Why have TUSD and FDUSD emerged as strong contenders in the new stablecoin battle under Circle's IPO?

Stablecoins have been hit hard one after another, giving new forces the opportunity to break through.

Stablecoins have been hit hard one after another, giving new forces the opportunity to break through.Author: flowie, ChainCatcher

Recently, Bloomberg reported that the stablecoin issuer Circle is planning to restart its IPO in early 2024. Compared to its previous tumultuous path to listing, this time Circle's IPO restart may be even more challenging. Currently, the market capitalization of USDC has nearly halved, dropping from $45 billion at the beginning of the year to about $24 billion.

As the market share of USDC has significantly shrunk, the entire stablecoin market landscape is being reshaped in 2023. On one hand, regulatory crackdowns and de-pegging issues have severely impacted leading stablecoins like BUSD and USDC, providing opportunities for new forces to break through; on the other hand, the emergence of yield-bearing stablecoins leveraging LSD and RWA, along with the entry of Web2 giant PayPal, has brought more imagination to the stablecoin market.

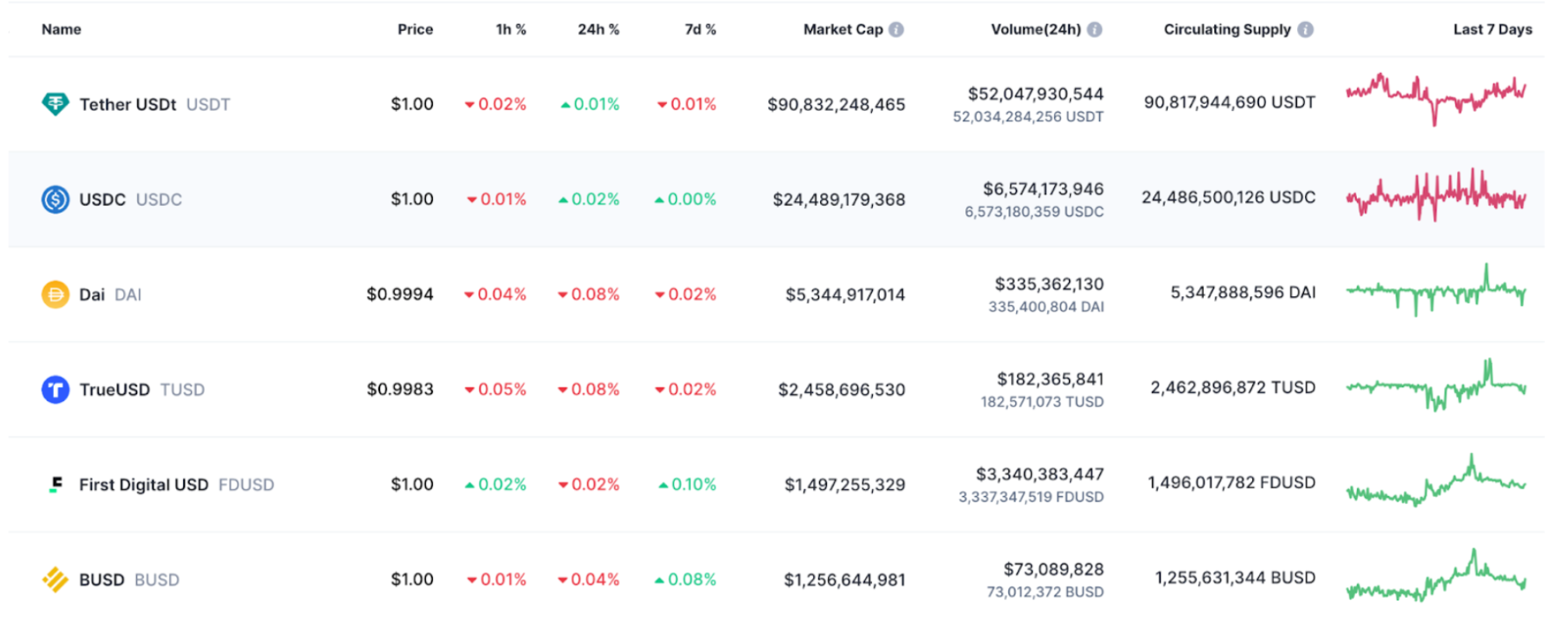

Currently, the ranking of the top five stablecoins by market capitalization has undergone significant changes. After BUSD faded from the stage and USDC faced de-pegging issues, DAI has taken the throne as the third-largest stablecoin, while the low-profile veteran TUSD and the new stablecoin FDUSD have risen to become the fourth and fifth largest stablecoins by market capitalization.

