Stablecoins are dead

The continuation of the term stablecoin is the best way to protect banks.

The continuation of the term stablecoin is the best way to protect banks.Original author: LUCA PROSPERI

Original compilation: Block unicorn

Inevitably Awkward Financial Markets One of the most confusing concepts I have encountered in my financial career involves the various plays associated with the word "money": smart money------very arrogant, real money------so there is indeed fake money, quick money, tangible money, multiple money------not to be confused with the money multiplier, and so on. Among these money-related descriptions, the money market has always been the most difficult concept for me to understand.

What exactly is the market for trading money? Isn't money itself just a means of payment? Why would I buy money with money? It turns out that these are actually markets for creating money, at least temporarily, rather than normal purchases. My confusion was not a coincidence, as the money market indeed makes opacity one of its core functional characteristics. Sometimes, a little opacity is a good thing.

Block unicorn notes: 1) Quick money refers to ways to quickly trade in liquidity markets, short-term speculation, and short-term high returns. 2) Tangible money refers to physical currency, real estate, and other fixed assets, tangible assets. 3) Multiple money uses a certain amount of initial capital to create greater monetary value through borrowing or other financial instruments, equivalent to continuously leveraging money to mobilize more funds. This kind of arbitrage method often appears in DeFi.

Transparency as a Characteristic of the Money Market

What is the money market (MM)? In short, money market instruments are a short-term/low-risk way in which one party can temporarily store liquidity in a safe place while the other can obtain short-term financing at very efficient interest rates. A large amount of funds is created and destroyed in this way by pledging safe assets between financial institutions and central banks. Money market instruments are ubiquitous, and because of this, their operation is very different from most other markets.

I am not the first to point out that the observable operation of the stock market often leads participants to imply that all markets should operate under similar premises. In BIS (Bank for International Settlements) working paper 479, Bengt Holmstrom (Nobel laureate in economics) excellently depicts how one of the money markets is structurally distanced from price discovery to fulfill its key functions. Money market instruments are indeed built on "no questions asked"; these markets are very large, almost ubiquitous, and operate too quickly to accommodate too many questions. Therefore, a well-functioning (i.e., with good liquidity and resilience) money market is actually built on a satisfactory foundation of opacity, where users ignore the details and specifics behind the instruments themselves and continue with their lives. This is in contrast to the stock market, where price discovery is crucial. In Holmstrom's words------the focus is on my:

The primary goal of the stock market is to share and allocate overall risk. To achieve this effectively, a market skilled in price discovery is needed. Information will quickly reflect in prices, and since prices are common knowledge, beliefs will not tend to favor either side; because prices are public information, it is difficult for those relying solely on price information to profit.

The purpose of the money market is to provide liquidity to individuals and companies. The cheapest way to do this is to use over-collateralized debt, thus eliminating the need for price discovery. With no need for price discovery, the demand for public transparency is much lower. Opacity is a natural feature of the money market and can enhance liquidity in certain cases, as I will discuss later.

Good money is (over-collateralized) debt → If money, as we have reminded readers countless times, is debt, then well-functioning money is usually significantly over-collateralized debt. By using a sufficiently large buffer, the money market avoids time-consuming negotiations, thus enhancing liquidity. We can say that in the money market, ambiguous information benefits both parties------at sufficiently large collateral ratios, private information about the true instantaneous value of such collateral is completely irrelevant, and transactions can be facilitated.

In determining this collateral ratio, the lender's goal is to impose sufficient punitive pain in the event of borrower default. On the other hand, the borrower has the incentive to minimize this collateral ratio to improve capital efficiency (well-intentioned borrower) or engage in fraudulent activities (malicious borrower). While this is a case for any debt market, in the money market, such negotiations are even more important for both liquidity and the universality of debt claims. All these considerations push the collateral ratio toward an exchangeable equilibrium state. This applies not only to the repo market (the most micro money market) but also to more complex money printing institutions, namely banks, where the boundary conditions are broader, being equity rather than collateral ratios.

