Metrics Ventures: The dish is ready, and the chip structure of BTC has entered a bull market preparation state

The Bitcoin market has established the prerequisites for starting a bull market, with a high proportion of long-term holders and a healthy chip structure.

The Bitcoin market has established the prerequisites for starting a bull market, with a high proportion of long-term holders and a healthy chip structure.Author: Metrics Ventures

October Market Observation Guide from Metrics Ventures, a Secondary Fund in the Crypto Market:

1. Bitcoin Market Has Conditions for Bull Market Start. The Bitcoin market has met the prerequisites for initiating a bull market, with a high proportion of long-term holders and a healthy chip structure.

However, it should be noted that we still judge that there will not be a so-called bull market that happens all at once. This round of market movement is mainly driven by leveraged funds, but a true bull market still awaits new capital to enter. Overheating will inevitably lead to adjustments. Once the leverage is cleared and the holding costs fall back to the moving average, it will still be a very good opportunity to increase positions.

The macro environment is favorable for the crypto market. The trends of the US dollar index, unemployment rate, and US Treasury yields indicate that the macro environment will be more favorable for the crypto market. At this moment, finding potential emerging market targets and observing the path and speed of incremental capital entering the market will be the focus of our research going forward.

This article is a summary and commentary by MVC on the overall market situation and trends of the crypto asset market in October.

A false rumor triggered a real surge, causing Bitcoin to break through the bull-bear dividing line.

Things started to go awry on October 17th. After the false news about the ETF was debunked and deleted, Bitcoin's price surprisingly stabilized and did not drop.

According to common logic, the rise caused by false news should be completely wiped out after the rumor is debunked, influenced by both selling pressure from trapped positions and stop-loss selling from those chasing the rise. However, Bitcoin's price remained stable for the next three days, indicating that some market funds ignored the ETF news and began to enter the market firmly.

For the long-term trend of Bitcoin, we generally refer to the weekly MA120 (120-week moving average) as the bull-bear dividing line. When Bitcoin completes its decline from the previous bear market cycle and the first rise exceeds the weekly MA120, it can be seen as the end of the bear market cycle. Similar time points can be referenced in December 2015, April 2019, and April 2020. Each time Bitcoin's price broke through the WMA120, there was a considerable trend, which can even be seen as the starting point of a new bull market cycle.

The logic behind the bull-bear dividing line is still based on the distribution of Bitcoin's chips. In our October monthly report, we repeatedly emphasized that the necessary condition for the start of a new bull market cycle is that the investment costs of long-term and short-term holders in the market must be leveled. This way, once the bull market starts, there will be no historical trapped positions' selling pressure, only profit-taking selling pressure, which can be absorbed by new capital.

The significance of the WMA120 in terms of chips is that it can be roughly regarded as the comprehensive cost of long-term holders. Currently, the price of WMA120 is around $32,000, while the market price at the time of writing this article is about $33,700. We believe that the current chip structure of Bitcoin has met the prerequisites for starting a bull market, which is also the meaning behind this month's report title, "The dish is ready, just waiting to be served."

From Glassnode's data, we can see that currently, the proportion of long-term holders holding Bitcoin for more than 155 days is as high as 76%+, with long-term chips locked in stably. Meanwhile, the cost range for short-term holders holding for less than 155 days is mainly around $29,000-$30,000, with the profit ratio exceeding 86%.

Although this data is constantly changing, the chip structure of the Bitcoin market has already indicated the current chip pattern: a high proportion of long-term investors holding positions, a firm willingness to hold, with the main cost range around the WMA120 at $32,000, currently mostly in profit (Microstrategy's weighted cost is also in profit, which is not easy), while the short-term investors have a small proportion of floating chips, with the main cost below $30,000, currently also mostly in profit. The current chip structure indicates that the long bear market's forced selling and turnover cycle can be declared over, and the market chips have completed the transition between forced selling and building positions. The subsequent market height will largely depend on the willingness and speed of new capital entering the market. The new crypto cycle in 2025-2026 can consider this month as the starting point.

The chip structure of ETH is not as healthy as that of BTC. The cost for short to medium-term investors in ETH is around $1,770, while the current market price is $1,788, just in profit. The concentrated cost area for long-term investors in ETH is around $2,200, and currently, long-term holders of ETH are still in the trapped range, which still imposes significant selling pressure. This is also the fundamental reason why the ETH/BTC exchange rate is still in the process of bottoming out.

