All set, only lacking the east wind: Exploring the possibilities of decentralized options

Decentralized options refer to smart contracts with options attributes issued on the blockchain. Compared to traditional options markets, they are permissionless, publicly transparent, have no default risk, and exhibit stronger composability with other decentralized products.

Decentralized options refer to smart contracts with options attributes issued on the blockchain. Compared to traditional options markets, they are permissionless, publicly transparent, have no default risk, and exhibit stronger composability with other decentralized products.Author: AC Capital Research

Introduction

Options are a type of choice, a rights contract where both parties agree on the delivery conditions and types of deliverables. The emergence of smart contracts allows contracts to be executed automatically in an on-chain environment without human intervention, with clear and transparent execution conditions and processes, creating a favorable environment for the operation of options. Since the DeFi summer of 2020, countless teams and projects have begun to advance towards decentralized options. After three years, the industry's development has shown a flourishing scene, with significant progress in accounting infrastructure, types of options, and market-making algorithms.

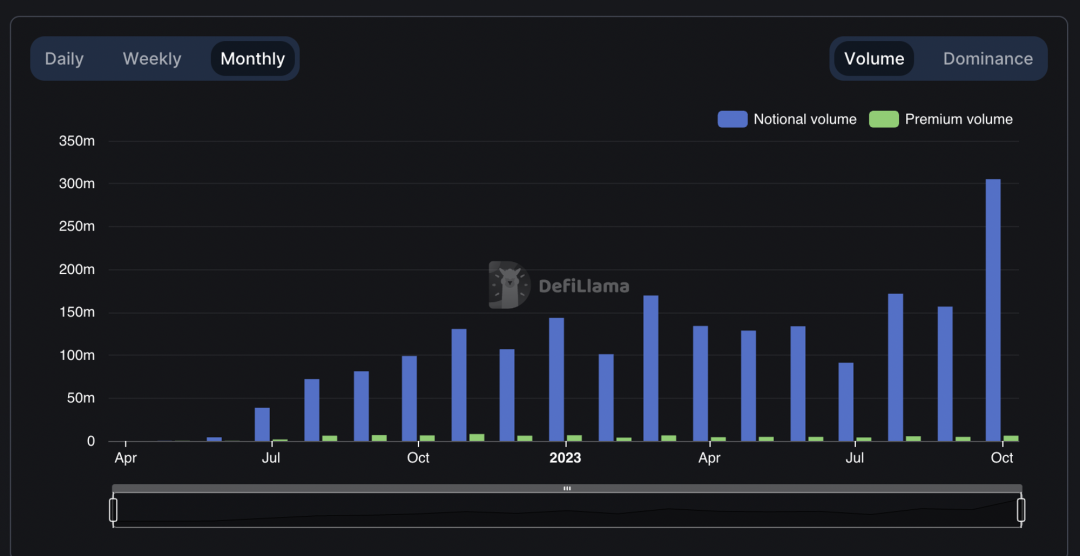

As the market enters a bear phase, the cost of token incentives is rising. The inflated activity of decentralized options has begun to decline. With a few exceptions, innovation has concentrated on micro-innovations in financial products. The market rewards breakthrough innovations that align with blockchain architecture and decentralized environments. Projects like Lyra, which stand on the shoulders of giants, have formed a DeFi matrix, creating a unique algorithmic system for options pricing. Although the market size has shrunk, Aevo and Lyra occupy an absolute leading market share.

In contrast to the hundreds of billions of dollars in off-chain trading volume, the current on-chain options market barely scratches the surface. In traditional markets, the nominal transaction volume of options is roughly on par with futures. From this data, we can infer that the on-chain options market is still in its early stages. In the second half of 2023, the technology of layer 2 networks has gradually matured, and low-cost infrastructure technology for trading book-style options markets has led to a new growth spurt in the on-chain options market.

We have long passed the "decentralization is good" phase of the DeFi summer, and all forms of decentralization will be questioned: WHY!

Background of Decentralized Options

What are Options

To understand decentralized options, we must address two questions: what are options, and why decentralize?

We can simply state that options are a type of choice, where both parties determine the exercise time and price. The holder of the option has the right to execute the contract as agreed.

Options are a special type of financial contract and a financial instrument related to price fluctuations. Analyzing from the nature of options, they reflect not only the price changes of the underlying asset but also the rate of price change, differences in exercise times, and more.

Options are financial instruments related to risk pricing. The changes in option prices can reflect price attributes that spot and futures cannot express, providing investors with more dimensions and tools for hedging risks and designing asset portfolios.

