Payment Financial Geography | A Global Perspective on Crypto Adoption: Exploring Financial Freedom in Turbulent Economies

Interview residents from 7 countries and regions, trying to explore the role of Crypto from the perspective of payment finance, and investigate how the adoption of Crypto affects local life.

Interview residents from 7 countries and regions, trying to explore the role of Crypto from the perspective of payment finance, and investigate how the adoption of Crypto affects local life.Author: Ivy, Youbi Capital

When a country's economy is on the brink of collapse, Bitcoin and stablecoins seize the opportunity to gain popularity among the public, as seen in Ukraine, Turkey, and Argentina. Over the past decade, the Turkish lira, Argentine peso, and South African rand have been among the three weakest currencies globally.

In regions where fiat currencies are weak, foreign exchange controls are in place, and mainstream currencies like the dollar and euro lack liquidity, Crypto finds fertile ground—providing local residents with tools for value storage and financial freedom.

Crypto presents two faces in different regions: it is a speculative target in developed areas and a financial liberator in emerging regions. I once heard an Argentine friend talk about using Crypto to pay for his clinic fees, renew his Spotify subscription, and shop at the supermarket. This was a scene I could hardly imagine, which inspired this research. During my time at ZuConnect, I interviewed residents from seven countries and regions, attempting to explore the role of Crypto from the perspective of payment finance and how its adoption affects local life.

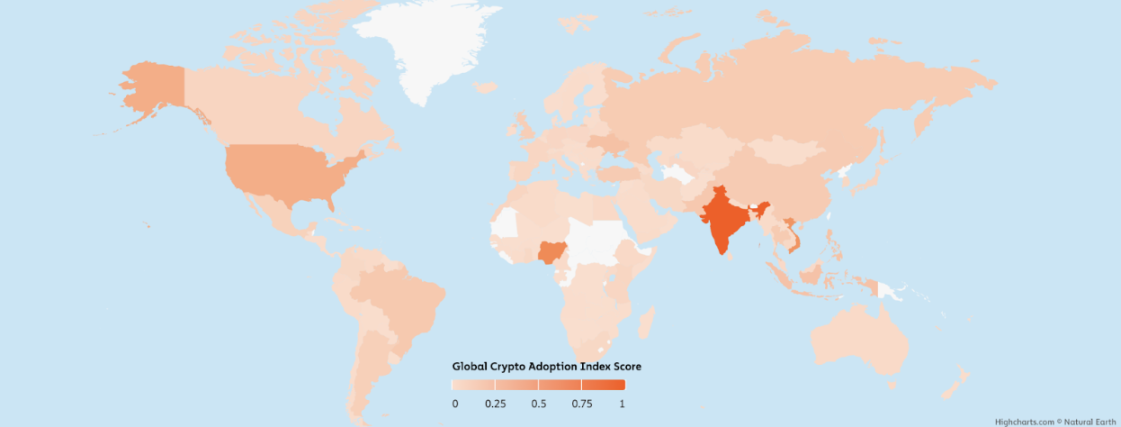

Figure: Crypto adoption rates in 2023, with Nigeria, Vietnam, Turkey, and Argentina ranking 2nd, 3rd, 12th, and 15th respectively.

Source: https://www.chainalysis.com/blog/2023-global-crypto-adoption-index/

1. Turkey - 52% of Turkish adults invest in Crypto, financial freedom, and relaxed regulations

Overview

With inflation soaring to 80%, no foreign exchange controls, the lira freely traded against the dollar and euro, a highly developed banking system, and easy account opening with low KYC requirements, this is the financial condition and regulatory environment in Turkey.

The investment threshold for crypto is low: local licensed exchanges (binance tr & coin tr) allow direct deposits and withdrawals to bank accounts, and even cash transactions (in dollars/lira/euros) at offline stores. There are many shops in bustling areas where fiat currencies are exchanged for crypto, with real-time prices flashing like a barrage. These cash exchange shops operate legally and must pay taxes to the government. However, crypto payments are illegal, as merchants report their earnings annually, and income tax is a core source of government revenue.

Free flow of foreign exchange: Individuals face no restrictions on currency exchange, while corporates have an upper limit of 800,000 USD. There are numerous currency exchange shops, and no KYC is required, making it easy for Turks to hold dollars and euros for savings.

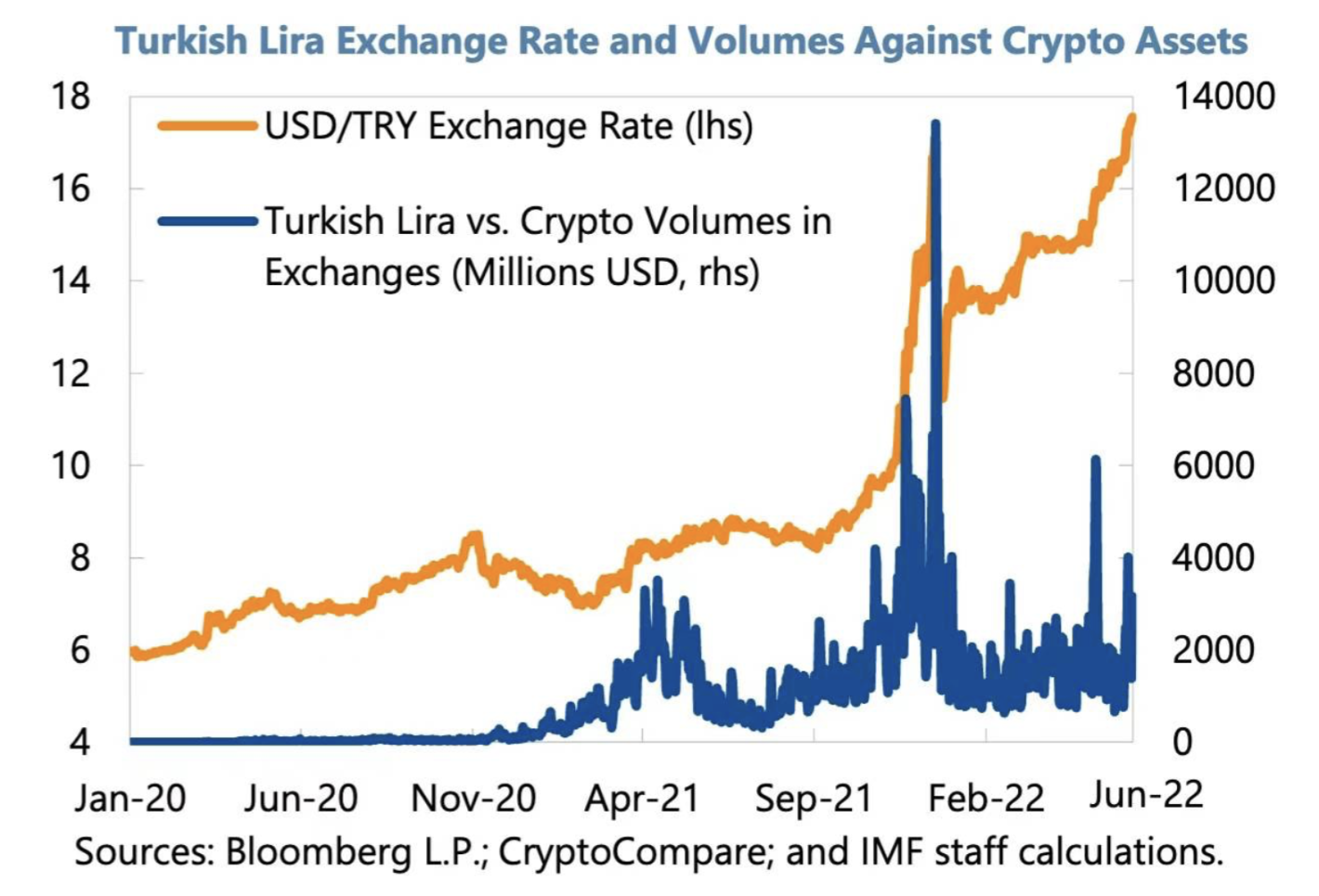

Figure: Trading volume of USDT/TL far exceeds that of other Emerging Market currencies.

