HTX Ventures 2023 Annual Review

Looking back at 2023, the cryptocurrency and blockchain sector has seen a series of significant developments, challenges, and innovations.

Looking back at 2023, the cryptocurrency and blockchain sector has seen a series of significant developments, challenges, and innovations.Authors: Haiyi, Juliet, Gigi, Jenny

Our Journey:

2023 marks a transformative era for Huobi. On the occasion of the company's 10th anniversary, our brand name has changed from the familiar "Huobi" to "HTX." This change is not just a name change but a renewed commitment to our core values. Here, H represents the legacy of Huobi, T signifies our focus on TRON, and X embodies the platform's vibrant characteristics. For HTX Ventures, 2023 also signifies a series of structural upgrades (such as the integration of incubation and research departments) to further optimize resource allocation and strengthen the support system built for our investment and ecosystem partners.

HTX Ventures was established in 2018, dedicated to empowering various projects that leverage the cutting-edge potential of Web 3.0 and crypto technology. Our business covers a wide range of fields, including DeFi, Real World Assets (RWA), ZK Roll-ups, infrastructure, NFTs, Digital Identity (DID), SocialFi, education, GameFi, AI, Layer 1, and Layer 2 projects. We are committed to maintaining a leading position in technological advancement and innovation through diversified investments.

HTX Ventures upholds three core spirits: business innovation, robust business models, and excellent operations. These guiding principles are crucial in our investment strategy formulation process, ensuring that we support not only cutting-edge technological innovation projects but also those that demonstrate sustainable and scalable business models. By combining technological foresight with commercial strategic acuity, we can identify and nurture projects with the potential for lasting impact and growth.

We adopt a comprehensive investment strategy, including direct investments and fund investments, which has significantly expanded our portfolio, now covering over 200 startup projects. This investment strategy not only diversifies our investment fields but also enriches our ability to drive meaningful change across various sectors. Each investment is a testament to our unwavering commitment to fostering innovation, sustainability, and excellence in the vibrant realms of Web 3.0 and beyond.

2023 Market Overview and Outlook

Looking back at 2023, the cryptocurrency and blockchain sectors have witnessed a series of significant developments, challenges, and innovations.

Infrastructure

2023 has been a breakout year for infrastructure. Across the entire infrastructure ecosystem, faced with an increasing number of Web3 use cases and users, a variety of solutions and technological routes have emerged, intertwining and awaiting market validation. Regardless, these solutions consistently focus on three key areas: faster transaction speeds, more decentralized forms, and more secure architectures. The ultimate goal is to create a more user-friendly blockchain network. There are many topics to discuss regarding infrastructure; here we select some noteworthy infrastructure topics from 2023 as a summary.

Five infrastructure topics worth revisiting in 2023:

1. Ethereum Development Roadmap

As the largest public chain, Ethereum is a crucial component of blockchain infrastructure, with a substantial amount of infrastructure relying on its operation, including various Rollup Layer 2 networks and new technologies like account abstraction. Even though Ethereum currently leads all public chains in total value locked (TVL) and user numbers, it still faces challenges such as insufficient throughput and transaction costs that are unsuitable for small, high-frequency trades, which hinder its goal of large-scale blockchain applications in the future. Therefore, Ethereum has been continuously upgrading through forks to enhance its performance. In mid-2022, Ethereum achieved the first milestone of its scaling plan: The Merge, transitioning from a POW consensus to a POS consensus, and more importantly, marking a shift towards a Rollup-centric scaling approach.

In 2023, Ethereum underwent a significant upgrade at the execution layer: the Shanghai upgrade, which primarily allowed stakers to withdraw their staked ETH and rewards. The prevailing prediction was that Ethereum's price might suffer due to a large amount of staked ETH being withdrawn; however, contrary to expectations, Ethereum exhibited strong upward momentum after the upgrade, and importantly, the entire network maintained stable operation post-upgrade, with staked amounts rebounding after a slight decline, indicating a resurgence of validator confidence.

The next important milestone for Ethereum is the anticipated "Cancun upgrade" scheduled for Q1 2024, which signifies Ethereum's move towards its next major goal: sharding scalability. A key proposal, Pro-Danksharding (EIP-4844), introduces Blob data blocks, providing cheaper data availability for Rollup and Layer 1 interactions, thereby reducing transaction costs for Layer 2.

In the second half of the year, Vitalik also raised the topic of "Exit games for EVM validiums: the return of Plasma," attempting to urge people to revisit this forgotten scaling technology. While it sparked lively discussions in the community, there is no doubt that Rollup scaling remains the mainstream route in Ethereum's mainline development narrative. In the future, we may see an Ethereum world where Layer 2 serves as the primary execution layer, with the Ethereum main chain acting more as a consensus layer and data availability layer, providing underlying support for numerous Layer 2 networks.

2. Layer 2 Summer

Layer 2 has been a rapidly developing and highly focused track in 2023. To date, there are numerous Layer 2 solutions in the market. According to data from L2 Beat, there are currently 32 active Layer 2 networks, primarily based on Optimistic Rollup and ZK Rollup. From a TVL perspective, the overall size of Layer 2 has nearly tripled in 2023. In terms of TVL distribution, Arbitrum One and OP Mainnet, both based on Optimistic Rollup solutions, occupy the vast majority of market share, with Arbitrum ONE accounting for 52% of TVL and OP Mainnet for 26.5%. This is mainly due to Arbitrum being the first to achieve EVM compatibility, allowing seamless deployment for Ethereum and other Layer 1 projects. Additionally, the early issuance of tokens by Arbitrum and OP spurred explosive growth in ecosystem projects. In March of this year, following the completion of the Arbitrum token airdrop, its ecosystem TVL saw nearly a twofold increase. In contrast, ZK Rollup public chains have been slower in token issuance and EVM compatibility, resulting in slower ecosystem project growth compared to Optimistic Rollup Layer 2.