Moreover, options have a wide range of uses. Understanding the uses of options helps us identify the precise users of option products. In the traditional world, options serve many purposes beyond being a leverage tool:

1. Risk Management Tool

Options are a risk management tool that can be discussed from both business and compliance perspectives. Enterprises or projects constantly face price fluctuations in raw materials and products. In addition to using futures to lock in costs in advance, they can also buy options to gain the right to buy or sell at a specified price within a specified time. This is equivalent to locking in the upper and lower limits of expenditures and revenues, ensuring minimum profits. For financial institutions, derivatives are a new phenomenon, with types and complexities exceeding those of stocks and bonds. In navigating regulations, options can often play unexpected roles. In trading, some traders hold large positions and may face high liquidity losses when managing risk and liquidation. Therefore, holding corresponding options during low volatility periods can convert liquidity loss risks into fixed cost expenditures.

2. Financing Tool

In finance, options are also an important financing tool. Without discussing convertible bonds as options + bonds, historically, many companies have financed themselves through the sale of options. In October 2022, Tesla raised $2.2 billion by selling 5 million call options, allowing holders to buy Tesla stock at $1,100 in January 2024.

3. Organizational Incentive Tool

Many traditional large organizations also use options to incentivize mid-to-high-level employees. This practice has become commonplace in the traditional world. There are numerous papers discussing the pros and cons of option incentives.

4. Leverage and Speculation Tool

Many investors use options for speculation, leveraging small capital for large returns, or even betting on trading opportunities based on time cost dimensions or volatility dimensions. This is a function not available in many other financial instruments.

In 2020, with the advent of spot DeFi, decentralized derivatives were mapped from traditional finance. Everyone hoped to share in the profits of centralized financial institutions' options businesses on decentralized platforms. So how do we define decentralized options?

In traditional finance, options have different circulation markets, including both exchange-traded and OTC markets.

What are Decentralized Options

Decentralized options refer to smart contracts with option attributes issued on the blockchain. Compared to traditional options markets, they are permissionless, publicly transparent, and have no default risk, offering stronger combinability with other decentralized products. Unlike traditional options on centralized exchanges or OTC options, the execution of options is guaranteed by blockchain smart contracts, which execute automatically. This is the only difference between decentralized options and traditional options.

Decentralized options projects stem from the mapping of centralized options markets. In traditional financial markets, the derivatives market is far larger than the spot market, with the scale of the options market being roughly equivalent to that of the spot market. The success of decentralized exchanges like Uniswap and Curve has demonstrated the potential of smart contracts in the financial industry. Many teams have seen the future of decentralized futures and even options. Under the halo of the DeFi summer, the drawbacks of decentralization were obscured, and numerous teams invested in the hot construction of decentralized options.

Why Decentralized Options are Important

The advantages of decentralized options over centralized options mainly lie in: 1. Eliminating default risk; 2. Greater fairness; 3. Deeper and closer capital collaboration.

Compared to centralized options, decentralized options have no counterparty risk. Risk is uncertainty. The execution environment, processes, and conditions of on-chain options are open and transparent, with no uncertainty from a clearing perspective. How a contract is cleared and the results are clear at a glance. Without uncertainty in clearing, there is no counterparty risk.

In traditional finance, to prevent wrongdoing, regulatory authorities have established various entry barriers. While this protects users' rights, it inevitably results in some individuals losing the opportunity to participate. Moreover, neither the creators of smart contracts nor participants have privileges; they can only participate under the smart contract, making decentralized options fairer.

Decentralized options are an indispensable part of decentralized finance. Decentralized finance has inclusivity, convenience, and can even reduce regulatory requirements. On one hand, it has the potential to replace centralized options. On the other hand, the decentralized world needs the services of options.

The prosperity of the decentralized options market requires a robust demand for decentralized options underlyings. Currently, on-chain, options are often labeled as gambling tools. A simpler thought is to make options a leverage tool or a volatility underlying, while a more complex approach is to integrate them into certain investment strategies, forming structured investment products.

The Market for Decentralized Options

New and traditional entities differ on many levels. Unlike traditional finance, whether from the underlying assets to users or channels, decentralized options have differences that allow for differentiated competition with traditional markets.

Decentralized finance is always pure on-chain data operations. The best underlyings are, of course, assets on the original chain. If there is a need to handle off-chain assets, it inevitably requires interaction with centralized powers and organizations. This falls under RWA (Real World Assets) business, constrained by compliance, and cannot avoid the drawbacks of centralization.

In addition, the users of options are also different.

