In-depth interpretation of the potential projects in the DePIN track: Render, Helium, and Livepeer, etc

DePIN is a perfect fit for the crypto space, combining decentralized infrastructure with blockchain technology and token economics.

DePIN is a perfect fit for the crypto space, combining decentralized infrastructure with blockchain technology and token economics.Author: LouisWang, Core Contributor of Biteye

DePIN (Decentralised Physical Infrastructure Networks) utilizes blockchain technology to allow participants to deploy hardware devices in a permissionless and trustless manner, providing real-world services or digital resources. The core concept is that users earn rewards by renting out the services provided by their hardware. According to Messari, the entire sector is currently valued at approximately $9 billion and is expected to grow to $35 trillion by 2028.

(Source: Messari)

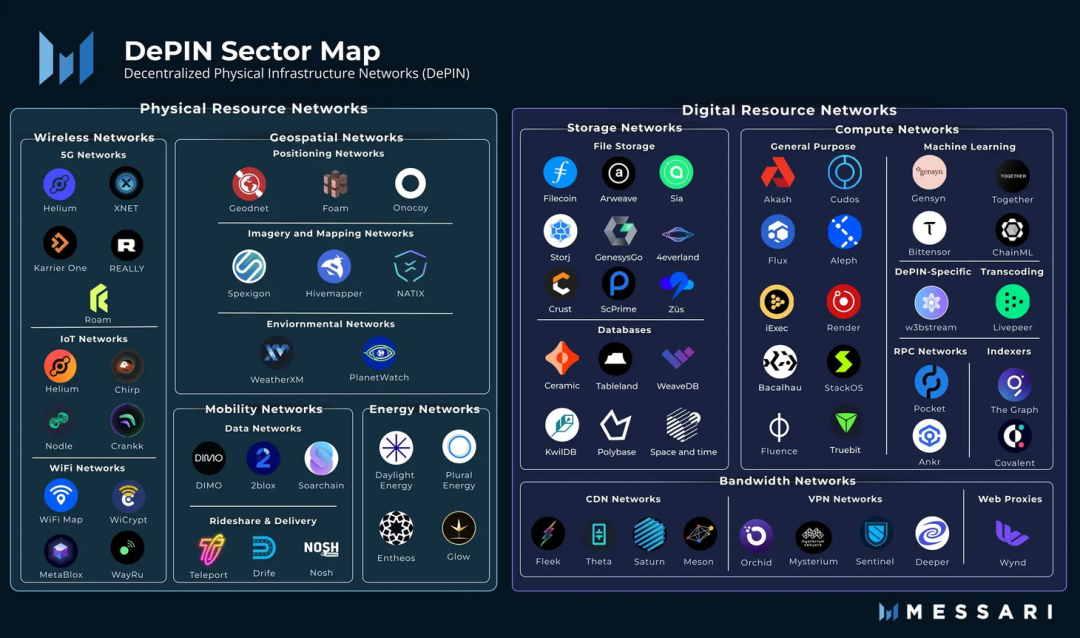

DePIN covers a wide range of fields. According to Messari's classification, it can be divided into two main categories: Physical Resources (PRN) and Digital Resources (DRN). Physical resources include wireless networks, geospatial networks, mobile networks, and energy networks; digital resources include data storage, computing power, and network bandwidth, with further subdivisions in each subfield.

(Source: Messari)

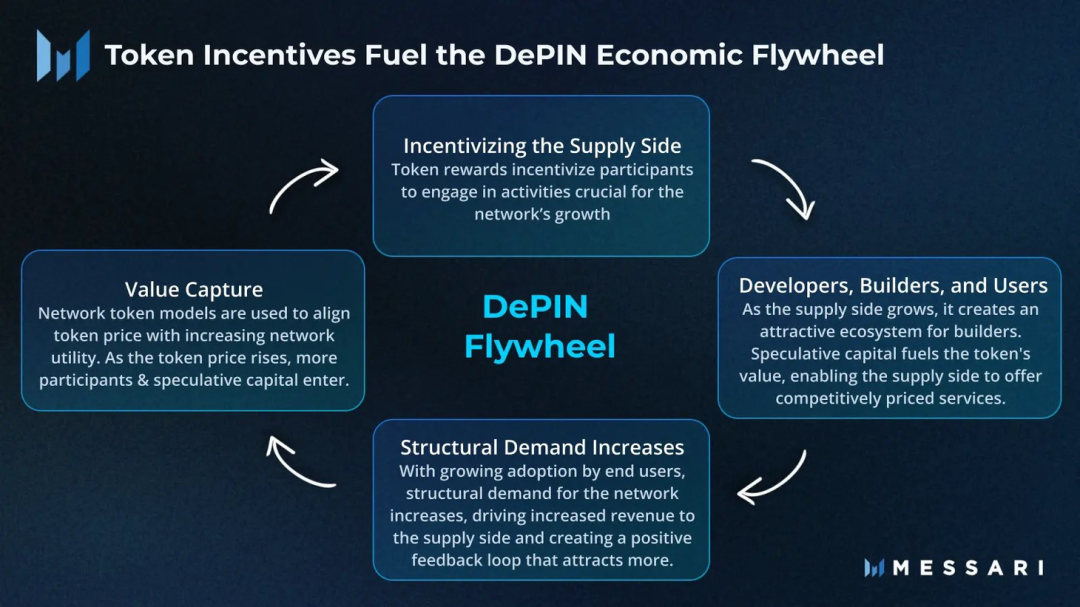

The basic flywheel logic of the DePIN sector is to incentivize more supply-side participation through token economics. With sufficient resource supply, price competition arises, and ample resources combined with good prices stimulate demand. With demand, tokens capture value, which can better drive price increases and attract more resource providers.