Figure 1: Layer 2 Locked Value

In a year where Layer 2 networks flourished, we also observed some issues faced by these networks. One major concern is whether their data growth truly reflects network prosperity or is merely an illusion. Many projects have been incentivizing user interaction with the network through airdrop expectations, and we have seen an increasing number of projects investing effort into designing airdrop rules, including how to combat witch attacks and attract high-quality users. However, we would like to emphasize that airdrops and token incentives, as a "prescription," can be effective while they are in use, but if projects fail to gain genuine user trust in their products, the effects will quickly dissipate once the airdrop or token incentives end. Moreover, current Web3 users still fall far short of the standards of mainstream users. This is because we believe mainstream users tend to be relatively lazy and have low willingness to switch between multiple ecosystems. Currently, users willing to interact on Layer 2 networks generally possess some knowledge and operational skills, leading to increased customer acquisition and retention costs for the ecosystem itself, or what can be termed as "involution." User loyalty to a particular public chain can easily diminish due to competitors' airdrop expectations and liquidity mining incentives. A prime example is the Blast project launched in Q4 by Paradigm and Blur founder Pacman, which integrates the concept of native yield into a Layer 2 network, extending the popularity of Layer 2 into the end of the year, achieving a TVL of $300 million within just a few weeks of its launch. As a project backed by a star development team and prominent institutions, it highlighted community engagement in its track selection, taking Product-Market Fit to the extreme, and providing a unique perspective on the current competitive landscape of Layer 2. While other Layer 2 solutions are still competing on technology and user quality, Blast quickly captured market attention and funding with simple features that align with community consciousness.

Overall, we maintain an optimistic outlook for the future development of Layer 2. With EIP-4844 further enhancing Layer 2 performance, we may see innovative products in DeFi and other non-financial DApps on Layer 2 in 2024.

3. Modular Technology Unlocks Blockchain Bottlenecks

As most public chains continue to strive for faster and cheaper solutions in pursuit of the most "mainstream" public chain goal, another solution has frequently been mentioned in 2023: modular blockchains. Strictly speaking, Rollup itself is also a form of modular technology, focusing on the execution layer of the blockchain, i.e., the user interaction layer. This year, we have seen more developments in modular blockchains that focus on data availability (DA) layers, such as Mantle and Celestia. The former, as a modular Rollup, utilizes its own data availability layer to liberate Layer 2 from Ethereum's data availability constraints, while Celestia has built a universal modular blockchain that allows blockchains built on Celestia to use it as a data availability layer. We believe that modular technology brings greater freedom, allowing applications or Layer 2 to be unbound from the performance of the main chain, gaining greater autonomy and customization. There is significant room for imagination in this space. Although there are currently not many practical use cases for modular blockchains like Celestia, we are optimistic about the development in this direction.

Of course, we cannot overlook the complexity and security issues that come with advancements in modular technology. This is not only reflected from the user's perspective, as understanding the performance of a single blockchain is relatively easy, while users of modular blockchains need to comprehend the interactions with other modular layers. At the same time, for developers, modular blockchains expose more risks in terms of security due to the involvement of multiple chains interacting with each other.

4. Current State of Application Chains

After the last DeFi Summer, application chains emerged as a new approach to address network congestion and lack of autonomy, exemplified by the decentralized perpetual contract dYdX, which was originally deployed on Starkware. In October of this year, we witnessed the mainnet launch of dYdX V4, marking the official transition of dYdX from an application to an application chain. Architecturally, dYdX chose the Cosmos SDK, which is currently the mainstream application chain architecture, allowing application chains to customize consensus mechanisms based on real-world needs and complete cross-chain interactions with other chains in the Cosmos network through the IBC protocol. Currently, there are over 70 application chains deployed on the Cosmos network, making it a mainstream implementation solution for application chains in the market.

The main advantages of applications developing their own application chains include:

- Performance Improvement: If an application chain is built on the Cosmos network, it can fully leverage Cosmos's 10,000 TPS speed advantage. Additionally, since it does not need to compete for block space with other applications, the environmental impact on the application itself will be minimized.

- Cost Reduction: In terms of transaction costs, application chains also have significant advantages. For instance, in dYdX, an important change in V4 is the redesign of gas fees, where users do not have to pay a fixed gas fee but will be charged a proportionate fee based on their trading volume, making the trading experience more akin to that of centralized exchanges.

- Enhanced Autonomy: The enhancement of autonomy includes various aspects, such as smart contract upgrades, data availability, and sequencer settings. Application chains have the capability to customize solutions in these areas based on application needs.

However, applications transitioning to application chains also face some challenges, including:

- Liquidity Isolation: Independent application chains increase the difficulty for external protocols to interact with the application. In Ethereum or other monolithic blockchains, the cost and threshold for interaction between applications are very low. However, application chains, being independent of other ecosystems, make cross-chain interaction the only way to engage with other ecosystems.

- Security: The consensus security of smart contract applications is directly influenced by the security of the blockchain on which they are deployed. Theoretically, the so-called security essentially depends on the market capitalization of the public chain, and for application chains, their own market capitalization determines whether their protocols can support the assets above. This is not friendly for some low-market-cap projects.

