Tightening regulations and ambitious aspirations: Can Estonia continue to attract investors?

Author: TaxDAO

1 Introduction

Estonia is located in northeastern Europe, facing Finland across the Gulf of Finland to the north, bordering Russia to the east, and Latvia to the south. Since gaining independence in 1991, the Estonian government has repeatedly promoted digital reforms, viewing the digital revolution as a vital source for attracting foreign investment and establishing international relations. In 2008, the government announced the birth of "e-Estonia," aimed at digitizing all activities related to citizens and the government. In 2014, the government launched the e-Residency program, allowing anyone from anywhere in the world to establish a company in Estonia. Over the past decade, with the government's strong emphasis on information technology, Estonia's e-commerce and digital finance have rapidly developed, transforming from one of the poorest countries in the Eurozone to one of the fastest-growing economies, and it has been hailed as "the most advanced business center on the European continent." Since 2017, more than 2,000 companies have obtained cryptocurrency licenses in Estonia. The accumulation of technological strength, the government's open attitude, and convenient and stable facilities have a strong appeal for the cryptocurrency industry. However, Estonia also faces challenges such as a fiercely competitive business environment and an incomplete legal framework. Therefore, it is necessary to further clarify Estonia's cryptocurrency taxation and regulatory policies, optimize investment strategies, ensure compliance, and mitigate investment risks.

2 Analysis of Estonia's General Tax System

2.1 Major Direct Taxes in Estonia

Direct taxes, namely income tax, are levied on various incomes of taxpayers. For personal taxes, the taxable subjects are residents whose permanent or primary residence is in Estonia or who have lived in Estonia for more than 183 days in a continuous 12-month period. Resident individuals are required to pay tax on all income earned both within and outside Estonia during the tax period, including employment income, business income, rental income, royalties, interest, taxable scholarships and grants, and capital gains from property transfers. Non-resident individuals are liable for tax on income derived entirely from Estonia, with tax rates influenced by bilateral tax treaties. Generally, the personal income tax rate in Estonia is 20%, with a basic exemption amount of up to 654 euros per month and 7,848 euros per year. If an individual is receiving a pension or has reached pensionable age, the basic exemption amount is 704 euros per month and 8,448 euros per year. Individuals with annual income exceeding 25,200 euros are not entitled to the basic exemption amount. Regarding land tax, landowners are obligated to pay land tax, with rates ranging from 0.1% to 2.5% of the taxable value of the land per year, with a maximum rate of 2% for arable land and natural grassland. Taxpayers with residential properties in urban areas are exempt from land tax if their housing occupies less than 0.15 hectares; any excess area is subject to taxation. Additionally, Estonia does not levy gift tax or inheritance tax.

In terms of corporate tax, Estonia has a low tax rate. All undistributed corporate profits are exempt from tax. This exemption covers both active (e.g., trading) and passive (e.g., dividends, interest, royalties) types of income, as well as capital gains from the sale of all types of assets (including stocks, securities, and real estate). Corporate income tax is levied on profits when distributed as dividends or deemed distributed, generally at a rate of 20% on the net amount distributed. Since 2018, companies that regularly distribute profits can benefit from a lower corporate income tax rate of 14%. If the recipient of dividends is an individual, a withholding tax rate of 7% applies, unless a lower withholding tax rate is stipulated by a tax treaty. According to tax law, profits from the global income distribution of Estonian companies are taxed, not just profits sourced from Estonia. Other income obtained from Estonia may require assessment to determine the amount of withholding tax or corporate income tax owed. Additionally, companies registered in Estonia and foreign entities with a permanent establishment are required to pay a social tax of 33% on total employee wages, of which 20% is for pensions and 13% is for health insurance. Individuals operating as entrepreneurs are also required to pay social tax. There is no cap on the social tax paid by companies, which primarily applies to wages, director fees, service fees, and additional benefits provided to individuals. If employees participate in a mandatory pension accumulation plan, the employer's wage withholding tax includes a 2% contribution.