This article briefly introduces projects in the DePIN sector:

Render Network

Render Network is a blockchain-based distributed GPU rendering network platform launched by OTOY in 2017, aimed at connecting more creators with idle GPUs to leverage unused computing power for rendering films and animated art. Unlike centralized cloud rendering, Render is an unlimited decentralized network that addresses supply and demand issues, breaking the limitations of centralized storage by aggregating idle GPUs and connecting creators who need additional GPU computing power, maximizing resource utilization.

In simple terms, Render Network's business matches computing power with artistic rendering needs. The computing power suppliers are referred to as node operators, and their number has remained stable, with currently 326 Render node operators providing computing power.

(Source: https://twitter.com/ejwallach)

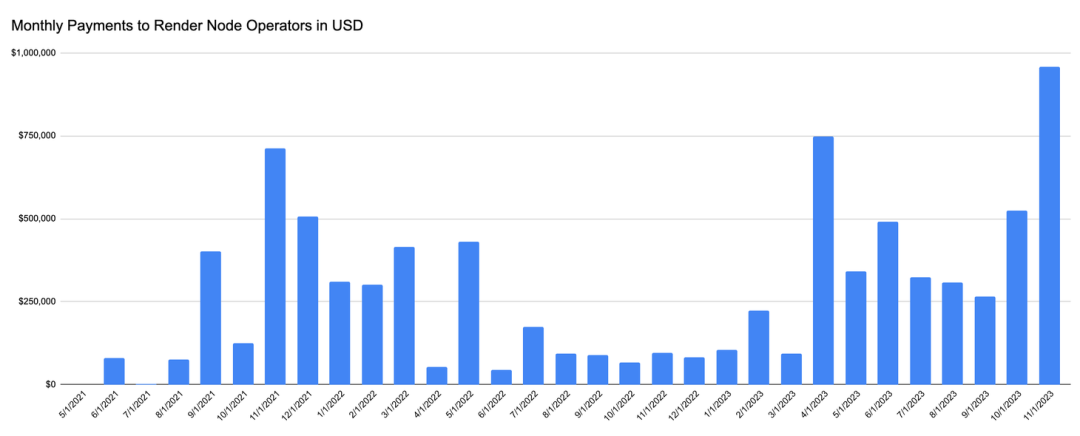

With the growth in rendering demand and the increase in RNDR prices, node operators received $958,000 in November, an 82% month-over-month increase and a 898% year-over-year increase. However, payments made by OTOY to GPU nodes are often significantly delayed, so the peak may reflect "catch-up" payments from previous months.

(Source: https://twitter.com/ejwallach)

Render Network was originally deployed on the Polygon network, but in March of this year, the community voted to migrate to Solana and build a BME (Burn and Mint Equilibrium) model on Solana. The BME model describes a state of relative balance between burned tokens and minted tokens in an ideal process and specific consumption market. It is a mature token model already applied in projects like Helium.

(https://medium.com/render-token/behind-the-network-btn-july-29th-2022-7477064c5cd7)