In 2021, the lira collapsed against the dollar, and USDT/TL even surpassed USDT/USD in trading volume at one point.

Figure: The collapse of the lira against the dollar in November 2021,

with daily crypto trading volume approaching half of Turkey's daily foreign exchange trading volume.

Cross-border remittances: Local PayPal has been unavailable since 2016 due to regulatory issues, and people generally use Wise or Western Union.

Cards as mainstream payment: The use of debit and credit cards is widespread in Turkey. According to data from the Turkish Interbank Card Center (BKM), there were a total of 291 million credit and debit cards in Turkey in 2021, including 150 million debit cards and 83.8 million credit cards. Turkey ranked first in Europe in terms of total number of cards in 2021. The total transaction volume using credit and debit cards reached 17.1 trillion lira in 2021.

The Turkish banking sector is highly developed, far surpassing that of Europe. There are over 50 commercial banks, most of which can provide an experience comparable to Alipay.

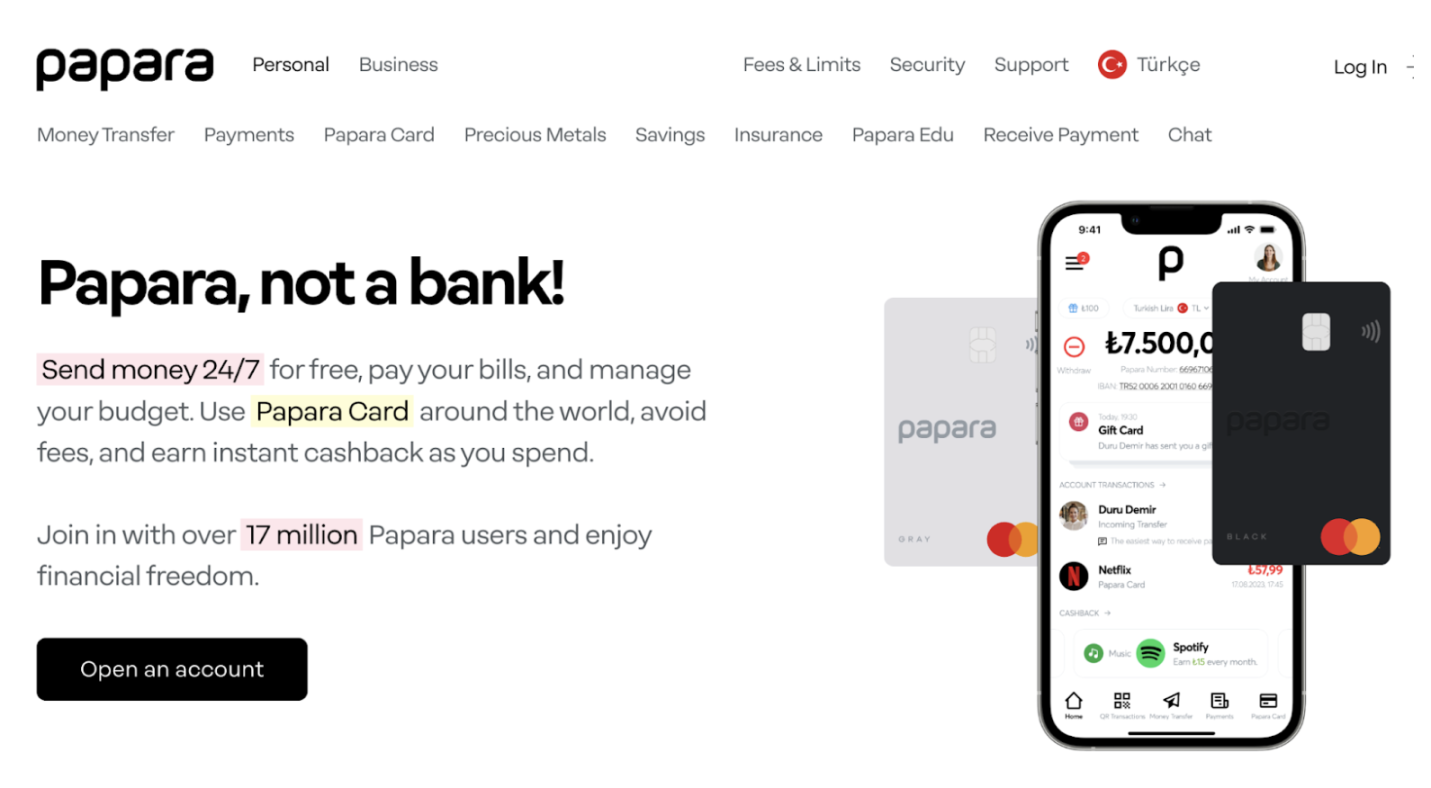

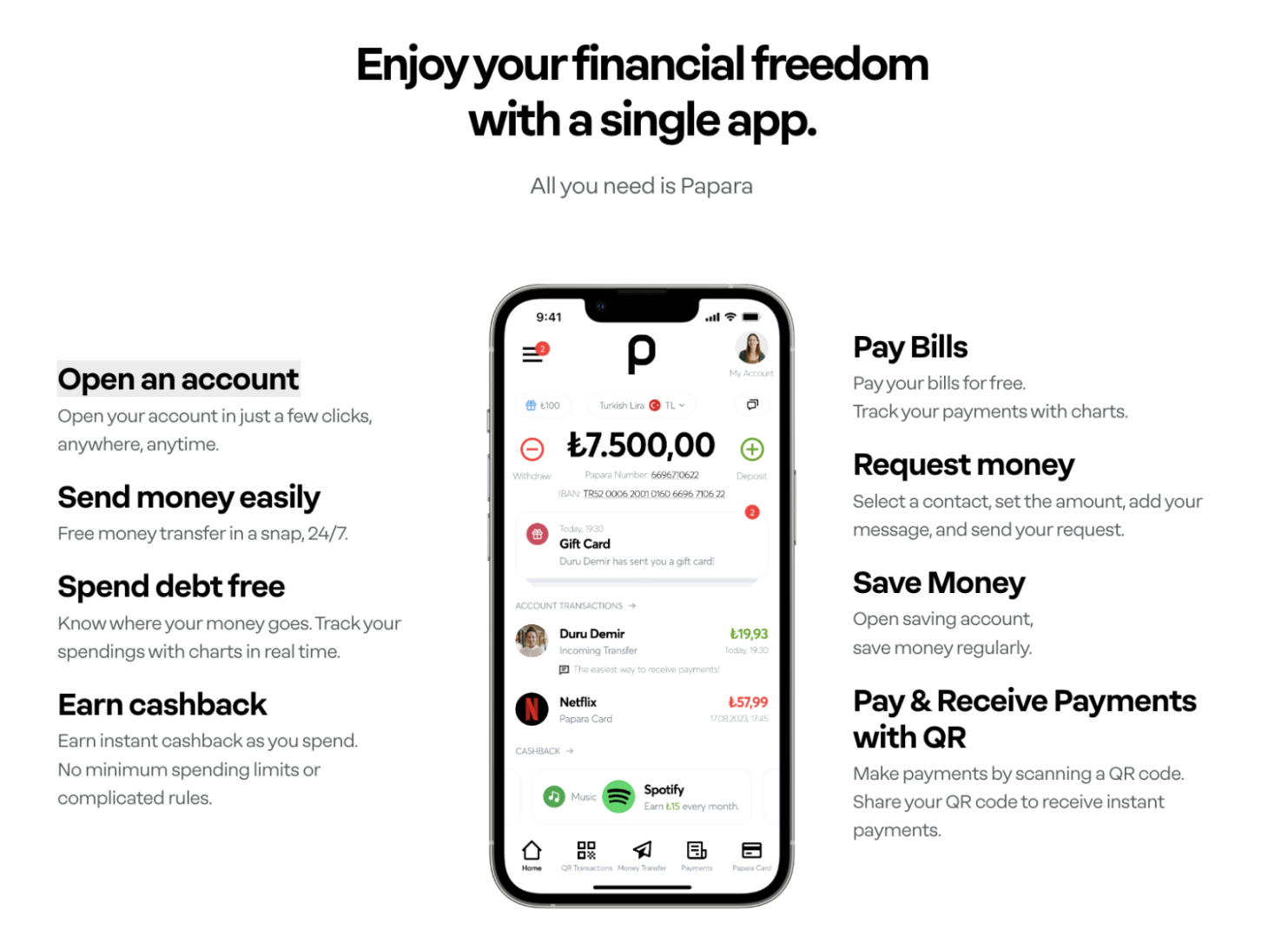

Relaxed fintech regulations: Despite having a developed banking system, the proportion of unbanked individuals in Turkey remains as high as 26%. A payment product outside the banking system, Papara, has 17 million users and only requires a local Turkish phone number and email, with no ID KYC needed. Transfers incur no fees, and it issues physical cards in partnership with Mastercard, regulated by the Turkish central bank, balancing a degree of financial freedom unique to decentralized wallets with the convenience of card payments.

Case Study: Papara, a payment product outside the banking system

Figure: Papara exists outside the banking system, offering a card experience through Papara Card.