2.2 Major Indirect Taxes in Estonia

The value-added tax (VAT) rate in Estonia is 20%, applicable to most transactions of goods and services. According to EU regulations, certain specific goods and services, such as financial services, telecommunications services, electronic services, and cultural entertainment services, may be subject to a lower VAT rate. A reduced tax rate of 9% is applied to books, journals, hotel accommodation services, and listed pharmaceuticals. Real estate transactions, healthcare, insurance, and financial and securities transactions may be exempt from VAT. If the taxable amount of a taxable Estonian or non-Estonian enterprise's permanent establishment exceeds 40,000 euros, VAT registration is required.

Regarding customs duties, as an EU member, Estonia applies the Community Customs Code and related implementing regulations: trade between Estonia and other EU member states is exempt from customs duties, while products imported from non-EU member states are subject to EU customs duties, and numerous free trade agreements between the EU and non-EU member states apply to Estonia.

In terms of excise taxes, excise duties are levied on tobacco, alcohol, electricity, certain packaging materials, and automotive fuels. In 2023, the parliament passed a bill announcing an annual increase of 5% in excise taxes on alcoholic beverages, cigarettes, and tobacco from 2024 to 2026, while eliminating the excise tax on special diesel. Property tax is exempted for the value of buildings, but property transfers are subject to local taxes and notary fees.

3 Analysis of Estonia's Cryptocurrency Regulation

Estonia has been early in paying attention to the application and development of cryptocurrency and blockchain technology. In December 2009, Estonia passed the Payment Institutions and E-money Institutions Act, aimed at establishing a clear regulatory framework to regulate the behavior of payment service and electronic money service providers. The act states that an electronic money institution is an entity that issues and provides electronic money services such as electronic wallets and prepaid cards. Electronic money is a monetary value stored on electronic media, representing a monetary claim against the issuer, issued at face value in monetary amounts, and accepted as a means of payment by at least one non-identical electronic money issuer. According to the act, companies providing payment services and electronic money services must register and obtain a license from the Estonian Financial Supervision Authority (EFSA).

With the development of the cryptocurrency industry, the taxation of cryptocurrency has become increasingly prominent. In 2014, the Estonian government announced that cryptocurrencies would be treated as property, subject to property taxation, and further classified them for tax purposes: profits from cryptocurrency transactions are subject to income tax, with profits calculated based on the difference between the sale price and purchase price, or in the case of exchanges, the difference between the price of the received property and the purchase price of the cryptocurrency. Each transfer transaction is treated as a separate taxable object that must be reported. Only in cases where securities are transferred under the terms and conditions stipulated in Article 39 of the Income Tax Act can loss-making transfer transactions be included in the tax consideration. In the same year, the Estonian Tax and Customs Board issued guidelines on cryptocurrencies, clarifying that cryptocurrencies like Bitcoin are not legal tender.

In 2015, based on a ruling by the European Court, Estonia announced that transactions involving non-traditional currencies should still be regarded as financial transactions, provided that the parties involved accept cryptocurrencies as substitutes for legal tender, and declared that exchanges between non-traditional and traditional currencies are exempt from VAT. However, paid wallet services provided are subject to VAT. If the paid wallet service can not only store cryptocurrencies regarded as means of payment but also trade with the mentioned cryptocurrencies, thereby generating rights and obligations related to that means of payment, it can enjoy the VAT exemption for financial services. Mining cryptocurrencies as a service provided to others can also enjoy VAT exemption. Taxable income obtained from cryptocurrency, such as rent, interest, and business income, is subject to income tax. Mining income is also considered business income.

In 2016, the Estonian government amended the Payment Institutions and E-money Institutions Act, requiring service providers to comply with anti-money laundering and anti-terrorism financing regulations and to strengthen international tax cooperation with other countries to combat tax evasion. The act stipulates that payment institutions and electronic money institutions must identify customers and take measures to protect customer funds and privacy. Additionally, institutions must establish a customer compensation system to address potential payment risks. Both payment institutions and electronic money institutions are required to report their business activities to the EFSA and retain customer identity information, transaction records, and other relevant information for at least five years to prevent money laundering and terrorist financing.