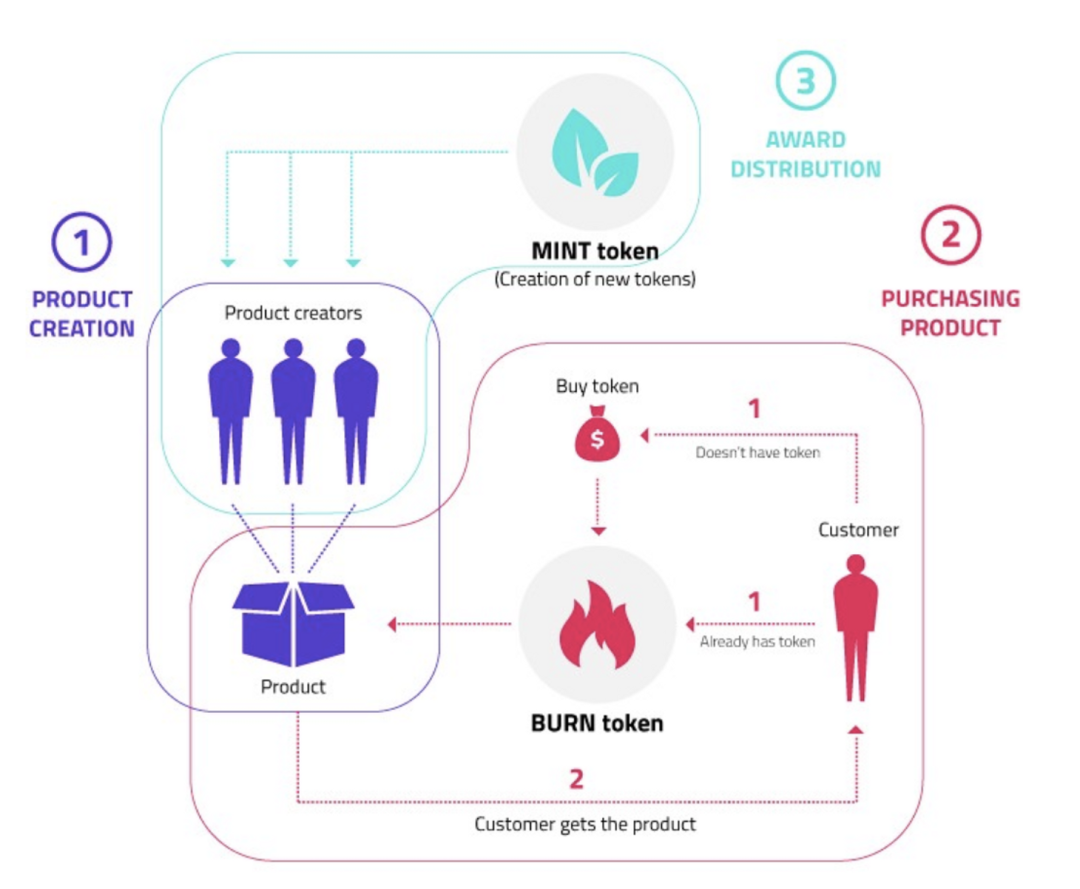

In this model, users use RNDR tokens to purchase GPU rendering services, and the tokens used upon task completion are burned. Service providers are rewarded with newly issued tokens, with the rewards based not only on task completion metrics but also on customer satisfaction and other comprehensive factors. Thus, RNDR tokens have more consumption scenarios within the entire economy, and the supply-demand relationship of tokens can be balanced and adjusted based on the algorithm between burned and minted tokens. The entire business model is evolving from a simple C2C to a more managed B2C model.

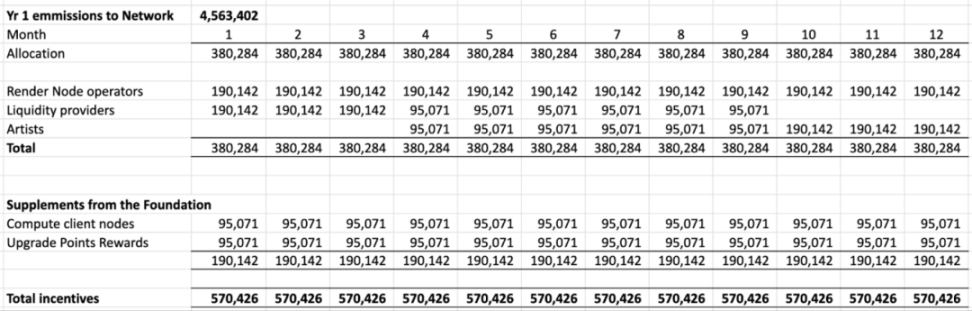

The initial distribution of token release is as follows:

(https://github.com/rendernetwork/RNPs/blob/main/RNP-006.md)

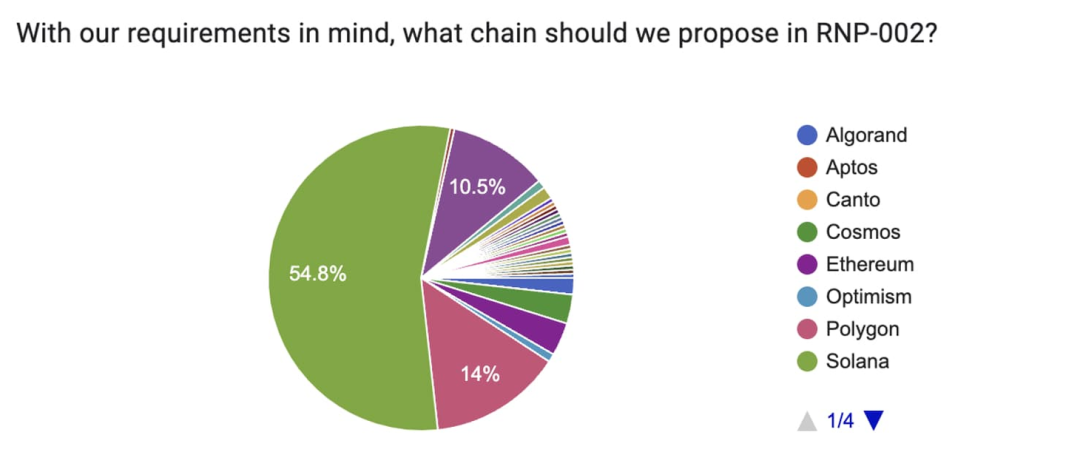

Regarding the destination of the network migration, over half of the users in the community vote chose to migrate to Solana. Since Render Network has reached an annual processing volume of millions of frames, and this demand is expected to increase with the development of AI, there are higher requirements for on-chain synchronization efficiency, throughput, network latency, and costs. Solana's TPS (4000) is about 137 times that of Polygon (29), with costs approximately 1/5000 of Polygon, and it also has a large number of mature developers, making it an ideal choice.

(Source: https://github.com/rendernetwork/RNPs/blob/main/RNP-002.md)

On November 2, the Render Foundation announced that Render Network had successfully upgraded its core infrastructure from Ethereum to Solana and launched an incentive program to encourage users to upgrade their $RNDR on Ethereum to the new token $RENDER on Solana.

(Source: https://coinmarketcap.com/currencies/render/)

Since the beginning of this year, $RNDR has increased by 800%. Currently, the market cap (MC) and fully diluted valuation (FDV) are $1.5B and $2.2B, respectively, ranking 51st in market capitalization. As the token has real application scenarios, the trends in token price and business volume are quite similar. Render's business resources are strong, and this year it has collaborated with Stable Diffusion for AI image rendering. It has also appeared in promotional videos for Apple computers and has provided services for companies like HBO and Netflix, with the rapid development of AI significantly increasing the project's ceiling.

Helium

Helium is one of the oldest and most well-known DePIN projects, a decentralized wireless network protocol that incentivizes users to deploy gateways, promoting a global network based on LoRaWAN technology. Initially, it built its own Layer 1 network, but adoption was hindered. In April of this year, it completed the migration to the Solana network, hoping to reach a larger user base and liquidity while fully utilizing Solana's efficiency for further expansion.