The market share of new forces like yield-bearing stablecoins and Web2 giants is still relatively small and will require a longer period of testing. However, TUSD and FDUSD, which already have market capitalizations in the billions and are growing rapidly, have begun to gain market validation.

New Battle for Stablecoins Under Circle's IPO Push: Landscape, Regulation, Yield, Web2 Giants

Circle has sought an IPO more than once. Back in July 2021, Circle planned to go public on the NYSE through a merger with a special purpose acquisition company (SPAC). At that time, USDC's market share was growing rapidly, and Circle's valuation reached as high as $9 billion.

However, despite this, the IPO plan, which took a year and a half, ultimately ended with a "temporary suspension." In December 2022, Circle announced that it had halted the IPO due to not being approved as "effective" by the SEC.

A year later, Circle's situation in its IPO push is quite different. From the perspective of the overall stablecoin market capitalization, according to Defillama data, the total market capitalization of stablecoins has reached $129 billion, having continuously declined since mid-May 2022, with a slight recovery recently as the crypto market has rebounded.

Behind the challenges facing the overall stablecoin market, the stablecoin landscape has been tumultuous throughout 2023, first impacted by the black swan events of Silicon Valley Bank and regulatory crackdowns, followed by the rise of yield-bearing stablecoins leveraging LSD and RWA, as well as the strong entry of Web2 giants like PayPal.

1. Leading Stablecoin Landscape Shifts, TUSD and FDUSD Rise

Currently, the major mainstream stablecoins by market capitalization have all been affected to varying degrees, and the rankings of stablecoins have changed significantly compared to the beginning of the year.

Looking back, the regulatory crackdown on BUSD began in February. The New York Department of Financial Services (NYDFS) announced an investigation into BUSD issuer Paxos, and soon after, the SEC also announced a lawsuit against Paxos due to issues related to BUSD. In desperation, Binance had to gradually withdraw BUSD. Most of the mainstream trading pairs for BUSD have been delisted from Binance, and recently, Binance's leveraged and contract platforms also removed BUSD.

BUSD's market capitalization plummeted from $16 billion in February to around $1.2 billion, a decline of 92%, and its position as the third-largest stablecoin after USDT and USDC has been ceded to DAI. BUSD is now ranked sixth.

After BUSD was forced out, USDC also suffered a severe blow. In March, the black swan event of the Silicon Valley Bank run caused USDC, which had reserves at Silicon Valley Bank, to experience a run and de-pegging issues. After USDC's safety was called into question, many large holders with USDC reserves, such as Binance, MakerDAO, and Frax Finance, sold off USDC to reduce their reliance on it. In August, it was revealed that Binance had sold a large amount of USDC in exchange for BTC and ETH as reserve assets. Subsequently, MakerDAO and Frax Finance converted a large portion of their USDC reserves into low-risk, interest-bearing assets like U.S. Treasury bonds.

Currently, although USDC remains the second-largest stablecoin by market capitalization, its market cap has actually dropped from $45 billion at the beginning of the year to about $24 billion, nearly halving and reaching its lowest level in nearly two years. Compared to the rapid growth of USDC one or two years ago, Circle's push for an IPO now seems more helpless. Since the de-pegging issues this year, Circle has taken measures to expand into emerging markets and partnerships to cope with the decline in USDC's market cap and pressure from new competitors, but the effects seem minimal. The transparency and safety endorsement that could come from going public may be one of Circle's last moves to revive USDC.

The impact of the de-pegging issues is not limited to USDC; DAI, which has a large amount of USDC as reserves, also experienced significant fluctuations. It once dropped from a market cap of $5.6 billion at the beginning of the year to $4.4 billion. After DAI converted a large amount of USDC into U.S. Treasury bonds, it gradually recovered to its current $5.35 billion.

In other words, among the original top four stablecoins, only USDT's market cap has grown from $66 billion at the beginning of the year to $90 billion. The other stablecoins, BUSD, USDC, and DAI, have all experienced varying degrees of decline. This also means that other stablecoin contenders have a lot of growth space. Currently, after DAI has taken over the original third-largest stablecoin position from BUSD, the rapidly growing TUSD is now ranked fourth, and FDUSD is in fifth place.