In 2017, Estonia improved its regulatory legislation, becoming the first country to issue cryptocurrency licenses, with hundreds of companies obtaining Estonian licenses and conducting related businesses. Estonia defines virtual assets as digital values that can be traded, stored, and transferred, accepted by individuals and legal entities as means of payment, but not as legal tender of any country; cryptocurrencies and their derivatives fall under this definition. The licensing system distinguishes between two types of services: the first type includes providing cryptocurrency wallets and custody services, including generating and storing encrypted customer keys; the second type includes cryptocurrency exchanges providing services for exchanging cryptocurrencies with legal tender. After the implementation of the licensing system, Estonia issued over 4,000 licenses, but there were also cases of shell companies conducting business and using the e-residency program to apply for licenses remotely. The 2018 Danske Bank money laundering scandal and allegations of up to $200 billion in suspicious fund flows prompted the government to reassess cryptocurrency regulation.

In 2020, the regulatory authority for cryptocurrency shifted from the Ministry of the Interior to the Ministry of Finance, with the Financial Intelligence Unit responsible for formulating cryptocurrency regulatory rules. After an in-depth investigation of cryptocurrency companies holding Estonian licenses, the Financial Intelligence Unit pointed out that large amounts of illegal funds were being transferred through blockchain and the shell companies behind it. Although these companies were registered in Estonia, they had no offices in the country. In subsequent actions, Estonia revoked most licenses, retaining only over 300. On June 14, 2021, Mátis Mäeker was appointed as the head of the Financial Intelligence Unit, stating that "the main task of the Financial Intelligence Unit in the coming years will be to establish a function for strategic analysis of money laundering and terrorist financing" and to promote the reduction of anonymity in cryptocurrency transactions to ensure transparency and more effective monitoring of the business environment. Subsequently, relevant regulatory policies were strengthened: providing cryptocurrency exchange services requires user identity verification, and personal data must be communicated with transactions in the same manner as bank transfers; if the recipient's wallet does not have a service provider or cannot receive data, real-time transaction monitoring and risk analysis must be ensured for each transaction; if a company holding a cryptocurrency license is found to have business unrelated to Estonia, measures may be taken to refuse to issue or revoke the license.