Helium has over 350,000 active IoT nodes, and the Long-Fi signals generated by Helium gateways can only support LoRaWAN devices. Currently, all gateways in the Helium network are full gateways, which will gradually be replaced by light gateways.

(Source: https://explorer.helium.com/stats)

Building a global, hardware-supported decentralized wireless network is a grand vision but also very challenging. The following image shows the distribution of active Helium nodes worldwide, primarily concentrated in the United States and Europe. Therefore, Helium's challenge in the coming years will be to drive rapid growth on the demand side.

(Source: https://explorer.helium.com/)

Helium's 5G business, Helium Mobile, recently announced a pilot program in Miami to offer local residents a mobile access plan with unlimited voice/data for $5 per month. This pilot reflects Helium's vision for an open 5G network in the future, providing low-cost and reliable wireless network access services to the public. Additionally, Helium Mobile has announced next-generation 5G hotspots, developer tools, and application-based network coverage suggestions and incentive mechanisms, aiming to strategically encourage rapid growth in network coverage in key areas and locations at lower costs and with richer access scenarios.

(Source: https://coinmarketcap.com/currencies/helium/)

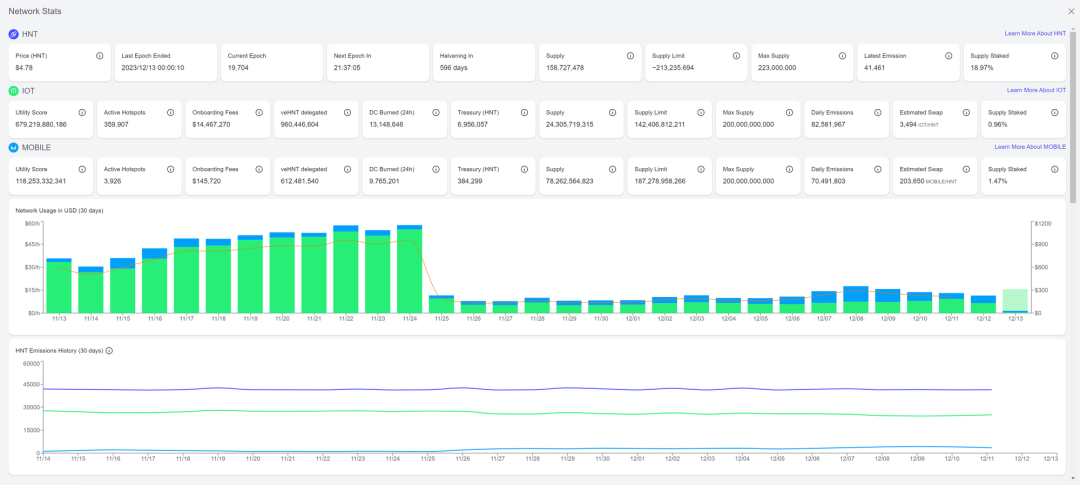

$HNT is the main economic asset in the Helium ecosystem, and the only way to pay for network data transmission fees is by burning $HNT. Currently, its market cap is $1.29 billion, and it was delisted from Binance for spot trading in October last year.

This year, Helium issued two new tokens, $Mobile and $IOT, which are governance tokens for the Helium Mobile and Helium IoT subDAOs, respectively, aimed at achieving governance separation. Helium Mobile's 5G hotspot business earns $Mobile, while $IOT is used to reward nodes focused on running IoT. $HNT remains the main asset in the Helium ecosystem, as the only token that can pay for network data transmission.

Mobile's role is similar to that of a telecom operator, offering low-cost services and allowing eSIM mining. The business model is very simple and effective, requiring no complex physical devices, making it very attractive to low-income users and highly scalable, thus achieving mass adoption.

Austin Federa, strategic director of the Solana Foundation, recently revealed that all employees of Solana Foundation/Labs/Eco have started using the eSIM and network services provided by Mobile. $Mobile has been live for two weeks, with a current market cap of $541 million, and if development goes smoothly, there is significant room for growth.

(Source: https://coinmarketcap.com/currencies/helium-mobile/)

Livepeer

Livepeer is a decentralized video transcoding network aimed at providing a decentralized, highly scalable real-time streaming protocol, significantly reducing the costs of video streaming applications. Founded in 2017, its business has now migrated from Ethereum to Arbitrum.

(Source: https://explorer.livepeer.org/)

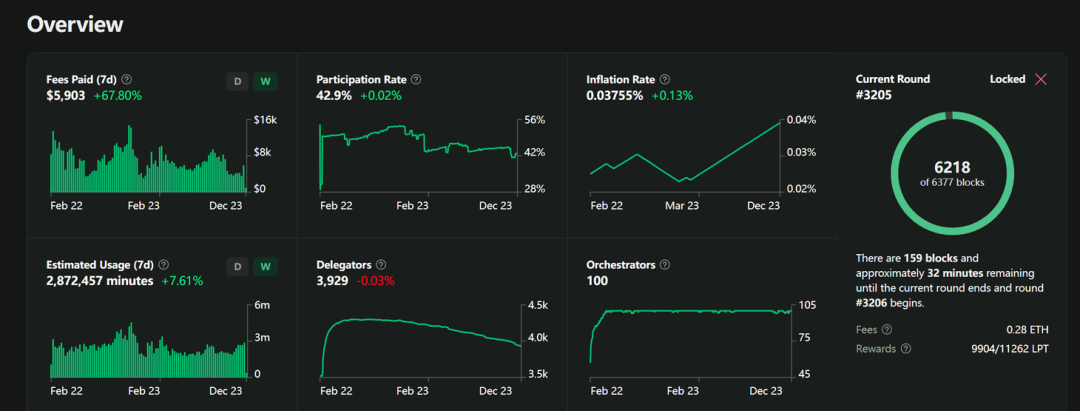

Livepeer's overall transcoding business volume has consistently maintained an average of over 2 million minutes per week, and in November, Livepeer successfully transmitted 11.3 million minutes of video. Despite the increasing number of streaming minutes, the publicly available price competition on the network has reduced the cost-effectiveness of video encoding for users by 48% (from $42,100 to $8,270) compared to two months ago (November vs. September), which aligns with the DePIN flywheel theory that competition among idle computing resources will lower user costs.

