Dialogue with MakerDAO Core Engineer: RWA is the Bull Market Engine, Stablecoins are the Killer App

Only by internalizing interest rates into decentralized finance can decentralized finance thrive again.

Only by internalizing interest rates into decentralized finance can decentralized finance thrive again.Guests: Sam Macpherson, Core Developer of MakerDAO; Tadeo, Developer Relations Engineer at Spark Protocol

Author: Sunny, Deep Tide TechFlow

"I believe the entire financial system will ultimately run on the blockchain, and there will be no more defaults from traditional finance; it will simply be finance, and all transactions will be settled on the blockchain. So, I don't know how long this will take, but to me, it's an inevitable future." --Sam Macpherson, Core Developer of MakerDAO

Background of the Conversation

At this year's Token2049 conference in Singapore, MakerDAO founder Rune Christensen proposed the "Ultimate Plan." This plan aims to address the scalability and inefficiency issues within MakerDAO. The "Ultimate Plan" suggests a transformation of the role of Maker Core. Instead of directly pursuing various small projects and growth plans, it will shift to a role more akin to that of a "wholesale creditor." In this new role, Maker Core will provide loans or support to other sub-DAOs (sub decentralized autonomous organizations) that will operate independently. These sub-DAOs are described as mini versions of MakerDAO, each focusing on different growth plans and projects. These sub-DAOs will be isolated from each other and operate independently.

Spark Protocol is an emerging sub-DAO aimed at establishing a lending protocol focused on DAI and has integrated with MakerDAO. Sam Macpherson is the founder and CEO of Spark Protocol and has previously served as a core engineer at MakerDAO. Tadeo is the Developer Relations Engineer at Spark. Since the end of 2022, the total value locked (TVL) in Spark Protocol has exceeded $1 billion. At the Ethereum Developer Conference in Istanbul last month, Spark Fi sponsored ETHGlobal Istanbul with a prize of 20,000 DAI to reward winning builders in the Spark Lend category. The Spark team aims to build a decentralized lending engine that provides users of DAI with the features and capabilities of a modern lending platform, as the existing MakerDAO core contracts are considered somewhat outdated.

During the interview with Sam and Tadeo, we learned that Spark does not require third-party liquidity, which differentiates it from other DeFi lending protocols, the impact of U.S. Treasury bonds on the Web3 market, and whether stablecoins are the killer application for Web3.

Sam firmly believes that real-world assets (RWAs) will trigger the next complete market equilibrium. Currently, traditional financial interest rates are so high that they essentially siphon all liquidity away from decentralized finance (DeFi). So the first step is to bring those interest rates on-chain, allowing the interest rates of decentralized finance and traditional finance to continue converging until they match. Only by internalizing interest rates into decentralized finance can DeFi thrive again. And all of this is already happening.

Here is a summary and conclusion from Deep Tide regarding this interview:

Knowledge Repository

MakerDAO:

MakerDAO is a decentralized autonomous organization operating on the Ethereum blockchain. It is known for its stablecoin DAI, which is backed by collateralized assets. MakerDAO allows users to generate DAI by locking collateral in smart contracts known as vaults or collateralized debt positions (CDPs).

Users can interact with MakerDAO through Web3 wallets and other decentralized applications (such as Lido and Aave v3).

The stablecoin DAI issued by MakerDAO has become one of the top stablecoins by market capitalization.

DAI's Over-Collateralization Model:

DAI is described as an "over-collateralized" stablecoin. This means that to create and maintain DAI, users need to deposit collateral (cryptocurrency or other forms of value) that is worth more than the DAI they create. This over-collateralization serves as a safety mechanism to maintain the stability of the stablecoin.

Importantly, the collateral backing DAI includes native cryptocurrency assets (such as ETH) and other assets, such as "sticky assets" (possibly referring to stable assets within the MakerDAO ecosystem) and Bitcoin. Additionally, it includes cash-like assets, which could be stable assets or fiat currency.

The over-collateralization ratio of DAI is precisely 0 or equal to 1, which differs from other stablecoins that require higher collateralization ratios (e.g., 150% or 200%). This means you can generate DAI using collateral equivalent to the amount of DAI you create. This is a unique feature of DAI.

MakerDAO's Native DeFi Protocol: Spark

Since the introduction of the modern lending engine within the MakerDAO ecosystem, Spark has experienced significant growth, making it one of the top 20 protocols by total value locked in DeFi.

Secondary Lending Markets: The interview mentioned secondary lending markets, such as Compound and Aave, which allow users to borrow various cryptocurrencies, including stablecoins like DAI, USDC, or Tether (USDT).