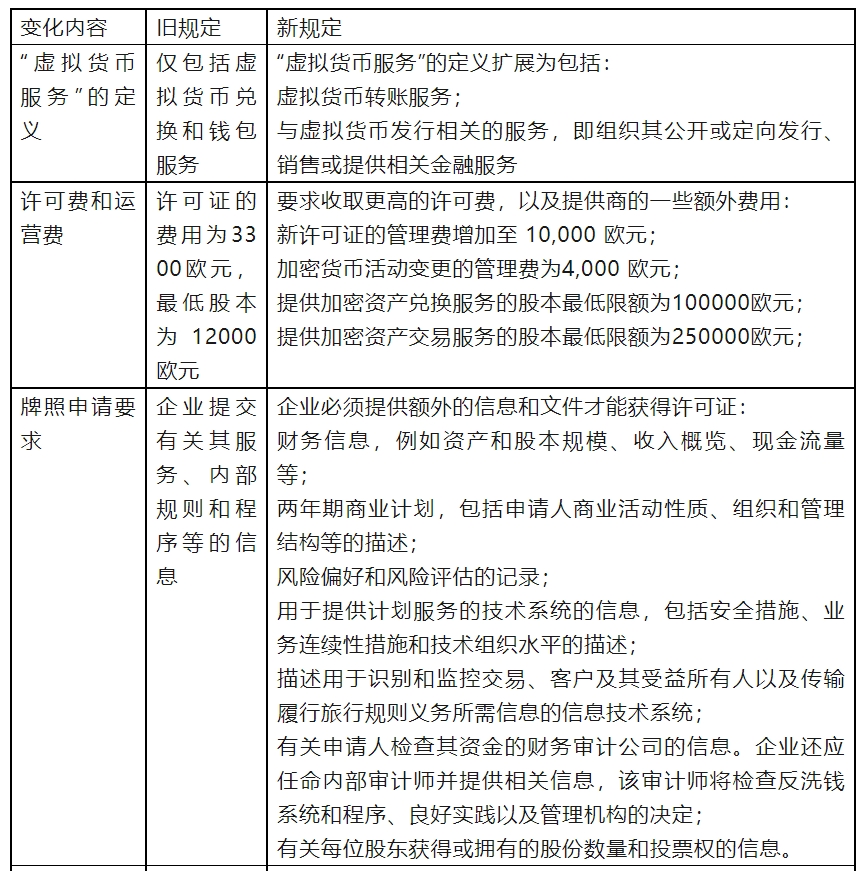

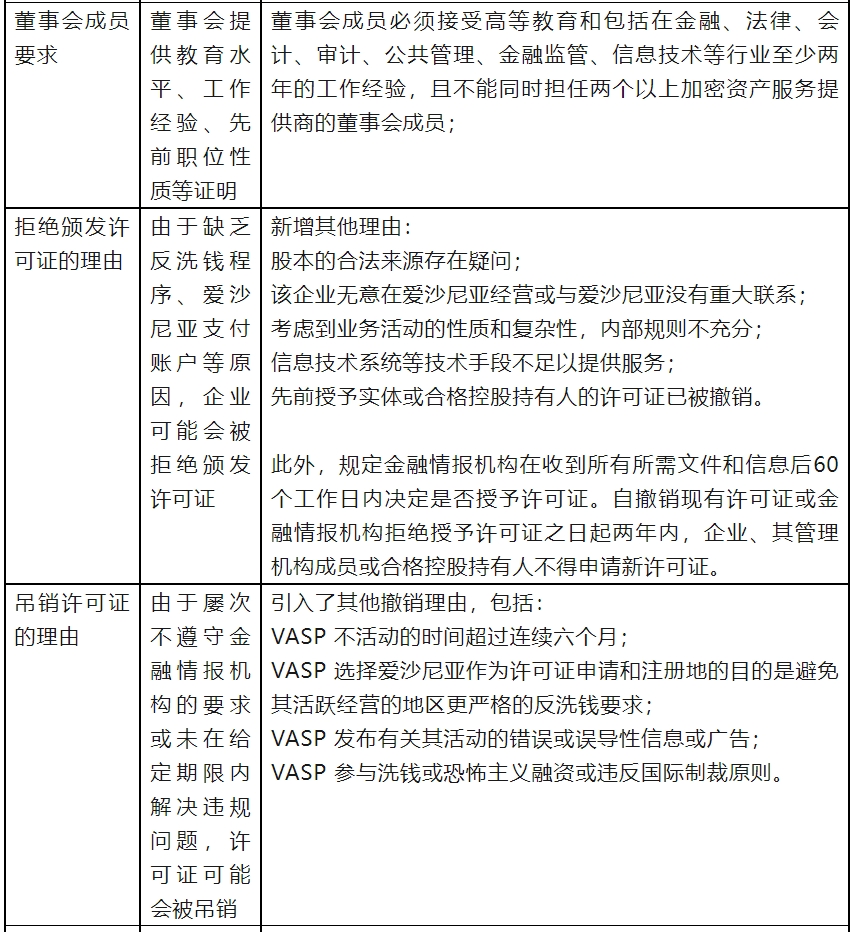

In 2022, Estonia passed the Money Laundering and Terrorist Financing Prevention Act, setting stricter requirements for companies applying for Estonian cryptocurrency licenses, including the following:

Despite the Estonian government's continuous refinement and tightening of cryptocurrency regulatory policies, Estonia attracts many investors in the cryptocurrency industry due to favorable conditions such as the exemption of undistributed corporate profits from tax, no annual licensing fees, economic stability, a friendly business environment, the availability of cryptocurrency accounting declarations, and a large number of issuances. In the future, Estonia's regulatory policies for the cryptocurrency industry may tighten further, but it maintains an open and inclusive attitude towards the development of legitimate and compliant cryptocurrency enterprises, striving to achieve the normalization and sustainability of the cryptocurrency industry's development to solidify Estonia's leading position in the global cryptocurrency industry.

References:

[1] Estonian Parliament. (1999). Income Tax Act

[2] Estonian Parliament. (2000). Social Tax Act

[3] Estonian Parliament. (2017). Customs Act

[4] Estonian Parliament. (2002). Taxation Act

[5] Estonian Parliament. (2009). Payment Institutions and E-money Institutions Act

[6] Estonian Parliament. (2022). Money Laundering and Terrorist Financing Prevention Act

[7] Pascale Davies. (2022). Estonia used to be a crypto pioneer but is now clamping down on crypto licenses. This is why?