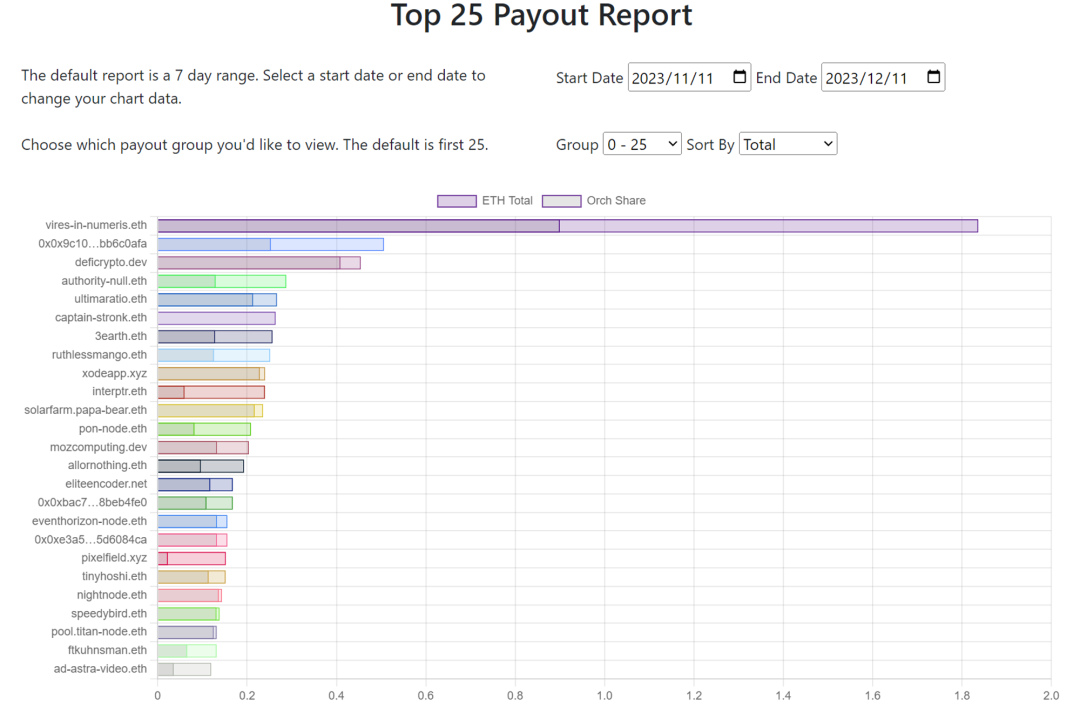

(Source: https://www.livepeer.tools/payout/report)

In addition to inflationary LPT rewards, node operators can also earn ETH through video transcoding work on the network. This 30-day payment chart highlights the top 25 nodes, each of which can earn between 0.12 and 1.84 ETH in rewards.

(Source: https://tokenterminal.com/terminal/projects/livepeer)

LPT currently has a market cap of $217 million, with a rapid surge in August, where trading volume increased thirtyfold in a single day, and the price doubled within a week. However, overall, it is still at a loss compared to the price at the beginning of the year. The protocol's annual revenue is estimated at $290,000, with no strong business cash flow.

(Source: https://coinmarketcap.com/currencies/livepeer/)

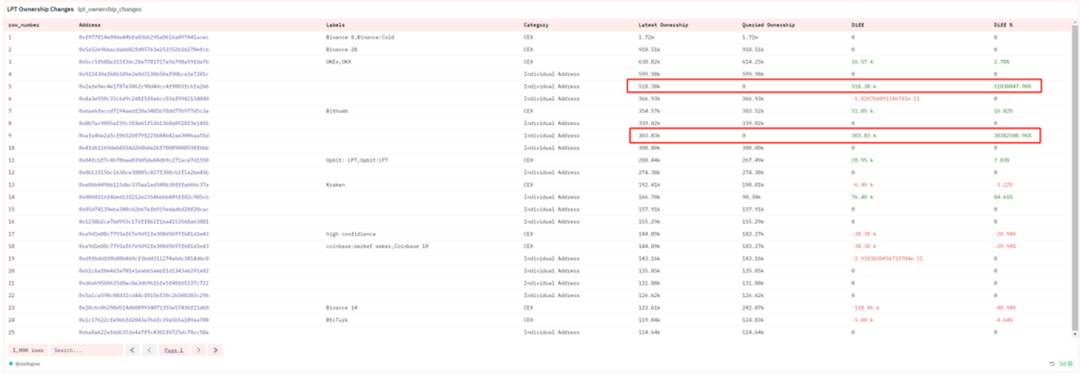

Interestingly, in the past two weeks, whales have completed their positions, purchasing a total of about 800,000 tokens (~$4.8 million) from exchanges and transferring them to wallets.