Figure: Papara product features include sending and receiving currency, paying bills, and subscription payments.

Source: https://www.papara.com/en

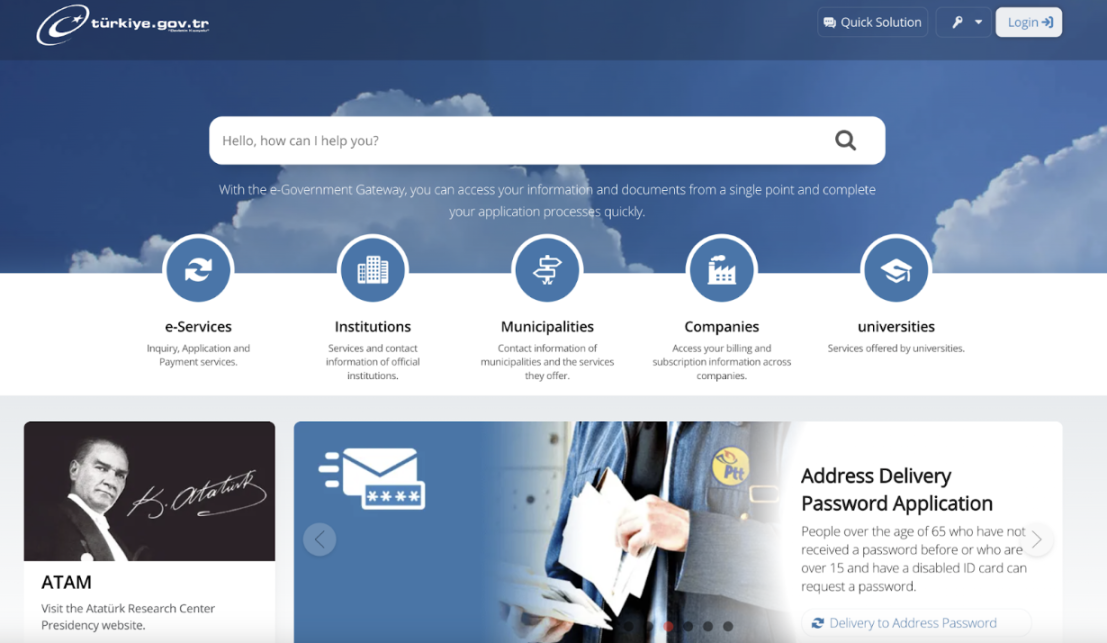

High degree of digitalization in population information/residency/government affairs: Residents can handle all government affairs at home, including paying fines, filing taxes, applying for passports, and obtaining student enrollment certificates.

Figure: Turkey's public government platform.

Source: https://www.turkiye.gov.tr/

Smooth deposit and withdrawal channels: Licensed exchanges Binance TR and CoinTR allow direct withdrawals to various bank accounts, with a fee of only 3 TL.

Crypto Adoption Rate

As of October 2022, approximately 8 million people actively invest in cryptocurrencies. If direct relatives are included, the number is about 14 million.

Source: https://www.kucoin.com/blog/more-than-half-of-Turkish-adults-invest-in-crypto

Turkish Crypto Exchanges:

Licensed exchanges in Turkey support bank card deposits and withdrawals.

- Binance TR

- CoinTR

Common local exchanges in Turkey: Local exchanges Paribu and Btctürk both have over 6 million registered local users.

- https://www.btcturk.com/

- https://www.paribu.com/ https://ventures.paribu.com/

- https://www.bilira.co/

Figure: The BtcTurk trademark is visible throughout Istanbul Airport.

Source: Author's photo

Notably, among the exchanges is the state-owned enterprise CoinTR. CoinTR has partnered with two national banks in Turkey, Ziraat Bank and Vakif Bank, to establish fiat deposit and withdrawal channels. It operates more like a company formed by regulatory authorities, traditional banking institutions, and international tech teams, aiming from the outset to address Turkey's currency exchange and dollar reserve issues.