Therefore, we believe that application chains are not a suitable development route for all applications. For example, for projects that frequently need to interact with other contracts and have a relatively small market cap, staying on a secure and prosperous public chain is a wiser choice. In contrast, for projects that require fast, low-cost trading experiences, are dissatisfied with the limitations of public chains, and have a certain user base, application chains indeed represent a way to maximize the value of their protocols.

5. Account Abstraction Opens the Door to Hundreds of Millions of Web 3.0 Users

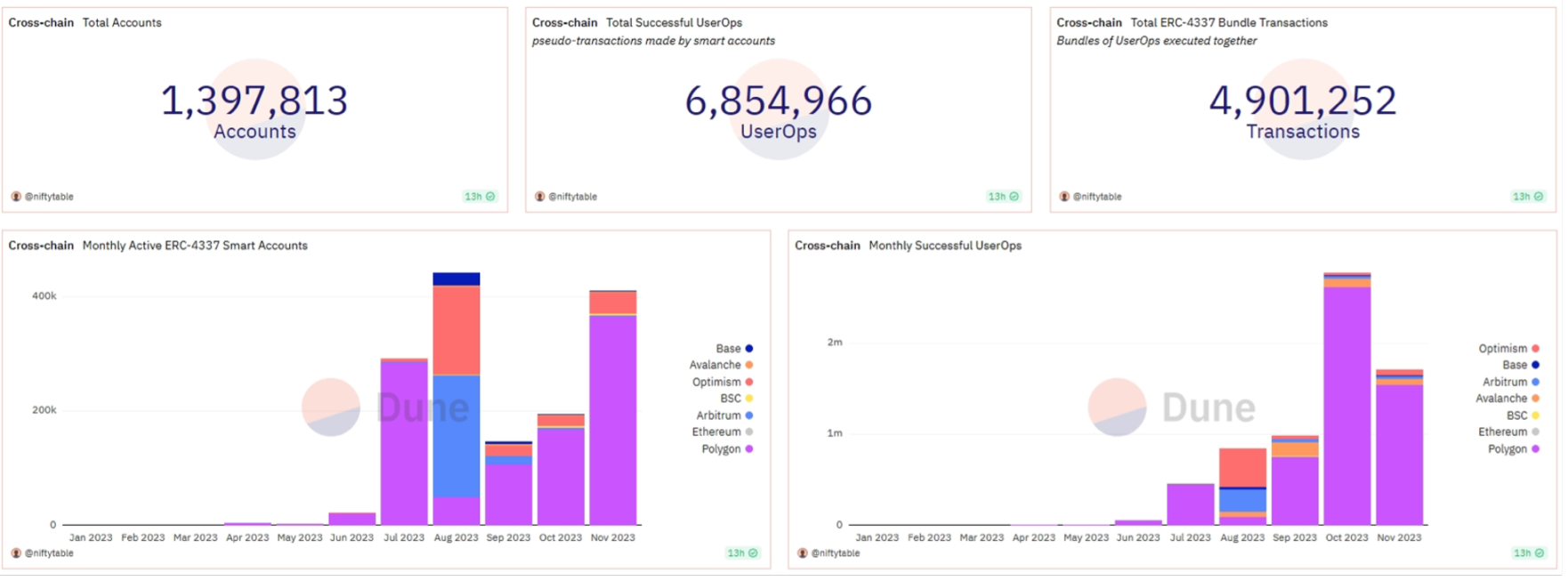

The concept of account abstraction first emerged in 2022, and with the update of EIP-4337: Account Abstraction Using Alt Mempool (a proposal for account abstraction that completely avoids changes to the consensus layer protocol and relies on higher-level infrastructure), many teams began to develop products around account abstraction. In terms of end products, the current direction mainly includes smart contract wallets that achieve social login, social recovery, gas payment on behalf of users, and batch transaction processing through integrated account abstraction. Many teams have delivered products in 2023, including Argent, Avocado, and Unipass, all of which have made significant innovations in user experience. According to Dune data, there are currently nearly 1.4 million accounts created based on EIP-4337 across the entire chain, generating nearly 7 million transactions (UserOps). As of the publication of this article, there are over 400,000 active smart contract accounts each month.

Figure 2: Adoption of ERC-4337 Smart Accounts, Source: Dune.com

Looking ahead, we believe that account abstraction can open the door to large-scale applications in Web3. However, account abstraction still faces some challenges, including increased security risks due to a more complex tech stack and rising gas fee rates. Therefore, we also believe that Layer 2 and other low-fee public chains are the best soil for developing account abstraction technology.

DeFi

Compared to multiple incidents of collapse in 2022, 2023 has been a period of stable development for decentralized finance (DeFi). In terms of protocol variety, there are currently over 30 DeFi protocols, and compared to last year, the market has become more segmented and specialized. The narratives around LSD and RWA have brought new users and attention to DeFi. Below are some DeFi topics we believe are worth noting.

Three DeFi topics worth revisiting in 2023:

- Current State of DeFi Protocols

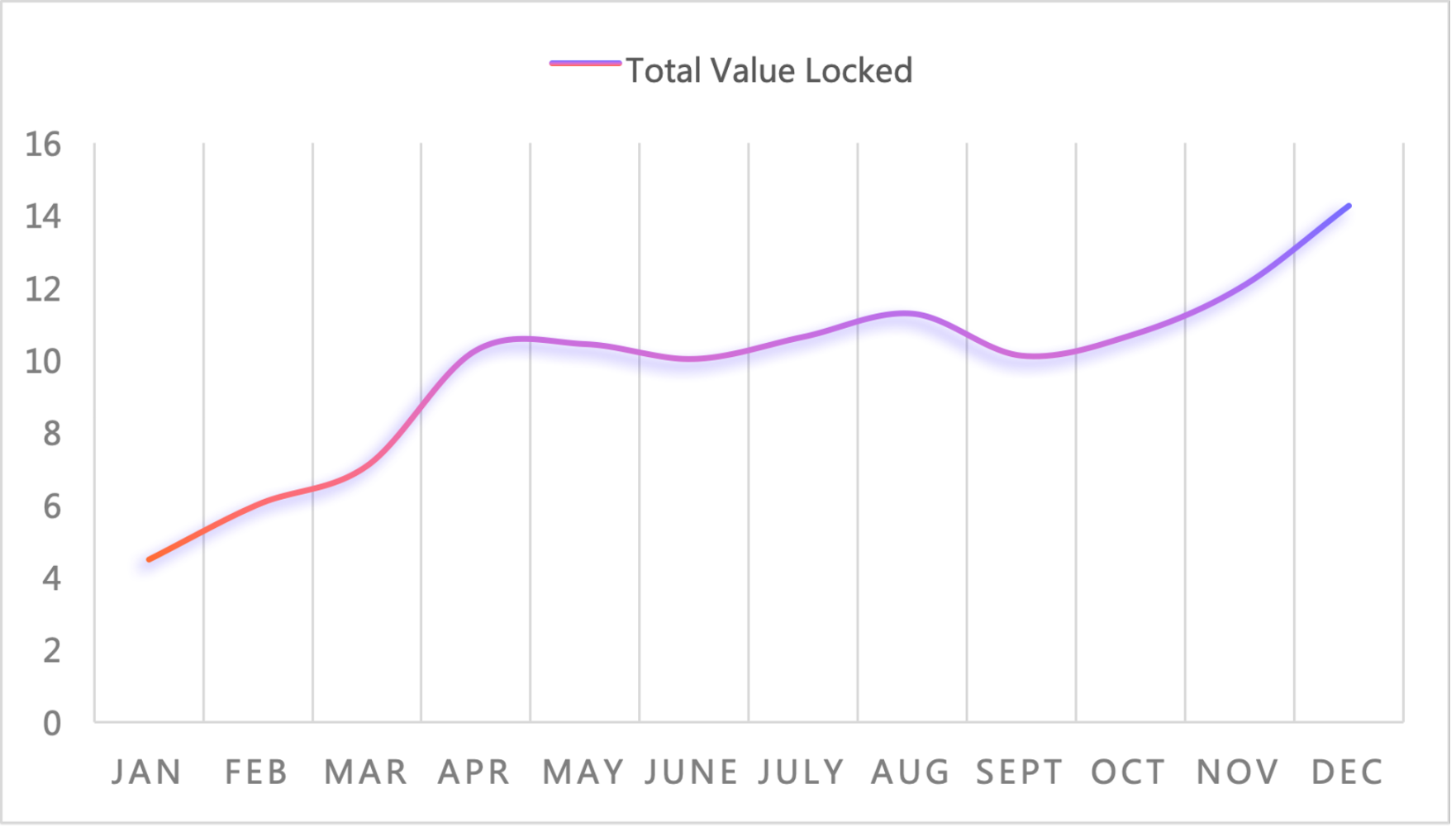

In 2023, DeFi has shown a stable trend in total value locked, with $47 billion locked in DeFi contracts as of the publication of this article, a 23.6% increase from $38 billion on December 31, 2022.

Figure 3: Total Locked Value, Source: Defillama.com

In terms of public chain share, Ethereum accounts for 56%, holding an absolute advantage, while TRON accounts for 16%, ranking second. In terms of projects, Lido, Maker, and Justlend rank in the top three for TVL, with Lido's TVL accounting for 41% of the total TVL across the chain.