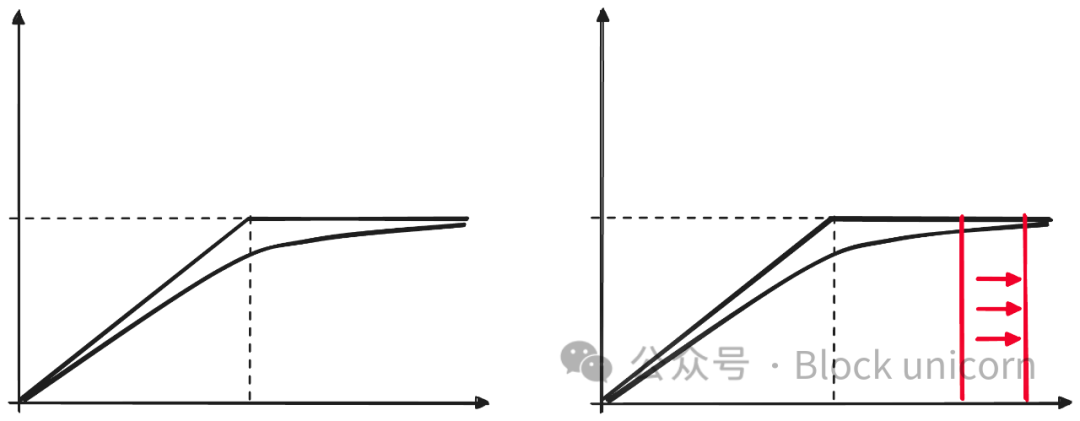

Graphically (see below), information only becomes relevant to collateralized debt instruments near the so-called default boundary, that is, only when the market value of the collateral approaches the boundary. Before this, you do not care about the business practices of your deposit bank until there are signs that you should care. Holmstrom reminds those who prefer terminology that in asset pricing terms, the borrower corresponds to the buyer of some call option (the borrower is like buying a call option, i.e., having a right), that is, having but not being obligated to forfeit the collateral (fixed value) through default at a fixed maturity date, which is why the return curve of debt instruments is concave.

Like other option instruments, the shape of the curve depends on a set of assumptions and structural decisions, and we can use the Black-Scholes model to estimate the default probability of such instruments.

Where N is the standard normal cumulative distribution function, B is the face value of the collateral, D is the default boundary, i.e., the face value of the debt, r is the interest rate, Sigma is the underlying volatility of the collateral, and T is the time to maturity. We can summarize the factors affecting default probability and thus the shape of the red line:

Debt vs. Collateral: In the initial stage, the larger the buffer, the closer the market value is to the face value of the debt, i.e., less sensitive to private information.

Maturity: As the maturity period extends, the value of the option increases because more events become more likely------in the debt market, a longer maturity date reduces the gap between the market value of the debt and its face value.

Interest Rate: Changing the risk-free interest rate affects the time value of money and the value of debt, but is not relevant in this discussion.

Volatility: The volatility of the underlying collateral has a significant impact on the market value of the debt------higher volatility collateral will decrease the market value of the debt, which can only be compensated by a larger collateral buffer.

Structural Implications for Money Market Instruments

The observations above have several noteworthy implications for the structure of the money market, which are of great interest to money users, regulators, and future designers of monetary instruments.

(i) The money market and debt market have different goals → Although money market instruments are a specific type of debt instrument, their primary purpose is to serve the liquidity of the system. This drives an extreme demand for standardization and frictionlessness, which is not necessary in the more general debt market. If debt instruments are some kind of call option, then money market instruments are deep out-of-the-money (or ultra-short-term) call options, extremely insensitive to private information.

(ii) Capital efficiency should not be the primary goal of the money market → Since the advent of DeFi, the idea of capital efficiency has been prevalent in the crypto space and has been used to defend new brand concepts: endogenous collateral stablecoins, low-collateral loan protocols, highly algorithmic money markets, etc. This idea claims that requiring a large amount of collateral to support financial rights is very inefficient, and we should look for (smarter) mechanisms to reduce collateral lock-up. Fairly speaking (to me), I do not oppose (well-intentioned) innovation in financial infrastructure, but we should also ask ourselves what the cost-benefit relationship of each innovation is. Given the central role of money markets in financial intermediation, they are likely to remain the most conservative markets; given their structural ubiquity, core failures in such markets could have devastating ripple effects throughout the economy. Imagine the impact of a U.S. Treasury default on global financial markets, or the structural devaluation of $USDT/$USDC on DeFi.