2. Argentina - 25% of Argentine adults frequently trade Crypto and use it as a daily payment currency

Overview

People in Latin America need to address issues such as inflation, remittances, value protection, and savings. They enjoy the benefits of Crypto and have become its most enthusiastic supporters. In Argentina, it has become mainstream, with about 5 million people (out of a total population of 45.8 million) using it.

Figure: Crypto trading volume surges as the Argentine peso faces inflation.

Source: Chainalysis

Inflation: In October 2023, Argentina's inflation rate soared to 121%, and such inflation has persisted for years.

Foreign exchange controls: The Argentine central bank faces a shortage of foreign exchange and implements foreign exchange controls to prevent capital flight. The central bank mandates that exporters must repatriate profits from overseas sales within five days, and institutions and banks require authorization to purchase dollars in the foreign exchange market. Argentine citizens are limited to a monthly dollar purchase quota of no more than 10,000 USD.

The desire for dollars and foreign exchange controls have given rise to a black market, with the black market exchange rate soaring nearly 600 times in 2023. When people cannot obtain dollars, they seek alternatives, namely crypto. This financial environment has fostered a demand among Argentines for investment, inflation resistance, and financial freedom—approximately 25% of adults in Argentina hold crypto.

Crypto Adoption Rate: According to Americas Market Intelligence data, Argentina's cryptocurrency adoption rate is growing rapidly. By the end of 2021, only 12% of Argentine smartphone users had purchased cryptocurrencies, but by April 2022, this number had risen to 51%. Additionally, as many as 27% of Argentine consumers claim to be regularly purchasing cryptocurrencies.

Local Exchanges in Argentina

- Binance

- Bybit

- eToro

- OKX

- Gate.io

Figure: Binance advertisement—Argentine merchants contribute to financial freedom in Latin America through Binance P2P.

Economic Structure and Geographic Factors

Argentina has about 50% of its economy in the gig sector, with a significant demand for cross-border payments. Argentina shares the same time zone as North America, and its education level ranks among the highest in Latin America, providing Argentines with ample time and space to offer R&D services to North American companies.

Crypto in the Daily Lives of Argentines

According to AMI statistics, 71% of Argentines hold crypto for investment, 67% for inflation resistance, and 46% for financial freedom.

- Daily Life: 25% of Argentines frequently use crypto for daily consumption and savings. Ordinary housewives can skillfully use cryptocurrencies for everyday shopping and paying clinic fees.

- AMI data shows that Argentina is an important market for crypto debit and credit cards. For example, Mastercard and Binance have decided to jointly launch prepaid crypto debit cards nationwide. According to Mastercard statistics, at least 51% of Latin Americans use cryptocurrencies for shopping. Furthermore, between 2021 and 2022, the total crypto inflow to Latin America exceeded 56.2 billion USD, a 40% increase compared to 2020.

Figure: In the past year and a half, the number of debit cards issued by local exchanges such as Lemon, Buenbit, and Belo has rapidly increased.

- Value Storage Investment: According to AMI survey data, over 50% of Argentines purchase crypto assets as a "hedge against inflation," similar to gold and other assets.

- Remittances: The World Bank reports that Argentina receives about 650 million USD in remittances annually. Chainalysis has found that an increasing number of Latin American immigrants use Bitcoin to remit money to their families back home. Argentines can now access the Bitcoin Lightning Network through applications like Strike, and more Argentine immigrants are beginning to enjoy the benefits of cross-border transactions using cryptocurrencies.

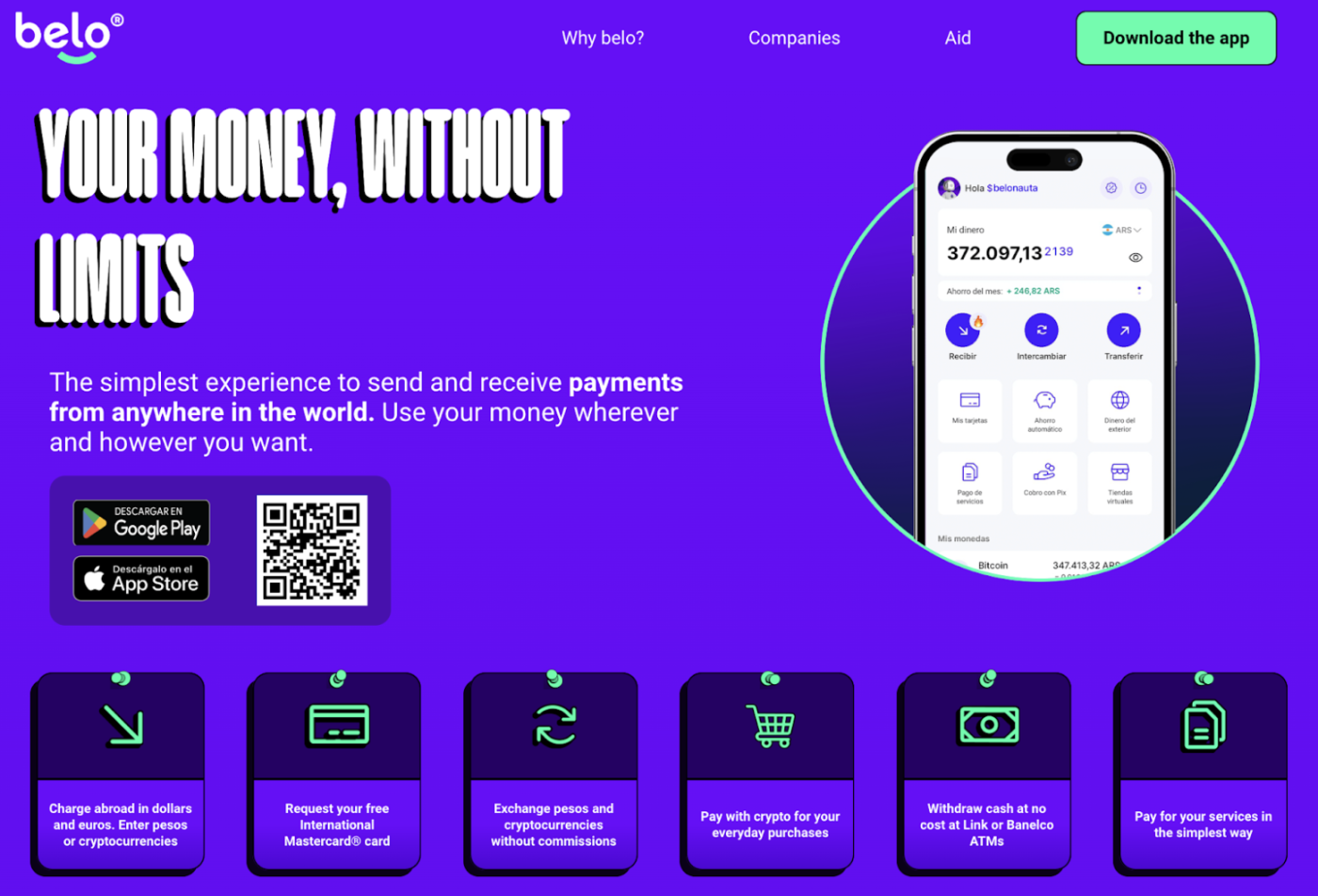

Case Study: Crypto Payment App Belo—Providing Argentines with Tools for Value Storage and Financial Freedom.

