Is the spring breeze of the re-staking market approaching? A review of potential projects in the re-staking track

With the increase in Ethereum's staking rate, the demand for restaking services has also grown, bringing EigenLayer back into focus. Will restaking become a new breakout point in 2024, and what potential projects are there in the restaking space? This article will take you on a deep dive.

With the increase in Ethereum's staking rate, the demand for restaking services has also grown, bringing EigenLayer back into focus. Will restaking become a new breakout point in 2024, and what potential projects are there in the restaking space? This article will take you on a deep dive.Author: Jian Shu

1. What are the reasons for the resurgence of EigenLayer?

With the approval of the Bitcoin spot ETF, Ethereum has shown positive signs: the expectation of the Ethereum spot ETF approval and the Cancun upgrade have revitalized Ethereum, which had been sluggish for a long time.

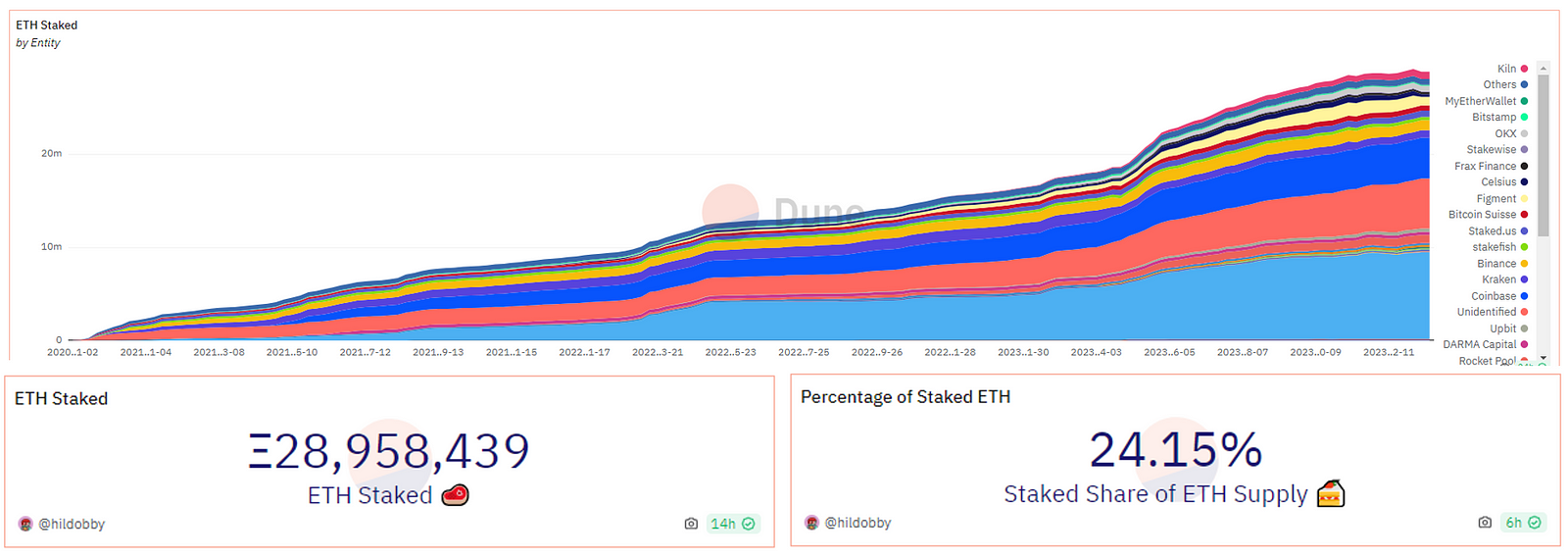

The staking volume of Ethereum continues to rise, and the demand for restaking is becoming increasingly prominent. EigenLayer allows users to restake ETH, lsdETH (liquid staked ETH), and LP Tokens on other sidechains, oracles, middleware, etc., as nodes to earn validation rewards. This way, third-party projects can enjoy the security of the Ethereum mainnet, while ETH stakers can earn more rewards, achieving a win-win situation.