TUSD's market cap has surged from around $750 million at the beginning of the year to $2.5 billion currently, peaking at nearly $3.8 billion in October, with an increase of over 400%. The newly launched FDUSD in June this year has already reached a market cap of $1.5 billion, rising at a remarkable speed.

2. Yield-Bearing Stablecoins New Narrative Emerges

In addition to the significant changes in the market share of leading stablecoins, this year has also seen the emergence of yield-bearing stablecoins as a new narrative in the stablecoin market. Established DeFi projects like DAI, Curve, and Aave, as well as new DeFi protocols like Lybra Finance and OpenEden, have all been leveraging yield-bearing assets like LSD and RWA to promote the development of their yield-bearing stablecoins. For example, the protocol Lybra Finance, which mints yield-bearing stablecoins using LST assets as collateral, saw its value surge 40 times within just over a month of launch.

Additionally, Curve's crvUSD stablecoin, launched in May 2023, allows users to use a range of LSD assets (such as EWETH, wstETH, WBTC, etc.) as collateral to mint crvUSD. Currently, the collateral for crvUSD exceeds $100 million. Aave has also launched the over-collateralized stablecoin GHO, which supports tokens from the Aave v3 protocol as collateral, and its TVL has shown a significant upward trend since its launch in July.

3. Web2 Payment Giants Stirring the Market

The entry of Web2 payment giant PayPal has stirred the stablecoin market. Its launched stablecoin PYUSD has already surpassed 200 million in issuance. Although its market cap is currently limited, with 400 million users, PYUSD's significance for the large-scale adoption of Web3 is immense, as it has the potential to attract a large number of users into the cryptocurrency space. According to several crypto KOLs, PayPal's entry is expected to drive more Web2 payment giants to enter the market.

4. Stablecoin Regulatory Framework Gradually Clarifying

Currently, the regulatory framework for stablecoins in key crypto regions such as the U.S., Singapore, Hong Kong, and the U.K. is gradually becoming clearer. In June of this year, the Deputy Secretary for Financial Services and the Treasury of Hong Kong, Chen Haolian, stated that a regulatory framework for stablecoins is planned to be launched before the end of 2024. In July, the U.S. House Financial Services Committee announced the passage of the "Payment Stablecoin Transparency Act (draft)," which establishes a regulatory path for approving and regulating stablecoin issuers while creating unified federal minimum standards for payment stablecoins. In August, the Monetary Authority of Singapore (MAS) published its final regulatory framework for stablecoins. In November, the Bank of England released its plan for regulating stablecoins, stating that legislation for fiat-backed stablecoins will be introduced early next year.

The clarity of the stablecoin regulatory framework also means that stablecoins have greater potential to enter mainstream applications and achieve larger-scale adoption.

II. In the Midst of Multiple Changes, Why Are TUSD and FDUSD Strongly Breaking Through?

With the leading stablecoin market landscape loosening, the entry of yield-bearing stablecoins and Web2 giants brings many highlights to the stablecoin market development in 2024. However, the market share of these new stablecoin forces is still relatively small and will require a longer period of testing. Currently, the strong rise of TUSD and FDUSD, which already have market capitalizations in the billions and are growing rapidly, is worth noting.

1. The Rise of New Stablecoin FDUSD is Inextricably Linked to Binance's Adoption

First, let's talk about the new stablecoin FDUSD, which launched in June. FDUSD is issued by FD121 Limited, a subsidiary of the Hong Kong-based custodian company First Digital Limited, and is a stablecoin pegged to the U.S. dollar at a 1:1 ratio.

The FDUSD white paper mentions that its reserve support will consist of cash and highly liquid short-term government bonds. Its advantages include: transferable, redeemable, programmable, low fees, and operating on a decentralized network. Currently, FDUSD is primarily issued on Ethereum and BNB Chain and can be traded on cryptocurrency exchanges such as Binance, BingX, BitVenus, and Gate.io.

As one of the fastest-growing stablecoins, FDUSD's rise is closely linked to its adoption by Binance. After BUSD faded from Binance, the exchange gradually announced the use cases for FDUSD on its platform. In fact, since its issuance, on-chain data for FDUSD has shown that it is almost entirely held by Binance addresses. Additionally, at the time of FDUSD's release, Binance founder Changpeng Zhao announced that First Digital would issue stablecoins on the BNB Smart Chain. Therefore, FDUSD's rise has been speculated to be driven by Binance.

