Inventory of the three major trends in the LSD project: decentralization, enhanced DeFi, and full-chain integration

What are the new trends and玩法 in the LSD field? Where is the LSD track headed? What kind of projects will gain a greater advantage in the competition? What is the ultimate outcome of the LSD track?

What are the new trends and玩法 in the LSD field? Where is the LSD track headed? What kind of projects will gain a greater advantage in the competition? What is the ultimate outcome of the LSD track?Author: 0xmiddle

It has been half a year since the upgrade in Shanghai, and the LSD War is still heating up. Due to the massive market capitalization of hundreds of billions, LSD has always been a fiercely competitive field. Established players like Lido and Rocket Pool are constantly at odds, while new players like Puffer and Stader have joined the table. What new trends and gameplay are emerging in the LSD space? Where is the LSD track headed? What kind of projects will gain greater advantages in the competition? What is the endgame for the LSD track?

Decentralization: A Banner of Political Correctness

In July this year, Lido launched an attack on Rocket Pool, pointing out that its contracts have sudo permissions, allowing the team to make arbitrary modifications to key parameters, accusing Rocket Pool of being insufficiently decentralized. Then, in August, Rocket Pool, along with five other Ethereum LSD protocols like StakeWise, initiated a proposal in the name of maintaining Ethereum's decentralization, limiting the staking share of each LSD protocol to below 22%. This initiative was aimed squarely at the industry leader Lido, as only Lido's staking share exceeded 22%.

Lido did not respond formally, but its community supporters countered that Lido should not be seen as a single entity, but rather as a coordinating layer.

Decentralization has always been one of the main narrative points for all DeFi protocols, including LSD protocols. In the crypto space, "decentralization" is a politically correct banner; whoever can prove themselves to be more decentralized than their competitors can argue their case more convincingly. This "atmosphere" has indeed promoted efforts towards decentralization among protocols.

In fact, Rocket Pool was one of the first protocols to implement a permissionless mechanism at the node level, while Lido has implemented the Staking Router mechanism and a dual voting system in its V2 version. Both have made certain achievements in terms of decentralization and are still working on it.

The decentralization of LSD protocols includes four levels:

First, the decentralization at the node level, referring to technologies like DVT/SSV, which allow multiple people to control a node;

Second, the decentralization of protocol node selection, whether the protocol allows free access for nodes? How many nodes can it cover? What is their geographical distribution?

Third, the decentralization of protocol governance. Who decides the protocol's changes and upgrades? Who chooses the nodes? Do protocol developers have super permissions?

Fourth, the diversification of LSD protocols. For a public chain, if the majority of tokens are staked in one protocol, it is indeed not a good thing. Lido cannot simply be understood as a coordinating layer.

In the struggle between Lido and Rocket Pool, the author does not take sides but feels that this competition, this mutual "supervision," is actually promoting everyone to move towards decentralization. The four levels of decentralization are all beneficial.

DeFi Enhancement: The Goal is to Maximize Yield

The base yield carried by LSD assets depends on the staking rewards defined by the underlying blockchain and the distribution method defined by the LSD protocol (the distribution ratio among validators, protocols, and users). In this regard, most LSD protocols are quite similar; some protocols adopt various methods to provide subsidies (like Frax Finance) to increase the base yield, but this is certainly unsustainable. From the user's perspective, what is more important than the base yield is the "stacked yield." The so-called stacked yield refers to the greater yield that can be obtained through certain DeFi combination strategies while controlling risk.

Currently, the most commonly adopted strategy is circular staking through lending protocols. For example, staking ETH in Lido to obtain stETH, then using stETH as collateral in Aave or Compound to borrow ETH, and then returning to Lido to stake again. This operation can be repeated many times until the borrowing rate equals the yield from LSD. Through circular staking, the stacked yield can far exceed the base yield. Essentially, this is a form of interest arbitrage and leveraging behavior. The risk of this operation lies in the fact that as the number of cycles increases, the liquidation risk will be amplified.