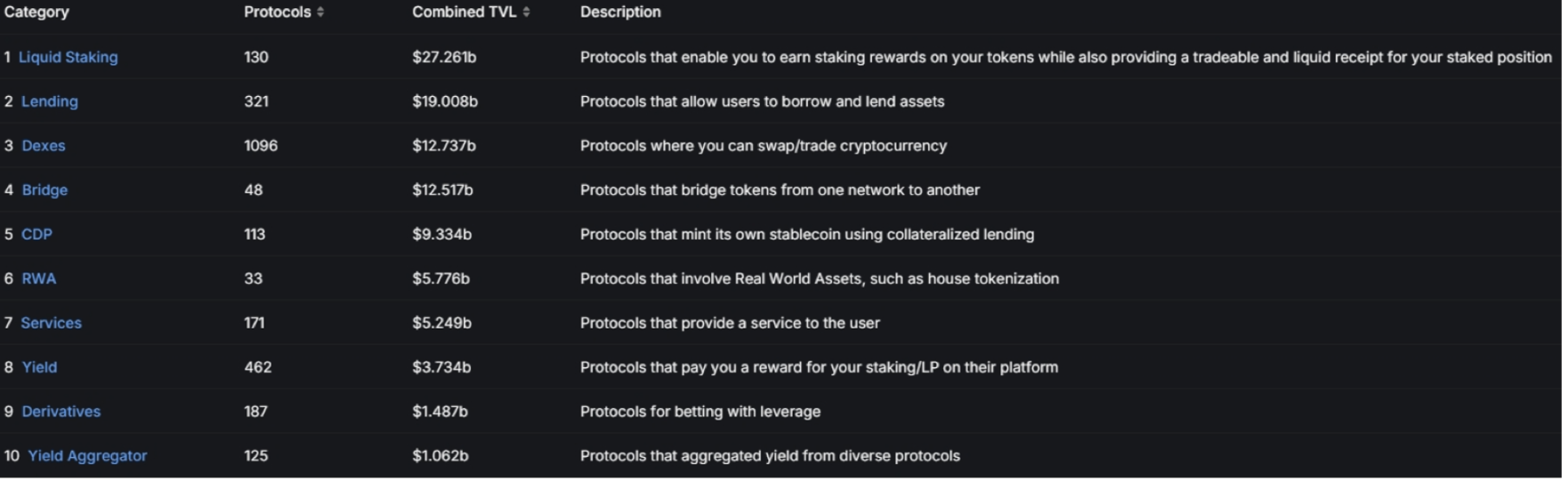

In terms of revenue, Maker ranks first with a daily income of $500,000. Among the top twenty revenue-generating projects, eight are exchanges or derivatives exchanges, and three are lending protocols. Exchanges and lending protocols remain the leading types of protocols for capturing value in DeFi, and the competition is, of course, the fiercest. According to statistics, there are currently over 1,000 decentralized trading protocols distributed across 234 public chains.

Figure 4: DeFi Categories, Source: Defillama.com

2. Real World Assets (RWA)

RWA (Real-World Assets) is a new DeFi theme that cannot be overlooked in 2023, attracting significant attention in a relatively sluggish market. Generally speaking, RWA mainly focuses on enabling the on-chain representation of real-world assets through off-chain and on-chain verification, transferring off-chain assets and their accompanying yields onto the chain. As a form of RWA, legal stablecoins have already demonstrated their important use cases in the cryptocurrency market, while other RWA assets tied to real-world assets have seen explosive growth in 2023. MakerDAO's RWA for U.S. Treasury bonds has already reached a scale of $2.8 billion, marking the first step towards large-scale application of RWA. Avalanche is also attempting to provide a good on-chain platform for traditional institutional capital by developing an RWA ecosystem.

The macro backdrop here is the Federal Reserve's interest rate hikes, with U.S. Treasury yields rising to 5%. In 2023, when overall yields in the DeFi market are at low levels, transferring real-world yields onto the chain is a natural progression. Of course, the future advancement of RWA requires substantial off-chain infrastructure, improved regulation, and advancements in on-chain oracles, wallets, and cross-chain technologies. Nevertheless, the door to on-chain representation of real assets has been opened, and we have the opportunity to see more RWA asset potential in 2024.

3. Decentralized Stablecoins

For mainstream stablecoins like USDT and USDC, there has always been criticism regarding their overly centralized risks. Currently, USDT and USDC account for over 90% of the market share, and the USDC de-pegging incident in March heightened discussions about the risks of centralized stablecoins. The crypto market has been continuously attempting to create a native crypto stablecoin that minimizes traditional world risks. As of now (November 29), there are over 120 stablecoins issued using over-collateralization (CDP), and one trend we observed in 2023 is that major DeFi protocols are developing their native decentralized stablecoins. Already launched examples include crvUSD issued by Curve and GHO issued by AAVE, with crvUSD currently reaching an issuance of $140 million, while AAVE has minted 3.48 million GHO on Ethereum. Although many challenges remain unresolved in the development of decentralized stablecoins, such as GHO never achieving the peg of $1 since its launch, we expect to see more native crypto stablecoins emerge in the future, reducing reliance on USDT and USDC.

Bitcoin Track

As 2023 comes to a close, Bitcoin has regained strong momentum, particularly breaking the $40,000 mark for the first time since last October. The market is sending clear bullish signals regarding Bitcoin and its related assets. However, the question arises: can this momentum continue into next year, or is it merely short-term speculation driven by ETF approval expectations? Today, we will delve into the fundamental driving factors behind this round of Bitcoin's price surge and share our views on the future development of the Bitcoin ecosystem.

Key factors driving Bitcoin's growth:

1. Favorable Macroeconomic Environment

By the end of 2023, Bitcoin has shown stronger momentum than traditional TMT stocks. That said, the market has already priced in factors that could lead to lower interest rates in the coming months, while investors expect that economic recovery may take longer to reflect on corporate balance sheets. Simultaneously, investors have been actively seeking various means to hedge against geopolitical conflicts and economic crises that occurred in 2023. Due to its inherent value storage properties, Bitcoin is gradually evolving into "digital gold," viewed by investors as a new alternative asset.

2. Expectations of Institutional Capital Inflows

In Bitcoin trading, a key factor driving market sentiment is the active applications for Bitcoin spot ETFs by various traditional asset management companies. This reflects the traditional market's acceptance and recognition of Bitcoin's investment value. On the other hand, the approval of Bitcoin spot ETFs is expected to bring new capital inflows and liquidity from the institutional market (participants include authorized participants and market makers), further stimulating trading activity in the Bitcoin market and enhancing capital efficiency.

In addition, traditional financial institutions such as Standard Chartered, Nomura Securities (Laser Digital), UOB, and JPMorgan are also leading the adoption of Web3 by formulating Web3 strategies and establishing Web3 investment departments. This further reinforces traditional financial institutions' bullish sentiment towards Bitcoin and the broader crypto ecosystem, bringing potential new capital inflows.

3. Bitcoin Halving

The next Bitcoin halving is set to occur in the second quarter of 2024. Halving events happen every four years, reducing the block reward for Bitcoin mining by half each time. This mechanism significantly lowers Bitcoin's inflation rate. Based on historical trajectories, the market generally expects Bitcoin's price to reach an all-time high within six months following a halving. Driven by expectations of institutional capital inflows, demand in the Bitcoin market has significantly outpaced supply, further pushing up Bitcoin's price.