Data source: https://dune.com/hildobby/eth2-staking

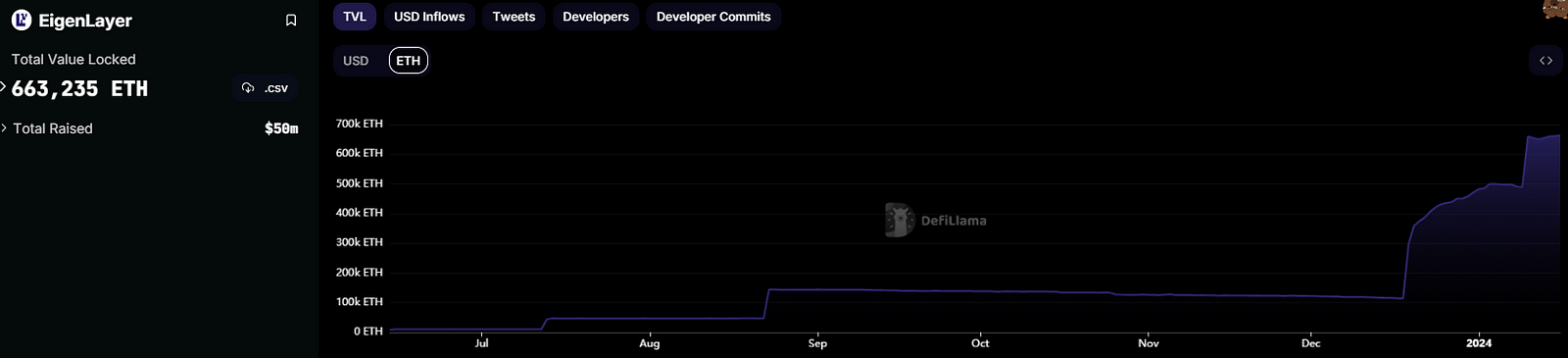

The trend of restaking has become the focus of the Ethereum ecosystem with EigenLayer increasing LST collateral limits. In just one month, EigenLayer has absorbed over 500,000 Ethereum, with a TVL exceeding 1.6 billion USD, making it the 12th top protocol on the Ethereum chain.

Data source: https://defillama.com/protocol/EigenLayer?denomination=ETH

Recently, EigenLayer announced that it would provide restaking services for Cosmos subchains, which is significant for both Ethereum and Cosmos. EigenLayer's provision of restaking services for Cosmos subchains allows Cosmos to gain Ethereum's security and opens up a new world of incremental revenue for Ethereum stakers.

The image shows the EigenLayer Universe, source: https://x.com/eli5_defi/status/1746550169183846503?s=20