First, traditional options users are very clear, while the target users of the decentralized options market are vague. In traditional businesses, industrial capital participates in the options market. Similar to the futures market, industrial capital is an important player in the traditional futures and options market. They even have a certain degree of decision-making power over the prices of underlying assets. The financial market is a bilateral market for trading risk and returns, with industrial capital responsible for providing risk and risk capital. In the decentralized options market, the underlying asset-related business is simple and the volume is not large. The decentralized industry that can truly form business mainly includes infrastructure like chains, oracles, data retrieval, and some DeFi projects. Taking BTC, the largest in scale, as an example, its annual output does not exceed 400,000, and the underlying value risk to hedge is less than 10 billion. Without a robust on-chain workforce, it is actually difficult to obtain sufficient industrial demand. This leads to the absence of a rigid demand decentralized options market.

On-chain options users should lean more towards programming rather than manual interaction. The usage threshold for on-chain options is low for programs but high for individuals. The design of on-chain options buying and selling products should increase interaction between smart contracts and reduce manual account interactions with smart contracts.

Secondly, there are differences in compliance preferences. Centralized options have complete risk control and compliance systems that can accommodate various legally defined qualified investors, while decentralized options have imperfect compliance and risk control systems. They engage in legally permissible businesses and attract individuals with low compliance requirements.

Thirdly, decentralized options allow for more option underlyings. The volatility of digital assets is significant, leading to high option pricing costs. Many digital assets are not subject to legal regulation, have high concentration of holdings, and the risks of price manipulation are difficult to estimate. Therefore, centralized exchanges find it hard to expand the business of option underlyings for digital assets. Except for some stablecoins and ETH, BTC, it is challenging to develop suitable option underlyings. Some decentralized exchanges have designed the concept of "private pools," allowing market makers to independently bear certain option exercise risks, enabling decentralized options markets to compete with centralized options markets.

Fourthly, due to the high difficulty of product usage, high thresholds, and significant compliance risks, even though many projects have adopted token airdrops, trading rewards, and other marketing strategies, participation funds and product users remain scarce. Inactive products face liquidity challenges. Decentralized exchanges reduce the range of selectable exercise prices and times for options. Opyn even created perpetual options, further concentrating liquidity.

Fifthly, although decentralized exchanges have achieved no default risk through smart contracts, this no-default under smart contracts requires the asset value controlled by the contract to exceed the loss risks faced by the options. The collateral in the contract is in an over-collateralized state. The overall capital utilization efficiency is generally low.

Bottlenecks in the Development of the Decentralized Options Market

The decentralized options market is an exciting new asset class but is still in its early stages of development. Therefore, many bottlenecks need to be addressed before it can fully realize its potential.

High Costs

One of the biggest bottlenecks is the high cost of using the decentralized options market. This is due to various factors, including operational fees, risk costs, and educational costs.

Operational fees are the costs users must pay to miners to process transactions on the blockchain. On popular blockchains like Ethereum, gas fees can be particularly high, and some projects may require oracle pricing. This can make the decentralized options market prohibitively expensive for some users.

Risk costs are another factor contributing to the high costs of using the decentralized options market. The decentralized options market is a relatively new industry, lacking sufficient historical practice compared to traditional options markets. Technically and design-wise, we cannot inductively prove that this system is sufficiently safe. The potential risk costs present a gap for massive adoption.

Finally, educational costs are another factor leading to the high costs of using the decentralized options market. The decentralized options market is complex and difficult to understand. Users need to fully grasp how they work to use them effectively. This can be a barrier to entry for some users.

Immature Market

Another bottleneck is the immaturity of the decentralized options market. This not only means greater risks compared to traditional options markets but also, as mentioned earlier, the lack of stable and necessary demand. This can make it difficult to find buyers and sellers for options, leading to insufficient liquidity. Without sufficient liquidity, it is necessary to gather liquidity by reducing participants' choices, which can further complicate trading.

The immaturity of the market is also reflected in the uses of options. Traditional options often serve multiple functions. In the decentralized options market, there is no demand for options based on compliance requirements (traditional institutions have a habit of using derivatives to navigate regulations); there are no projects seen financing through options or using options for incentives; and the design of options based on business risk hedging is not as mature as in traditional financial markets.

Low Capital Efficiency

Another bottleneck is the low capital utilization rate of option margins. In traditional financial markets, platforms allow users to have a certain margin risk exposure. This is based on centralized credit. Platforms hold user information and can pursue users in the event of a derivative liquidation. However, in the decentralized options market, users are not only in a semi-anonymous state, but platforms also lack the ability to pursue. Once the margin cannot cover the losses from trading, the losses must be borne by the platform.