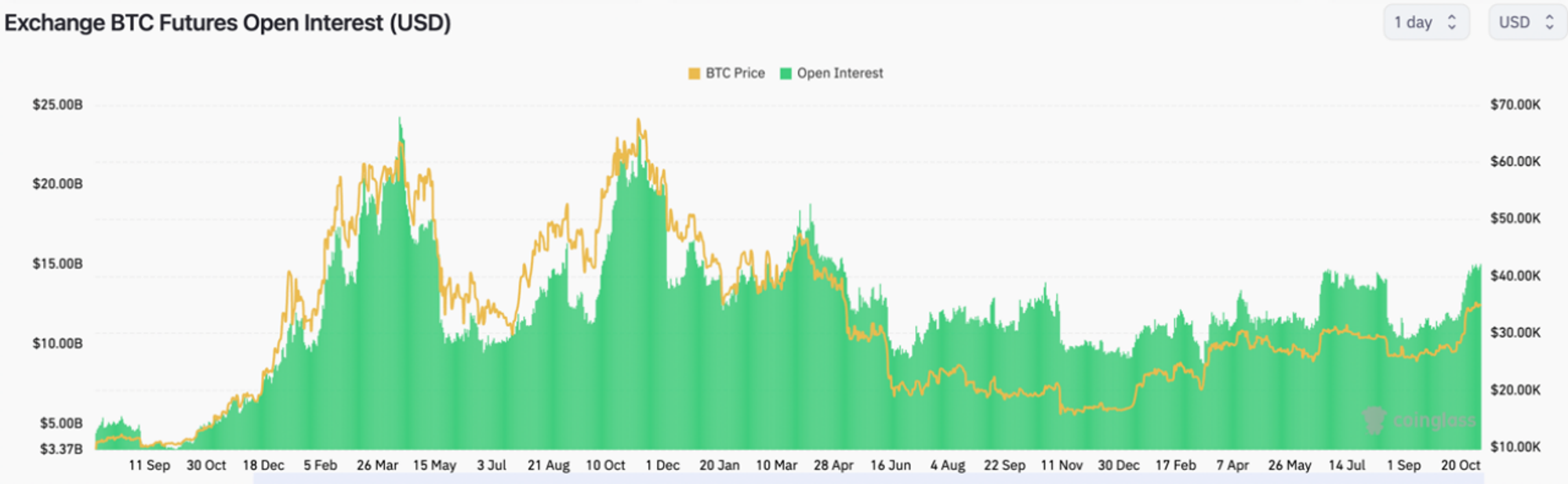

Many people feel that the speed of the market this time is too fast. In fact, this round of market movement is still a very rapid leveraged fund market and a rebound from oversold conditions. From Coinglass's data on the overall BTC contract positions, we can see that even on October 16, the day of the false news surge, the total number of BTC open contracts was still at a very low level of around 11.67B, with a relatively high short-to-long ratio and a slightly negative funding rate, indicating that the low positions were mainly short positions.

However, once the BTC price stabilized above $30,000, leveraged funds surged, and within just two days, the total number of BTC open contracts and remaining positions broke through the annual high, reaching a level of 14.97B. The funding rate also reached its annual peak, with extremely high enthusiasm for going long.

Interestingly, as of the date of writing this article, the number of BTC open contracts on Binance is about 3.7B, still not back to the August high of 4.54B. However, the main force of leveraged funds increasing positions, CME, saw its open interest rise from the August high of 2.33B to the recent 3.58B, while BitMex's open interest rose from the August peak of 261M to 300M. The funding rate and premium on Bitmex have also simultaneously reached levels seen in October 2021 when BTC was around $60,000, indicating the enthusiasm of investors from the United States.

In terms of market sentiment, October also saw some intriguing emotional shifts. We still remember that in the first couple of weeks of October, there were suddenly many discussions about "crypto is dead" and "no bull market after halving." When we talked about this with many old friends, we all shared a knowing smile, as it was so reminiscent of the deep bear market at the end of 2019. This was also an emotional indicator that prompted us to decisively start bottom-fishing.

For ETH and Altcoins, ETH's performance is still lagging behind BTC. For Altcoins, this round has a particularly strong flavor of a simple rebound from oversold conditions. The market has not seen any particularly mainstream themes or narratives. Aside from some projects taking the opportunity to announce tokenomics transformations or changes in charging models, the most rebounding assets are still those that had previously fallen significantly, many of which set new lows compared to November 2022. For fund-type capital, these oversold rebound assets seem to have large gains, but in reality, their liquidity remains very thin, and their trading value is low.

Regarding the market that first broke through the WMA120 at the end of a bear market, after the first breakthrough in December 2015, it continued to oscillate for five months before starting a unilateral upward trend. After the first breakthrough in April 2019, it fell below the line twice in December 2019 and April 2020 before starting a unilateral trend.

From the perspective of chip distribution, BTC breaking through the WMA120 marks the completion of the bear market turnover, but there is still a certain time window before the true bull market starts. The significance of this period is to allow the market chips to settle around the WMA120 as the cost center, continuously accumulating and turning over chips, solidifying costs while waiting for new capital to enter.