(iii) Highly volatile (or opaque) collateral is inefficient for the money market → However, there are good and bad ways to improve capital efficiency in the money market. If merely reducing the collateral ratio is a bad improvement, then adopting less volatile/opaque collateral is a good method. In option pricing terms, this means lowering the expected volatility of the underlying reference asset, thereby increasing the curvature of the red line. Unfortunately, from a dollar-denominated perspective, cryptocurrencies do not have (too many) non-volatile collateral------technically, stablecoins are considered more stable assets. Ironically, because debt is structurally more stable in valuation than equity claims, structuring debt against debt is a very good way to build money market instruments------this is precisely what happens in the repo market and is why debt collateral is more prevalent and has a greater impact on the economy, with U.S. short-term Treasuries being the cornerstone collateral of the money market.

(iv) More information does not always lead to better outcomes → In a world where the characteristics of collateral are fully transparent (imagine continuous market-to-market or real-time accounting information on bank balance sheets), private information will become more valuable, and the aforementioned red line will become more unstable, having unpredictable and discontinuous effects on money market claims. As Holmstrom states, "intentional ambiguity is a rather common phenomenon," and "purposeful ambiguity can enhance the liquidity of the money market." Money, as the ultimate money market instrument, is absolutely opaque, which is good enough------until it is not. We ignore the quality of U.S. balance sheets or JP Morgan's quality and do not bother to check the credit default swap curves of the institutions holding our savings. Money is absolutely fraught with many problems, more importantly, the initial positioning of the structure and boundary conditions of claims: if banks start failing one after another, people will begin to care about where they are putting their money.

(v) Invisible risks are risks on the tail → There is no free lunch; creating a system that is normally insensitive to private information (point four) and structurally incentivizes leverage (point three) pushes many risks to the tail. Everything is fine, making people blind to the underlying market structure until problems arise, and then it’s doomsday. In financial engineering terms, panic is an information event: the expected change in the market value curve suddenly occurs, triggering a chain reaction in market structure. This often happens in the money market, and there is already sufficient literature documenting large-scale financial crises. It is unclear whether the rise of the so-called shadow banking issue has actually brought negative effects (due to increased hidden leverage) or has actually acted as a better risk allocator for the entire system. Yes, it makes contagion more seismic, but for a time it increased liquidity and growth through better capital allocation (through better capital allocation). It can be argued that what is happening in DeFi today, creating structures on top of other structures to expand leverage, and arguably improve capital efficiency, bears similarities to the emergence of the shadow banking sector.

(vi) Credible emergency assistance is good preventive measure → Given the structures involved, contagion dynamics seem inevitable, and panic is a reasonable------yet extremely rare cost to pay for liquidity and interchangeability. The best thing we can do is to reduce the occurrence of panic by improving structures and taking safety measures when panic occurs. For a useful money market, emergency assistance may be unavoidable. The question is how expensive these assistances are and who ultimately bears the costs. But these topics are beyond the scope of this article.

Observations on the Timeliness of Stablecoin Tools

Most of the points above can be applied to the current cryptocurrency-backed (so-called) stablecoin tools. Before proceeding, let me clarify: the purpose of this section is not to criticize the status quo but to refine individual mental maps and guide research and construction activities.

CDP (Collateralized Debt Position) is Key → The so-called crypto-native stablecoins become very interesting to economists because they affect the money creation process itself. Maker DAO's collateralized debt position (or CDP) allows anyone with qualified collateral to access the protocol's discount window and mint a fully interchangeable, soft-pegged, dollar-denominated liability. For borrowers, this liability increases the liquidity of their collateral without giving up ownership and upside potential; for lenders, i.e., $DAI holders, this means convenient trading with digitally native stable liquidity tools. The original concept of Maker DAO attracted most of the attention in the DeFi space. We clearly see the analogy between the early over-collateralized $DAI printed by Maker and the more traditional money market instruments mentioned above.

$BTC as Support + Dollar-Denominated Issues → The decision to denominate the liabilities of cryptocurrency money markets (like $DAI) in dollars is more about marketing than financial engineering; however, the extremely high volatility of the underlying collateral (mainly $BTC and $ETH) relative to the liabilities exposes clear weaknesses in the structure. This mismatch issue can only be resolved by adopting strict collateral depreciation, leading to capital inefficiency. This capital inefficiency is unavoidable: while $BTC and $ETH are the most stable crypto assets, they are not stable enough. Almost every other design goes in the same direction, and analysts often point out that these assets lack fixed income, but to me, this is just a minor issue compared to the cost of volatility------though I have not done specific calculations.