In centralized trading platforms, all of a user's assets are managed by the platform, and other non-monetary assets can also serve as collateral for credit. In contrast, current decentralized platforms require the ownership of assets to be transferred before they can become collateral.

Since decentralized platforms cannot pursue users for excessive losses, they must reduce liquidation risks. Increasing the margin ratio or raising the risk costs of options is a reluctant measure.

Immature Infrastructure

The decentralized options market also relies on immature infrastructure, such as wallets and exchanges. These infrastructures can be complex and difficult to use, and they are not always reliable. For example, saving private keys can be challenging, and wallets can sometimes be hacked. Additionally, the trading interfaces of decentralized options exchanges may be cumbersome and difficult to use, lacking sufficient analytical tools and software.

Despite these bottlenecks, significant progress has been made in developing the decentralized options market. Many new projects are working to address these challenges, and the market is growing rapidly. As the market matures, we can expect to see bottlenecks resolved, making the decentralized options market more accessible and user-friendly.

Landscape of the Decentralized Options Track

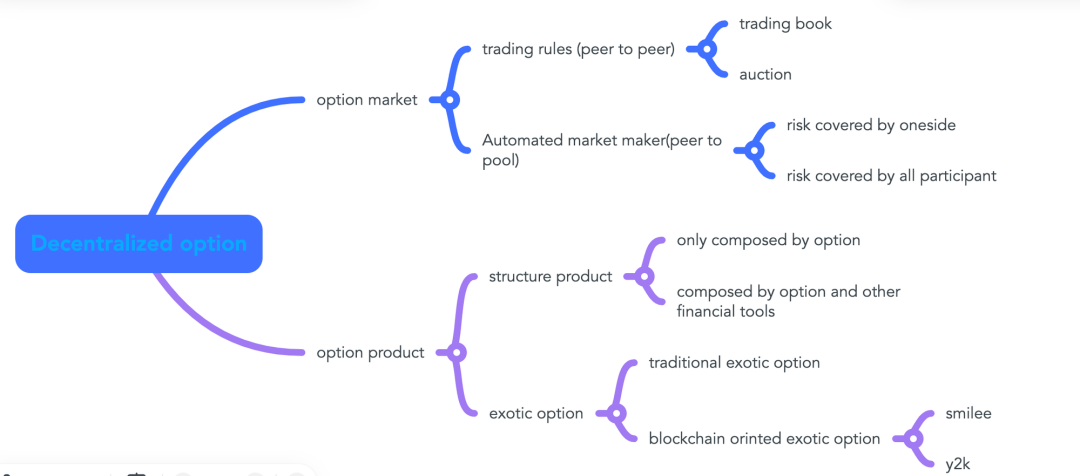

The decentralized options track can be divided into options issuance, options market-making, and structured products under options based on the problems that need to be solved and methods.

Decentralized options can be categorized differently based on various dimensions.

From the dimension of option price formation, they can be divided into the "pool-to-pool" model with algorithmic centralized pricing and the "peer-to-peer" model with independent pricing from counterparties. The "pool-to-pool" model can be further divided into public pools and private pools. Public pools maintain consistent algorithmic pricing, while private pools can be understood as each private pool having its own set of algorithmic pricing, with market pricing being the sum of private pools. The "peer-to-peer" model may also differ based on trading processes, which can be order book-based or auction-based.

If categorized by option types, it includes standard options and exotic options. To address the issue of insufficient on-chain liquidity, on-chain options have produced a type of perpetual option. In perpetual options, there is no final exercise deadline. The downside is that this type of option becomes insensitive to time value.

Based on the scale of margins, some projects only allow full margin, while others permit partial margins. Projects with partial margins enhance the flexibility of option issuance. In my view, options with insufficient margins resemble option spread strategies. The design of cross-margin increases capital utilization. For non-full margin options, smart contracts will arrange for liquidation steps. Even if full repayment is not possible, the profit and loss situations of each participant are clear under known conditions.

Automated Classic Options Market-Making

Asset pricing has always been at the core of the financial industry. How to price options and form pricing mechanisms is the crown of on-chain options models. Pricing that approaches equilibrium prices can stimulate trading, thereby improving capital utilization and yielding richer returns. The market-making mechanism addresses the pricing issue. Years of practice have shown that exchanges and market makers are profitable businesses, naturally attracting capital and projects.