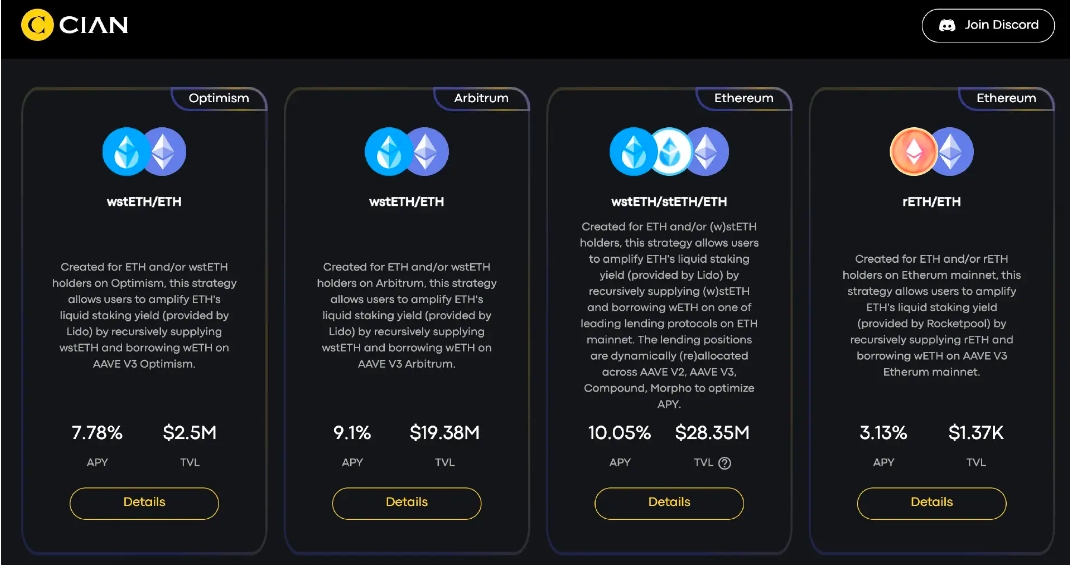

Some protocols provide yield maximization strategy management tools for LSD asset holders (even allowing management of the leverage rate of circular staking). LSD holders can complete circular staking with one click through these protocols without having to do it manually. Notable examples include DeFiSaver, Cian, and Flashstake, which all offer diversified DeFi enhancement strategies for LSD and leverage rate management tools.

Cian App Screenshot

In addition to circular lending, users can also use LSD assets for other yield-generating activities. For example, providing liquidity in DEXs or earning yield in index-type protocols or yield aggregation protocols. Here, readers can refer to the article “LSD Hides 'Sevenfold Yield,' The Endgame of APR-War is a 10X Growth in TVL”

These protocols based on LSD assets are sometimes referred to as LSDFi protocols. In the future, LSDFi protocols and LSD protocols will intertwine and merge. Some LSD protocols will launch their own LSDFi or integrate other LSDFi protocols to provide combined yield strategies for users on their interfaces. Conversely, LSDFi protocols will also integrate LSD protocols, allowing users to execute yield strategies with base assets like ETH with one click.

For LSD protocols, the LSD War should not be viewed merely as an APR War at the level of base yield; rather, they should strive to promote their LSD assets to be listed in more LSDFi protocols, enabling them to be combined for better stacked yields to meet the needs of yield maximizers.

Multi-chain: From Multi-chain Deployment to Full-chain Architecture

When discussing LSD, we often implicitly refer to ETH LSD, as Ethereum's massive market capitalization and its PoS transition have spurred the explosion of LSD. However, LSD is an old track. Earlier PoS consensus public chains had LSD long ago, although it was then referred to as "staking derivatives."

In fact, early emerging LSD protocols supported more than one chain, and even newer LSD protocols are continuously expanding towards multi-chain to broaden their territory.

Lido now supports not only Ethereum but also Solana and Polygon, allowing users to mint stSOL on Solana or stMatic on Polygon through Lido.

Stader supports seven chains, including: Ethereum, Polygon, Hedera, BNB Chain, Fantom, Near, and Terra 2.0.

Ankr supports seven chains, including Ethereum, Polygon, BNB Chain, Fantom, Avalanche, Polkadot, and Gnosis Chain.

StaFi, which emerged from the Cosmos ecosystem, supports nine chains: Ethereum, Polygon, BNB Chain, Solana, Atom, HUAHUA, IRIS, Polkadot, and Kusama.

Bifrost, which emerged from the Polkadot ecosystem, supports six chains: Ethereum, Polkadot, Kusama, Filecoin, Moonbeam, and Moonriver.

