewrite subgraphs for chains like EVMOS or Solana, but in Covalent, they only need to patch these chains once to comply with the Block Specimen standard.

- Lower operational costs for customers. With Covalent's ELT-based approach, customer costs mainly come from analysts and IT operations personnel writing queries, rather than developers building and maintaining subgraphs. Covalent eliminates redundant data engineering work, allowing teams to focus on analytical work, thus helping them make more informed business decisions.

- Ability to handle queries that require data from the entire chain. This is also why Covalent is very popular in portfolio tracking and tax reporting applications. The fact that all data is provided through a unified API makes Covalent suitable for machine learning efforts, such as address classification and clustering. With this, developers can also use the API as a single point of integration to build a range of data-driven applications.

- Achieving truly chain-agnostic data consumption. Covalent's block specimen producers will become full node operators of the source blockchain, extracting and normalizing on-chain data before publishing it to storage nodes. Query nodes read data from storage nodes to respond to external API requests. This means customers can use the same queries on data that is very different from its original form, which is a powerful feature for dapps to become cross-chain native.

- Differences in User Demands

Applications using Covalent often require versatile, widely applicable data, which typically does not need the highly specialized and diverse datasets constructed by subgraph developers of The Graph. Applications in areas like wallets, NFT markets, and tax services are more likely to use the official data API launched by Covalent. Meanwhile, if an application relies on niche market and scenario data, it may lean towards using The Graph.

- Ecosystem

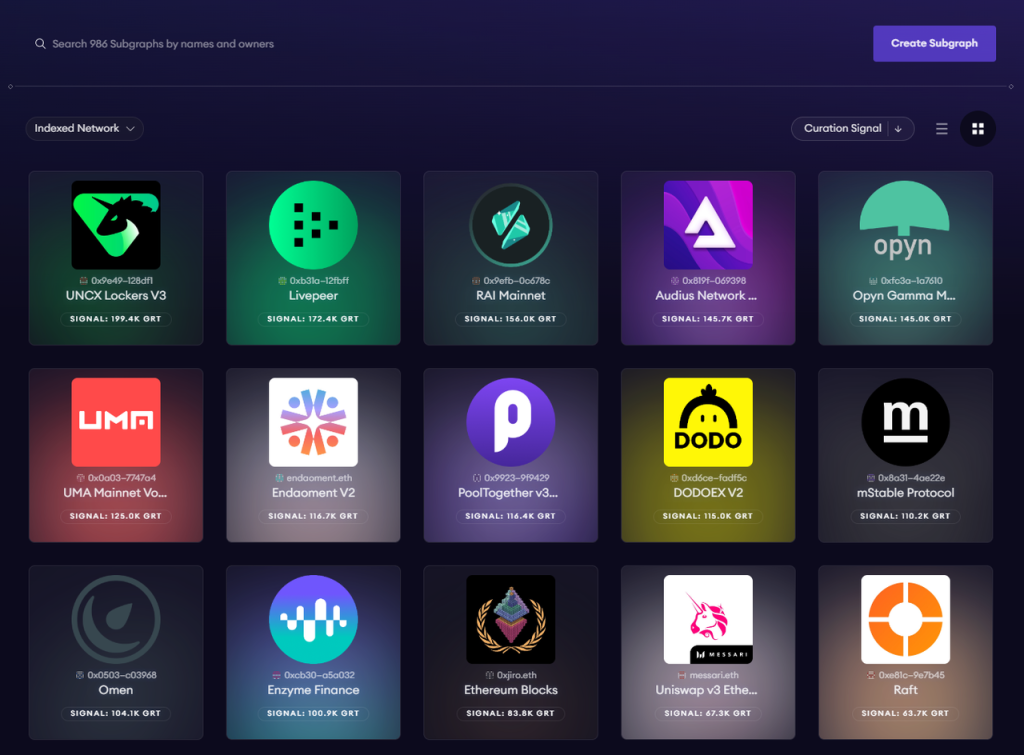

Image Source: https://thegraph.com/explorer?chain=mainnet

Image Source: https://thegraph.com/explorer?chain=mainnet

Number of Subgraphs: The number of third-party self-built subgraphs on The Graph far exceeds the number of Covalent's third-party endpoints. The number of subgraphs supported on both arb and eth chains by The Graph has reached over 1500, while Covalent has only a few dozen, which is related to its recent start of opening third-party endpoints (similar to subgraphs).