4. Innovative Breakthroughs in the Bitcoin Ecosystem

Bitcoin's POW blockchain was originally designed for value transfer and lacks composability. Recent breakthroughs in technical architecture brought about by new standards like Taproot and Ordinals have improved Bitcoin's composability, programmability, and transaction efficiency, further unlocking its potential in trustless staking, complex DeFi strategies, and even gaming. As a blue-chip cryptocurrency that has already penetrated widely, Bitcoin is expected to see broader adoption in the near future with the aid of technological advancements.

Based on the above factors, we are optimistic about Bitcoin's growth in the coming year. The active product development over the past year indicates that there are several key areas in the Bitcoin ecosystem worth focusing on:

- Developer SDKs and Marketplaces: Oyl, Unisat

- ZK Rollups: Bison, Chainway, Alpen Labs

- EVM L2/Scaling Solutions: Botanix Labs, B2 Networks, Bitcoin Wizard

- Sidechains: Liquid Network, Threshold Network

- Staking: Babylon

Overall, these developments and initiatives indicate that the Bitcoin ecosystem is presenting a vibrant and ever-changing landscape, laying the foundation for sustained growth and innovation in the foreseeable future.

SocialFi Track

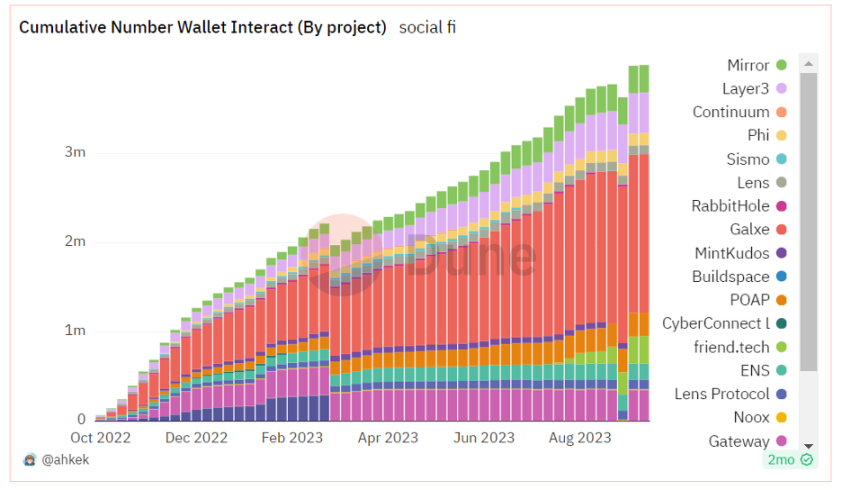

Since 2021, the SocialFi track has gradually entered the sight of crypto users, similar to the social and entertainment attributes of chain games, and is regarded as a phenomenal track that can bring a large influx of new Web3 users. Compared to the relatively subdued situation of the entire track in 2021-2022, some innovative gameplay and designs in the SocialFi track have gained significant traction in 2023. As shown in the figure below, the entire SocialFi track has seen good development over the past year, with mainstream projects accumulating nearly 4 million wallet interactions, while new projects like Galxe, Friend.Tech, and Sismo have also garnered considerable traffic.

Figure 5: Cumulative Wallet Interactions of Various Projects, Source: dune.com

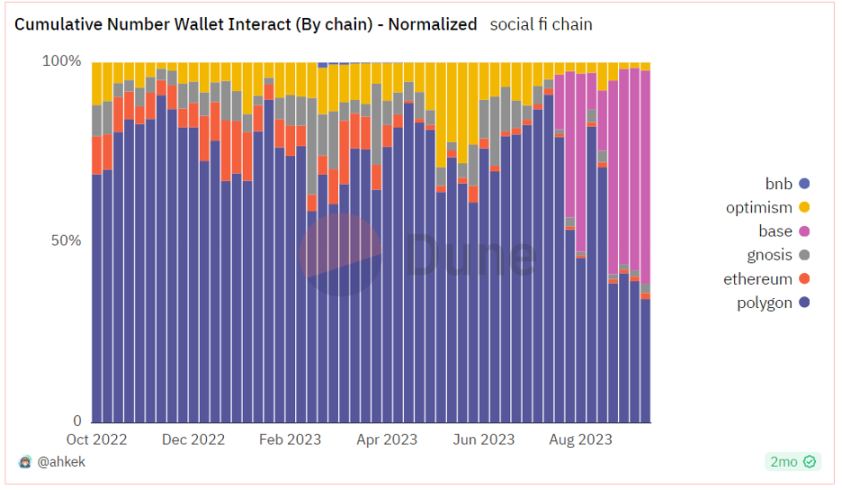

From a specific chain perspective, the main SocialFi projects are concentrated on the Polygon and Base chains, while other chains have seen relatively little traffic in the social domain. In addition to providing stable networks, fast computation speeds, and low interaction costs, Polygon has actively developed various application projects such as games and NFTs within its ecosystem over the past 1-2 years, while also expanding its audience by collaborating with major Web2 IP institutions, resulting in a steady increase in traffic from both within and outside the crypto space. Base has captured a significant share of SocialFi traffic, benefiting from the large influx brought by Friend.Tech. Other chains like Ethereum and BNB have seen relatively slow growth in community-related traffic.

Figure 6: Cumulative Wallet Interactions by Chain, Source: dune.com

Currently, projects in the SocialFi track are primarily divided into three mainstream development directions:

1. Social Infrastructure

Social infrastructure serves as the foundational construction and general tools for the entire SocialFi track. Unified, simple, and convenient infrastructure helps lower the user entry threshold, reduce usage barriers between different DApps, and accumulate more users and data. Projects like Galxe, Lens, and CyberConnect have approached from various dimensions, integrating users and supporting DApp products, becoming traffic entry points and interfaces for the Web3 SocialFi track. This track is expected to see phase-based traffic growth opportunities as ecosystem projects mature and explode further.