(Source: https://dune.com/sixdegree/liverpeer-lpt-ownership-and-governance)

Arweave

Arweave is a decentralized protocol for permanent data storage, utilizing a PoA (Proof of Access) mechanism for consensus block generation. Compared to IPFS, its biggest feature is one-time payment for permanent storage. When people spend tokens to store data, a small portion of the paid AR goes directly to the miners (nodes) responsible for storing the content, while a large portion is stored in a donation fund (endowment) that can technically release rewards indefinitely at a slow rate. Through this mechanism, Arweave guarantees infinite permanent storage.

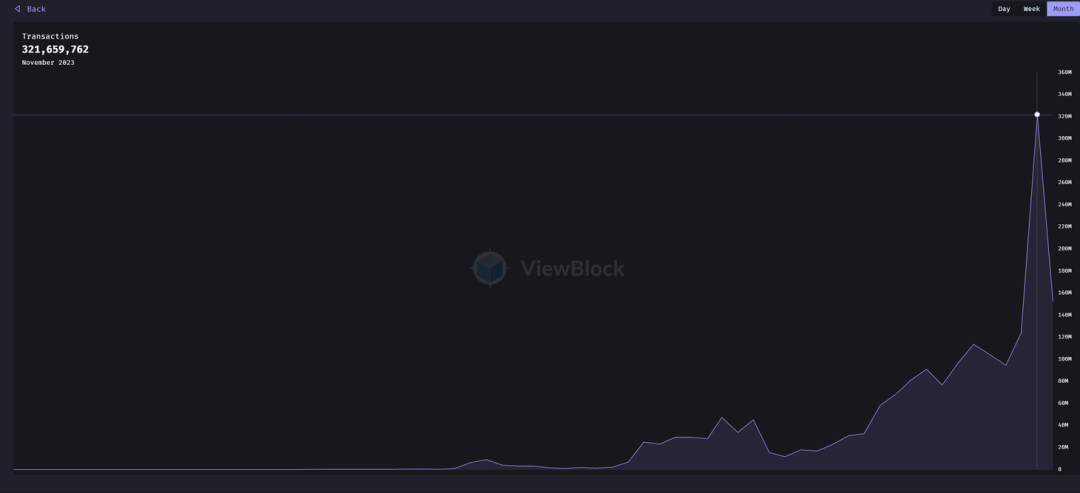

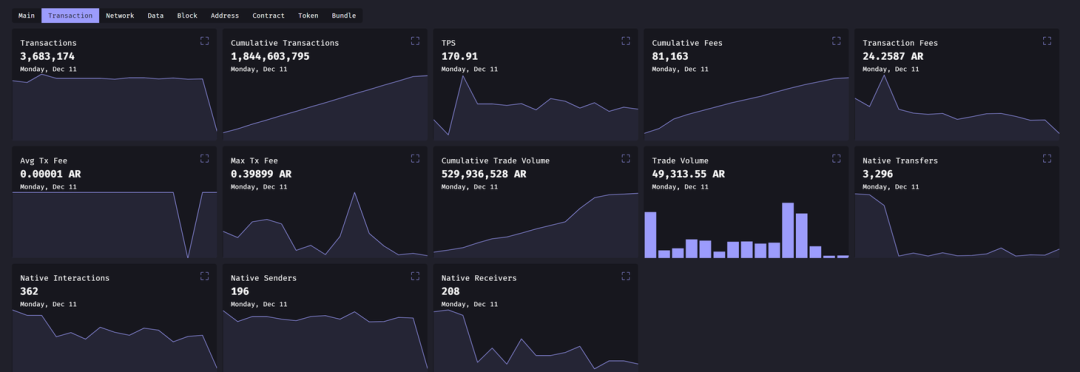

Arweave has many partners and a rich ecosystem, with Solana and Nervos adopting Arweave as the default data storage layer, and it also provides data storage services for multiple public chains like Avalanche and Near through its middleware project KYVE. As of November 2023, Arweave's monthly transaction volume has reached 321 million. The monthly transaction volume in November increased by over 159% year-on-year and approximately 9.4 times month-on-month.

(Source: https://viewblock.io/arweave/stat/tx?time=month)

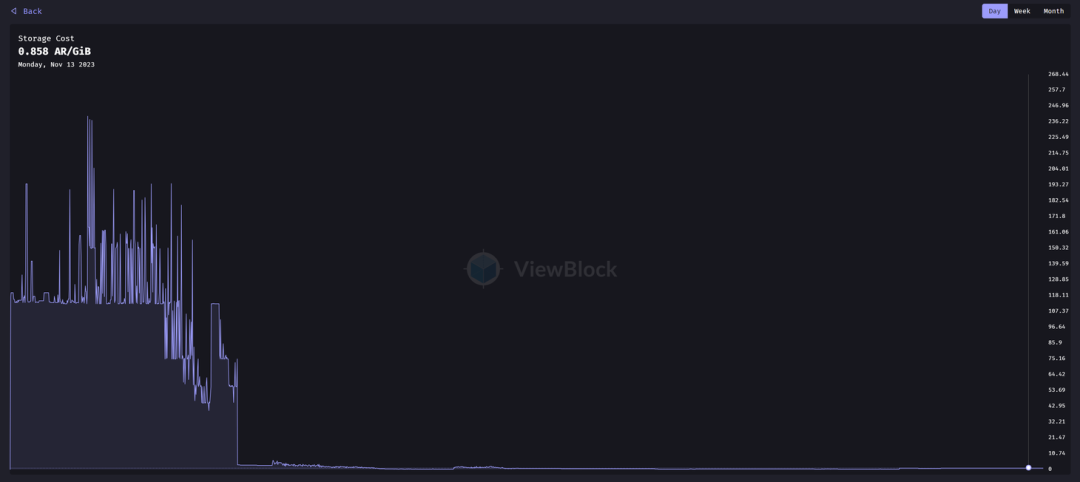

Arweave can currently add about 170 data entries to the network per second. Although the transaction volume continues to grow monthly, Arweave's charging market remains stable at 0.858 AR/GiB, proving Arweave's scalability.