2. Amidst the Stablecoin Trust Crisis, Real-Time Auditing New Paradigm Supports TUSD's Takeoff

As a veteran stablecoin, TUSD's rise this year is also more traceable. TUSD was originally issued by TrustToken and was launched on Ethereum in March 2018, with its listing on Binance following in May 2018. TrustToken has also received investments from well-known institutions such as Blocktower, a16z, and Alameda.

The TUSD team has remained low-profile, leading to widespread speculation after its rapid rise this year. In fact, as early as December 2020, TrustToken officially announced the transfer of TUSD's ownership to the Asian consortium Techteryx. It is reported that Techteryx has a global presence, with offices in Asian countries and regions such as Singapore and Hong Kong. Additionally, Techteryx has established long-term partnerships with industry-leading companies to enhance user trust in TUSD and promote its adoption and development.

The acquisition of TUSD has further focused on safety and transparency to gain more user trust. According to official information, TUSD is the first U.S. dollar stablecoin to have its underlying reserves verified in real-time by an independent third-party organization.

The continuous efforts in safety and transparency, such as reserve verification, have brought TUSD a significant turning point in early 2023. The series of collapses in the crypto market last year had already weakened user trust in crypto assets, and this year, the regulatory crackdown on BUSD and the de-pegging issues of USDC led to a trust crisis in stablecoins. Who can provide a more reliable stablecoin asset naturally became the first choice for some trading platforms and crypto users.

At this moment, TUSD provided a good answer. In February 2023, TUSD announced the use of Chainlink's reserve proof technology to ensure minting security, further ensuring TUSD's transparency and reliability. TUSD also became the first stablecoin to achieve real-time on-chain verification of off-chain reserves and programmatically control minting.

In March 2023, TUSD announced a partnership with The Network Firm to provide real-time auditing services. It is reported that The Network Firm is an independent accounting firm in the U.S. focused on serving the digital asset industry, and its founding team has a strong background, having accumulated experience in traditional tax and auditing services while deeply engaging in crypto-native auditing and assurance services since 2016. After partnering with The Network Firm, TUSD's reserves can maintain 24-hour real-time auditing, thus achieving more stable transparency.

Currently, users can check TUSD's reserve proof and automatic audit results in real-time through its official website tusd.io.

Real-time reserve proof and auditing provide TUSD with minting security, transparency, and reliability. After BUSD faced regulatory crackdowns, TUSD became one of the preferred stablecoins for platforms and users like Binance. Blockchain data from Nansen shows that after BUSD faced challenges, Binance minted approximately $130 million worth of TUSD within a week. This also led to a rapid increase in the circulating supply of TUSD, surpassing Frax Finance to become the fifth-largest stablecoin by market capitalization. Subsequently, Binance and OKX also adjusted the transaction fees related to TUSD to increase its adoption. As of now, TUSD is active on over 100 trading platforms, including Binance, Coinbase, OKX, HTX, and Gate.io, and circulates across more than a dozen mainstream public chains such as Ethereum, TRON, Avalanche, and BNB Chain.

Moreover, the adoption of TUSD by crypto trading platforms and users has allowed TUSD to make strides in the global payment sector. Recently, TUSD established a partnership with international payment service provider ivendPay, entering ivendPay's payment option list. It is reported that ivendPay operates in seven countries and has over three hundred active merchants. Previously, TUSD has also been used in various scenarios, including partnerships with Web3 shopping platform UQUID, Web3 freelance marketplace HYVE, and travel platform Travala.com. This means TUSD has established broader accessibility and usability for users.

III. Conclusion

In 2024, with the recovery of the crypto market, the stablecoin market also has greater growth potential. While leading stablecoins like USDT, USDC, and DAI hold their ground, rising stablecoins like TUSD and FDUSD, as well as new players like yield-bearing stablecoins and Web2 giants, will compete for the incremental market.

However, in this new competition, as the regulatory policies for stablecoins gradually clarify, safety and transparency remain one of the core themes of stablecoin development. In the major changes of the stablecoin market in 2023, we have seen existing stablecoins like USDC suffer significant blows due to safety concerns, while stablecoins like TUSD have welcomed significant turning points due to their establishment of new paradigms in safety and transparency. Stablecoins that can achieve breakthroughs in reserve proof and auditing, continuously enhancing safety and transparency, may have greater growth potential.