As for when new capital will come in and for what reasons, it still requires the market to provide innovations at the industry or sector level, making it difficult to find answers from trading alone. The halving time point may serve as a relatively meaningful anchor. If there is still an opportunity for the market to pull back or fall below the WMA120 before the halving arrives, it will still be a highly potential opportunity to increase positions.

If the most frequently asked question at the beginning of October was "Can it still rise?", the most frequently asked question recently has been "Will it still fall?". We believe the market certainly still has opportunities to decline. Compared to the Echo Bubble from January to August 2019, I think the current cycle position is closer to January-February 2020.

The reason for this conclusion is that the period from January to August 2019 is actually quite consistent with the cycle position of January to August 2023, both completing deleveraging and major clean-ups at the lowest point of the bear market, resulting in an Echo Bubble, which is essentially a large short covering. The reason the rebound from January to August 2019 had a very large space is that many institutional investors were in a bear market mindset, densely opening short positions around the $6,000-$7,000 range, providing fuel for the upward trend. Many investors who experienced 2019 should have a deep impression of this; most investors who made money from the rebound at the beginning of the year lost it after June by shorting.

After the emotional release in August 2019, the market entered a four-month correction, which is similar in nature to the period from June to October 2023, both being correction phases after the completion of short covering, representing a natural turnover and accumulation of chips after the market has cleared. However, because the rebound in early 2023 was relatively small, the correction did not appear so severe.

We believe that the current situation resembles the script of January 2020 being played out in advance because, first, we have already gone through the process of short covering and chip turnover, and second, the last shorts in the market have surrendered and closed positions below $33,000, with little willingness and momentum to short. With the halving approaching next year, early capital is starting to act, and institutional investors generally have low positions, leaving room for increasing positions, so the market aligns more with the characteristics of January 2020.

Since we are positioning the market to January-February 2020, many people may subconsciously think whether there will be a "3-12" level disaster occurring next. First, from the chip structure perspective, BTC has entered a new trading range of $32,000-$41,000. According to the current momentum, which has not yet accelerated, there is still a possibility of hitting the $40,000 mark, and ETH also has the momentum to accelerate towards the WMA120, which is around $2,200.

However, we still judge that there will not be a so-called bull market that happens all at once, as the current market movement is still driven by existing funds and leveraged positions, and there is currently no data support for new capital entering the market. Moreover, the number of open contracts is high, and the fear and greed index is in the greed range. The funding rates and contract premiums on Bitmex are at levels seen during the 2021 bull market. The market's phase of overheating will inevitably lead to a cleansing of leverage, and once this round of market movement accelerates, there is still a very high chance we will see a large-scale deleveraging decline. Once the leverage cleaning is completed, we will observe a decrease in open interest and funding rate data, and when the BTC price returns to the long-term cost moving average, it will still be a very good opportunity to increase positions.

As for when this decline will come, we do not want to make predictions lightly. From June to August 2019, the funding rates and contract premiums rose for two consecutive months, with emotions even more overheated than in a bull market. Those who easily tried to call the top and continuously shorted suffered significant losses. Even when the market enters an accelerated top, we will have ample time to think and make decisions.

We believe that starting in November, the chip structure of BTC has entered a state of preparation for a bull market. Before next year's halving, it is expected to continue to be a process of frequent shakeouts, accumulating chips, and solidifying long-term holding costs, while ETH still needs to wait for a breakthrough of the WMA120. Whether it falls or not, whether there will be a crash, and when leverage will be cleaned out are not the core contradictions. The core contradiction is how to buy smartly. At this moment, finding potential emerging market targets and observing the path and speed of incremental capital entering the market will be the focus of our research going forward.

In addition to the endogenous market structure of the crypto market, we have also observed recent favorable news at the macro level, especially regarding capital. Whether it is the unemployment rate above expectations, the tendency to approach the peak of US Treasury yields, or the peak of the US dollar index, all point to a macro environment that is more favorable for the crypto market. However, we believe these are not very important. Many investors were hesitant to bottom-fish in October due to concerns that declines in the equity market would affect the risk appetite for the crypto market. However, the crypto market and the equity market have significantly decoupled. In the coming times, we should look forward to what kind of innovations the builders in the crypto market will present to us, and which of these will become the entry points for new capital, thus opening a new crypto bull market cycle.

The dish is ready, just waiting to be served.

In summary, Bitcoin's breakthrough of the bull-bear dividing line marks the end of the bear market, with both long and short-term holders in profit. Market sentiment has shifted from pessimism to exuberance, with the market primarily driven by leveraged funds, but a true bull market still awaits new capital to enter; the key lies in patiently accumulating leading assets and waiting for incremental capital to sound the horn for a new bull market.