2. Social DApps

Social DApps represent the largest project category in the entire SocialFi ecosystem, exhibiting a flourishing development trend. In terms of project types, they include various types and gameplay such as post forums, fan platforms, video streaming, social games, and social identities. DApps are the most direct type of ecological project that binds and interacts with users. In 2023, some projects achieved good development results, with Friend.Tech's ecological development being particularly outstanding. Its clever economic design and capital augmentation factors successfully achieved a breakthrough in traffic, providing a good reference sample and design route for the development and design of subsequent social projects. Currently, the main development direction of social DApps focuses on decentralized censorship resistance and the fun of gameplay, meeting the demand for social privacy and social gaming attributes. This track currently attracts a large number of project developers and active players, nurturing the Alpha projects of the next bull market in the SocialFi track. Other projects like Facaster, Nostr, and RepubliK have also generated some discussion in the market. Overall, most social DApps are currently in mid-development, with products either launched and operational or in testing phases. In the future, as infrastructure projects go live, there may be a wave of concentrated project launches or token releases.

3. Social Bots

Social bots represent another project type in the SocialFi track that attracts market traffic in 2023. They mainly include trading bots, harvesting bots, and Q&A bots. Representative projects include Unibot, Banana Bot, Wagie Bot, and Loot Bot. These projects are primarily built on Telegram, implementing applications for crypto trading and other business types on this globally popular social network platform with 800 million monthly active users. Social bots, strictly speaking, originate from Web2 social derivatives as Web3 project types, significantly lowering user entry barriers and effectively leveraging platform advantages to expand a large number of new cryptocurrency users. Such Web2-friendly projects have broad market demand and development prospects. Similar to games and social DApps, social bots are also one of the incremental tracks for the next bull market.

In summary, the Web3 SocialFi track is in the early to mid-development stages, relying on the maturity of other infrastructure developments, including but not limited to cross-chain information transmission, data storage, reduced transaction costs, and compliance issues. Currently, the types of projects in the SocialFi track mainly include social infrastructure, social DApps, social bots, and other social tools. Among them, social DApps have the largest number and variety, and are most likely to nurture the Alpha products of the next bull market. Currently, many developers are working on Web3 social products, and capital is gradually paying attention to and investing in this track. With the launch of some hot projects and token issuances, the market heat of the SocialFi track is gradually rising. While the SocialFi track shows opportunities, it is also essential to fully recognize the current challenges it faces, including incomplete infrastructure development, bottlenecks in new user growth, and potential compliance issues. Overall, the crypto social track is expected to see concentrated project maturation, launches, and token issuance in 2024, with good investment potential and development prospects.

GameFi

In 2021, the gaming track received substantial traffic and capital support, followed by a cooling in 2022, where the reduction of wealth effects led to a Waterloo-like downturn for gaming projects that relied on gold farming for user growth. In 2023, the gaming track has shown relatively stable overall performance. As a traffic-driven track born during the bull market, launched blockchain games have experienced a prolonged period of consolidation during the bear market, and many projects that raised funds at the end of the bull market have essentially entered the final stages of development. It is expected that the gaming track will still exhibit good traffic effects and project performance in this cycle.

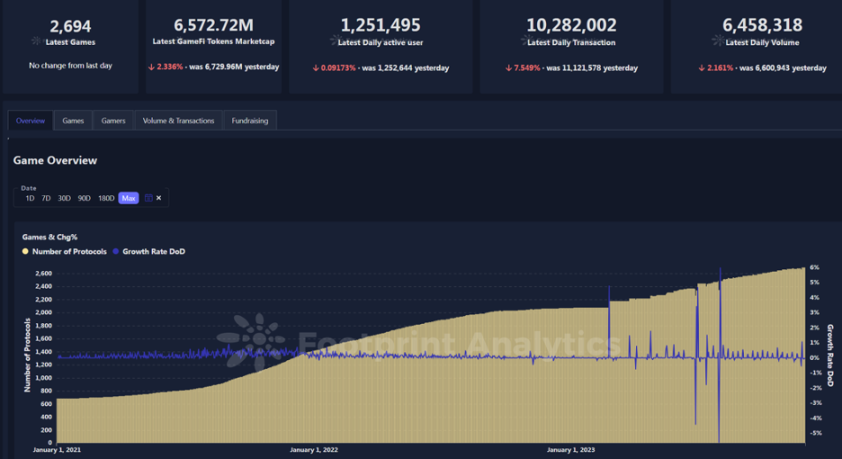

From the data shown in the figure below, gaming projects have maintained a continuous growth trend in 2023. According to project data statistics from Footprint Analytics (data as of December 1, 2023), there are currently over 2,600 market chain game contracts, with launched projects having a circulating market value exceeding $6.5 billion, daily trading volume exceeding $6 million, and daily active addresses exceeding 1 million. The overall market has maintained a certain level of activity during the bear market.