Automated market makers are an innovation in the DeFi industry. From the initial spot market to the continuously evolving futures market, even the options market has seen market-making algorithms emerge. Among them, Lyra stands out.

Lyra

Lyra's options market-making draws on the successful experiences of DeFi predecessors like Synthetix and GMX, establishing a capital pool as the counterparty for all options traders, absorbing potential risks with collective funds. Lyra splits the risks of options into Delta risk, which arises from changes in the underlying asset affecting option prices, and Vega risk, which arises from changes in the underlying asset's volatility affecting option prices. Delta risk is hedged in the futures pool, while Vega risk is absorbed by the capital pool, corresponding to fees charged. In Lyra's design, an option quote ultimately becomes the basic pricing of the BS model plus risk margin adjustments. The risk margin adjustments change with the net risk exposure of the capital pool.

Lyra's market-making approach effectively addresses the pricing of options for highly liquid assets. Highly liquid assets are at the forefront of the market, dominating the mainstream. The market capitalization of BTC alone has already surpassed 75% of the total market capitalization of fungible tokens. Whoever can dominate the leading market can control the entire options market. The downside, however, is that these major underlyings have long been heavily marked by centralized exchanges. The drawbacks of centralized risks only become apparent in risky situations, and long-term usage habits lead to reliance on the convenience and practicality of centralized exchanges.

Deri

Deri is also a comprehensive financial trading platform. The platform acts as a market maker. Pricing adopts the DPMM model, which, in short, is similar to Lyra's approach, first using the BS model to create a standard quote for an option, then introducing the platform's positions as adjustment parameters. This guides net positions to approach zero.

Optix

Optix's design leans towards a structure of market maker + trader, adopting independent capital that bears its own profits and losses, allowing for equal competition. The Optix platform allows for multiple capital pools, each associated with a set of oracles responsible for independently determining the pricing of the products they cover. An asset pool can serve as collateral for multiple products. In this way, Optix hands over the pricing power of products to independently strategized asset pools, with each asset pool acting as a market maker. Optix resembles an asset management tool for option collateral, addressing the management of option fees and payouts.

Because asset pools bear their own profits and losses, Optix can tolerate higher risks. It accepts not only highly decentralized and liquid underlying assets like BTC and ETH but also other ERC20 assets. If Lyra's pricing activates liquidity in the mainstream market through mathematics, then Optix activates trading in the long-tail market through game theory. Pricing mainstream assets is crucial, but providing quotes for long-tail assets is also essential for options to fulfill their functions.

Observing the underlyings of Optix, many small tokens still struggle to make it onto the platform, limiting the expansion of underlyings. The reason lies in the lack of motivation to market-make options for small tokens.

Premia

Premia's design philosophy treats all traders equally. It adopts an order book format for quoting and trading. It provides automated market-making algorithms for ordinary investors without market-making experience and specialized asset pool services for institutional and professional investors.

I believe that accurate quotes from market makers are a necessary condition for efficiently creating liquidity. Therefore, the pricing algorithm of automated market makers is its core asset. Although Optix and Premia have centralized components, such as pricing data from oracles potentially coming from private sources, we cannot prove that a mixed system cannot produce efficient liquidity.