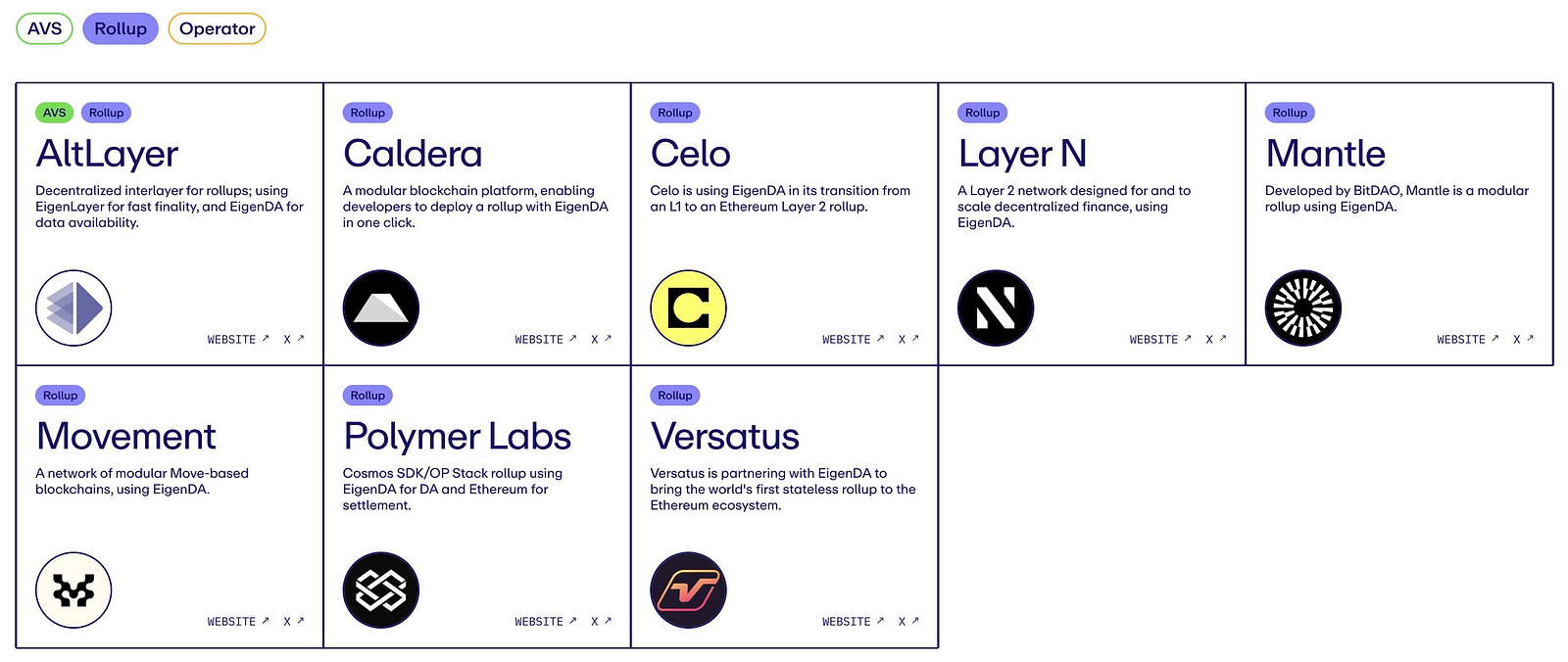

The first project to use EigenLayer's validation services, AVS --- EigenDA, is also about to launch, and its DA service narrative has become a market topic following the surge of Celestia's token TIA.

The image shows EigenDA's partners, source: https://x.com/eigen_da/status/1731674794347860449?s=20

2. What are the potential projects in the restaking track?

The restaking track is not limited to EigenLayer; there are many opportunities under the Restaking narrative. Here’s a brief introduction to the four types of Restaking:

LSD Restaking: Restaking the LST (stETH, cbETH, etc.) obtained after depositing into an LSD protocol back into EigenLayer.

Liquid-LSD Restaking: Through protocols like Kelp DAO, entrusting LST to the LRD protocol, which will restake it in EigenLayer on behalf of the user, who will receive a collateral certificate token called Liquid Restaking Token (LRT).

Native Restaking: Native liquid staking refers to validators using EigenPod smart contracts to redirect their validator withdrawal receipts to EigenLayer.

Liquid Native Restaking: This refers to projects like etherf.fi or Puffer Finance that provide small ETH node services, allowing the ETH within the nodes to be restaked in EigenLayer.

Image source: Delphi Digital, source: https://x.com/Delphi_Digital/status/1740463277099151482?s=20

Below are five unlaunched restaking projects for your reference. All five projects allow users to earn EigenLayer points while obtaining points for their respective projects.

Kelp DAO

Kelp DAO is a Restaking project developed by Stader Lab, a multi-chain supporting LSD project, and falls under the Liquid-LSD Restaking category. It currently accepts deposits of Lido's stETH and Stader's ETHx, but deposits are currently paused due to the full capacity of EigenLayer's LST.

Although Stader Lab has already launched its token, Kelp DAO has introduced a points system, and as a subproject of Stader Lab, Kelp DAO is expected to launch its own token. There is also anticipation for the synergistic effect between SD (Stader Lab's token) and Kelp DAO.

Swell

Swell is an established LSD protocol that recently announced its entry into the Liquid Restaking space, belonging to the Liquid Native Restaking category. After adding the restaking feature, users can deposit ETH to receive rswETH, thus Swell will no longer be limited by EigenLayer's LST capacity.

As Swell has not yet launched its token and has airdrop expectations, its LST token swETH has attracted the attention of airdrop hunters, making it the second-ranked staking asset in EigenLayer. Previously, LSD could earn points, and participating in restaking can also earn points.

ether.fi

ether.fi is a Liquid Native Restaking product that recently secured $5.3 million in seed funding from BitMEX founder Arthur Hayes. Unlike Lido, ether.fi employs a decentralized, non-custodial approach to ETH staking and has announced restaking services. Since it is native ETH restaking, it is not affected by EigenLayer's LST limits and can still accept deposits. Its collateral certificate token eETH (wrapped token weETH) is also one of the few liquid LRT collateral certificate tokens available.

Renzo

Renzo is also a Liquid Native Restaking product and is not subject to EigenLayer's LST deposit limits, allowing deposits to continue. However, it should be noted that ETH deposited in Renzo is currently not redeemable, and the collateral certificate ezETH cannot be transferred, making it locked in the short term.

On January 16, Renzo announced the completion of a $3 million seed round financing, ensuring its security. Compared to similar protocols, it has a smaller locked amount, making it appear more cost-effective.

It is important to note that due to the point rewards for bringing in new users and the undisclosed team background, along with the lack of redemption options, some users have expressed skepticism and distrust.

Puffer Finance

Puffer Finance is an anti-slashing liquid staking protocol, similar to ether.fi, and also falls under the Liquid Native Restaking category. It has not yet opened staking. Puffer Finance has secured a total of $6.15 million in seed funding led by Jump Crypto, with its valuation undisclosed.