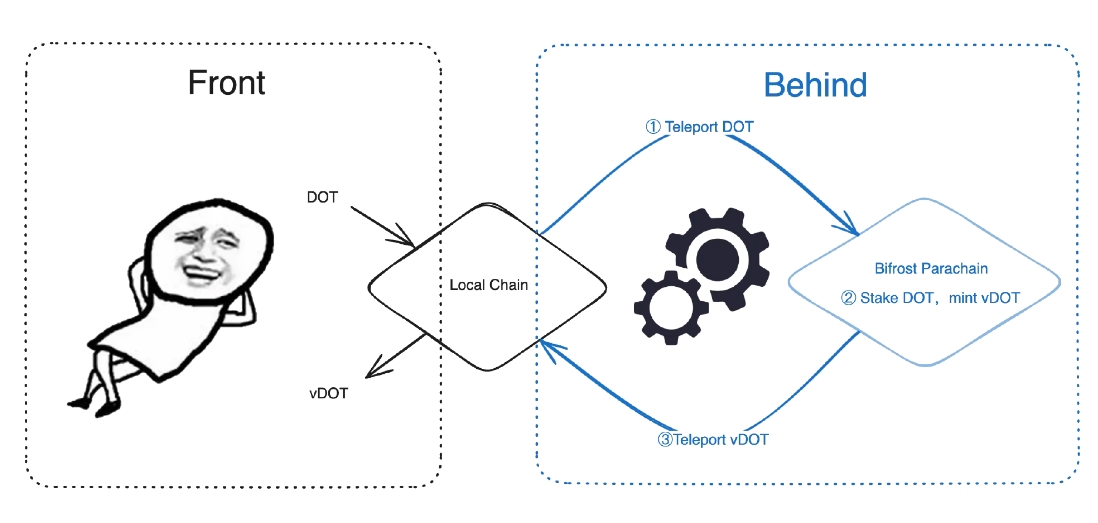

Here, Bifrost's multi-chain strategy is somewhat unique and differs from other LSD protocols. Bifrost does not redeploy the Bifrost protocol across multiple chains but adopts a brand-new architecture.

Bifrost has its own chain called Bifrost Parachain, which is a parallel chain of Polkadot. Bifrost only deploys the main protocol on Bifrost Parachain and then deploys a lightweight module on other chains to support remote access. The LSD minted by the Bifrost protocol is called vToken. When users mint vToken on other chains, they access the main protocol of Bifrost Parachain through the remote module, and after the main protocol mints the vToken, it is sent back across chains to the user's chain.

What users experience is the completion of LSD minting locally, while the underlying process involves cross-chain transmission back and forth. According to Bifrost's article “Analyzing the New Paradigm of Full-chain Applications with Bifrost as an Example,” Bifrost is designed this way mainly for the following two reasons:

The global state of vTokens minted for all chains is on Bifrost Parachain, rather than being fragmented across different chains. The unification of data brings better cross-chain integrability. Any dApp on any chain can integrate with the corresponding remote module to access all chains' vTokens without needing to integrate different chains' vTokens one by one. Users can also mint any vToken on any chain, such as minting vDOT on Ethereum;

The liquidity of all vTokens is entirely on Bifrost Parachain, so Bifrost does not need to guide liquidity across different chains. Users on other chains who want to exchange vTokens do so by accessing the liquidity pool on Bifrost Parachain through remote access. This avoids the problem of insufficient depth caused by fragmented liquidity. If lending dApps on other chains integrate vTokens, they can also complete liquidation by accessing the unified liquidity pool on Bifrost Parachain, resulting in lower slippage during liquidation due to the absence of fragmented liquidity.

Bifrost refers to this architecture as "full-chain architecture." Under this architecture, dApps are only deployed on one chain without multi-chain deployment, while users and applications on other chains access the dApp through remote access, but the experience is consistent with using local chain applications. Bifrost believes this architecture has better cross-chain composability and the advantage of unified liquidity.

The author believes that Bifrost's "full-chain architecture" is undoubtedly the correct answer for multi-chain applications and may represent a more universal application form in the future. This architecture reflects a new way of thinking about application construction, treating multi-chain interoperability as a premise and designing the parts of dApps across different chains as a whole, rather than simply replicating single-chain applications to run on multiple chains.

With the excellent cross-chain composability of the "full-chain architecture," Bifrost can implement more complex, multi-chain DeFi yield strategies for vTokens. At this point, do readers sense a hint of "Intent-Centric"?

However, this architecture places high demands on cross-chain bridge infrastructure, requiring a sufficiently secure and high-performance cross-chain protocol layer to support high-frequency cross-chain interoperability.

Conclusion

Driven by the cultural impetus for "decentralization" in the crypto world, LSD protocols will continue to evolve towards decentralization to gain narrative points and positive impressions;

Users' use of LSD protocols will not be limited to obtaining basic Staking Rewards but will also involve formulating DeFi combination strategies through various means like circular lending to achieve higher yields.

At this point, the competition among LSD protocols has also shifted to a competition of composability and stacked yields; to expand their business scope, LSD protocols tend to deploy across multiple chains, but there are also approaches like "full-chain architecture" that can achieve "single-chain deployment, multi-chain access," which has better cross-chain composability and the advantage of unified liquidity, representing the future paradigm of multi-chain applications.

The competition and innovation in the LSD field are still intensifying. Currently, although the top five LSD protocols account for over 80% of the LSD market, with Lido alone holding over 70% of the ETH LSD share, seemingly unshakeable, the winds of change are brewing. Users' faith in decentralization, their pursuit of stacked yields, and their expectations for a unified multi-chain experience will undoubtedly reshape the landscape of LSD.

Risk warning Risk warning

Risk warning Risk warning