Belo is a local payment app in Argentina that combines the advantages of web2 and web3, integrating the banking system, fintech, and crypto payments. The receiving end can achieve cross-border payments without review, allowing for quick and secure fund transfers. The paying end allows the payer to spend crypto directly while the recipient receives fiat currency, akin to a debit card experience.

However, opening a Belo account requires an Argentine ID/passport.

Figure: Belo—Providing Argentines with tools for value storage and financial freedom.

Source: belo.app

Payment Features:

- Card Payments: Payers can spend crypto, while recipients receive fiat currency. C-end users can spend any crypto (BTC, ETH, USDT) and pay in fiat (Argentine pesos) in the form of a debit card, receiving a similar experience to Mastercard, with 2% cashback on each transaction.

- Daily consumption payment features are numerous and highly localized, including phone top-ups, utility payments, financial insurance payments, basic service payments, shopping services, dining services, and telecom services (supporting four telecom operators), among others. Users can also create an unlimited number of virtual cards, similar to Wise, with each virtual card having a daily spending limit for various subscription services.

Receiving/Reloading:

- Transfer to Payoneer Balance

Transfer the balance from Payoneer (a Latin American online payment company) to Belo with no delay. Funds will be automatically converted to USDC at the current exchange rate upon deposit for storage, exchange into other cryptocurrencies, or use with the Belo Mastercard. A 4% commission is charged for deposits, with a minimum amount of 5 USD, and a maximum of 5 withdrawals per day, amounting to 5,000 USD.

- Cross-border Receiving of Euros

Belo supports SEPA transfers to receive euro payments. In the future, it will also support receiving dollar payments through SWIFT and ACH transfers.

Incoming payments from abroad incur a 1.5% commission and may take 1 to 4 business days to arrive. The balance will be automatically converted to USDC at the current exchange rate, and it can also be exchanged for other cryptocurrencies. Accounts created with Argentine-issued DNI can use the Belo Mastercard.

- Directly Deposit Crypto via Address

Figure: Belo supports SEPA transfers to receive euro payments, transferring to Payoneer balance, and direct crypto deposits.

Source: https://help.belo.app/es/articles/5705712-ingresar-fondos-desde-el-exterior-a-tu-cuenta-de-belo

Key Success Factors: The Belo product is developed by Argentine founders, and the local team has several advantages:

- Deep insights into users' daily needs, with a high level of detail. As PG said, where it seems smooth, there are still gaps when magnified a thousand times, and these gaps are areas for product optimization, such as automatically converting peso balances to stablecoins with selectable conversion cycles (daily, weekly, monthly).

- Bridging web2 and web3 account systems: Transferring funds using crypto to local banks, fintech (Payoneer), and various account systems, achieving seamless connections between fiat and crypto, requires strong local relationships and resource integration.

3. Africa - Significant regional disparities, fragmented markets, ambiguous Crypto regulations, and limited infrastructure have solutions

Overview

Africa's situation is complex, with significant regional differences, 54 sovereign countries, and over 900 million people. Geographically, Africa is often divided into five regions: North Africa, East Africa, West Africa, Central Africa, and Southern Africa. Africans and Latin Americans are eager to share their experiences, hoping that the economic and financial conditions of their countries will be heard and seen by the world.

Mainstream Payments and Account Systems in Africa:

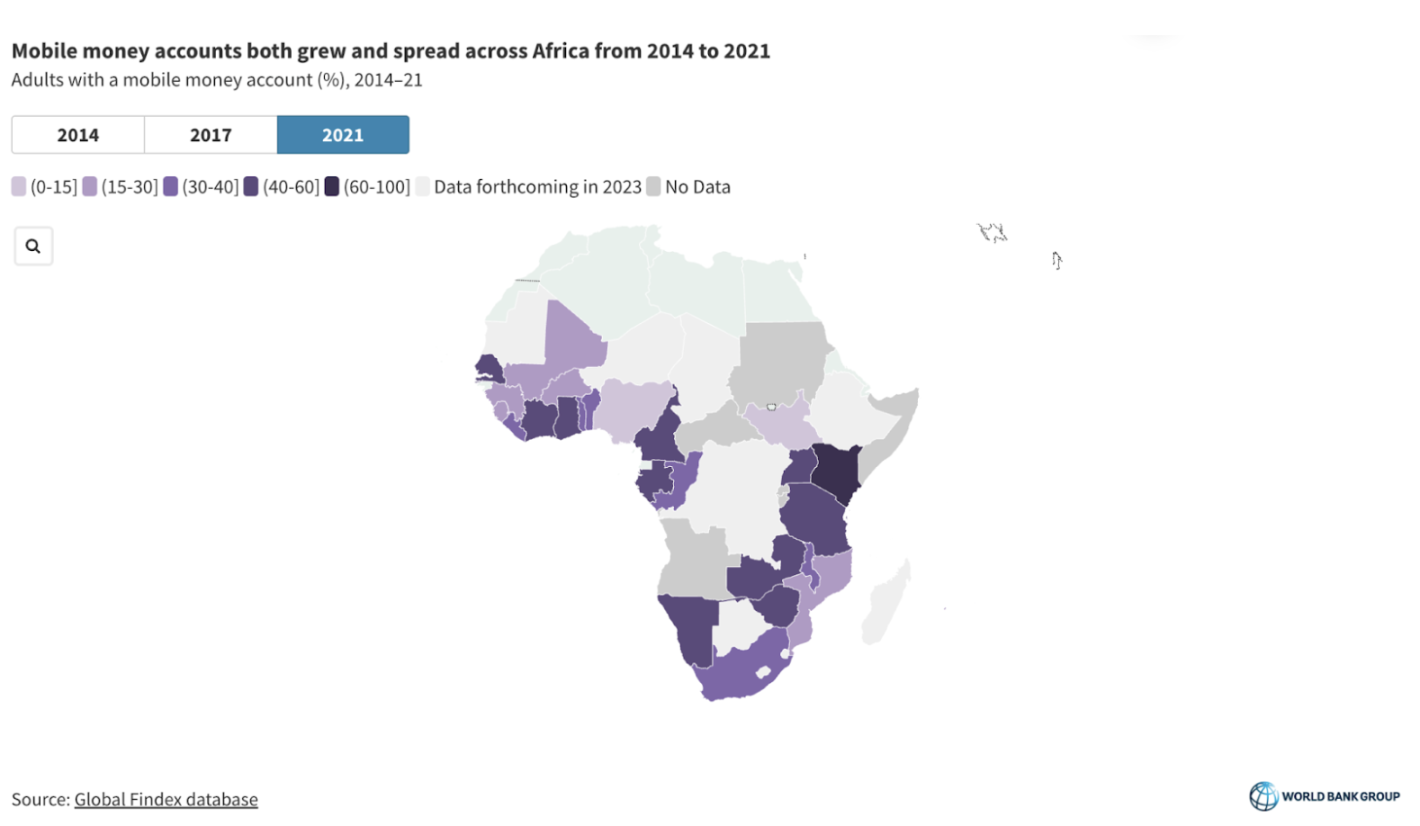

Mobile money is a significant driver of inclusive finance in sub-Saharan Africa, promoting account penetration through mobile payments, savings, and lending.