Who Will Save Cryptocurrency → We have acknowledged the necessity of having a credible safety valve in place when chaos occurs in the money market, even if it exists beforehand. The dollar money market has such a reliable rescue infrastructure, but what about cryptocurrencies? Today, our best option is to rely on real-world central banks. To my knowledge, no one has designed an ultimate, global safety insurance for DeFi money markets on the blockchain, which could be one of the transformative innovations we need to achieve complete digitization in money creation.

Obsession with Pegging → One of my main issues with the term stablecoin is the excessive emphasis on short-term stability at the expense of other factors. While stability is a good proxy for solvency in the long run, in the short term, it is more related to liquidity. This obsession leads projects to over-invest in secondary liquidity at the cost of stability (see USDT) or to pollute their original designs by introducing dangerous stabilization mechanisms, such as Maker DAO and PSM (Peg Stability Module).

The crypto space is a murky beast where the boundaries between assets and the infrastructure supporting the liquidity of those assets become blurred. Many of our conceptual errors can be traced back to this. Stablecoins sit at the intersection of two worlds, trying to meet the demands of both, and thus they are inherently complex. So, what alternative approaches can be more appropriately applied to useful blockchain constructs?

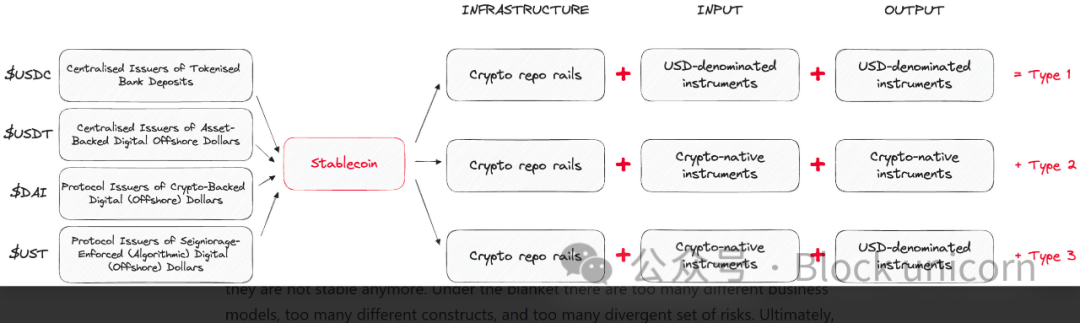

Crypto Repo Channels + Dollar Instruments: Blockchain protocols continue to be used as effective repo channels for non-crypto-native collateral (such as U.S. Treasuries) to issue dollar-denominated money market instruments on the blockchain; to me, this is one of the most powerful use cases today.

Crypto Repo Channels + Crypto Native Instruments: Blockchain protocols serve as effective repo channels, where collateral providers offer crypto-native collateral to obtain new types of crypto-native liabilities unrelated to dollars. This system has many advantages, not least of which is elegance and structural robustness, as, for example, the issuance of $BTC is separated from monetary policy considerations within the ecosystem. The downside is that this construct has almost no application in today’s dollar-dominated world.

Crypto Repo Channels V2 for Hybrid Structures: A construct that only deals with crypto-native collateral to generate dollar-denominated liabilities may not be applicable today, but could be applicable in the future when the digital collateral pool expands or the dollar valuation of digital assets stabilizes. This is a powerful construct, but it is not the reality today.

The term stablecoin is a marketing strategy designed to convey an unverifiable stability with an all-encompassing promise------stablecoins tend to be very stable when they are no longer stable. Under this cover, there are too many different business models, too many different constructs, and too many different risks. Ultimately, the term stablecoin reduces money to a purely payment tool, while I am more interested in how money is created. Regulators and central banks are very clear that it matters who controls the printing press and are trying to perpetuate the idea that "money = payment" (hence the term stablecoin), as this helps to simply confine this phenomenon to the subcategory of digital payments, away from more fundamental issues, and perpetuating the term stablecoin is the best way to protect the banking industry.