Need for Intermediaries: In these secondary lending markets, intermediaries or lenders are needed to provide liquidity. These lenders need to have a certain asset reserve (e.g., DAI, USDC) and seek to profit by lending these assets to borrowers.

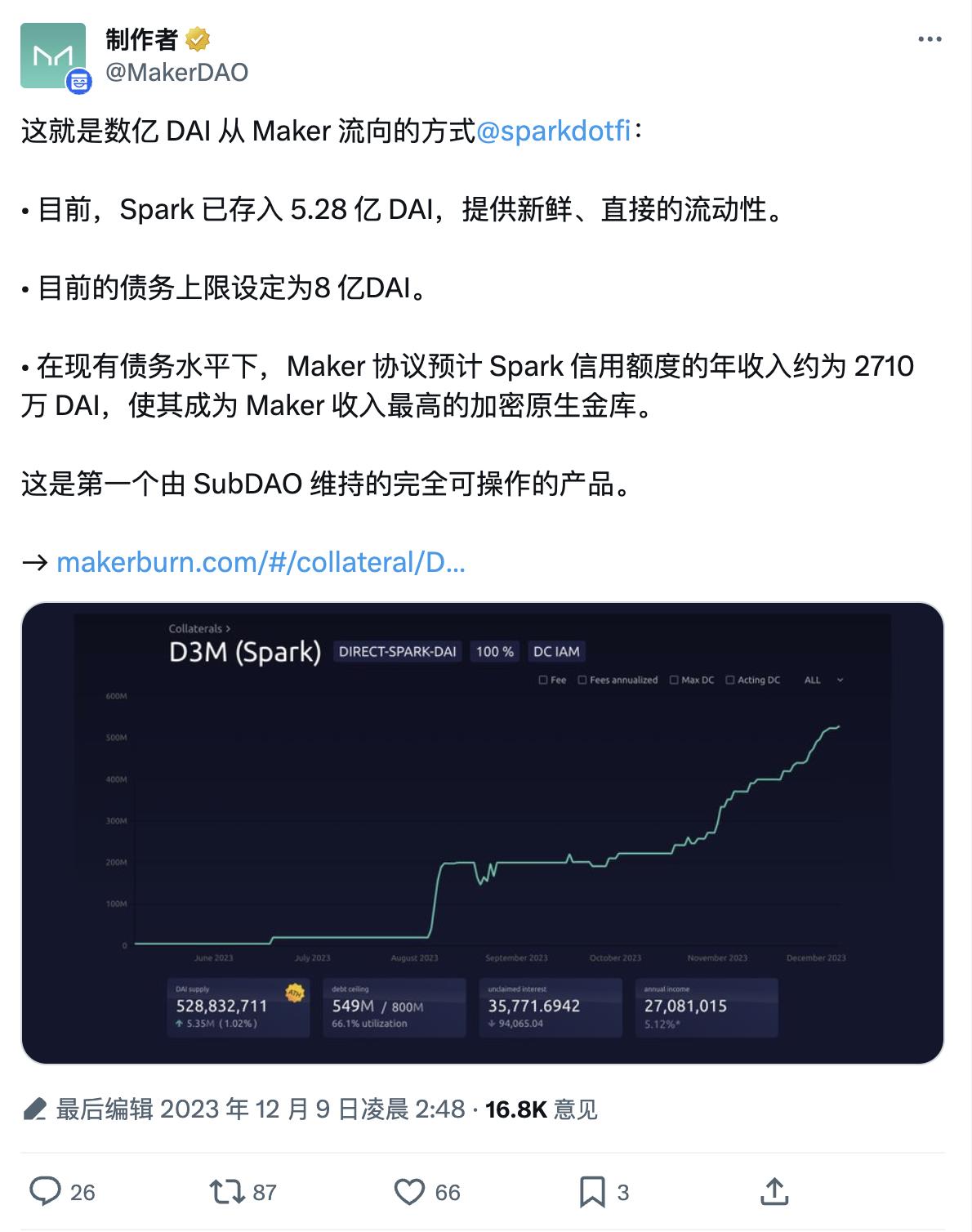

Role of Maker in Spark: The innovation introduced by Spark is that MakerDAO itself can act as a lender on this platform. In other words, instead of relying on profit-driven individual lenders, liquidity is provided directly by MakerDAO.

Minting DAI: MakerDAO can directly mint DAI tokens onto Spark's lending platform. When users want to borrow DAI, they are essentially borrowing directly from MakerDAO, similar to how the internal vault system of MakerDAO operates.