The penetration rate of mobile money accounts is high. Mobile money account owners use their accounts not only for P2P payments as originally designed. In 2021, approximately three-quarters of mobile account owners in sub-Saharan Africa used their mobile money accounts for or received at least one non-personal payment.

Mobile money accounts have also become an important savings method in sub-Saharan Africa, with 15% of adults (and 39% of mobile money account holders) using mobile money accounts for savings, a rate comparable to that of formal accounts at banks or other institutions.

Mobile money serves as the infrastructure for financial institutions. In sub-Saharan Africa, 7% of adults also use mobile money accounts for borrowing.

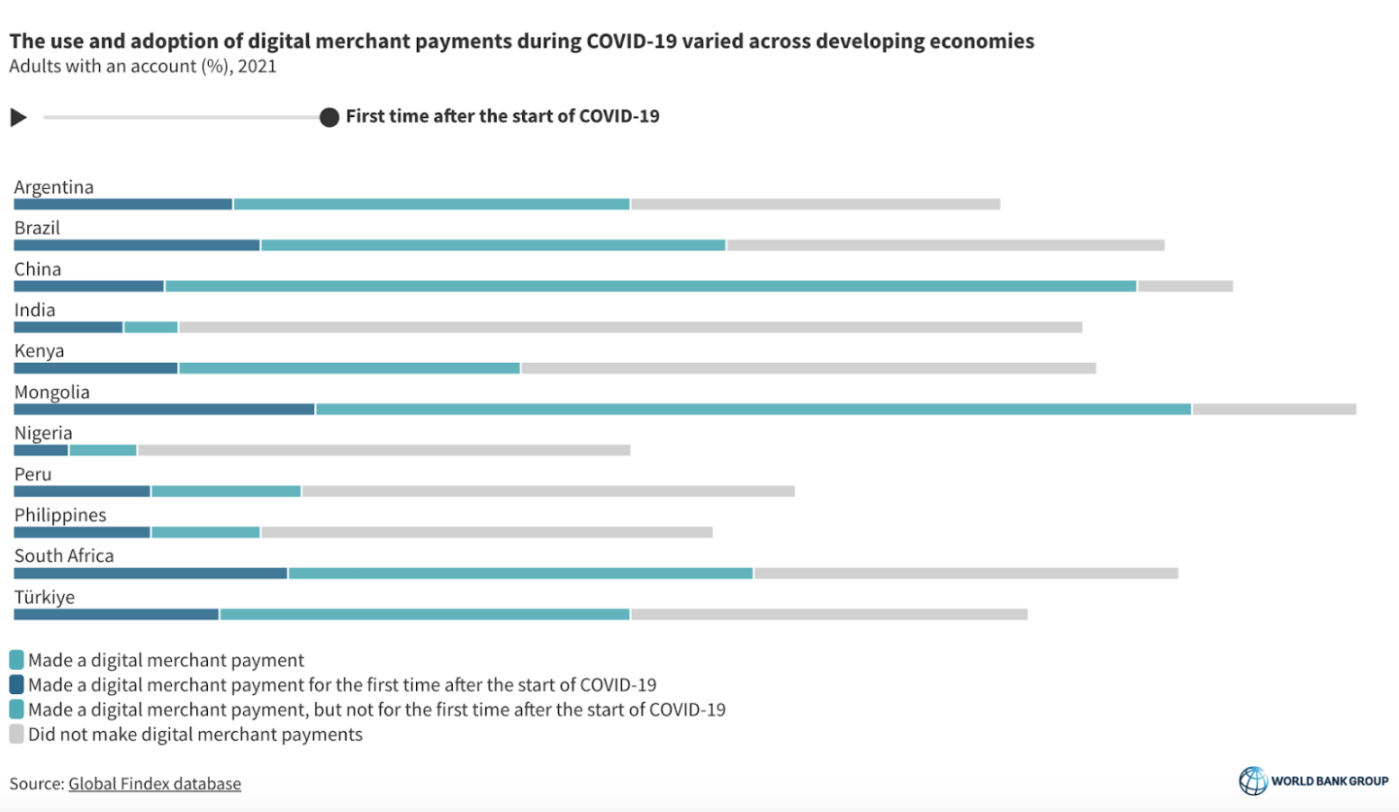

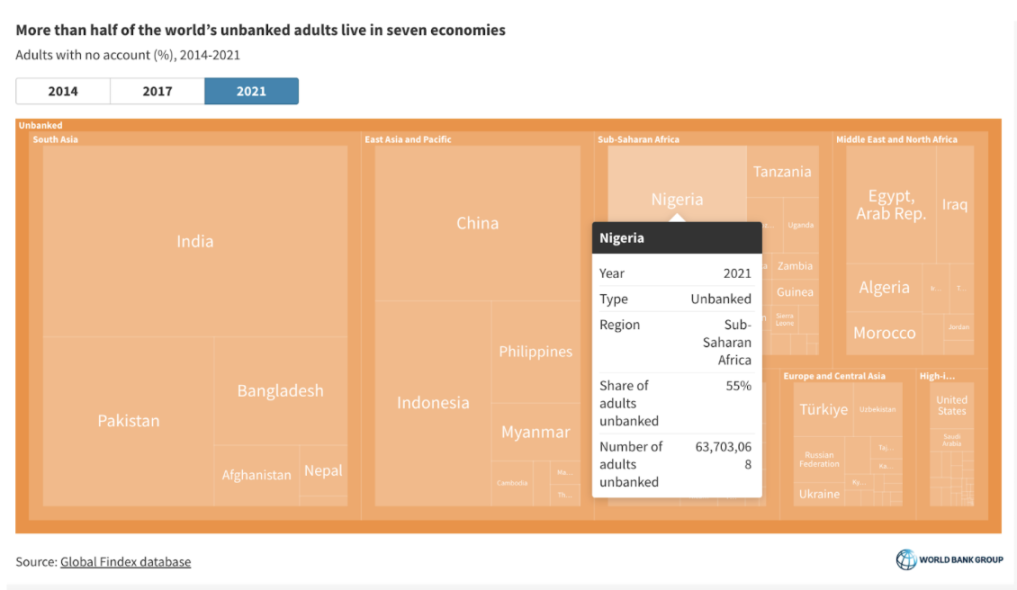

Figure: The World Bank's 2021 Global Financial Index found that 55% of adults in sub-Saharan Africa have accounts, with 33% having mobile money accounts.