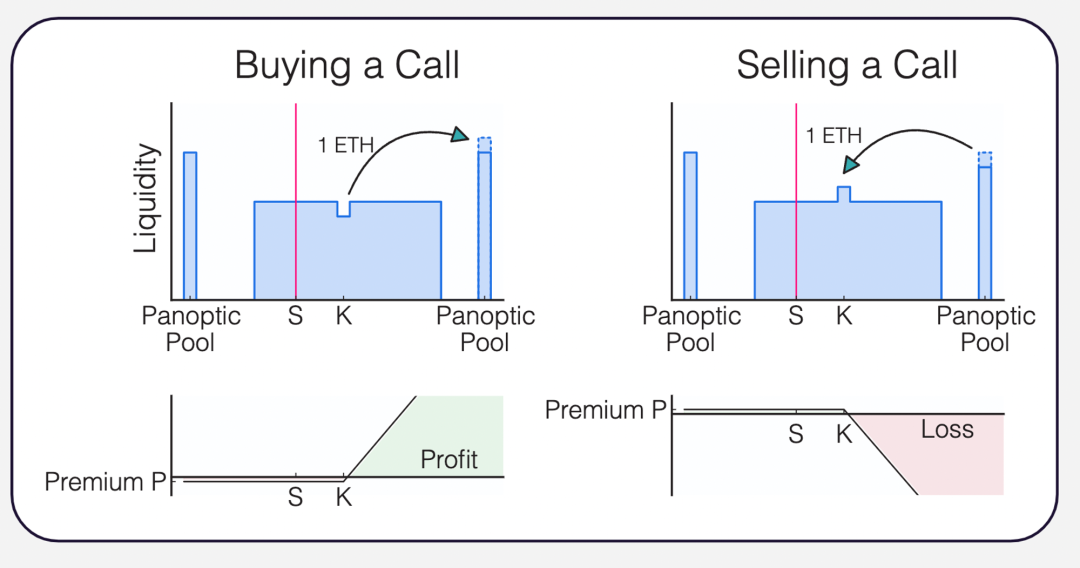

Panopic

Panopic employs a strategy of using LPs on Uniswap as a replica of options. To create options, liquidity is provided to the public pool; to hold options, liquidity is withdrawn from the public pool.

Panopic also uses an insufficient margin system. Unlike closed centralized options, one does not know if there is a liquidation risk until the clearing occurs. Traders can read on-chain data combined with clearing plans to help them assess counterparty risks. In other words, option prices can better incorporate counterparty risks. Related practices have just begun, so let the bullets fly for a while.

Hegic

Founded in 2020, Hegic is considered a pioneer in decentralized options. Unlike later entrants, Hegic was born in an era of very high on-chain costs and ideologically difficult compromises with centralization. Therefore, in its pricing model, Hegic simplifies the complex option prices related to time, exercise price, and volatility to a model that only relates to market prices and interest rates, with longer exercise periods leading to higher interest rates. Undoubtedly, this design has significant limitations. When volatility is high, the fair price of options should be higher than Hegic's quotes; conversely, when volatility is low, the opposite is true. The option quotes do not reflect supply and demand.

In terms of risk dilution, Hegic pits the buyers and sellers of options against each other, with losses from options needing to be borne entirely by the providers of the capital pool.

Aevo

Aevo replicates the business of traditional centralized options exchanges using layer 2 networks. Adhering to the business logic of performing complex calculations off-chain and recording the final results on-chain, Aevo is a hybrid exchange. As a layer 2 network + order book-style options exchange, Aevo features a cross-margin function, and its clearing process is similar to that of centralized exchanges. It prioritizes clearing assets and liquidates the positions of profitable parties when margins are insufficient, while the remaining portion is covered by the platform's insurance fund. It is important to note that Aevo is also a hybrid business platform, offering various services beyond options, including perpetual futures and lending. On top of its basic services, Aevo has also built wealth management products, forming a financial matrix similar to Lyra.

Over the past three years, we have seen the decentralized pricing system become increasingly sophisticated and efficient. With the improvement of infrastructure, the on-chain options track has gradually matured. Like the vast majority of on-chain projects today, the endpoint for decentralized projects is not merely to match centralized projects but to achieve what centralized projects cannot in certain aspects. We are nearly able to achieve the same level of quality; we need to find the demands that centralized projects cannot meet.

Structured Products

With the development of the decentralized options market, decentralized structured products based on options are also emerging rapidly. However, the current innovations have little to do with decentralized attributes or blockchain architecture. The products themselves have similar shadow products in centralized options tools.

Structured products use smart contracts or other programs to replace manual interactions with decentralized options.

We know that options serve an important value as hedging tools. Just like buying insurance, users with hedging needs are willing to pay a premium for risk coverage. However, the premise is that the design of option products can address the actual risks faced. For example, if someone participates in an AMM, estimating an annual return of 20%, and hedges against unilateral asset price fluctuations through futures, there are still unhedged losses. If spending some money can hedge against unhedged losses, allowing the remaining annual return to exceed that of U.S. Treasury bonds, then this is a risk-free arbitrage mechanism. This mechanism can provide a continuous profit stream for option sellers, rather than a zero-sum game.

Ribbon Finance and Theanuts Finance are both focused on raising funds for a single covered call + put selling strategy, benchmarking against yield-enhancing products from centralized exchanges. By selling options, they allow funds to obtain sustained positive cash flow over the long term. Since they are selling short-term out-of-the-money options, the chances of exercise are low. As long as the design of the options is well controlled, it is possible to achieve sustained profitability in the short term. The reality is that Ribbon Finance has lost its pricing power for options through auction pricing by external institutions, and many structured products are currently in a loss state.

Cega offers structured wealth management products, where if the underlying asset portfolio does not touch extreme prices (a 50% drop) within 27 days, the funds in the asset pool will grow; otherwise, they will be paid to the counterparty. Essentially, this is a bond + out-of-the-money put option.

