2023 Ethereum On-Chain Data Review: On-Chain Activity Focused on DeFi, Liquid Staking Leading New Use Cases

The adoption of L2 has expanded, DeFi occupies the majority of activities on Ethereum, and ETH staking has increased.

The adoption of L2 has expanded, DeFi occupies the majority of activities on Ethereum, and ETH staking has increased.Original Title: "Ethereum Wrapped: An Onchain Year in Review for 2023"

Original Author: J Hackworth

Original Source: mirror

Original Translation: Deep Tide TechFlow

At the end of 2022, the cryptocurrency industry faced the collapse of FTX, and market sentiment was extremely low. Now, the industry is filled with excitement and positivity from cryptocurrency users and developers.

So, what does the on-chain data say about the situation in 2023? This article explores Ethereum's on-chain data to determine which activities and trends impacted Ethereum in 2023.

Facing the Bear Market

Given that we spent most of the year in a severe bear market, it is not surprising that various indicators saw a decline across the board. However, it’s not all bad news.

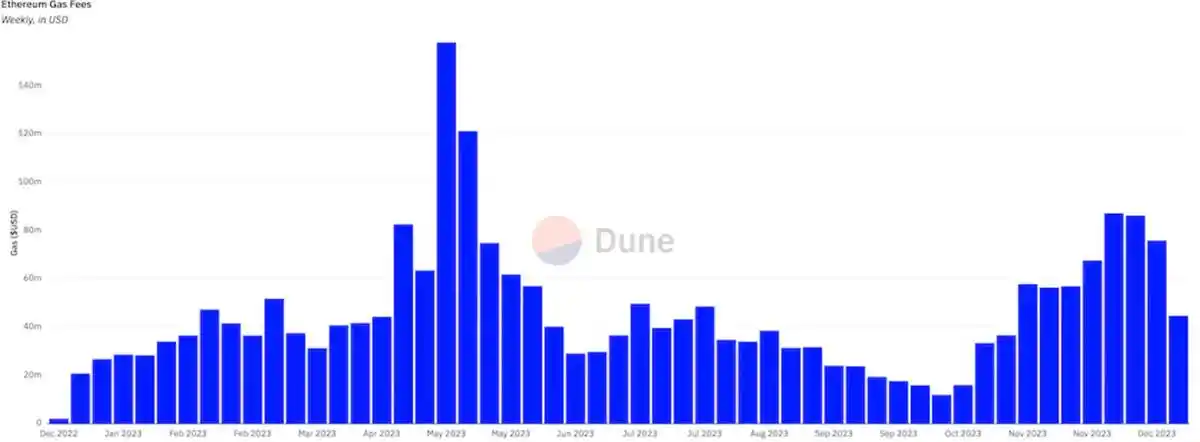

The negative side: In 2023, all major indicators saw a decline. Notable drops include total Gas fees (-26%), NFT trading volume (-59.9%), and DEX trading volume (-35%).

The positive side: By the end of 2023, data showed some recovery. Since the beginning of 2023, TVL has increased by 33%, likely due to the rise in ETH and other token prices. Additionally, despite some indicators not performing well, the situation is improving, including $20 billion in stablecoin inflows since October and a strong upward trend in Gas.

Diving deeper into what happened on-chain, we can see three major trends that shaped the Ethereum ecosystem in 2023:

· L2 Growth

· DeFi driving Gas demand, while NFT interest declines

· Increase in ETH staking

Embracing L2

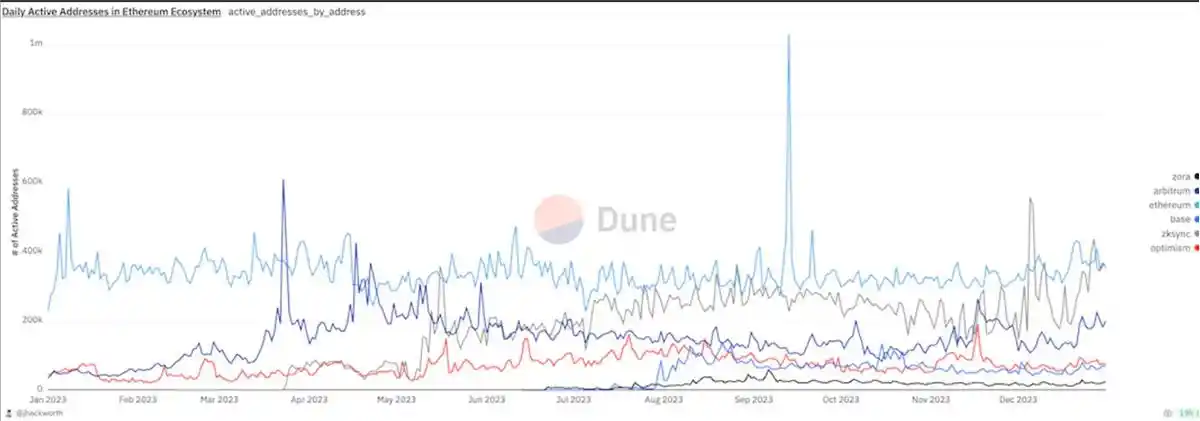

Despite the decrease in Ethereum activity, the use of L2 continues to grow. At the beginning of 2023, there were a total of 16 active L2s with a TVL of $4.95 billion. By the end of 2023, there were over 34 L2s in the market, with a TVL reaching $20.74 billion.

The increase in L2 adoption has led to a surge in activity. The number of active addresses on L2 increased from less than 70,000 to over 400,000, even surpassing the total addresses on Ethereum.

While the number of active addresses on L2 overall exceeds that of Ethereum, no single L2 can match Ethereum: during 2023, there were only 9 days when a single L2 had more active addresses than Ethereum (zkSync, Arbitrum). Therefore, the conclusion is that L2 still needs to further develop its ecosystem and infrastructure to compete with Ethereum's activity.

In 2023, L2 made significant progress by attracting new capital and users, providing cost-effective features for protocols, and allowing the creation of unique applications that are not feasible on Ethereum.

Delving into DeFi Data

Through the charts below, you can see the top ten applications by trading volume this year and the categories classified by Gas. We can draw a clear conclusion: Ethereum mainnet activity in 2023 was primarily focused on DeFi.

You will immediately notice two things:

· USDC and Tether are the two applications with the highest trading volume, accounting for 7% of Gas usage, highlighting the demand for stablecoins on Ethereum.

· DeFi, led by Uniswap, accounts for 41% of Ethereum's Gas usage, emphasizing the important role of DeFi and DEX in Ethereum use cases.

DeFi indeed had a pretty good year. At the beginning of the year, in January, DeFi accounted for about 31% of Ethereum's total Gas, but by the end of the year, it used nearly half of Ethereum's Gas.

Although most of the Gas usage comes from DEX, there are still other strong use cases:

· Maker set a new all-time high in total fees, exceeding $105 million, and reached a historical peak in daily revenue this year.

· Curve and Aave launched new stablecoins, growing by over $103 million and $34 million, respectively.

· Tokenized government bonds are part of the surge in real-world assets, growing to over $450 million on Ethereum within a year.

NFT Trading Cools Down

As DeFi began to occupy more activity on Ethereum, NFT trading activity declined. Data shows that NFT Gas usage on Ethereum dropped from 32% in January to 7% in December, indicating a waning interest in NFTs.

Additionally, in September 2023, NFT trading volume reached its lowest point in two years. However, the recent rise of L2 and interest in NFT use cases suggest that no one can predict what will happen to NFTs in the future.

Staking Data

It is hard to believe from the data that Ethereum's proof-of-stake system has only just surpassed one year.

2023 marked the first year of ETH withdrawals from the beacon chain, leading to a significant influx of funds into staking. In 2023, the supply of staked ETH increased by 82.6%, with about 24% of the ETH supply now staked. 2023 was the year with the largest increase in ETH staking.

As more ETH is staked, it is becoming a key part of Ethereum's next phase of applications and use cases:

· Using LST as collateral in DeFi applications, even earning yields on L2 (like Blast).

· Supporting new stablecoins like Lybra, Prisma, and Ethena, which have a total market cap exceeding $345 million.

· Re-staking ETH through Eigenlayer to provide security for other applications on Ethereum.

As staking and LST become increasingly common, ETH will be used in various ways, and the number of its use cases will continue to grow.

Conclusion

Despite facing many challenges, Ethereum made significant progress in 2023. The adoption of L2 expanded, DeFi accounted for the vast majority of Ethereum's activity, and ETH staking increased. With these trends, Ethereum is laying the groundwork for substantial growth in 2024.