(Source: https://viewblock.io/arweave/stat/tx?time=month)

Since its establishment, Arweave has completed a total of 1.84 billion transactions, with rapid business development this year, of which about 1.2 billion transactions occurred this year.

(Source: https://viewblock.io/arweave/stats?tab=tx)

$AR is currently in a fully circulating state, with a market cap of $583 million. Its business volume is comparable to Filecoin, but its market cap is only 1/4 of Filecoin's, with significant business growth and limited token appreciation.

(Source: https://coinmarketcap.com/currencies/arweave/)

Irys is the storage solution for the AR ecosystem, handling about 95% of Arweave transactions. It is considering forking Arweave, ceasing maintenance of the dataset, and resetting the token supply, which may lead to the inability to achieve permanent storage of data on AR, potentially having a significant impact on the price of AR.

Hivemapper

Hivemapper is a blockchain-based mapping network where contributors can collect data by installing Hivemapper's dashcams and earn $HONEY tokens as rewards. The distribution and settlement of tokens occur on the Solana network. The dashcam in Hivemapper is similar to a mining machine, connecting with Hivemapper's application to upload street view images as data.

(Source: https://hivemapper.com/explorer)

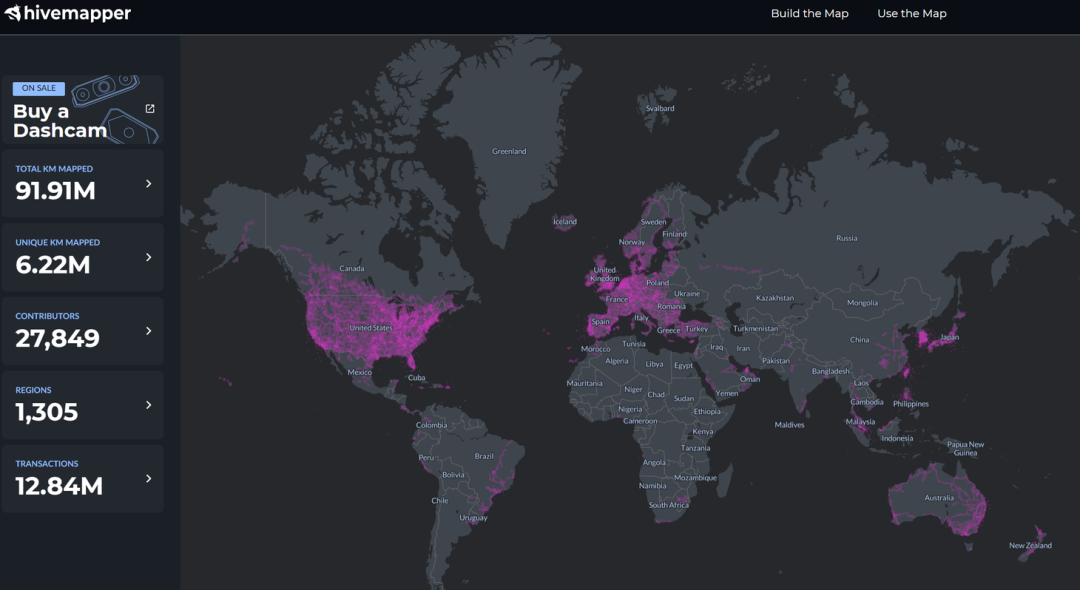

In just one year since its establishment, Hivemapper has mapped approximately 91 million kilometers of road, covering 10% of the total global road mileage, with over 6 million kilometers being unique. With the delivery of over 8,000 dashcams worldwide, drivers are helping to map the freshest maps of the world every day.

(Source: https://hivemapper.com/explorer)