Source: The Global Findex Database 2021

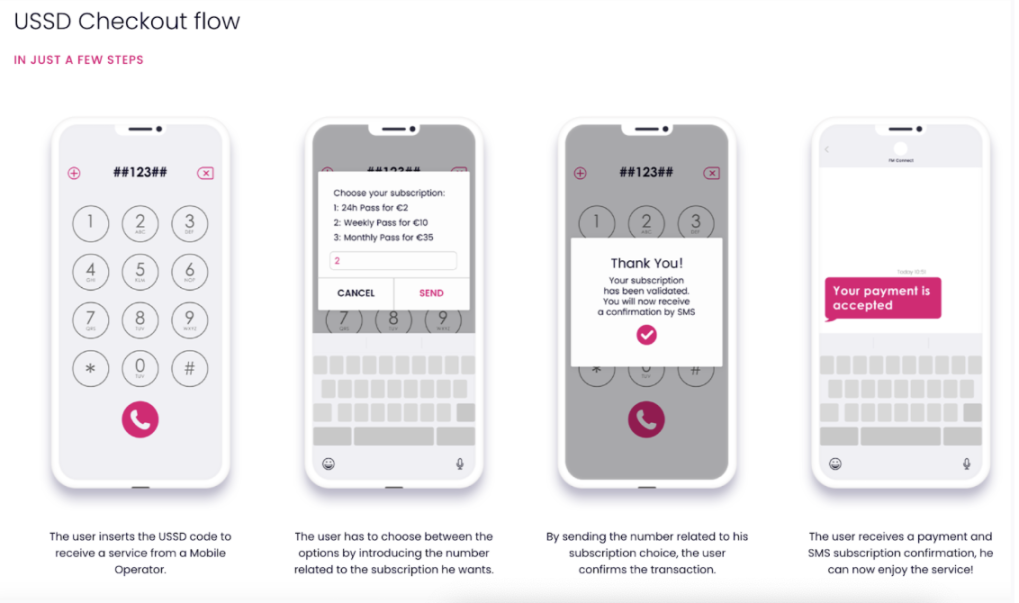

Mobile Money Technology Implementation: USSD

USSD has very low infrastructure requirements, making mobile money a powerful payment method in Africa. USSD technology allows users to create mobile wallets using their phone numbers to electronically store funds and directly transfer money, pay bills, recharge phone credits, and make payments to merchants on their phones. It is accessible and usable globally without an internet connection, meeting the needs of all types of consumers.

Figure: USSD technology allows users to create mobile wallets using their phone numbers to electronically store funds.

Source: Author's photo

Figure: USSD user flow.

Source: https://www.digitalvirgo.com/mobile-payment/ussd/#down

Nigeria - 25% of Nigerians hold Crypto, another solution for no-threshold financial services

Nigeria's currency is weak, with a significant disparity between black market and official exchange rates. According to World Bank statistics from 2021, the proportion of unbanked individuals in the region is as high as 55%. All of this greatly stimulates local demand for Crypto.

Figure: In 2021, the proportion of unbanked individuals in Nigeria reached 55%.

Source: The Global Findex Database 2021

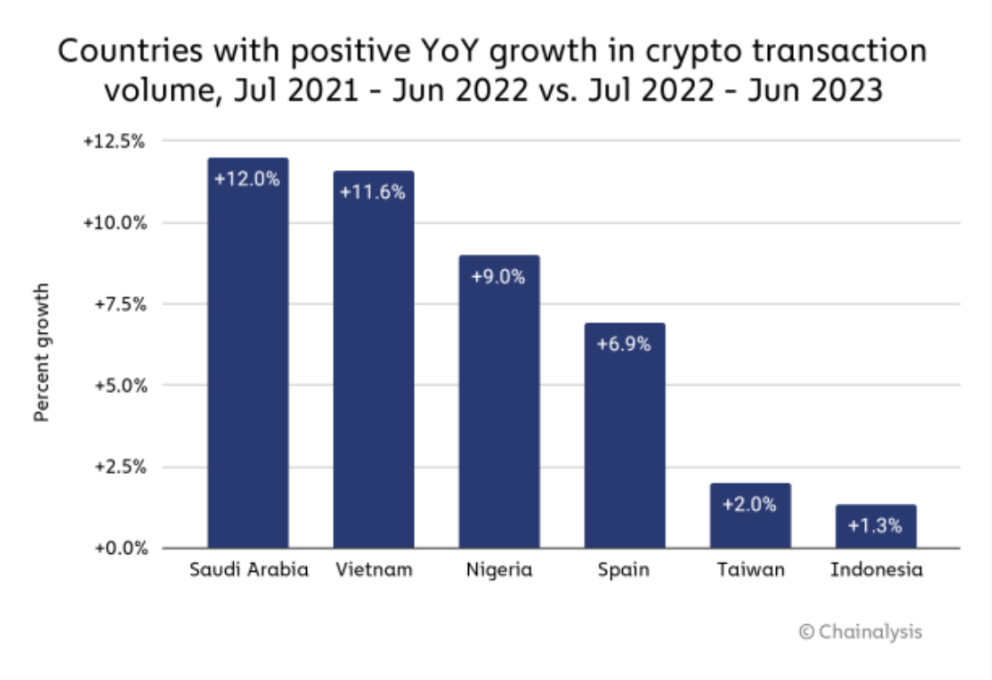

Figure: Nigeria's cryptocurrency adoption rate increased by 9% year-on-year.

Source: Chainalysis

The regulatory environment remains strict, with the majority of regions prohibiting the use of crypto payments. Binance C2C is the most commonly used deposit and withdrawal channel.

4. Vietnam - 16M Crypto holders, ample economic growth momentum, and a young population structure

Overview

Vietnam's crypto usage and regulatory situation are very similar to China's, with the vast majority holding crypto for speculative purposes, primarily using centralized exchanges for trading, and KOL-led trading being common. Additionally, Vietnam has a very high crypto adoption rate, increasing the market's attractiveness for global projects.

Foreign exchange controls: Vietnam has strict foreign exchange controls.

Inflation: The inflation rate of the Vietnamese dong (VND) is 4-7%, which can generally be offset by bank deposit interest rates of 6-7%.

Economic and Geographic Characteristics of Vietnam

Vietnam has seen significant economic growth over the past decade, with an average annual GDP growth rate of 6%, making it one of the fastest-growing economies in Southeast Asia.

The booming economy, combined with its strategic geopolitical positioning, has attracted leading tech companies like Apple, Samsung, and Intel to establish their manufacturing bases in Vietnam. In addition to manufacturing, Vietnam often provides software development services to developed countries and regions.