Number of Networks: Covalent supports over 200 chains, while The Graph supports over 10, showing a significant difference in quantity. However, the latter covers all major business chains.

5. Valuation

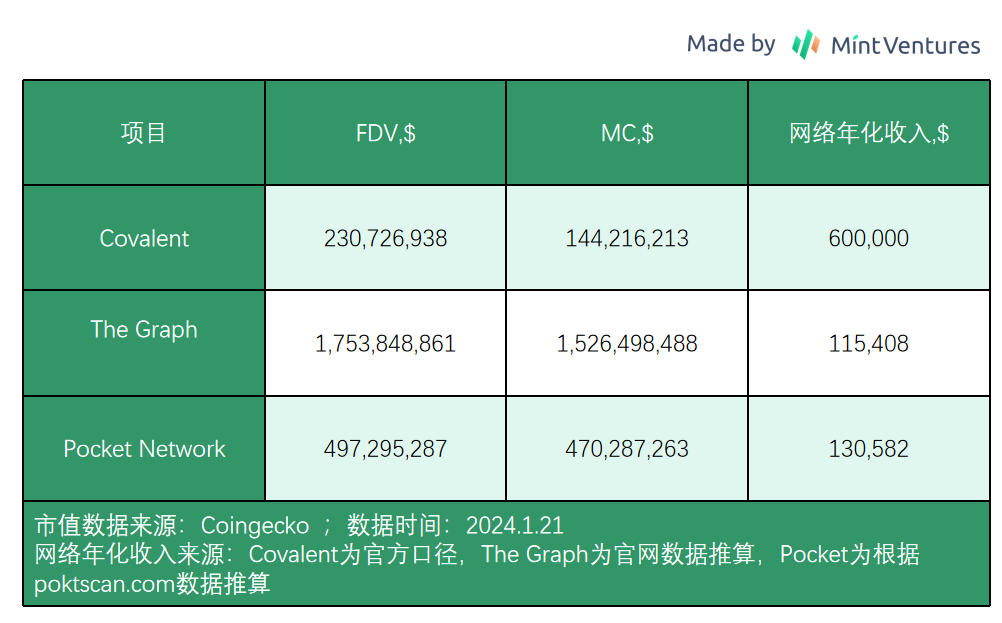

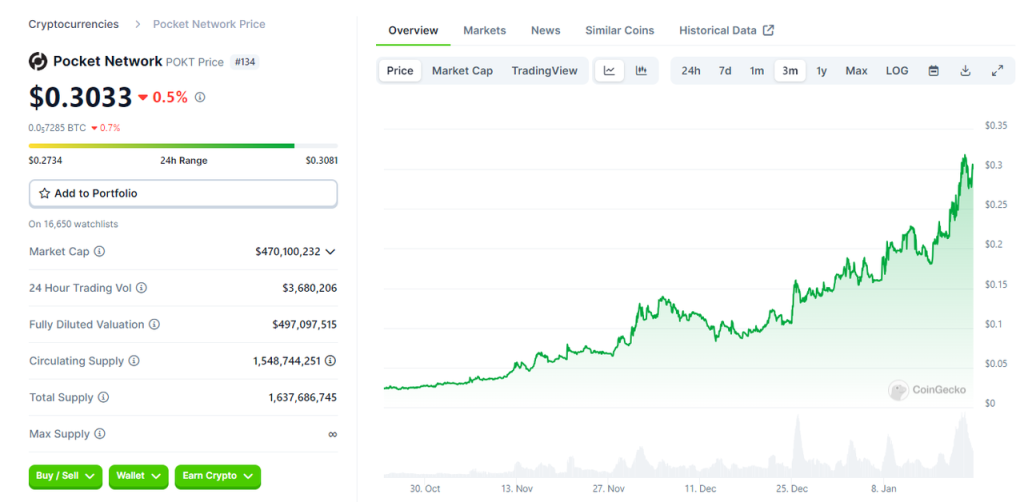

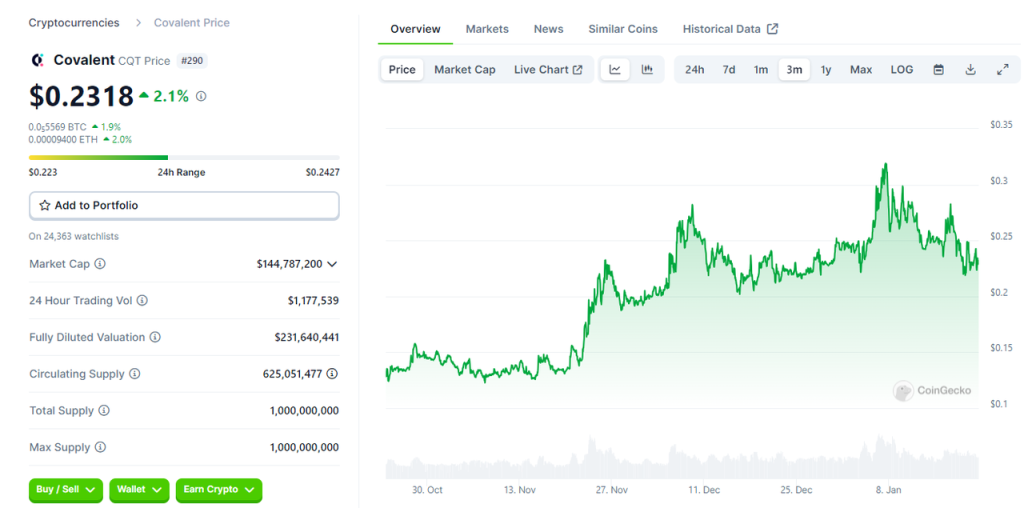

In terms of valuation, I mainly use comparative valuation, selecting two decentralized data service projects in the same sector as Covalent for comparison: The Graph and Pocket Network.

The Graph is a direct competitor to Covalent, making its valuation highly relevant, while Pokt, as a decentralized RPC service project, is also upstream of Covalent's industry, making its valuation similarly relevant.

From the valuation perspective, Covalent is still nearly 7 times lower in FDV valuation compared to The Graph. When considering that Covalent's annualized revenue is nearly 6 times that of The Graph, this valuation seems very attractive.

Compared to Pocket Network, Covalent has higher revenue levels but lower valuations, yet both are in the same order of magnitude of valuation—i.e., in the hundreds of millions of dollars. However, Pokt has achieved nearly a 12-fold increase in the past three months, completing an astonishing "value discovery."

In contrast, CQT has only risen about 80% in the past three months, mainly following the market rebound, and has not yet gained significant attention from large funds.

6. Risks

Regarding Covalent, I believe there are two main risks worth noting:

If other centralized blockchain data service providers with larger user bases, such as Alchemy, Infura, Quicknode, etc., enter the downstream data indexing service sector from RPC and offer similar data indexing services, it may squeeze Covalent's market share and pricing. For instance, Alchemy completed the acquisition of the data indexing platform Satsuma in September 2023.

Data indexing is a relatively niche sector with low awareness among general investors, and currently, it has not attracted investor attention. This trend may continue in the absence of hot narratives in the sector.

7. References and Acknowledgments

This article would like to thank Leo and Bruce from the Pocket Network community for their review and feedback.

Messari: Covalent: A Unified API for Retrieving Blockchain Data

1KX: Indexing the universe of blockchains with Covalent

The Graph Data Dashboard: https://thegraph.com/explorer/network?chain=mainnet

Pocket Network Data Dashboard: https://poktscan.com/

Risk warning

Risk warning Risk warning

Risk warning