EigenLayer requires a threshold of 32 ETH for general Ethereum restaking to operate AVS.

Puffer's restaking feature lowers this threshold to below 2 ETH, aiming to attract small nodes.

3. A different approach: How to use Pendle to participate in restaking?

Pendle is a decentralized interest rate trading market that provides trading for PT (Principal Token) and YT (Yield Token). By trading YT in Pendle, we can accelerate the acquisition of ether.fi and EigenLayer points.

Enter the Pendle YT-eETH trade and purchase YT-eETH. Holding YT-eETH allows you to earn staking rewards, double points from ether.fi, EigenLayer points, and Pendle's trading rewards. Currently, 1 eETH can buy approximately 11 YT-eETH, which is equivalent to 11 times leverage.

The returns look enticing, right? However, after understanding the pricing mechanism of YT, you will realize that the price of YT gradually decreases as the expiration date approaches, essentially trading time for staking rewards and points.

Of course, you can also obtain the above rewards in a lower-risk form by forming LPs, but there are also downsides, such as susceptibility to impermanent loss and relatively low efficiency in earning points.

Note: If you are not very familiar with Pendle, please learn relevant knowledge before proceeding, as this article cannot provide overly detailed explanations due to space constraints.

4. Risks of restaking that cannot be ignored

Restaking, as an emerging concept in the crypto space, is gaining prominence, providing stakers with more opportunities to join different networks and increase their earnings. EigenLayer claims to be the "Airbnb of decentralized trust," highlighting the attractiveness of this opportunity. However, restaking is not without risks; it introduces a series of potential issues that deserve careful consideration.

Slashing Risk: The risk of losing staked ETH increases due to malicious activities.

Centralization Risk: If too many stakers migrate to EigenLayer or other protocols, it could pose systemic risks to Ethereum.

Contract Risk: There may be risks associated with the smart contracts of various protocols.

Layered Risk Accumulation: This is a key issue of restaking, combining the already existing staking risks with additional risks, forming a multi-layered risk.

5. Conclusion

The ETH/BTC exchange rate has seen a strong rebound following the approval of the Bitcoin spot ETF, and with favorable factors such as the Cancun upgrade and the Ethereum spot ETF, the Ethereum ecosystem is also expected to rebound. The main themes for the Ethereum ecosystem moving forward are the Cancun upgrade directly benefiting the L2 sector and the restaking ecosystem of EigenLayer.

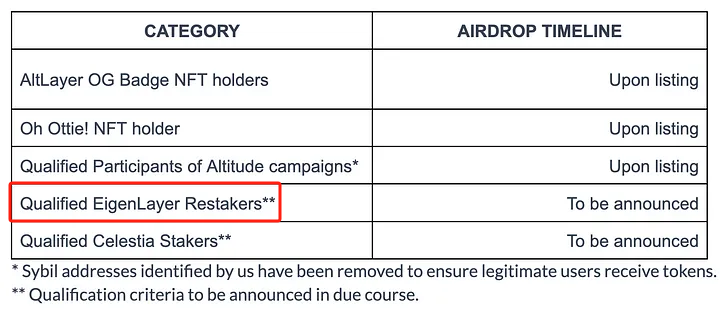

Participating in restaking through the projects mentioned today is undoubtedly the most cost-effective choice, allowing for double or even triple benefits from staking. It is important to note that the recent airdrop rules from Altlayer mentioned that it would airdrop to EigenLayer stakers, but whether staking in protocols like Kelp DAO or Renzo can be recognized as EigenLayer stakers remains uncertain.

Image source: https://blog.altlayer.io/altlayers-alt-token-launch-f49bf8ac2556

Of course, we must also recognize that the continuously nested restaking essentially creates speculative leverage for liquidity. While it brings higher returns, it also amplifies risks; any contract issues at any layer of the protocol could harm user assets.

Glossary

Restaking: Restaking involves staking liquid staked tokens to enhance security while allowing stakers to earn rewards from middleware applications.

AVS (Actively Validated Services): Any system that requires its own distributed validation semantics for verification, such as sidechains, data availability layers, new virtual machines, keeper networks, oracle networks, bridges, threshold encryption schemes, and trusted execution environments.

LSD (Liquid Staking Derivatives): Liquid staking derivatives refer to receipt tokens obtained after staking tokens, equivalent to deposit certificates after depositing in a bank.

LST (Liquid Staking Token): Liquid staking tokens represent tokens staked on POS (Proof of Stake) blockchains, such as Lido's stETH, Coinbase's cbETH, etc.

LRT (Liquid Restaking Token): Liquid restaking tokens are obtained by restaking LST to earn LRT.