BracketX provides a short-term (2-day) product that bets on price ranges, determining whether the underlying asset triggers the boundaries of the price channel within the agreed time. Whether it triggers or not decides who pays whom. This product is a simple asset combination of options. This approach increases the tools for speculation and reduces the operational difficulty of speculation.

There are also platforms like Hegic that provide a front-end platform for one-click deployment of corresponding option combination strategies.

The emergence of numerous structured products highlights the trustless and non-regulatory characteristics of on-chain derivatives. It breaks monopolies and lowers the barriers to issuing option derivatives. However, we can easily find that the design of structured products themselves has no relation to decentralization or blockchain. We can also see twin-like wealth management products in centralized exchanges. The intelligence of structured products still needs to be strengthened.

Exotic Option Design

In terms of options issuance, general options trading platforms come with options issuance. It is worth noting that options trading platforms focus on head traffic, which may not effectively cover niche markets like exotic options, leading to the emergence of a batch of exotic options projects.

Exotic options largely serve the on-chain ecosystem, with Y2K Finance being the most prominent. It primarily establishes binary options betting on stablecoin de-pegging, determining option pricing based on the distribution of chips on both ends of the option. The downside of Y2K Finance is that its yield is not clear; it continuously adjusts option quotes based on the size of bets from buyers and sellers. For investors, this means participating in a gamble with unclear odds.

Additionally, some projects competing for major assets have created perpetual options to pool liquidity and reduce the complexity of options. The birth of perpetual options signifies a more aggressive exploration of exercise times. If American options extend the exercise window of European options, perpetual options simply demolish the entire wall, allowing exercise at any time. Correspondingly, perpetual options sacrifice sensitivity to time risk. People are no longer suited to speculate on the volatility based on the time value of options using perpetual options. Perpetual options are a brand-new product; although they offer greater freedom and avoid direct competition with centralized exchanges, the auxiliary pricing tools become scarce, and the learning costs are high. Currently, the onboarding effect is not ideal. Without sufficient incentives, users lack motivation to learn. Among perpetual options projects, Opyn and Deri are relatively well-known. Opyn is the pioneer of perpetual options, backed by Paradigm, which helps it gain an early lead. Deri expands into perpetual options based on its perpetual futures business, adopting a strategy similar to Synthetix to provide "comprehensive" financial services.

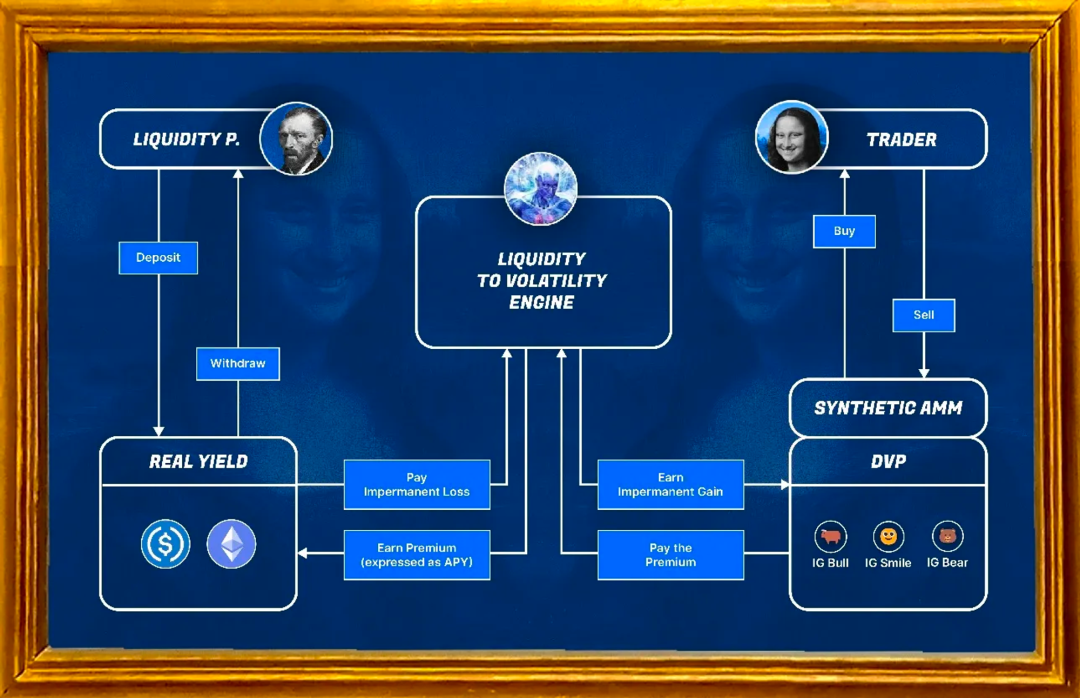

Smilee Finance has been developing products aimed at unhedged loss risks, hoping to price and trade unhedged risks through its products. The product design employs the perpetual options model, using the BS model to measure the price of perpetual options. For the product, the entire smile curve is segmented into bullish, bearish, and full segments. When selecting bullish or bearish options, leverage can be increased.