Predictable Borrowing Rates: One of Spark's main advantages is that users can borrow at predictable rates set by MakerDAO. In contrast, rates in other secondary markets can be highly volatile and depend on the availability of liquidity. Sometimes rates can spike to very high levels, creating uncertainty for borrowers.

Governance Process: Spark's predictable rates are maintained through a clearly defined governance process. Users are notified weeks in advance of any upcoming rate changes. This advance notice allows users to plan and adjust their positions accordingly.

Minimum Rates: Due to MakerDAO's substantial liquidity (which Sam referred to as "unparalleled liquidity"), the rates on Spark are expected to be the lowest in the entire market. This makes borrowing more cost-effective for users.

The Background of RWAs

Historical Context: Two years ago, traditional banks and money market funds offered very low rates (around zero) to users holding USDC. This meant users were content to keep their USDC on-chain for various purposes, such as trading Ethereum (ETH).

Changes: Over the past two years, traditional banks have begun paying customers higher rates (in this example, 5%). This change in rates has made holding USDC on DeFi more expensive, as users can now earn potential interest income by transferring USDC to their bank accounts.

Changes in User Behavior: Due to this change in rates, users are more inclined to consider moving their USDC out of DeFi and into their bank accounts. This action has removed liquidity (funds) from the DeFi ecosystem, potentially impacting DeFi projects and markets.

Tokenization of Treasury Bonds: To address this issue, the tokenization of U.S. Treasury bonds has been mentioned. This refers to the process of converting U.S. Treasury bonds into digital tokens that can be used within the DeFi ecosystem. Users can use these tokenized Treasury bonds as collateral for lending and other DeFi activities.

Impact on DeFi Rates: By tokenizing and introducing Treasury rates (the interest rates of Treasury bonds) into DeFi, users can now earn interest on their tokenized Treasury bonds while participating in DeFi activities. As more users use these tokenized assets as collateral, DeFi platforms begin to offer higher lending rates and other service rates. The effect of this is to raise the baseline rates within the DeFi ecosystem.

Rate Comparison: Sam mentioned that DeFi lending rates, which were previously close to 0%, are now typically between 3% and 4%. This means that DeFi lending rates have become competitive with the risk-free rates offered by Treasury bonds.

The Next Killer Application for Mass Adoption

Web3 Needs a Killer App: Sam and Tadeo acknowledged the importance of having a compelling and widely adopted application (a "killer app") that can drive the adoption and use of blockchain and cryptocurrency technology among everyday retail users. However, they admitted they do not have a specific idea for such an application but emphasized the importance of building the underlying infrastructure.

Current Retail Use Cases: Currently, in the cryptocurrency space, the primary use case for retail users is seen as speculative investment, where individuals buy and hold cryptocurrencies, hoping their value will grow over time. However, Sam believes that this situation will change in the future as scalable blockchain solutions become more prevalent.

Potential of Stablecoins: Tadeo pointed out that stablecoins have already shown potential as a retail use case. Stablecoins are digital assets designed to maintain stable value, making them suitable for everyday transactions. They are considered a superior product compared to traditional fiat currency, especially for cross-border payments, primarily due to the inefficiencies of systems like SWIFT and the high costs of international money transfers.

Challenges of Stablecoins: Despite the potential of stablecoins, the speakers mentioned that there are still challenges to be addressed. They expressed a desire to improve stablecoins to make them more practical and user-friendly for everyday transactions (such as buying coffee).

Both Sam and Tadeo believe that speculative investment and using stablecoins for cross-border payments are currently two prominent retail use cases, but there is still room for improvement and innovation in making cryptocurrencies more accessible for everyday transactions.

Conclusion

When asked whether more engineers are increasingly choosing to join Web3, Tadeo pointed out an interesting phenomenon regarding the correlation between developer commits and Ethereum prices. As prices rise and fall, the number of commits also rises and falls (the recent decline may be due to the holiday season). Therefore, as RWAs drive the next bull market, it is believed that more developers will join the industry to promote the development of infrastructure.

Source: https://cryptometheus.com/project/ETH

Note: Protocol Security

Sam acknowledged the inherent risks of smart contracts within the DeFi space. However, they emphasized that extensive precautions have been taken to minimize these risks. This includes having their smart contracts audited multiple times by independent auditors and conducting internal reviews to ensure a deep understanding of the code. The goal is to provide the highest level of security for user funds and to follow best practices in smart contract development.