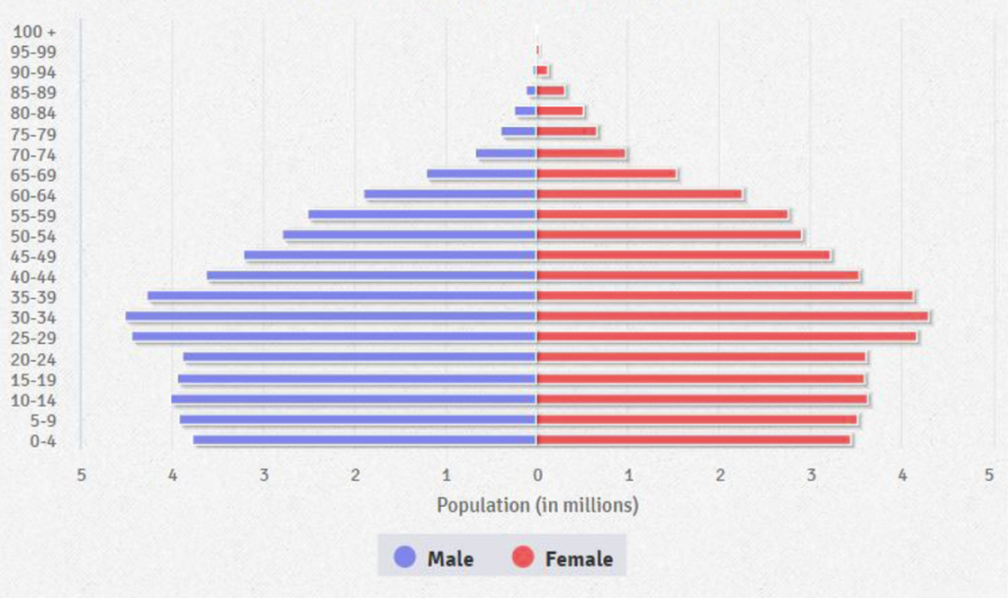

Demographically, Vietnam is one of the youngest countries in the world, with 30% of its population under the age of 25. Young people (aged 10-24) make up 21% of the total population, amounting to 20.4 million people. This demographic window is expected to last until 2039.

Figure: Vietnam is one of the youngest countries in the world, with 30% of its population under the age of 25.

Source: vietnamplus.vn

Vietnam has over 16.6 million crypto holders, making it the second Southeast Asian country with the most crypto investors. About 31% of these investors hold Bitcoin, accounting for approximately 17% of Vietnam's total population. The motivation for holding crypto is primarily speculative, leading to a significant number of local crypto trader KOLs.

Vietnam has around 200 active blockchain projects, mainly in the DeFi, NFT, infrastructure, and GameFi sectors. Notable projects include Axie Infinity, Kyber Network, and Coin98.

In terms of the regulatory environment, in 2020, the State Bank of Vietnam announced that it would not accept cryptocurrencies as legal tender or payment methods. Crypto payments remain in a gray area.

Local Payments

MoMo (digital wallet) is the most popular e-wallet in Vietnam, with 20 million users, leading the mobile wallet sector, followed by Mocan and Zalo Pay.

In Vietnam, credit cards remain the primary online payment method, accounting for 31% of the market share.

5. Switzerland - Zug, as an experimental ground for Crypto Valley

Switzerland is known as Crypto Valley, primarily due to historical reasons, with the Ethereum Foundation registered in Switzerland. Zug is also a pilot city for crypto payments. However, wealthy regions like Zug, with low taxes, do not require crypto as a supplement to financial infrastructure; establishing crypto payment special zones is more experimental in nature.

Additionally, in the 2021 Economist Democracy Index, Switzerland ranked 9th, making it a suitable region for DAO practices.

Summary: The Polarization of Crypto—Speculative Target in Developed Regions vs. Financial Liberator in Emerging Regions

In regions where fiat currencies are weak and mainstream currencies (dollars, euros) are hard to obtain (due to foreign exchange controls and insufficient liquidity), Crypto finds fertile ground, providing local residents with tools for value storage and financial freedom.

Among the four countries and regions mentioned above, Argentina has the best soil for crypto payments:

- Turkey has a developed banking system and a relatively high degree of financial freedom, but the crypto payment ban looms overhead, making it unsuitable for developing crypto payments; Vietnam has a good crypto ecosystem, but the motivation for holding crypto is largely speculative;

- Africa lacks financial infrastructure, making it difficult to open bank accounts, and the currency is weak, leading to a strong demand for stable currencies and cross-border remittances. However, the lack of infrastructure and regulatory issues have caused many crypto wallet projects to fail;

- Wealthy regions like Zug in Switzerland do not require crypto as a supplement to financial infrastructure, and establishing crypto payment special zones is more experimental.

Moreover, Crypto, along with fintech products like Papara and mobile money, can help users obtain financial accounts without barriers.

According to World Bank data from 2021, 1.4 billion unbanked adults cite lack of money, distance to the nearest financial institution, and insufficient documentation as the main reasons for not having accounts. This can be addressed through some technical solutions and financial regulatory policies, referencing the technological experience of mobile money popularized in Africa; it can also be achieved by directly using unlicensed crypto accounts to increase the account penetration rate among the population.

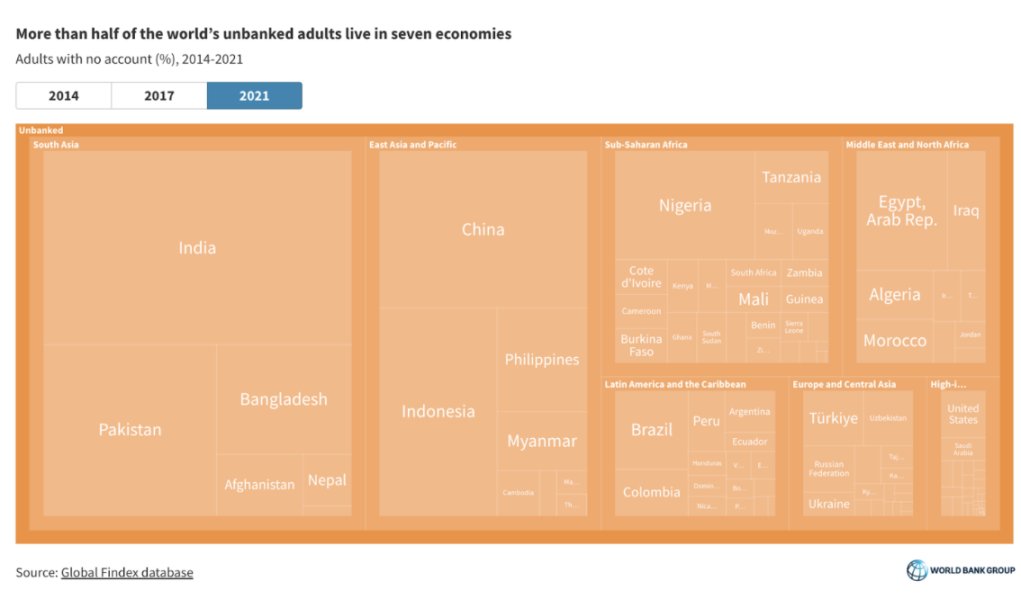

Figure: Proportion of unbanked populations in various countries in 2021.

Source: The Global Findex Database 2021

As two friends from Africa and Argentina said,

Living in China, the US, Japan, and Korea, you don't really need Crypto. They hold crypto to speculate. People in Africa and Argentina need Crypto to live their daily lives. People don't care about self-custodial, they don't give you a shxx. People care about how to transfer money across borders easily.

Crypto presents two faces in different regions: it is a speculative target in developed areas and a financial liberator in emerging regions. For residents living in regions like China, the US, Japan, and Korea, Crypto is not a necessity and is more often used for speculation and narrative. However, residents in Africa and Argentina genuinely need Crypto to improve their daily lives, which has nothing to do with narrative.

Risk warning Risk warning

Risk warning Risk warning