Opyn leverages options to add tools for risk hedging. In contrast to Smilee, which directly targets unhedged losses, Opyn aims to fit unhedged losses using Squeeth + traditional financial tools. Squeeth returns are curved. Like other newly created financial tools, Squeeth faces high learning costs and promotional difficulties.

Ecological Niche of Decentralized Options

The decentralized options track lacks user presence. For ecosystems, they either pursue user traffic or cash flow. User traffic is the specialty of social and gaming, enhanced by various wallets to improve user experience. Traditional options users are high-net-worth individuals, comprising only about 1% of spot users. Therefore, options cannot be used as a tool to attract users.

Cash flow comes from either trading or lending. In trading, decentralized perpetual options have leveraged contracts up to 200 times, leaving no room for options to leverage.

So, do options have no functions to attract ecosystems? Not at all.

As mentioned earlier, the uniqueness of options lies in their pricing of volatility and risk management. The current blockchain market is still in its infancy and has not evolved to a detailed control of risks.

As decentralized options approach the capital efficiency of centralized options platforms, in today's accelerating integration of traditional capital and blockchain, RWA is gradually transitioning from ideal to reality. With changes in investor composition, capital preferences will shift from high-risk, high-return to low-risk, moderate-return. Perhaps now is a critical time for change.

We are currently in the era of Layer 2 battles, where various infrastructures strive to stand out based on traditional successful applications, which is increasingly difficult. Controlling risks and forming financial systems with different risk preferences may be the key to winning the DeFi battle in the Layer 2 war. Who still remembers UST's contribution to Luna? Not all investors enjoy wild fluctuations.

Spot has succeeded, and futures have also succeeded. Is the spring of options far away?

Conclusion

After the DeFi summer, the decentralized derivatives track has developed rapidly, forming a series of projects centered around classic options with BTC and ETH as core underlyings, alongside various ERC20 options and exotic options. Projects lack interconnections and have not discovered options trading aggregators. Currently, there are also few opportunities for collaboration with other blockchain industries. Some projects aim to bridge liquidity between options and spot, as well as between options and futures. In an era of high traffic costs, operating a DeFi matrix will significantly reduce operational costs.

In terms of options pricing, I believe the future of decentralized options should be in the pool model, the automated market maker model, and a model where platforms and individuals bet against each other, with all participants jointly bearing extreme risks. The structured products formed by options are still evolving, and creating low-risk, moderate-return on-chain products is the key to the success of structured products.

In the use of decentralized options, there has yet to be a prominent on-chain characteristic. On-chain options players are far fewer than those in centralized exchanges. Without significant dividends, players lack motivation to learn the decentralized system. The on-chain industry has not formed a scale, nor is there a clear need for risk management. Additionally, traditional functions like options financing and options incentives have not manifested in on-chain businesses: this is one of the signs that DAOs are still in their infancy.

Compared to decentralized spot exchanges that allow low-cost on-chain trading of tokens, decentralized futures exchanges enable users to form leverage of up to hundreds of times directly on-chain without borrowing. Options do not hold a core demand position in the current layer 2 competition. Layer-level competition revolves around capital flow and user flow. How to issue credit is a more crucial function at present. However, regarding risk tools—options—we should not underestimate their value. Options provide us with the opportunity to redefine the attributes of on-chain assets.

References:

https://medium.com/smilee-finance/pt-1-introducing-smilee-v1-69-synthetic-amm-directional-impermanent-gain-redacted-dca97cef13b1

https://medium.com/smilee-finance/smilee-the-first-primitive-for-decentralized-volatility-products-dvps-9a7584b13d42#ad2f

https://www.theblockbeats.info/news/32903?search=1

https://www.theblockbeats.info/news/34380?search=1

https://medium.com/@polygontech/best-practices-for-building-decentralized-option-vaults-5ff254687ab2

Lyra: Precise Pricing of On-Chain Options:

https://www.theblockbeats.info/news/24899?search=1