Figure 7: Number of Game Protocols and Growth Rate, Source: footprint.network

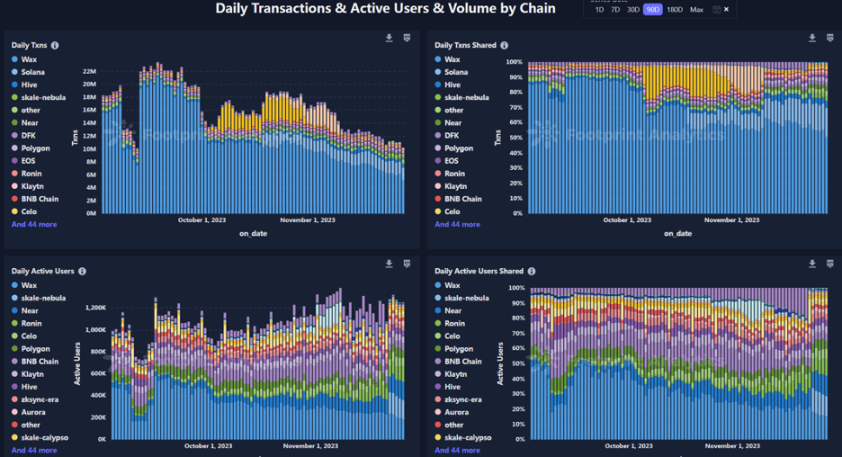

In terms of specific ecosystems, the overall market has over a million daily active addresses, with absolute traffic concentrated on the Wax chain. Thanks to its low interaction costs and quick settlement experience, Wax has maintained its highest market share position throughout both bull and bear markets, while other public chains like Near, Celo, and Polygon also hold a certain market share.

Figure 8: Daily Transaction Numbers, Active User Counts, and Transaction Volumes by Chain, Source: footprint.network

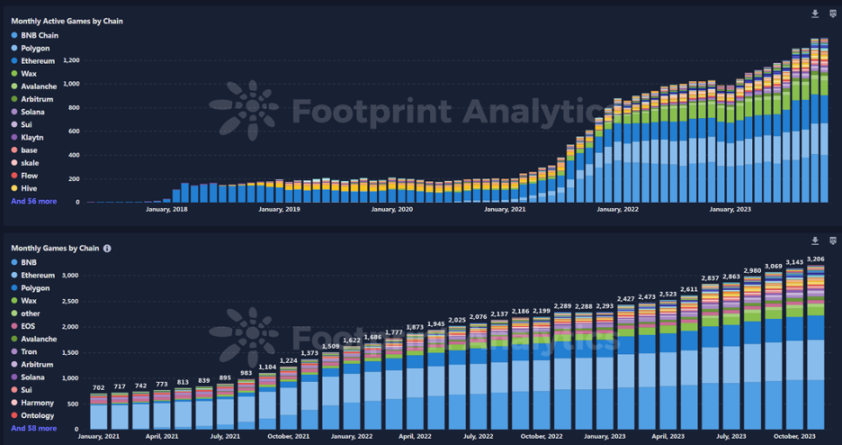

Regarding the development of GameFi projects, overall, thanks to the development and maturity of entrepreneurial projects from the previous bull market, the number of gaming projects has increased in 2023 compared to 2022. BNB remains the ecosystem with the most gaming projects, followed closely by Polygon, Ethereum, and Wax, which have a certain market share in deploying gaming ecosystem projects.

Figure 9: Monthly Active Games by Chain, Source: footprint.network

The overall ecosystem of blockchain games has shown a steady development trend in 2023, and this track is expected to perform well in the next bull market. Unlike the previous bull market driven by token economics, the next bull market's driving factors may shift from gold farming back to entertainment itself, with the long-term entertainment attributes of games being priced in. As the most anticipated user traffic track in the Web3 space, the next bull market is expected to achieve breakthroughs in user entry barriers, helping more Web2 users seamlessly experience blockchain games. Additionally, in terms of game types, besides traditional on-chain games, well-produced AAA games and fully on-chain games have become key development routes in this bear market. AAA games, with their large production and playability, are expected to achieve significant user growth, while exploration of fully on-chain games is likely to enable new asset types and gameplay upgrades, leading to richer game designs and experiences.

2024 Outlook Summary

As 2024 approaches, HTX Ventures stands at the forefront of transformation in the blockchain and cryptocurrency tracks, filled with optimism and a clear vision for the future. Key trends and developments that will influence the landscape of the crypto track in the coming year include:

- Trading Innovations: The emergence of mature trading bots and new trading infrastructures witnesses continuous innovation in trading mechanisms, suggesting more dynamic and efficient market interactions.

- Layer 2 Evolution: Driven by the highly anticipated Cancun upgrade, fierce competition among Layer 2 solutions may lead to significant advancements in scalability and efficiency, further solidifying the critical role of this track.

- Dynamics of Web3 and X-Fi: The shift towards genuine Web3 projects (e.g., the success of platforms like Friend.tech) marks a more integrated approach, incorporating social and gaming elements into the crypto space.

- Integration with Traditional Finance: Discussions surrounding Bitcoin ETFs and Real World Assets (RWA), especially regarding the potential breakthrough of Bitcoin spot ETFs, highlight the increasing convergence of traditional finance and the crypto industry, likely marking a new era of market growth and mainstream recognition.

In 2024, HTX Ventures will continue to lead these advancements, leveraging our expertise and insights to support and strengthen projects that are not only at the forefront of technological innovation but also strategically positioned for long-term impact and success. We remain optimistic about the coming year, as we believe the potential of these trends will foster meaningful progress and create new opportunities in the ever-evolving crypto landscape.

References: https://www.eip4844.com/ https://www.erc4337.io/ https://vitalik.ca/general/2023/11/14/neoplasma.html https://dune.com/niftytable/account-abstraction https://defillama.com/ https://defillama.com/stablecoins https://gho.xyz/ https://crvusd.curve.fi/ https://www.demandsage.com/telegram-statistics/#:~:text=How%20Many%20People%20Use%20Telegram,800%20million%20monthly%20active%20users https://www.footprint.network/research/gamefi/game-overview/chain-stats?series_date-79658=past90days~