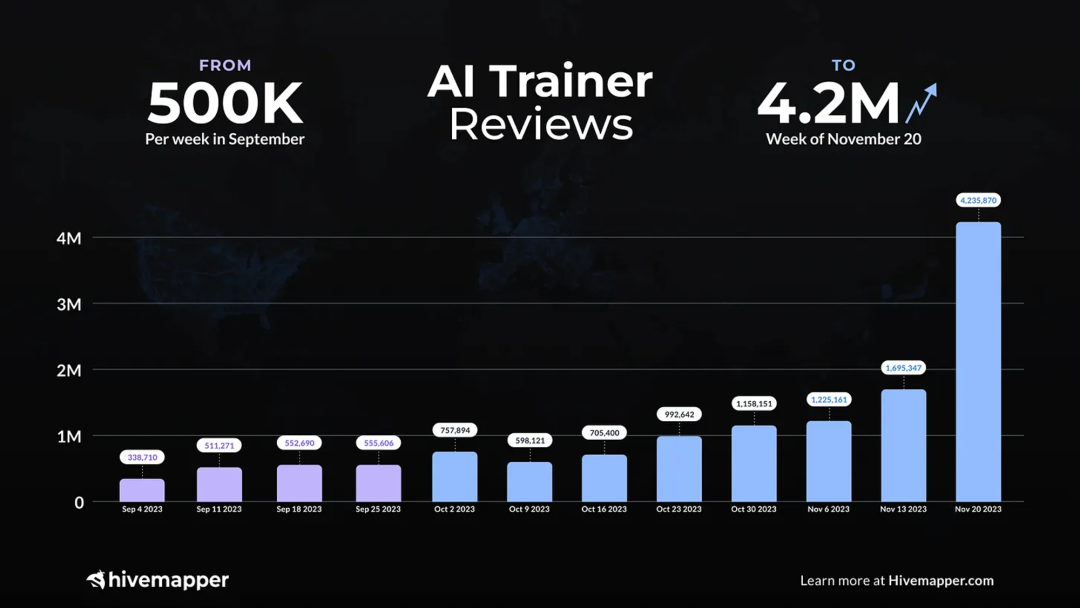

Hivemapper's map AI training has been put into operation, autonomously generating map features based on road images, with over 2,000 AI trainers responsible for validating the system's output results each month. In September, there was an average of 500,000 training results per week, which rapidly increased to over 4.2 million weekly by November.

(Source: https://coinmarketcap.com/currencies/hivemapper/#Chart)

Hivemapper's revenue comes from two sources: selling dashcams and selling map data APIs. Each dashcam is priced at $300 (with a high-end version at $649), and the annual revenue from this alone is conservatively estimated to exceed $2 million. The price of the $Honey token cannot be too low; otherwise, the demand for dashcams will diminish, and the map cannot be effectively expanded, leading the entire business to a standstill. The token has not yet been listed on mainstream exchanges and is primarily traded on Orca, with a high FDV currently at $2.4 billion, but only 2.6% of the tokens are circulating. Projects with high FDV and low circulation have previously been a characteristic of SBF's tokens, making their prices very susceptible to rapid surges and crashes.

Conclusion and Discussion

DePIN is a perfect fit for the crypto sector, combining decentralized infrastructure with blockchain technology and token economics. Blockchain technology can solve issues of rights confirmation and verification, while token economics serves as the source of incentives for more participants, building network effects.

As mentioned at the beginning, DePIN can be simply categorized into two main types: physical resources and digital resources. Projects in the physical resource category, such as Helium and Hivemapper, are currently mainly concentrated in the United States, extending to Europe, facing significant geographical limitations. How to expand the market while effectively managing regulations is a crucial challenge for these projects. Projects in the digital resource category, while also having physical device thresholds (such as GPUs, hard drives, etc.), benefit from breaking geographical limitations and providing peer-to-peer services. With the rapid development of AI and the popularization of large models, ordinary people can also utilize AI for creation, leading to an increasing demand for computing power, thus expanding the reachable market scale for DePIN. Effectively collecting demand and expanding business cooperation are growth challenges for digital resource DePINs.

The DePIN sector is still in a very early stage. Although it has significant potential for breaking into new markets, the barriers for non-Web3 users to access, understand, and use it are relatively high. Additionally, the lack of complete infrastructure and unified standards results in a generally average development and user experience, with insufficient network availability. The competitive moat of various projects is not deep; for example, after the entry of the 5G project Pollen, Helium miners also began deploying Pollen nodes, indicating fierce competition in similar sub-sectors. How projects develop their own competitive moats is crucial. Furthermore, issues such as preventing cheating and facing regulatory restrictions are significant obstacles on the path to development.

From an investment perspective, DePIN is a business with both upper and lower limits. Unlike most meme projects that lack practical applications, DePIN projects have real demand, supply, and revenue, allowing for quality analysis from these angles. Compared to mature centralized services, DePIN services are cheaper, more flexible, and better suited to the needs of small-scale users, making them ideal clients from individuals to startup teams.

Token economics is a crucial part of DePIN. Without incentives, participants will lose motivation to become distributed nodes, similar to BT seeds that have a great vision but ultimately fade away. Token economics effectively fills this gap, with a good example being Filecoin as the incentive layer for IPFS. Additionally, some projects' physical devices are also significant sources of income, such as Livemapper's dashcams. If the token does not have an attractive enough price to cover costs, users will lack motivation to purchase hardware, preventing the physical network from further expanding and forming network effects, leading the project to a standstill. Therefore, DePIN tokens have a certain lower limit, akin to the shutdown price for miners.

Conversely, this will also become a condition that constrains the ceiling of DePIN projects. DePIN projects generally settle using project tokens, such as RNDR, LPT, and AR. Therefore, when tokens rise, the cash expenditure burden on users increases, and when price advantages are insufficient, users will inevitably be lost, leading to a decline in token prices. Thus, even very successful DePIN projects have an invisible ceiling on token prices. More importantly, DePIN projects are too solid, lacking the imagination of Memecoins, and do not have the Ponzi mechanisms of stepping on the left foot with the right, making it difficult to generate FOMO. Therefore, DePIN is an investment sector with both lower and upper limits, and finding early-stage, low-market-cap projects with applications is a relatively prudent approach.

With the maturity of Ethereum Layer 2, high-performance public chains like Solana, Aptos, and Sui are all good choices for the future rooting of DePIN, offering much higher cost-effectiveness than early projects building their own blockchains. The improvement in blockchain network performance also lays the foundation for the development of DePIN. Recently, a new concept emerging on Solana called "OPOS (Only Possible On Solana)" claims that many applications can only be realized on Solana, with DePIN being one of their main tracks. It can be observed that many DePIN projects are either migrating to Solana or settling using Solana, as Solana's high throughput and low transaction fees align perfectly with the needs of DePIN projects, making Solana a potential Beta for the rise of the DePIN sector.

![[Fogo Research Report] SVM L1 Track New Star](https://www.chaincatcher.com/upload/image/20250527/1748342134736-354298.webp)